9 Practical Tips for Going to One Income (You Can Do This!)

This article was first published in 2008. But the message is still relevant today.

Going to one income?

We’re going to one income very soon.

This is the last month that we’ll receive two paychecks, as Mrs. PT will be going back to school next month. I decided I would do a little preparation. I did some research and came up with 9 tips for going to one income:

1. Reorganize Your Banking Situation

If you’re like me, you have multiple bank accounts. One for each spouse’s paycheck. These two accounts likely have their own direct deposits and outgoing automated bill pay and withdrawal. In order to ensure you don’t incur any NSF fees, you’ll need to adjust your automatic bill pay and withdrawals. Next week I’ll share how I moved my bill pay to Capital One 360‘s checking account. (subscribe and never miss a post)

2. Re-adjust Your Retirement Contributions

Since you’ll likely lose the ability to contribute to one of your retirement accounts (401(k), 403(b), Stock Plan), you’ll need to make up for it using an IRA, or adjusting the income earning spouse’s contributions. We’ll lose the option of contributing to a 403(b). I plan to supplement that by maxing out a Roth IRA by next April and by increasing my 401(k) percentage.

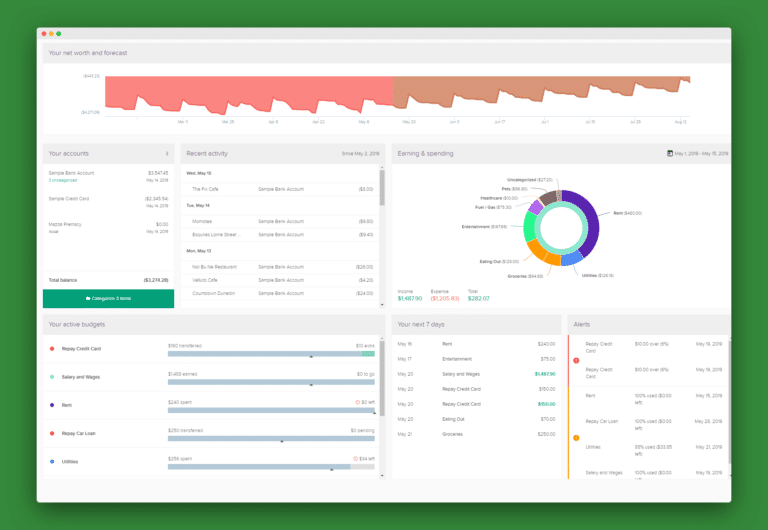

3. Know Your Finances

Beyond banking and retirement, make sure you have a full understanding of your financial situation prior to pulling the plug on the second income. I recently built a dashboard view of my finances. Using something like this or a simple pen and paper budget accounting for your new income and expenses will give you confidence in making the move.

4. Get Serious About Reducing Unnecessary Expenses

If, after you analyzed your finances you realize things are going to be tight, it’s time to get serious about reducing your expenses. Start with the unnecessary items like dining out and luxury items. Learn to live a frugal life.

5. Consider Going to One Car

While we’re discussing reducing expenses, if going to one income means that a spouse will now be at home, consider selling one of your cars. We’ll be keeping our second vehicle because Mrs. PT will need to commute to school, and because here in sprawling Dallas it’s really hard to go without two cars.

6. Make a List of Frugal Things You Can Do

The last thing you want to do is shut off one income and increase your expenses because you’re spending more out of boredom. Check out your local library and community event calendar for good ideas.

7. Consider Working from Home

If you’re making the move to one income to stay at home with kids, consider doing some part-time work with a few free hours you may have.

8. Make Sure You’re Still Insured

Don’t forget that the loss of a paycheck usually means you’ll be losing benefits as well. Health insurance is something you may need to switch to the other spouse.

9. Adjust Your Tax Withholdings

Here’s a plus. Moving to one income means you’ll likely pay less in taxes. Consult your tax professional and see if it’s necessary for you to adjust the withholdings on the remaining income.

Should You Go to One Income?

Of course, the financial aspect is only one portion of it. There are many great reasons for going to one income. I believe a majority of us can make the move with just a few sacrifices.

As always, I don’t know all the answers. I couldn’t think of a 10th tip for going to one income. If YOU have one please leave it in the comments below.

We ‘practiced’ for a few months before going to one income because I knew it would be an adjustment not being able to buy things or go out on a whim 😊

Our strategy has been to always base our spending on 1 income (granted it’s the higher one) in case we lost one. Makes it easier if something happens.

Like everything, living on one income has its pros and con, not of all which are related to financial aspects. But having experienced both two income and one income living, both options can be great depending on the circumstances. The best situation is that both partners are happy and able to adjust things accordingly depending on which phase they are in.

We are most likely moving to one income soon. My wife may be staying home to take care of our little one. Great list of tips!

@J – Thanks for contributing. Excellent point. That’s sort of what we’re going to attempt to do with her last direct deposit. Let it sit in the old account as a security blanket, and to show we can live off of the other account only.

@No Debt Plan – Thanks for swinging by. I appreciate it.

Wow — congrats on going to one income. At least you’ve got time to think about it ahead of time. Best of luck with it!

#10 – Take a practice run. If I’ve followed you’re posts correctly, and you have your accounts set the way I think you do, give it a try in the next few weeks. Set everything up to run on just your account, and completely ignore hers. If you have to delve into hers at some point, you may need to further recalibrate. Plus a bit of practice while you have a safety net can’t hurt.

@ Mike D. – That’s awesome. My tip: try and live like you’re still on one…save as much of the new income as you can. Have a little more fun too though. Work hard, play hard.

Wow. That must be really hard cutting back like that. I’m counting the months (10) until we go to a dual income situation!! Can’t wait. I’ll need some tips on that too, PT.

@ Caveman – Thanks for the comments. It’s good to hear that you are managing it well. Less dining out is going to hard for me, but I know it’s worth the effort.

@ Jesse – Wow. That’s quite a price jump. Mrs. PT is already on my plan actually since my plan was more affordable than her old one anyway. I’m lucky in that regard I guess. As for our new baby, I’m sure it will jump up a bit. *runs off to check insurance plan*

I think its the insurance thing that scares me the most. For me to add Lauren + baby it would be roughly $650 extra per month for me based on my company plan. Ouch!

My wife and I have been on one income now for over a year and a half. It’s been difficult, but I know from personal experience that it can work. Your list is solid and I wish we had seen it when we were first starting out.

One thing we’ve done that wasn’t on your list is to change our eating habits. When my wife worked, we were far more likely to eat out. Now we eat home-cooked meals whenever possible – a huge benefit of a stay-at-home mom. Even if one person’s not staying home, changing your eating habits can save a great deal of money: brown bagging lunch, making large meals and eating leftovers for a few days, etc.

@Steward – Thanks for offering that one up. That’s a great point. Like a car, housing is a big expense you may want to look at reducing, or in your case, eliminating. I guess it all depends on how much you like your relatives. 🙂

@David – Thanks for swinging by.

Great tips here, thanks for including my post!

My wife and I are moving to one income in a couple of weeks in expectation of a baby coming in early November. One thing that we needed to do as well was rearrange our living arrangements. So we have moved in with a relative to help reduce our expenses for the time being. With the move we have turned a $200 projected budget deficit into a $700 projected surplus.