How to Automate Your Savings (Step by Step Banking Guide)

We all want to save more money, but for most of us, that’s way easier said than done. Saving more money means you need not only the intent to save but also the discipline to follow through with it. Most of us have the good intention to save part down pat. It’s the action part that usually hangs us all up.

When you automate and separate your savings, you’re setting up a system to regularly save money with automatic bank transfers to your savings accounts. Using long-term savings accounts like a 401k or IRA can separate your savings and lessen the chance of you taking money out of savings.

Creating a system to automate and separate my savings has helped me save more money. Here’s how I did it.

Why You Should Automate Your Savings

Automating your finances is not a novel concept anymore. But it’s something that shouldn’t be overlooked. It works. It’s a process that has served me well in my life. I automate many aspects of my financial situation:

- paying bills

- short-term savings

- debt reduction

- retirement savings

- college savings

In general, the bills are paid by a recurring bill pay feature, or the money is automatically withdrawn from my bank account by the service company. Probably, more importantly, my savings is also automated by using auto-withdrawals by the bank or financial institution who will be holding the savings.

Why do I do it? Because it works. It helps me achieve more with my money than I could if I were trying to manage it all manually. I just don’t have time to fool with writing out checks or depositing money into various accounts. Plus, I don’t have the mental strength to remember to do it all each month. I have so much else I want to be doing and have to do.

Does this mean that I don’t think about my spending or saving? No. I just don’t have to worry about it as much. It’s on auto-pilot. I can take a few days away from it and not worry. I still watch my accounts regularly via Empower. There are still two bills that I haven’t been able to automate. So I deal with them monthly.

Lastly, every few months, I adjust my financial goals and make sure that my automatic system is ensuring that I’m moving towards those goals.

How to Automate Your Savings

To make saving easy, make it automatic. Set it up and forget about it. Inform your HR department that you’d like your check split into different percentages and give them the bank, 401k, IRA accounts to make this happen. They’ll directly deposit the desired percentage into the accounts.

If they’re not willing to work with you, have all the money direct deposited into a bank and then set up the automatic withdrawals to savings accounts from there. Check out these automated savings apps. They help you by automating your savings and motivating you to save by having you set up goals to achieve.

When You Shouldn’t Automate

However, automating isn’t for everyone. It can be a real plus for those people with a stable financial situation who simply need an advanced technique to take them to the next level. I find that it’s ideal for those who seem to always spend what they earn no matter how much their income has gone up over the years. I am this type of person.

When you shouldn’t automate your finances:

- When you have a major spending problem. If you’re trying to reign in your spending, automation might not be right for you. A cash-only system may better serve you. Ridiculous spending could be masked by the automated payments to your credit cards. [However, I’m also of the opinion that true automation doesn’t worry about spending. Since you’ve automated your savings, bills, and debt reduction, you don’t need to watch your spending. Your spending money is there for you to spend as you please.]

- When you’re just getting started with properly managing your finances. This is a time when you need to be seeing every little detail and understanding the ins and outs of your money. Get to know your financial situation and slowly move towards automation.

- When you have a lot of different debts to pay off. If you’re coming out of a bad debt situation, you may need to be in the trenches with this process. Since debt reduction requires a “pay as much as you can” mentality, you may find it’s easier to manually make payments each month as soon as your paycheck arrives. Learn more about how to pay off debt.

- When you want to ultra-simplify. If your aim is an “off-the-grid” type of lifestyle, then automation isn’t for you.

Automation and Separation

Looking back over some of my old posts on saving money (whether for the short-term or for retirement), two basic themes seem to bubble up over and over again: automation and separation. I’ve decided that for me, these are the two necessary actionable steps to truly make savings work.

Let me add that there are a lot of good savings concepts out there: spend less than you make, pay yourself first, live within your means, a penny saved, etc. While these are great concepts, they aren’t exactly action steps you can take to help you save more money.

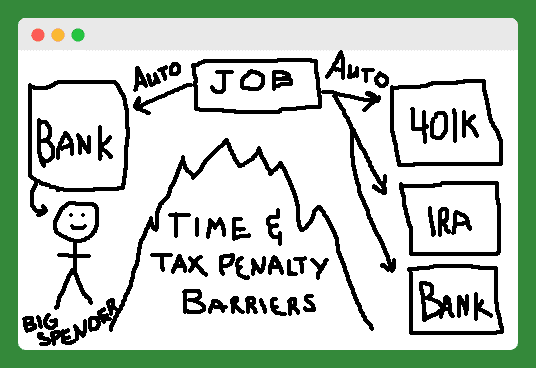

So, I attempted to put the automation and separation ideas in picture form. My drawing skills aren’t what they used to be, but hopefully, you’ll get the point.

Okay, I know it doesn’t look like it, but that is a mountain (or big fire) in the middle, separating the big spender from his or her automatically saved short-term and retirement accounts. Let’s look at these action steps one at a time.

Separate Your Savings

Most people get the automatic step and are already doing it. To make savings stay put, though, you need to separate it. There are two types of separation you can set up to make it hard to tap into your savings. Think of it as if you’re setting up an imaginary wall between you and your savings accounts.

First, use 401k and IRA accounts to save for your retirement so that you’re discouraged from withdrawing the funds by their strict tax penalties.

Second, use online-only savings accounts (like FNBO Direct and Capital One 360) to save up for short-term savings goals. These accounts don’t come with a debit or credit card, and transfers from these accounts to your other bank account take a few days, lessening the chance that you’ll tap into them readily.

A System vs. Self-Discipline

These two actions steps have been working for me for some time now. I’m a good saver now, not because I’m the most disciplined person in the world, but because I have a system that works. I encourage you to set yourself up for success with your savings by automating and separating today.

What is Forced Savings?

Forced savings is when a system or purchase you’re required to spend money on or are already spending money on forces you to save money whether you like it or not.

No one’s forcing you to save money. Well, actually, they are. The “forced” savings account is being used in several areas of our lives, and many of us don’t even know it. In some cases, you may even be forcing yourself to save, which isn’t necessarily a bad thing.

Types of Forced Savings Accounts

Social Security

The biggest forced savings account that we all participate in here in the U.S. is the Federal Old-Age, Survivors, and Disability Insurance program (i.e., Social Security). We are forced, by federal law, to pay 6.2% (temporarily reduced to 4.2%) of our income into this program. Our employer is required to chip in another 6.2%.

What do you get for this forced savings? For me, the future equivalent of around $1,100 each month when I retire at 67. Depending on your income, your ability to save money elsewhere on your own, or your thoughts on the general liberties granted by our Constitution, you may view this forced savings account as a good or a bad thing.

Home Ownership

The most classic example of the forced savings account comes in the form of your own home. Here the idea is that you spend your working years paying off your home. By the time you retire, you will have paid off your mortgage, and you’ll have a nice bit of savings in the form of home equity. You can use this equity to pass wealth on to your heirs.

When doing a rent vs. buy analysis, many proponents of buying (vs. renting) point to this forced savings as one of the major benefits of homeownership. Home equity ends up being the biggest asset for many when they retire.

According to AmericaSaves.org, over four-fifths of the assets of lower-income homeowners represent home equity. But just because it is the biggest asset, it doesn’t mean it should be.

With mortgage interest, property taxes, and the cost of maintenance, a home is one of the worst places to save money.

Tax Refunds (Not the Smartest Forced Savings?)

Another frequently cited form of forced savings, at least on an annual basis, is the federal tax refund. By adjusting your W-4 to include fewer allowances, you will have more money withheld from your paycheck.

The government will then hold this money until you file your taxes, and they’ll pay it back to you in the form of a tax refund. Some taxpayers prefer this method because they feel it forces them to save money that they wouldn’t. In the past, I could understand this strategy. But today, with online savings and easy automation of periodic contributions, it’s just lazy.

Retirement Accounts

If you have a job with good benefits, your employer may force you to begin saving money by automatically enrolling you in the 401K. An increasing number of companies are using automatic enrollment these days.

I think this is a good thing. Someone should have forced me to start with a 401K right away after college. I missed out on a lot of free money in the form of a matching contribution.

That leads me to the next, more subtle, form of forced savings: the 401K match. Companies dangle free money, typically 2% to 5% of your earnings, for you to participate in their 401K program. This money makes it very hard to pass on at least participating at the minimum level.

Another subtle form of forced savings plan is through the use of tax-advantaged savings accounts. Examples include the IRA, 401K, HSA, FSA, 529 Plan, Solo 401K, etc. Each of these types of accounts has a tax-advantage to reward you for saving more of your money.

Read more: Which Retirement Plan Should You Choose for Your Business? [Solo 401k vs SEP IRA vs SIMPLE IRA]

Most of them also have specific annual minimums that give you a target to shoot for each year. Knowing that these accounts exist (and that I can use them to reduce my tax burden) in a subtle way, forces me to use these accounts over other forms of saving or spending.

Except for the 401K, you’ll likely have to set up your own forced savings account with these types of accounts. You can do it in two simple steps. Step one is open the account. Step two is create a periodic automatic contribution to the account from your employer. Pay yourself first!

Auto Savings Apps

There’s a whole new category of forced savings tools out there: automatic savings apps that connect to your banking accounts and facilitate automatic savings deposits. I’ve used one of these apps, Digit, to save over $1,000 without lifting a finger.

Read more: I Saved $1,191.90 Automagically with Digit in Just 5 Months–My Digit Review

Should You Automate Your Bill Paying

Now let’s look at automated bill payment. I have two types of expenses: fixed and variable. By nature, the fixed expense payment are all that I can automate.

While I call them fixed, they’re really just recurring bills. This includes mortgage, insurance, utilities, and loan payments—basically any type of payment that I’m going to be paying every month.

So, I’ve got all these recurring payments. What do I do with them? Instead of sitting down every month to write each one of these payees a check, I automate it. I do this by providing each payee (that will allow it) my banking information so that they can withdraw the proper amount from my bank account each month. Most companies will allow this. This can be set up fairly easily online or by calling their customer service line. That’s it. Easy right? Let’s look a some of the pros and cons of doing this.

Pros of Automating Your Bills

- No more late fees. Turning the reins over to the bill company means never being responsible for the timing of the payment.

- Less time wasted and hassle. Let’s face it, paying bills stinks. Anytime you can take a boring task away from your life, it’s a plus. Spend the saved time with your family and friends.

- No more (or at least considerably less) checks, envelopes, and stamps.

Cons of Automating Your Bills

- Risk of someone getting your banking information. The assumption is that many different companies (and people within those companies) have access to your banking information if you use this method of auto bill payment. I technically don’t know if this is true. For many people, this is the deal-breaker. Using the method I described above, you’ll have given out your banking information to several payees. Each one of those payees is then going to have to keep your information secure. Do you trust them? Are you protected? I’ve minimized this risk by only keeping enough money in my checking account to make the monthly payment. Therefore, if my information leaks out, only a small amount of my cash will be at risk. Also, only give your information to those payees with the VeriSign seal. Sites that use VeriSign will have SSL, which “establishes an encrypted communication channel to help prevent the interception of critical information when transmitted over the Internet.”

- Less flexible. When it’s time to change bank accounts, I’m going to have to tell each of those payees my new banking information. That might be enough motivation to keep me at a bank I’m not happy with for much longer than I should.

- Overdraft fees. What if one of your bills has a huge incorrect charge on it, and you end up over-drafting on your account? Well, this risk can be minimized by checking your statements every month and keeping a line of credit or overdraft protection on your bank account.

- Losing touch with your finances. Setting up auto payments can have a negative effect on the overall awareness of your finances. Similar to automating your savings, once your payments are out of sight, they can quickly become out of mind. Again, this risk can be minimized by reviewing your statements carefully every month.

Why People Do Not Save Enough

Everyone wants to save more money: whether for short-term needs and wants, a safety net, retirement, or for financial freedom. It’s hard to imagine a person who doesn’t want more money stashed away. So, why are there so many people with so little savings? Why are so many people throwing their arms up in frustration, saying, “I can’t save money!”?

Can they really not afford to save? I suppose some people barely scrape by…and it’s understandable that some people would be unable to save given their situation. Still, I believe most Americans bring in enough income to be able to save some of their money. Can’t we all agree on that?

So, if we can save, then why aren’t we? Is it because we’re lazy? Unmotivated? Undisciplined? I say…none of the above. Here are two key reasons people aren’t saving enough money, even if they really want to.

They Aren’t Making Savings Automatic

Make saving money automatic. If you can’t already tell, this is my number one tip for saving more money. Not to try *really* hard, think positive, or wait till I make more. Those are failed mantras.

The best way to truly save more of your money is to set up a direct deposit from your paycheck directly into different savings accounts—one for retirement and another for short-term goals.

Don’t know how to do the direct deposit thing? Ask your company’s human resource representative. Want to know where to put your money? See my second point…

Their Savings is Too Easy to Access

Money in a savings account attached to your regular checking account is just begging to get raided. No one has enough discipline alone to keep their hands off of cash savings in a regular bank savings account. Well, maybe some do, but those people are few and far between. Most of us struggle with this.

Short-term savings should be kept in an Online Savings Account or a Certificate of Deposit. Both of these products make your money harder to access, increasing the chances that you’ll leave it alone.

Long-term or retirement savings should be kept in a tax-advantaged account like a 401k or an IRA. Both accounts come with big disadvantages for early withdrawal, more motivation to just leave your savings alone.

Now, just spend the money that’s leftover. The beauty of this setup is that you can literally spend the rest without worry. If you’ve got your retirement and short-term savings taken care of before even getting your money, then you’re set. No worries, right? Pay your bills and spend the rest.

How to Set Up Your Bank Accounts for Automation

Over time our financial goals have changed, and because of it, so have our banking needs and automation. The main goals of our newest setup are:

- Automate bill payments and money transfers – ING DIRECT has these capabilities. It’s nice.

- Take advantage of free services – BOA’s Bill Pay is FREE and easy to use.

- Avoid fees – I pay no fees with any of these accounts.

- Maximize interest – While I’m not getting the best interest rate compared with some online-only savings accounts, I am doing considerably better than by only having my money in BOA.

- Convenient access to ATMs and a brick and mortar bank – If I need to visit an ATM, both banks have these. And if I need to go inside a bank for any reason, I can always find a BOA to go into.

Business Banking

Business Credit Card

I use my Chase INK rewards card for at least 75% of the spending I do for my business. This card pays for website hosting, domain renewals, newsletter management, various marketing expenses, home office equipment, and the occasional business lunch.

I also have this card attached to my PayPal account as the backup. If I’m ever short of funds at PayPal, it gets pulled from here. This card is paid off each month, automatically and in full, using my business checking account.

I love this card because it gives me added protection for my business expenses, and it provides cashback rewards.

Business Checking Account

I use Chase business checking as my primary hub for all of my business activities. I pay off my business credit card with this checking account. All my business income is directly deposited into this account, or I deposit the physical check (I occasionally use their photo check deposit feature…very cool).

I use this account for any business expenses that I can’t pay with my credit card: taxes, invoices from contractors, etc. Once or twice a month, I move some money from this account over into my personal checking account.

Resource: Best Free Business Checking Accounts

Personal Banking

Personal Credit Card

Recently we made the switch to using the Chase Freedom credit card as our primary personal spending account. We use this card for all of our discretionary spending (groceries, gas, dining out, travel, entertainment, household goods, convenience items, etc.).

Several bills are paid automatically using this account: internet service, cell phone service, gym membership, and toll road charges. We also have our auto insurance paid automatically using this account, but it only hits every six months.

We would have more bills set up on autopilot, but this is every one that would let us pay with a credit card. As you can imagine, with all of this spending going through the card, the cashback rewards rack up pretty quickly. We’ve already cashed out over $200 in rewards.

Like my business credit card, this card is paid automatically and in full each month. Except this one is paid off from our personal checking account.

Personal Checking Account

We use Capital One 360 Checking as our primary hub for all of our personal checking. This account is funded by my business checking account using electronic transfers on an as-needed basis. From this account, we pay the following bills automatically using bill pay: mortgage, homeowners association dues, life insurance, and car payment.

We are forced to use our debit card for this account when we shop at Sams Club and we pay the following bills using the manual bill pay or check-writing features: water and city services, electric, gas, health insurance, as well as annual charitable donations and property tax payments.

Finally, we automatically withdraw funds from this account for the following savings accounts: Roth IRAs for each of us, and 529 Plans for each of our children.

Personal Savings Account

We use Capital One 360 Savings account for our emergency fund. We earn a bit of interest on this money, and it remains separate from our checking, which is key. Ideally, we should have some sort of automatic transfer going into this account, as we discovered last fall that we don’t quite have enough short-term savings.

Resource: The Best High Yield Online Savings Accounts

Additional Banking Accounts

Personal Retirement Accounts – As I mentioned above, we are automatically funding Roth IRAs each month. These accounts are held at Vanguard. I also have a rollover IRA there as a result of closing my 401K at my old job. Mrs. PT is taking steps to move her old 403B to a rollover IRA as well.

Taxable Investing Account – We don’t do much of this, but we have a small amount of money with Capital One Investing in a taxable investing account.

College Savings Accounts – We opened these 529 college savings plan accounts a couple of years ago and have funded them on and off with various funds. Recently I set up a small automatic contribution to each as the plan I’m with will provide bonus money and sweepstakes funds for people automatically contributing.

What’s Missing?

Going from corporate job income to being self-employed has thrown kinks in our banking setup. Much of the work of saving and insurance will be on our shoulders now. As you can see, we need to set up some type of auto contribution to our personal savings account.

We also need to look into ways to automate more of our bill and/or move them to credit card payment to earn more rewards. Finally, I need to start contributing to a self-employment retirement plan, either a SEP IRA or a Solo 401K.

Next Steps

If you haven’t tried it yet, I would encourage you to try automating and separating your own savings. With time, your financial goals will change—you will likely want to improve things. Use that energy to take the time to set up your automatic financial system to save more money.

Do you automate your savings or banking? Share your automation tips in the comments below.

Photo by JESHOOTS on Unsplash