How and Why to Start Building an Emergency Fund Now

I write a lot about the emergency fund (i.e. rainy day fund) on Part-Time Money.

Yet, it has occurred to me that I haven’t actually written a post on starting one. And with them being such an important part of your financial plan this is quite the oversight.

An emergency fund is money set aside to be used only in an emergency. It protects you against an unexpected loss of income or an unexpected expense. A good emergency fund can cover three to four months of expenses, is accessible, and makes money for you. Three great places to put your emergency fund are high-yield savings accounts, money market funds, and bonds.

What is an Emergency Fund

Wow, I said “emergency” a lot in that first paragraph. Sorry about that. Truth be told, I’ll likely say it often in the rest of this post so just bear with me.

I was first introduced to the concept of the emergency fund while listening to Dave Ramsey’s radio show. I mean, I knew about having savings, but I didn’t know to call it an emergency fund. So, thanks Dave!

I think calling it an emergency fund is a great name because it gives you a clearly defined goal for that money. Which can motivate you to start, and keep one.

My definition: An emergency fund is money you set aside to be used only in an emergency. It’s like a fire extinguisher for your personal finances.

The fund is usually made up of three to six months of your expenses and is typically held in a place separate from your normal spending account.

Why You Need an Emergency Fund

A good place to start this discussion is to decide why you might need one of these funds. The reasons basically break down into two main categories:

- You could have an unexpected loss of income (i.e. lose your job, get hurt or pregnant and can’t go to work for a while) OR

- You could have an unexpected expense (i.e. your car breaks down). Here’s how to budget for those.

Most people aren’t insured against every type of event that could happen. This means an emergency fund is an excellent choice for just about everybody.

If you need help building an emergency fund check out the 52-week money saving challenge. If you complete it you will save $1,378.

Other savings you may want to have which aren’t technically going to fall under your emergency fund account are things like:

- Major planned expenses. These are funds where you’re saving up for a big purchase, like a new car if the engine blows, or perhaps money for the house if (when) something like the A/C unit goes. In either case, you don’t know when it might happen, but it could happen any day – and not having a car or A/C unit could mean a pretty big headache.

- Avoiding debt. These are funds set aside strictly to help you float beyond the typical 6-month period, should it occur, where you can avoid taking on higher interest debt, like credit card debt. Think short-term savings or even a low interest credit line as a worst-case scenario.

Key Elements of a Good Emergency Fund

How do you know when you have a good emergency fund? Here are some the boxes that you’ll want your emergency fund to check.

Big Enough

Your fund should be big enough to help you through those events I just mentioned above. For example, if it would take you three months to find another job after a layoff, then plan on having an emergency fund of four months of your expenses.

What expenses? The quickest way to calculate this is to get online and view the last six months of data from your bank. Use that data to determine the total average monthly spending over the last six months.

Use that data to determine the total average monthly spending over the last six months. Multiply that average by 3, 4, 5, and 6 months. The other factors listed below are going to help you determine which of these numbers (3x, 4x, 5x, or 6x) to use as a basis for your emergency fund.

What feels comfortable for you?

Accessible, but Not Too Accessible

The fund should be kept somewhere where you can get to it in your time of emergency. But I tend to think it should be kept far enough away so that you can’t spend it on day-to-day spending. This means, don’t keep it in your safe, regular checking account, or the savings account attached to that checking account.

On the flip side don’t use a CD to hold your emergency savings either. CDs mature on a monthly basis at the earliest, so if you needed it right away, you’d likely pay a penalty for withdrawing your money early.

Of course, you could use several CDs and have them in a revolving maturity schedule. That way part of your money would become available every month. That’s still not flexible enough for me, though.

Making Money for You

Lastly, as a bonus, you’d like your emergency fund to be earning money for you.

No, you don’t want to invest your emergency fund money in the stock market. But there are several safe places to store your emergency fund that will still give you a decent return. In the next section, we’ll take a look at a few ways to make money from your emergency fund.

Related: The Best High Yield Online Savings Accounts

Separated and Automated

These are the two specific steps you need to take to actually save more of your money:

- Separate your savings account from your spending account

- Automate direct deposits into the savings account

The idea here is getting your emergency money automatically stored in a place where you aren’t as tempted to go and get it (unless it’s a real emergency).

Where Can You Keep an Emergency Fund?

The national average savings account rate is a dismal 0.09%, according to the FDIC. That means for every $10,000, you’ll earn a measly $9. That’s terrible!

But the good news is that you can earn a much higher return on your money if you’re willing to shop around. Here are three great places to consider keeping your emergency fund.

High-Yield Savings Accounts

In the last few years, online banks and fintech companies have used high-yield savings accounts as a way to attract new customers. Today, it’s easy to find accounts that will pay you 20 to 25 times the national average.

The rise of fintech high-yield cash accounts has pushed online banks to raise their rates too. Even some traditional brick-and-mortar banks have responded with higher rates. In fact, there are several banks that currently offer rates at or above 2.0%.

Just be aware that some banks have a minimum deposit requirement to get their highest APY. And you’ll want to keep an eye out for junk fees too.

Check out our favorite high yield savings accounts here.

Money Market Accounts

Money market accounts are similar to savings accounts in many regards. But one of the biggest differences is that are typically allowed to write checks and/or use a debit card to access your funds.

That can make the money in your money market account a bit more accessible than a savings account. It’s like a blend between a checking account and a savings account. And, in many ways, you get the best of both worlds. The downside? Many money market accounts require higher minimum deposits.

But if you’re able to meet the minimum deposit requirement, you can expect your interest rate to be near or higher than savings account rates. And all money market accounts are insured by the FDIC or the National Credit Union Administration.

Bonds

Finally, you could use your emergency funds to purchase bonds. This might seem like an unusual place to store an emergency fund. But bonds could be a better option than most think, especially if you buy the right kind.

When you buy a bond, you are lending your money to the buyer. In most cases, that buyer will be a corporation, the government, or a municipality. The bond issuer will then pledge to pay you a specific interest rate on the bond, in addition to repaying the principal at its maturity date.

The great part about bonds is that they provide a steady stream of income. Most of them make interest payouts twice a year. And some have an even more frequent payout schedule.

Can You Cash In Your Bonds At Any Time?

The biggest concern that many people have with bonds as a place for their emergency fund is accessibility. After all, many bonds have a maturity date of 30 years. Further, many are “non-redeemable,” which means that you can’t sell the bond back to the issuer before the maturity date.

However, most bonds can be sold on the secondary market. Bond rates tend to move in the opposite direction of general interest rates. So depending on how the interest climate has changed since you purchased your bond, you could sell it on the secondary market for less or more than you originally paid.

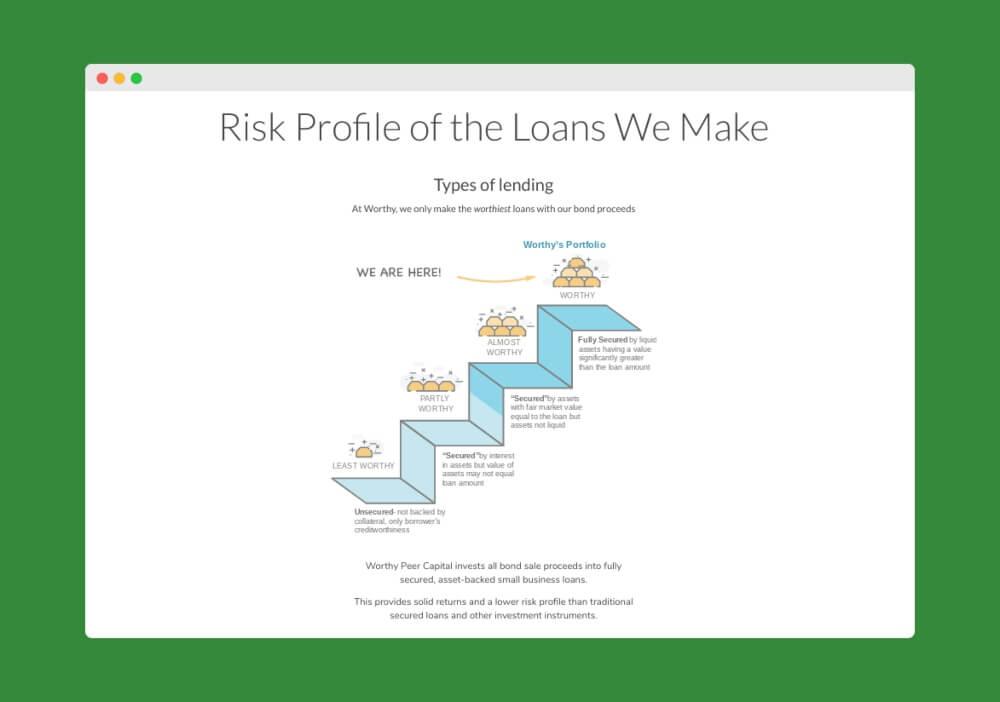

If having to sell a bond on the secondary market sounds like a hassle, that’s ok. There are companies out there that sell redeemable bonds with great interest rates. With that in mind, let’s take a look at Worthy Bonds, a trailblazer in the bonds space.

How to Earn a 5% Fixed Rate on Your Emergency Fund With Worthy Bonds

Worthy Bonds sells bonds that come with a 5% fixed-rate annual return. Yes, you read that right–5.0%–over 50 times the national savings account rate! Each bond costs only $10, so that’s all the money you need to get started.

Here’s how it works. Worthy takes the money that they receive from bond sales and invests it in “asset-backed” small business loans.

What that means is they only give money to companies that can secure the loans with collateral. That makes their investments less risky — which is why they’re comfortable offering the 5% rate on their bonds.

And since Worthy’s interest rate isn’t based on the Fed, it should be more stable. Worthy says that they have no intention of dropping rates any time soon. If anything, they hope to raise rates down the road.

Worthy Bonds come with 3-year maturity rates, but can be cashed out at any time. Their bonds pay interest daily and once you’ve reached $10 in interest, you can use the money to buy another bond if you’d like. That’s a pretty cool way to essentially earn compound interest on bonds.

Ready to earn 5% on your emergency fund? Here’s where you can get started.

Is Your Emergency Fund Big Enough?

The first thing I’d say is, if you have to ask, odds are it isn’t big enough. 😉 I know I’m not going to get away with that easy answer though. So what I will do is try and give you some points to think about to give you confidence in your emergency funds. After all, I’m not going to be there to bail you out.

Know the Rule of Thumb

Most money experts will tell you that you need anywhere from 3 to 6 months worth of expenses in liquid savings (i.e. cash). If you’re unsure of how to calculate that number, or if you did calculate it and it didn’t give you warm and fuzzy feelings, keep reading.

The reason the 3-6 rule is used is that for the typical family that’s enough to help you get by for a bit if you lose your job. It also ends up being enough to help you cover unexpected medical bills, car repairs, etc. for the insured.

If you want more on this specific topic, here’s our article about how much cash you should keep on hand.

Know Your Monthly Expenses

If you’re going to use the 3-6 months expenses rule, you’ll need to determine what your monthly expenses are.

Plan on spending the bare minimum during your downtime (i.e. cut the cable, don’t dine out as much, etc.). Go through your expenses and add up things you would have to pay even if you had no money coming in. Bills like rent/mortgage, electricity, insurance, minimum payments on debts, etc.

Next, think about expenses you’d still have, but perhaps at lower levels. For example, you’ll still need to put gas in your car, but likely not as much if you aren’t commuting. You’ll still need to buy food, but how much could you cut this cost if you had to? Are there other expenses you could reduce even if you can’t eliminate them?

Work to figure out the minimum spending you could maintain for a few months if you had to. Multiply that number by three, and the result is the amount you’d have to keep to maintain a three-month emergency fund. Do the same for a four, five, and six-month time frame.

Consider the odds of losing all your income at once. If you are married, how likely will you both lose your income at the same time? The chances are higher for this if you both work at the same company, or even in the same industry.

Use what feels comfortable and aim to be overly conservative.

Know Your Insurance Deductibles

A job loss isn’t the only type of emergency you could experience. Something could happen to your car, your house, or the health of someone in your family.

Do you know how much your insurance company is going to cover? Are there large deductibles on your plans?

Someone with a $5,000 deductible and a catastrophic health insurance plan is going to need a bigger emergency fund than someone with a premium plan who’s deductible is in the $100s.

Based on what you find out here, you may be in need of a 6-months e-fund vs the 3-month variety.

Know Where You’re Not Insured

If you actually go without insurance for some area of your life, consider what an emergency in that area would cost you. Bump your emergency fund up based on what you have uninsured. Those without health insurance should really have a huge emergency fund to help cover those unexpected medical bills.

Know Your Assets

If you’re a one-car family, unless you live in the city, you are highly dependent on that car (asset.) If that car needed a $2,500 repair, you’d have no choice but to spend the money to repair it. Likewise with your home. If your home is old and in need of constant repair, your emergency fund will need to trend higher to be able to cover those repairs.

Know Your Job Market

Are you the sole bread-winner in the family? How confident are you that you could get another job a few weeks or months after you’ve been laid off?

If you think it would take more than a few months, because (a) your industry is in bad shape, or (b) you aren’t that marketable (for whatever reason,) then consider bumping your e-fund number up above the 6-month mark. Keep going until you feel comfortable with the number.

So where does that put your emergency fund? I think if you start with the 3-month rule and then bump that up based on the risks in your personal situation, you can get pretty close to your actual required emergency fund.

When in doubt, just strive to make your emergency fund big enough to cover you for six months of income instead of expenses. That’s a very conservative number and would put you way ahead of most other savers.

How to Know If Your Emergency Fund is Too Big

Let’s take a quick look at emergency funds and examine how much is too much when it comes to cash savings.

As a disclaimer, everyone should look at their own unique situation and decide how much short-term emergency savings is necessary. For some, it may be $1,000, for others, $75,000. To get the conversation started I’ve come up with a list of reasons your emergency fund might just be too big:

1. It’s More than 6 Months Worth of Expenses

Most by now have heard this basic rule of thumb. Somewhere between 3 and 6 month’s worth of expenses is what you should probably aim for when saving cash for emergencies. So I ask you, if you have more than this, why? Why isn’t that money in an asset that will appreciate more for you, like real estate or other investments?

There may be some legitimate reasons though: You may have a history of illness in your family, or you may work in a specialized field with unemployment that is trending higher. If that’s your situation then the rule of thumb above may not apply. Save an amount in cash that will provide you the confidence you can make it through an illness or major career change. But also consider that most non-liquid assets could be transferred into liquid assets within six months, so more than that may never be a good idea.

2. It’s Not Insured

“The Federal Deposit Insurance Corporation (FDIC) preserves and promotes public confidence in the U.S. financial system by insuring deposits in banks and thrift institutions for at least $250,00.”

If you’ve got more than $250k in the bank (1) you are awesome, (2) the amount over $250k may not be insured. If you’re keeping this much cash because you think it’s safer, think again. You might as well have it in stocks with the potential to earn more.

I have a friend in the banking industry and he shared that you can have more than $250k insured by having multiple accounts in different family member’s names. So, if you’re dead set on keeping it in cash, then just make sure you know the rules and you’re protected.

3. You Have High-Interest Debt

Your emergency fund may be too big if you have high-interest debt, like credit cards or auto loans. Earning 3% on your cash savings isn’t doing you any good if you are paying 17% interest on consumer debt. Get rid of that debt and then begin building up an emergency fund.

Check out my post Credit Card Balance: Make Payments or Pay in Full? for more detailed information about the balance of savings and debt.

4. You Have No Retirement Savings

You have $75k cash in the bank but you haven’t been contributing to your company’s 401k or an IRA then you’re emergency fund is too big. Your 401k (or 403b or IRA) is a great tool for securing your retirement AND deferring your taxes.

On top of that, it most likely comes with a matching contribution. If so, then if you aren’t contributing to it then you are essentially telling your employer you don’t want all of your salary. Trade the cash in for some long-term security and get your match.

5. You have No Home Equity

Building up at least 20% equity in your home ASAP is a great idea. Getting to 20% will allow you to avoid private mortgage insurance (PMI) and will usually allow you to escrow your own property taxes and insurance. (Here’s how you can do that.)

Plus, it shows financial responsibility and commitment to your debt. Take your cash savings and pay down that mortgage till you’re at the 20% level, then begin building cash savings.

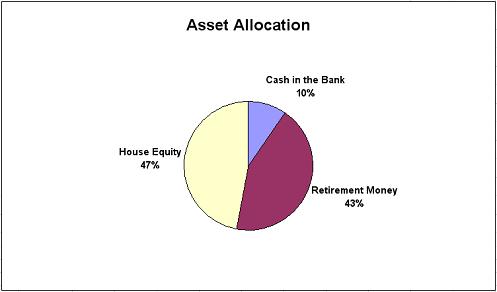

In the name of full disclosure, here’s our current allocation between home equity, retirement savings, and cash:

According to my stats on the Millionaire in the Making series, the average in cash savings is $38,569.76, while retirement and home equity averages are $180,434.75 and $210,635.42, respectively.

In my opinion, we should probably shoot to have a larger percentage in retirement money even though we line up with the future millionaires. What are your thoughts on our allocation?

How to Use Your Emergency Fund: A Real-Life Example

Part-Time Money staff writer Emily Guy Birken learned the value of an emergency fund when she got a call from her stepfather that her mother had gone into the hospital.

Her mom had an acute case of pneumonia and was put in a medically induced coma to help her heal.

Like many financially savvy young couples, Emily and her husband have an emergency fund with several months’ worth of living expenses. Technically, this fund is there in case their income dries up for any reason.

And because of that “technical” reason for this fund, Emily wondered how on earth she would pay for the plane ticket to Baltimore to see her mother in the hospital.

What is an “Emergency?”

Flying with only a few days’ notice is expensive and finding the money for the ticket in her budget was impossible. Eventually, Emily realized she was defining “emergency” too narrowly.

Yes, she and her husband had set the money aside for a loss-of-income emergency. But they may never have one of those.

They were having a bona fide family emergency and had plenty of money available in the emergency fund for a plane ticket and associated travel costs.

Just because this wasn’t exactly the reason they set aside money every paycheck didn’t mean they couldn’t use it.

When you have a true emergency, don’t get hung up on how you were planning to use your emergency fund. Take comfort because you have money to carry you through a rough patch and help you get back on your feet.

Final Thoughts

Life is a lot less predictable than you think. It’s important to do what you can to be ready for any surprises that come your way.

Keep the elements of a good emergency fund and your main goals in mind and you should have no trouble setting one up. Good luck.

Do you have an emergency fund? How have you used it before? Share in the comments.

Life is full of unexpected surprises. You don’t want to wait until last minutes to build your emergency fund. A famous Buddhist once said, when you take off your shoes today, you don’t even know if you would ever have a chance to wear them again. Cherish the moment and always prepare for the worst.

An emergency fund is a must. If you look at like an insurance plan it makes sense. People typically buy term to protect their family if they die. So I view an emergency fund in the same way. I’m protecting my family for a short period of time where my ability to earn money is dead.

We’re just FOUR weeks from early retirement (@ 49 yrs old) and so the concept of Emergency Fund has taken on new meaning for us. We’ve always held 6 months expenses in a money market or CD. Typically in a CD without an early withdrawal penalty through our credit union. We have expanded that to 36 months expenses as we approach our escape from corporate life. This way, when the financial markets start to rock, we are protected from having to sell anything.

You could use no penalty CD’s and also rotate / ladder them.

Thanks for the kind remarks, Joshua. I appreciate you swinging by and for the click love.

This is a fantastic breakdown of an emergency fund… i like the fact that u mention accessible but not too accessible… I will probably be checking into ING… i will use your affiliate link if i do.

Gotta love the E-fund. Always good to start somewhere… Nicely laid out…