Should You Payoff Your Mortgage Early? Yep! Here Are 6 Strategies to Pull It Off!

My wife and I are 38 and 43, respectively, and we just paid off our home mortgage – a home we purchased seven years ago. It feels great to own our home outright and not have the risk of that big debt in our life.

Making the decision to pay off our mortgage early is a decision we’ve gone back and forth on. We’ve wrestled with it. But, ultimately, our financial successes and inertia pushed us to go forward with the payoff.

If you’re reading this post you’re probably wrestling with the decision too.

Let’s stop right here and recognize how amazing it is that you are even considering this question. No doubt things are going well for you financially and you’ve made some smart decisions with your money. Congrats!

If you’re contemplating this decision and you have the means to pay off your mortgage early – either with a lump sum or through routine prepayments – I think you should, even though the long-term math says you shouldn’t.

In this article, I’ll share in more detail why I think you should pay off your mortgage early, how I thought through this decision, some of the pros and cons, and, finally, I’ll share the actual process we took to pay off our mortgage early (PLUS, 5 more strategies).

Things to Do Before You Consider Paying Off the Mortgage Early

A few caveats before we look at this question. I’ll assume you are living within your means and have all the basics taken care of. Here are some more things you should probably have taken care of before you go about paying off your mortgage early.

- Have a well-established emergency savings fund. This is personal finance 101. Have enough emergency savings stashed away so that in case of an emergency you can cover it with these funds.

- Have no other debts. In most cases, the home mortgage should be the last debt that you tackle. Get rid of those car loans, personal loans, medical debts, and certainly any credit card debt before you dive into the mortgage prepayment process.

- Be getting your employer match. If your company 401k offers a matching savings program, you should definitely be getting that, and you should be able to maintain that level of savings while you are paying off your mortgage early.

- Be mostly settled. Life changes all the time, but those who want to tackle their mortgage head-on should have their life in order and be somewhat settled. Is your income stable and growing? Are you done with family planning? Are you rooted in your community? If you aren’t settled in life, frankly, you shouldn’t be buying homes to live in.

What About Student Loans?

Student loan debt and mortgages are often lumped into the “good debt” bucket.

Student loan debt, which generally has a very low-interest rate, creates value over time in your ability to qualify for a higher paying job. It’s also tax-deductible like the mortgage interest.

So which should you pay off first?

As you know, there are two ways to pay off your debt that are most often touted.

One is the “snowball” method. Under this technique, encouraged by financial guru Dave Ramsey, an individual attacks the smallest debt first.

By attacking the debt with the smallest balance, an individual is going to have success fairly quickly.

This is important, according to Ramsey, because it’s exciting to pay off a debt. That enthusiasm makes it easier to stay disciplined.

Most people subscribing to this method would choose to pay off the student loan debt first because of the lower balance.

The second way many people decide which bills to pay off first relies on a very basic financial principle. Take a look at the interest rates of all your bills and target the bill with the highest interest rate first.

Student loans generally carry a low-to-moderate interest rate, currently averaging 5.8% in the U.S. according to New America.

Mortgage rates are really low, currently averaging below 4%, per Bankrate.

If your rates are in those ranges, it’s a no-brainer to knock out the student loan debt first.

Related: The Lame 25% Rule and How Much House You Can (Responsibly) Afford

Pay Off Mortgage Early or Invest?

The argument around paying off your mortgage early mostly revolves around whether you should instead be investing the money.

The math actually supports investing in most cases, especially as the term becomes longer. I’m not going to get too deep into it, but here’s a couple of short, crude examples:

- Let’s say you have a $200,000 mortgage at a 30-year fixed 4% interest rate.

- Let’s also assume you have an extra $1,000 each month to either invest in taxable investment accounts or apply to your mortgage.

Example 1 (Invest): If you spend the next 30 years paying that off with the minimum payments, you will have paid a total of $343,739.21 in combined principal and interest payments. If you invested the $1,000 each month into a taxable investing account at a projected 6% annual return, your investment alone would be worth around $1,000,000 at the 30-year mark.

Example 2 (Debt Payoff): If instead, you apply the extra $1,000 to your monthly payments, at the end of 10.5 years you will have paid off your mortgage. You will have paid a total of $245,007.71 in combined principal and interest payments. If you then started investing the $1,000 plus the mortgage payment of $954.83 each month into a taxable investing account at a projected 6% annual return, your investment would grow over the next 19.5 years and be worth around $850,000 at the 30-year mark.

So, even though you will save around $100,000 in interest payments, you are giving up over $150,000 in potential investment gains.

Over 10 or 15 years the difference isn’t as drastic AND stock market returns do vary. But it’s important to understand what you are giving up over the long-haul, and I think this example shows just that.

Before we leave this section, you should know: you can do both! You can fast track your mortgage and still aggressively invest. It’s not an either-or proposition.

You’ll likely make more money in the future. You’ll get a raise. Your business will take off. You’ll create that second or third stream of income. Pretending that you can only do one or the other only limits your mindset.

Go after both! When you do both, the math always works out in your favor.

Related: What’s Keeping You From a Radical Financial Life?

The Benefits of Paying Off Your Mortgage Early

- Reduce the amount of interest paid on debt. By reducing the amount of time it takes to pay off the loan, you are reducing the amount of interest you’ll pay. In the example above, you’re saving around $100,000.

- Reduce monthly outflows. Once you pay off the mortgage, you’ll no longer have a mortgage payment. Now your monthly expenses are lower and you’ll have more money in your monthly budget to do other things with: invest, spend, give, etc.

- More freedom. By eliminating the mortgage early, you bring more freedom into your life. Maybe you or your spouse can now stay at home with your children? If you’re a budding entrepreneur like me, think about how much easier it would be for you to leave your full-time job to pursue a business idea full time. No mortgage = freedom!

- Security and peace of mind for your family. With one less expense, you’re creating more security for your family in case of future emergencies. You’ll always have your home to go to regardless of the economy or the bank’s issues. This is big for my wife. It’s the main reason she wanted this debt gone. She’s much more secure in our overall financial position without the home debt.

- Simplify your finances and life. The older I get, the less I want to think about my finances. Removing the mortgage means I don’t have to think about the mortgage payment, my lender, or fuss with online payments.

The Disadvantages of Paying Off Your Mortgage Early

- Reduced liquidity. When you pay off your mortgage early you’re likely taking money off the table that could be implemented quickly to help you in your life. Paying off your mortgage early could leave you “house rich”, cash poor for a while.

- Overall less diverse portfolio. By paying off your mortgage you may be putting many of your eggs in one big basket. This makes you really dependent upon the local real estate market (some of which are actually going down in value) and dependent on the overall economy.

- Loss of tax deduction (although the new tax law changes this for some). One of the nicest benefits of having a home mortgage when it comes time to pay your taxes is the home mortgage interest deduction, which you can claim if you itemize your deductions. The new tax law increased the standard deduction, however, and so many folks are going to be losing the ability to take this deduction anyway.

- Lost potential investment returns. This is the biggie. By saying yes to paying off your mortgage, you are saying no to investing in the stock market, rental properties, your business, and other investments. The opportunity cost can be huge as we showed in the example above.

- You’ll still have payments (property taxes, insurance, HOA dues, maintenance, etc.). Just because you got rid of the mortgage it doesn’t mean you still don’t have to pay for your house. In fact, there are still likely at least three major expenses you’ll have: taxes, insurance, and maintenance. That’s a bummer. On top of that, you’ll have to start saving for and making your own insurance and tax payments yourself if you previously escrowed them.

- Possible prepayment fees and negative credit consequences. Watch out for prepayment fees. They could make your early payoff plan a terrible idea. Lastly, know that if you pay off your mortgage – your primary installment credit line – you’re likely going to reduce your attractiveness to future lenders who’d rather see a more diverse credit mix. Albeit, you probably don’t need credit once you pay off your home.

6 Different Strategies to Pay Off Your Mortgage Early

Okay, so you’ve decided to do this. Let’s actually get into some ways in which you could go about paying off your mortgage early. There are quite a few:

1. Making Routine (Extra) Prepayments on Your Mortgage.

The most common way would be to simply start making additional principal payments each month.

Ideally, you can automate this function with your lender. Just make sure that when you start making extra payments they get applied to your actual principal vs both principal and interest.

An extra $250 per month on a 200,000 loan at 4% interest would knock 10 years off your loan – taking it from a 30-year mortgage to a 20 year.

2. Setup Biweekly Payments

Instead of paying your mortgage each month, you could switch to bi-weekly payments. This would give you 26 half payments each year vs the 12 full payments.

This strategy will help you speed up your mortgage payoff and will help you save on interest without actually changing much of your cash outlay.

I know Quicken Loans allows this type of payment to be automated now. Check with your lender to see if they can set it up for you.

3. Refinancing to a 15 Years vs 30 Year Mortgage

As a way of forcing yourself to pay off your home faster, you could refinance your mortgage down to a 10, 15, or 20-year term. Before you refinance, you need a good credit score. Consider Experian Boost to increase yours.

There might be closing costs to account for here. But a better rate and a shorter term could be just the strategy you need.

We actually did this ourselves after we’d been in our home for three years. We thought we’d be fine just paying it off at the 15-year term. But just three years later we got itchy again and decided to start making big lump sum payments.

Related: Pros and Cons of the 15 vs 30 Year Mortgage

4. Rent Out a Room (aka House Hack) and Apply the Rent Payment

An alternative strategy is to become an Airbnb host and rent out a room in your home to the occasional visitor. This extra income stream could be applied directly to your mortgage balance and help you pay off your home sooner.

5. Mortgage Acceleration Software/HELOC

I’ve looked into the mortgage acceleration software/strategies and I just can’t wrap my head around how they actually work, much less do an actual cost/benefit analysis of the software required to pull it off efficiently.

They feel too complicated and scammy, too. My advice is to stay away from anything that seems weird or that you can’t understand. I don’t understand these things, so I’ll skip it.

6. Paying Off Your Mortgage Early with Lump Sum Payments

This is ultimately the method we chose to use over the past two years to knock out our mortgage. We stashed cash from business successes mainly and used it to make big lump sum payments, concluding with a ~$49k payment this past month.

Whether it’s annual bonuses, tax refunds, stock options, or some side-hustle business boom, think of the lump sums you’ll be getting over the next few years. Make plans to apply those big chunks to your mortgage.

There are no ways to automate this, unfortunately. But if you are in a place where you’re just crushing it financially and you trust yourself to not let your lifestyle creep up, this can be a massively effective strategy.

The Actual Process of Paying Off Your Mortgage (aka Making the Final Payment)

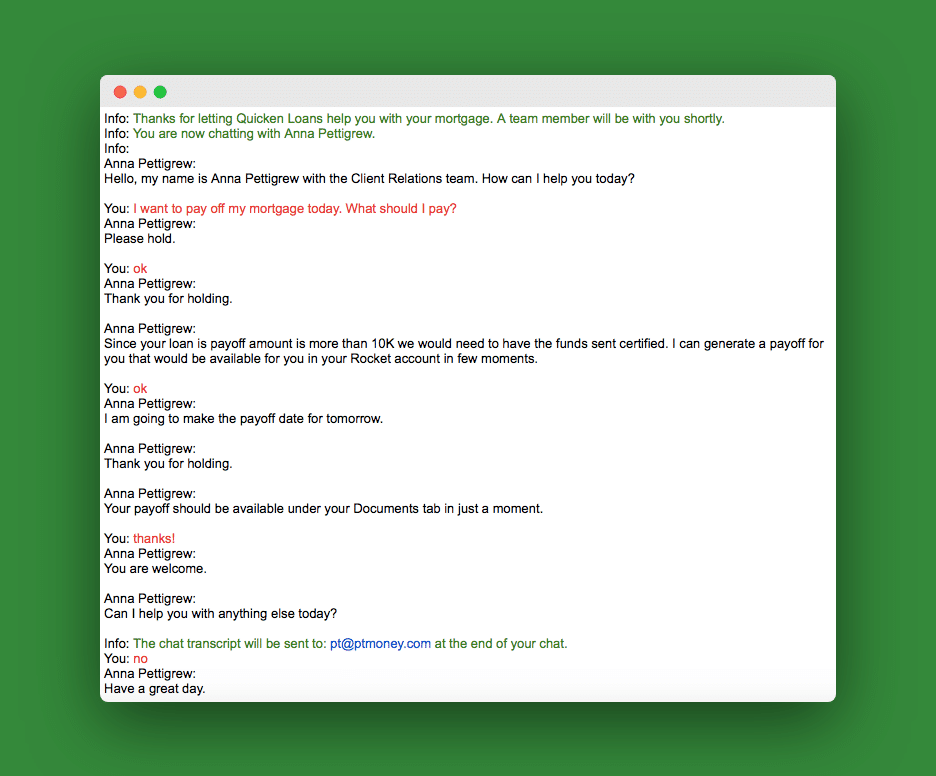

When it’s time to make the final payment using a lump sum approach, you’ll need to request your payoff amount. This amount it going to be slightly different than your actual mortgage balance shown on your statement or on your lender’s website.

You can either call and request it or do like I did and use the lender’s website customer support chat. Here’s my chat thread:

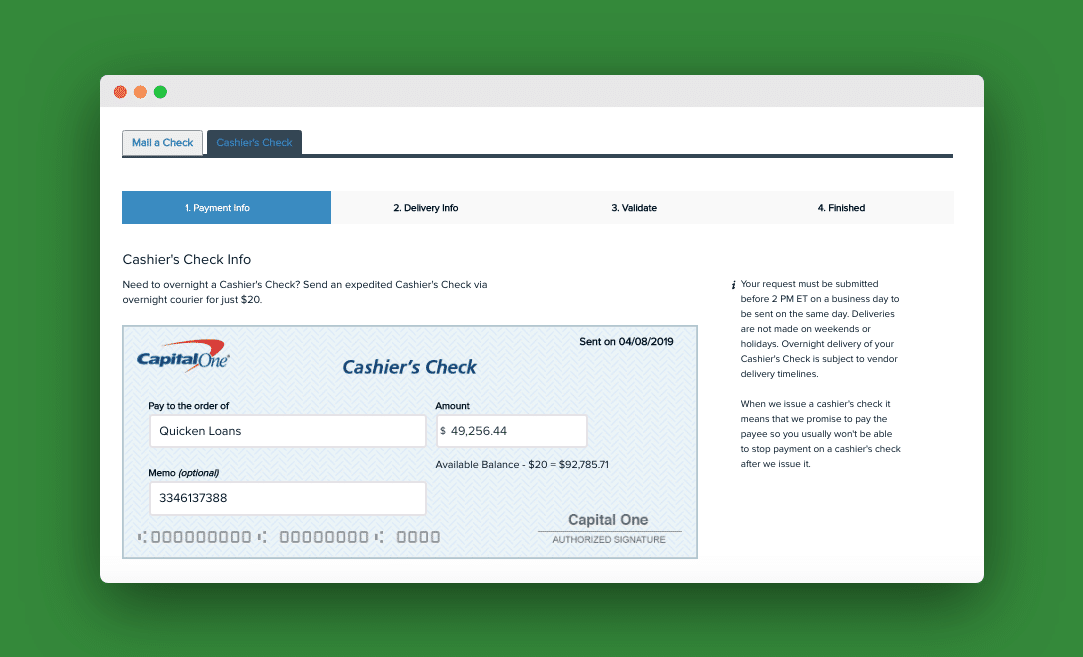

Once we got that payoff number, we went to our personal checking account online account and set up a cashier’s check payment. There was a fee of $20 to overnight it. Here’s a snapshot of our cashier’s check:

Once the lender receives the final payment they will apply it to the loan and send you a letter to inform you that your mortgage loan is paid in full.

More Questions

What if you have two mortgages on your home? Let’s say you have two mortgages on your home: the primary mortgage and a second mortgage or HELOC. In that instance, you should definitely pay off the second mortgage or HELOC first. 99% of the time those second loans will have higher interest rates and be smaller in amount. Knock them out first and then tackle the primary.

What if you have a rental property mortgage like I do? If you have a rental property mortgage, unless it’s some minuscule amount, that debt should come second in priority to your home mortgage. If something happens to your rental property mortgage, the worst that can happen is you can no longer rent it out. But if the bank makes a call on your home mortgage, you’d be out of a home. The smart thing here is to pay off the home mortgage first.

Final Thoughts on Paying Off Your Mortgage Early

If you’re asking this question of whether to pay off the home mortgage early then you are in a great spot. Honestly, what you do here doesn’t matter that much because you’re already making such good financial decisions.

If you’re the type to hyper-focus on the math and you’ve got a home for this investment money, then, by all means, let the numbers lead you.

But if you can shoot to be completely debt free and still maintain some aggressive saving (likely what you’ll do either way) then go for the early mortgage payoff.

What’s your plan? Will you be paying off your home mortgage early?

I paid off my 30 year mortgage after 20 years in January 2020. I knew that given the interest rate on my mortgage, 3.25%, that based on historic gains investing the $200K I used to pay off the mortgage was the “right” financial decision. Given what has happened in the stock market the past 2 months I couldn’t be more happy with my decision to pay it off. There is zero guaranty that investing that money will give a better yield than paying it off. And, I have an extra $1450 after tax dollars in my pocket each month which feels awesome. Had I invested that money in stocks I would be down 15% at the moment. Yes, it will come back eventually. But now I get to save over $1K a month that I was not saving previously. I’ll take that any day.

You have already stated that the math shows very clearly that you should NOT pay off your mortgage if your rate is relatively low, but still “feel” it is the best choice.

However, one aspect of keeping your mortgage that is often overlooked by those in the “all debt is bad” camp and that you failed to mention is the power of leveraged returns.

Assuming you have a fixed rate mortgage, when your real estate appreciates, lets say 3% (conservative for national average), you enjoy that 3% growth on the entire value of your property, but you only have some small portion, lets say 25%, actually “invested” in that security. Making the effective growth rate on your investment 12%. Example: 200k property, 150k loan balance, 50k invested, 3% annual growth on 200k is 6k = 12% of 50k investment.

Lets say you are in the “no-debt” camp and you are doing “well” and have the $150k sitting around to pay off the mortgage. You pay off the mortgage but now only enjoy 3% growth on your full $200k, sad…

Had you invested the $150k, rather than pay off the mortgage, into buying more investment properties that had similar numbers you’d be getting another 12% + extra cash flow on rental income, or an easy 9-12% in stocks, in addition to the 12% you enjoyed when you had the mortgage on your home.

Additionally, if you want to talk about financial peace and security, if you invested the money in a well diversified portfolio you’d probably be looking at closer to 6% annual return with very low volatility. More than enough to cover your P&I of your $150k mortgage. Ex: 150k 30/fixed mortgage at today’s rates of 3.75% = $695 P&I / mo (remember you still have to pay the tax man and insurance when mortgage is paid off).

Returns of $150k investment at 6% = $750 / mo.

So that very conservative 6% investment of the money more than covers your mortgage P&I and gives you an extra $50 / mo you can reinvest! Plus you keep enjoying the nearly 12% return on your home investment.

If you want to get back to feelings, I personally feel a lot more secure having 14x the wealth in 30 years (12% vs 3% growth) to ensure my family is taken care of and we can give generously by being wise with the money we have now and investing it prudently, rather than effectively keeping it under the mattress of paying off a primary residence.

We are 3 years into a 25yr term mortgage and we’ve saved enough to pay it off now. Question is just what you are asking, do we pay it off or invest. That’s a hard question to answer so I think we’ve decided to pay it off, get it out the way and take the money we will save every month and start investing and saving that. Where’s that crystal ball… I need it. Cheers and great post. Mr.CBB

Can you not consider your rental as your home in the future god forbid something bad happened and you lost/gave up your home. Therefore freeing up your mind to just go on best numbers? Just curious.

Interesting analysis Phil. Great methodical approach and a good read for others considering paying off a mortgage.

And suddenly a hashtag is born! 🙂 #FinNews

@ptmoney @applecsmith

@bowaterecu Thank you for the RT!

@annuityearl Thank you for the mention yesterday!

If you ever listen to Dave Ramsey or read his books you would know that the snowball method does NOT apply to mortgages that are more than half your income (personal or rental homes). Also, if you called in to his show he would tell you to pay off your personal residence first! You would rather the bank take your rental from you than your personal home if things went bad.

Payoff your home first. I currently have a paid off home, plus one rental unit with a $120k mortgage. We’re working to pay that off next. The “number people” may tell you that money is cheap right now and to pay off neither, but those people probably haven’t experienced a mortgage free life. Take it from me…when you live in your home debt-free: the food from the kitchen taste better, the air smells sweeter, and the st. augustine grass feels better between your toes. You truly can’t put a price on it. Few people have a chance to payoff their home, so go for it PT! You have plenty of future decision you can make based on “the numbers”. But go with your gut on this one…it’s leading you to a peaceful place, I promise.

@GRSblog @ptmoney I didn’t realize you couldn’t do both at the same time.

@desluna It’s more of a “would your rather” type of question. Of course, your mortgage gains interest.

If you are in the phase-out range for itemized deductions, then losses on the rental may not be deductible either, they just carry forward. At least until the place runs positive, then those losses are used up.

I’d slowly tackle the higher rate, I suppose.

@joetaxpayer Good point about the rental deductions. My Dad, CPA, asked the same thing. But I should be running a gain from my rental unit (it’s cash flow positive), unless I don’t understand how much the depreciation will affect things. Something my CPA will look at before the year ends. TBD.

@payoff @ptmoney if I could, I would; why not?

@Orly7581 @ptmoney Paying off debt is tough, but not impossible!

@payoff @ptmoney you are right; I wish there are better options, interest rates on debt kills me.

@Orly7581 @payoff Math and history says the money might be better spent investing. But it’s a personal choice. I’m choosing to pay some off.

. @ptmoney I’m glad I’m not in your shoes; I’d not be able to sleep if I owe so much. Me? focus intensity -house #1 paid for, working on #2

@gbarquero What if I said I had a million in retirement accounts? Would it make a diff?

@ptmoney Good point! but you would owe more than half of it, so it’s not really yours. Good discussion, thanks for what you do.

@gbarquero Agreed. Great discussion.

fully think being debt free is way to go…i’m tired of being a slave to the lender. we are aggressively paying off our mortgage just to be free from anyone owning a piece of our pie…one day, i hope to buy some real estate with cash and use the proceeds to buy the next one.

as for your case, i think it is six one way half dozen the other … i’d probably attack the smaller one first, simply because you could always move back in it if you had to. i’d also consider refinancing them … you might get 15 year loans that would be comparable PLUS pay more principal.

Personally I am leaning toward not paying off my mortgage early as well. With my low interest rate combined with the tax write-off, I think I can get better results investing elsewhere. When this no longer becomes the case I will reconsider. However, I agree that I would not throw more money at rental property at the moment if you are not planning on that being your main source of income. It would be a better idea to diversify at this time for some security.

Normally, I would never payoff my mortgage early! I am paying off my mortgage early to coincide with my retirement in 4.5 years.

I’m really leaning toward NOT paying off my mortgage due to inflation. I think it’d be awesome to pay the same mortgage payment in 25 years when things cost 2 or 3 times as much. My thought process may change one day though and my mortgage payment is ridiculously low.

Hi PT – I would first consider refinancing both mortgages. I just did my primary home refi to 2.625% for a 5/1 ARM jumbo. I refied my rental property last year to 3.375% for a 5/1 ARM. I’m sure you can lower your rate!

I’d also just go with your gut and throw money at your mortgage whenever you feel like it over a period of time. Liquidity is good!

Thx for finding my post.

Cheers, Sam

@Yakezie I guess I need to take a second look at the risk of ARMs. That is a good rental property rate. If I refi-ed mine I’d lose my personal residence rate and would have to go ARM to beat it. Ultimately I think I’m just ready to be rid of the hassle of debt.

@Philip Taylor I am a STRONG proponent of 5/1 ARMs and ARMs in general. Take a look at a 30 year chart of the 10-year yield. It’s been going straight down!

If I could borrow at 1 month libor I would! Sam

It’s interesting to me that the decision to pay off the mortgage early isn’t a numbers decision but a feeling one, yet “which” mortgage you pay off first is a math equation. Why the change?

@AverageJoeMoney Good point. Well, even though I said gut, you could really say it was math I guess – my debt to asset ratio is too high. I guess I’m just ignoring the invest % vs debt % math. In the second question, we’re following both math (mort int issue) and gut (desire to live in a debt free home), and actually ignoring the snowball/avalanche math. All that to say, it’s a mix of things. Ultimately I don’t think it matters much. Financial freedom is in our future. It’s just a matter of which road to take. Both roads have about the same distance. One’s more scenic? Okay, I took the analogy too far there.

It’s a question I ponder often. Given that I’m earning at least 6% on dividend stocks and my mortgage interest is less than that, I’ve opted to keep both and pocket the difference. The difference isn’t a lot, though, so I’m still on the knife’s edge. What’s tipping the balance is the question of whether or not inflation’s going to take off. If it is, I want the capital to purchase another house to get the appreciation benefit.

@William_Drop_Dead_Money I think what we’ll do William is probably pay off our home and then build downpayment money for another rental. Great idea that ties back into your inflation post from last week.

@Philip Taylor @William_Drop_Dead_Money

“probably pay off our home and then build downpayment money for another rental.”

@PT this makes no sense to me. Rates and homes are at historic lows and you are going to wait what could be years because the debt feels “icky”? It would make sense to me if you weren’t looking to take on additional real estate, but if you found a cash flow positive unit you could then deleverage over the next decade as rates increase.

@MJTM @Philip Taylor @William_Drop_Dead_Money @PT “what could be years” Who said it would be years? What if it’s 6 months? 🙂 I think having one paid off property changes everything.

@Philip Taylor @William_Drop_Dead_Money @PT

Yes, I think if it is 6 months that changes my answer. But that is a whole lot of debt to pay off in 6 months! lol