You’re probably reading this because you want to see your financial life improve—likely because you’re trying to move toward financial independence.

Good on you, my friend! A great way to get better at something is to start tracking it.

Let’s talk about calculating and tracking your net worth.

How to Calculate Your Net Worth

Simply put, your personal net worth is equal to your assets (the things you own) minus your liabilities (i.e., debts).

The trick to getting an accurate number is to carefully examine what you have and what you owe, inclusive of all accounts—and, remember, it’s a snapshot in time.

Don’t just think to yourself, “Well, I have two thousand bucks in my savings account, so my net worth must be two thousand dollars.” There is much more to it than that.

Assets

For instance, your assets might be:

- cash in checking and savings

- investments

- real estate

- cars

- jewelry

- collectibles

Liabilities

Your liabilities might be:

- your mortgage

- credit card balances

- student loans

These are some of the more common elements. You might have more or less and/or different items.

See my net worth spreadsheet at the bottom of this post to get an idea of the things you can track. For a quick and easy way, I suggest plugging your numbers into Empower for free to quickly see your own net worth.

How is the net worth actually calculated? It’s simple, really.

All you have to do is add up the value or balances of each category (assets and liabilities) and simply subtract your liabilities from your assets.

Ideally, this will equal a positive number, but, it’s okay if it doesn’t initially. Most people start out their journey in the negative (I sure did).

It may seem a little weird to reduce your entire financial existence into a mere number, and it can be truly bizarre to actually see the number once all the calculations are complete.

Keep in mind it’s just a number which indicates how much your assets are worth and really has nothing to do with you as a person.

Why You Should Know Your Net Worth and Track It

It’s always good to take a moment to understand why you want to do something.

Knowing your net worth will:

- Bring clarity to your financial life. Instead of living in ignorance, you will see the truth. Knowledge is power!

- Motivate you to see the net worth number improve. I promise you, your mind will instantly be drawn to how you can increase your assets and decrease your liabilities. It’s natural. Don’t turn from this feeling. Embrace it.

- Allow you to set a specific goal towards improving your net worth. If you don’t know where you are, it’s hard to know how to get to where you want to be.

What Should Your Net Worth Be?

As much as possible!!! Okay, I’m joking (but, not really).

Try not to think in terms of a static number. Don’t get caught up in comparisons, either.

Simply put, your net worth should be moving in a positive direction.

Once you get it going in a positive direction and set goals around it, you’ve found the sweet spot for understanding this simple little calculation.

Of course, at some point, you might want to set a goal of financial independence (the point in which you are able to live off of the income produced by your assets).

In this case, your net worth needs to be roughly 25 times your annual expenses, or enough so you can withdraw 4% (the Trinity study’s safe withdrawal rate) of your assets to live on each year (e.g. $40k on $1M). If that’s your goal, get crackin’.

It’s hard not to compare though.

How Do You Track Your Net Worth?

I recommend tracking your net worth using Empower. It’s simple, automated, and free.

Manual tracking more your thing? My wife and I have used a few spreadsheets to track our net worth through the years.

Initially we used this personal financial statement template. That was sort of an all-in-one sheet.

Then, I wanted to have a sheet specifically for net worth, so we switched to using a simple Excel spreadsheet (see below). You don’t have to use Excel though.

There are plenty of online-based calculators out there which will help you get to your net worth, and keep it up to date for you every month.

Again, the one we use now is Empower.

If your net worth isn’t a positive number or isn’t as high as you’d like it to be, set a goal. Put it on paper.

Make both a short-term and a long-term goal. Decide how long, based on your ability to save or pay off debt, it should take you to reach your goals.

My Net Worth From 10 Years Ago

Several years ago now, fresh off of my first FinCon where I was inspired by “coming out” to all of my money nerd friends I began to share my net worth monthly on the blog.

Initially, I found the process fun and revealing. Then I realized after 6 months no one was commenting anymore on the updates (so it felt useless and uninspired) and I felt once again a little exposed by sharing such detail.

By this time I was no longer an anonymous blogger and so I stopped sharing the specifics publicly.

You can still piece together my net worth by going through my annual savings goals post and my annual rental property analysis.

But those don’t even include my business net worth, so it’s still off. Still, I suppose if you are desperate to know you can hunt around and find it.

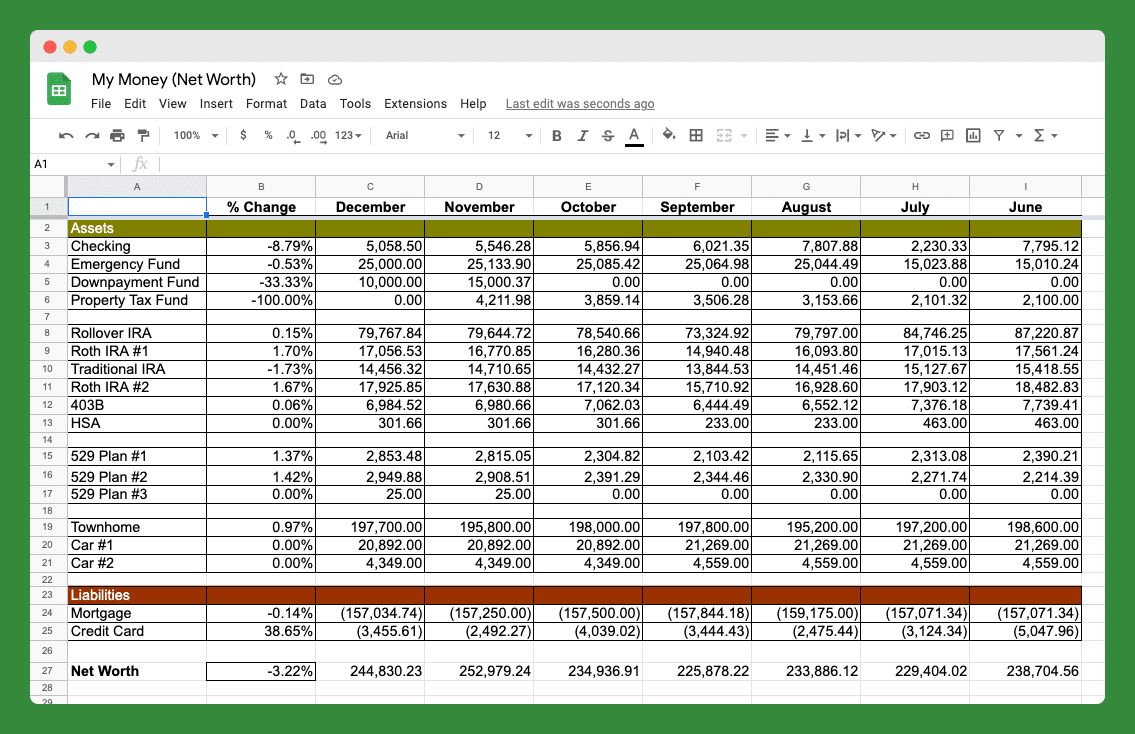

Here’s the Spreadsheet I used previously to track my net worth:

Below you’ll find the commentary from five months’ worth of data (don’t ask me where the July and September commentary are). To see it, click show

June Net Worth

Below is the latest snapshot of our personal net worth. I share these numbers so that you will encourage me and keep me accountable. Also, I share so that you can see how the information on this blog ties into my actual strategies for building wealth (aka security and freedom).

This personal net worth statement includes Mrs. PT’s stuff, but it doesn’t include my business data. I will attempt to update this each month and thus, let you guys in on my progress. After all, net worth isn’t worth much on its own (for all you know, I could have inherited this money). Thus, net worth should primarily be used to gauge if you are moving in the right direction.

Check back next month to see how I’m doing.

(notes to explain some of the accounts)

Checking – Nothing too exciting here. We do most of our spending using our Chase Freedom cash back credit card. The way we have our bank accounts set up, the credit card is paid off automatically, in-full each month from this checking account. We also pay a few small bills directly from this account. My main goal with this account is to make sure there is enough money here to cover the credit card bill in full. This account is held right now with Capital One 360.

Emergency Fund – I’m a big fan of keeping emergency cash-on-hand. It must be FDIC insured and liquid. It’s a bonus if this money can earn a bit of interest. That’s pretty hard to come by these days. $15K is not enough of an emergency fund for my risk tolerance. I’d like this account to be around $30K by the end of the year. This account is held right now with Capital One 360.

Property Taxes – We do not have the mortgage company escrowing our property taxes for us. We pay them ourselves in December or January, depending on our tax strategy. The tax rates are pretty high in Texas since we have no State income tax. I put around $350 into this account each month.

Rollover IRA – This is my old 401K. After I quit, I moved it here. It’s sitting in a target-date fund now with Vanguard. I won’t be contributing to it. My efforts will be on my Roth IRA and a possible SEP IRA I want to set up.

Roth IRAs – We opened these Roth IRAs back in the Spring of 2009 and have made the maximum contributions to them in tax years 2008, 2010, and half the limit in 2009. Right now we have an automatic contribution of $100 per month going into these accounts. It’s not much, but it’s something, and I’ll let me business determine if we’re able to true them up to the maximum at the end of the year.

Traditional IRA – This is my oldest retirement account. I’ve had it since 2001. I’m not sure what I want to do with it now. I do like having it as an option though.

403B – Mrs. PT used to be a teacher. A great one, actually. Anyway, she saved up a bit using this 403B (it’s just like a 401K) and hasn’t contributed to it since she quit and we went to one income. She needs to roll this over to Vanguard. She has the Rollover IRA setup, she just is having trouble getting the funds transferred.

HSA – We just drained our health savings account on $6,000 worth of baby delivery related medical expenses. I will need to bulk it up towards the end of the year.

529 Plans – We have one for each of our girls. We opened them up with Ohio’s CollegeAdvantage plan. We contribute $25 a month to each plan, and we throw the occasional “found money” or gift money in there. We also have some generous grandparents to help fund them.

Townhome – We’ve owned this bad boy since 2007. We purchased it at the height of the market, for about $10K more than Zillow is appraising it for now. I suspect that this will be one of the most in-flux accounts on this list. We live in a new neighborhood and Zillow has historically been all over the map with regard to our home’s value. We will probably add some more real estate in the new year and will keep this one as a rental investment.

Cars – These are estimates from Edmunds.com (trade-in value). We actually just paid off car #1 early since we needed to free up some income for the home refinance we are doing. We are considering selling car #1 and going to one car for a while. This will free up some cash to help us get to our next home down payment quicker.

Mortgage – We are currently in the process of closing on a refinance with the folks at Quicken Loans. This will enable us to drop our rate from 2007 levels and possibly rent out the home in the future and be able to “cash flow” it. Right now we have no plans to aggressively pay off our mortgage.

Credit Card – This is our Chase Freedom card. We use it as much as possible so that we can rack up cash back reward points. We pay it off in full each month. In June we spent more than the usual.

[note about debt] We weren’t always “debt free, except the mortgage.” Over the years we’ve made a big effort to pay off our high-interest car loans and student loans. Check the archives for those older debt updates.

I’m tempted to close comments on this first net worth post because there are really no changes to discuss. However, I realize you might have some feedback or questions about how we have everything structured, so fire away in the comments below…

August Net Worth

Another month has come and gone. Now it’s time to review the personal net worth to see how my finances are progressing. As you’ll see, the markets had another negative effect on my numbers. But my cash accounts saw some improvement mainly due to business income being strong over the late Spring and Summer months. The numbers will also reflect the completion of our refinance. Let’s take a look…

Checking (250%) – If you recall, last month I hadn’t quite made my business income transfer by the end of the month. Thus, numbers were down. As expected, I made sure to transfer funds before the end of the month and my checking account is back to normal levels. We’ll use these funds to pay off the credit card (in full), pay our new mortgage payment of $842, and a few other bills (water and electric) which we have to pay with our checking account.

Emergency Fund (67%) – Our emergency fund is now more than fully funded. As I said in the intro, business income was strong this Summer and we had the funds to get this account up to speed. We spend around $3,500 each month, so $25,000 is a little over 6 months. Truthfully, Mrs. PT and I also look at this account as a partial down payment fund. We’ve discussed it and we would like to at least leave $15,000 in this account when we decide to buy a new home and rent out our current place. In the coming months, I may establish a true down payment account with Capital One 360 so that we can have a dedicated home for our goal. Another factor involved here is that we are going to sell our Car #1 soon, and temporarily become a 1 car family. This would instantly give us at least $20,000 to beef up the emergency fund or down payment fund.

Mortgage (1.3%) – You’re probably wondering how a mortgage can increase. Well, we refinanced and Quicken Loans used the credit report value of the mortgage to set up the loan. They didn’t use the current bank pay off amount for some reason. Regardless, we received a refund check from our old lender, Bank of America, for $1,135. This was deposited into our checking account and will be used to make an extra principal payment when our first mortgage payment under the new lender (Wells Fargo) become due this month.

I’m not going to even comment on the retirement accounts this month. Just another down month to stomach. These accounts are all going to be used 15 years or more from now so we have aggressive allocations and will ride the short-term ups and downs.

Credit card usage was down again. That’s nice to see. In the future, I may show you the details of our monthly spending so you can see what goes into this.

Any comments or questions? I welcome them in the comments below.

October Net Worth

The big thing you’ll notice about this month’s net worth update is the increase across all equity (stocks) related accounts across the board. Net worth can rise and fall pretty quickly if you’ve got a significant portion of your financial portfolio in stocks like me. I’m young, I don’t mind it. The previous three months have been pretty tough (saw negative returns) so this month is a welcomed change, with all accounts rising an average of 7%.

Property Taxes – As you know, we pay our own property taxes (we don’t escrow) and so we have to save this ourselves. We create multiple savings accounts with Capital One 360 and each month I manually transfer $350 over to this account. I just received our two property tax statements (one for the school district and the other for the county and city) and the total is around $4,200. So, the November transfer should get us to where we need to be for the year. Our property tax statements are showing home value numbers that are about $7K higher than what Zillow.com shows (the number I use in my net worth calculation), so I may consider appealing my property taxes to get them to the correct number.

Cars – This month, since it’s a new quarter, I went to Edmunds.com and recalculated the value of our cars. If you want to do this for your own cars you should first navigate to Edmunds.com, then:

- Click the “Used Cars” Tab

- Find the “Appraise a Used Car” Box

- Select the Make, Model, Year, and Zip Code

- Click “Appraise It”

- Click the “Appraise Your Car” Button below the TMV Number

- Further Refine the Value by Mileage, Condition, Color, etc.

- Click Get Pricing Report and Choose Your Value: Trade-In, Private Sale, etc.

I use the trade-in number just to be conservative.

This month we are going to look further into selling our SUV (car #1) and using that cash towards a more solid down payment on our next house.

Note: If this is your first time seeing my net worth, you should know that the credit card balance gets paid off each month in full. The number in that row is the amount that’s on the bill for me to pay off.

So that does it for this month’s update. Nothing terribly exciting, but it’s always good to see the net worth rise.

November Net Worth

Alright, you net worth update junkies. Here it is. Time for another look behind the scenes at our finances.

Before we dig in, let me say that these last five months of updates have been great. The updates are spawning conversations with several readers and also helping Mrs. PT and me to zero-in on some of our financial goals. If you don’t review this stuff on a routine basis, you start to lose your intensity for better finances. With that, here are the numbers from November:

Key bullet points from this update:

- Property tax fund is fully funded. I’ll write the check before the end of the year.

- We started a down payment fund using funds transferred from the business account. Our goal is to have $60K by March this year.

- Grandparents gave us some extra funds for the girls’ 529 plans. Thanks, Mom and Dad!

- We also started a third 529 plan for future kid or for our own future education needs. Mrs. PT wasn’t big on this presumptuous move, but I couldn’t pass up the $50 bonus from CollegeAdvantage.com.

- Credit card spending* was down. Second lowest spending month in the previous six. Nice work.

So that’s it. I’m going to keep this one short and sweet, and let you ask questions or add on some suggestions.

*Paid off in full each month at the end of the cycle.

December Net Worth

Each month I review our personal net worth statement. This isn’t a perfect balance sheet, but I think it provides some solid info for you to gauge how we’re doing from month to month or year to year.

Net worth is down slightly from the previous month. But a lot more went on in cash that the numbers don’t necessarily reflect. Right up front I can say that retirement, college, and health savings didn’t see much action. No big contributions and no big market gains. Slow and steady, which is fine by me.

Key bullet points from this update:

Charity and Down Payment – We temporarily borrowed some funds from the down payment account. We used this to help us bolster our year-end charitable contribution. This year, one of our goals is to become a more consistent giver and not do these catch-up contributions. In reality, we should have at least had a charity savings account set aside so that we wouldn’t have to borrow from another account. It all comes out in the wash, but it’s better for clarity if you have the separate account. Instead of a separate account for this year though we’re just going to automatically give each month using Capital One 360 bill pay. Due to a strong December with the business, I expect us to have plenty of funds to replenish the down payment account and then some.

Car Repairs and Sales – Our credit card balance (which we pay in full each month) shows $1,000 more in spending this past month. This was due to the car repair on the Honda that I already shared with you guys. Hopefully, that major repair gets us another 50,000 miles (or 3 years) on the Honda before we have to invest much more. I love used cars. Speaking of cars, we’ve placed the SUV on the market for sale. We expect to sell that within the month and use the cash towards our down payment fund.

Property Taxes – Finally, you’ll notice that the property tax fund has been wiped out. We paid that in December (to get the tax deduction this year) and so we need to restart the contributions. We’re making a $350 deposit into that account each month. I usually do it manually at the end of the month. I think I’ll automate it for next year.

That’s the update for this month. I’m open to your comments or suggestions. Thanks!

Interestingly, I have my first networth update getting posted tomorrow! Six months out of training as a doc. I am encouraged by it and have some ideas where we can continue to build. Hoping to have a zero dollar net worth (started with NEGATIVE 308,000) in the next 12 months.

Tracking your networth is definitely a good exercise!

True. A clear vision of what our net worth should be will avoid unnecessary expenditures thereby affording us comfortable fallback with a sound state of mind and body.