How to Open a Health Savings Account

How to open a health savings account is a question I’ve struggled with myself. After my group insurance ran out, I started a high-deductible individual health insurance plan with BlueCross BlueShield.

At that point, finding a Health Savings Account (HSA) was top of my list. We wanted to start saving tax dollars on out-of-pocket healthcare costs as soon as possible.

To open a health savings account, you must be enrolled in an HSA-eligible High Deductible Health Plan (HDHP). You may be able to open an HSA with your HDHP insurance provider if they also offer health savings accounts. Individuals can open an HSA by researching and picking a plan provider. After that, you set up an account and begin making contributions.

Knowing where and how to open your HSA isn’t always clear throughout the health insurance process. Doing a little research to determine the best plan provider and their benefits can help you decide where to open one.

What is a Health Savings Account?

A Health Savings Account or HSA can maximize your health savings. They are tax-advantaged saving accounts to pay for out-of-pocket medical expenses like doctor visits, deductibles, copays, and medicine.

An HSA can function primarily for spending on qualified out-of-pocket expenses or can also be used to save and invest the excess money you don’t spend on medical costs for your future.

At the end of the year, any unspent HSA money rolls over, so you can use the money in the future. With an HSA, you receive three tax benefits:

- Tax-free contributions: Contributions you make as an individual can be deducted from your taxes

- Tax-free gains: Earnings on the money in your account grow tax-free

- Tax-free withdrawals: You do not pay taxes on money taken out for qualified medical expenses (Here is the IRS definition of that qualified medical expenses.)

HSAs can be employer-sponsored if you have an employer or self-employed individuals who can open their accounts.

Related: High Deductible Health Insurance Plan Plus HSA

Can I Open a Health Savings Account?

If you have an HSA-eligible High Deductible Health Plan, you can have an HSA.

For a plan to be considered HSA-eligible by the IRS, it must meet criteria like minimum deductible amounts and maximum out-of-pocket expenses. You are not eligible if someone else can claim you as a dependent.

If, like me, you are on one of the popular healthsharing plans, then you are not eligible for an HSA.

How to Open a Health Savings Aaccount

Opening an HSA is as easy as setting up a new bank account. More effort goes into finding the right provider than the actual setup. You’ll need to provide the institution with information about yourself to open an HSA account.

Most accounts can be set entirely up online if you prefer. When the account is set up, your provider will let you know how to contribute to your HSA.

For me, the sign-up process was pretty straightforward. I went down to the credit union branch with my ID and a check for $1,000 as an initial deposit for my account.

There wasn’t a minimum requirement. It’s just what I chose to fund the account with initially.

Next, they gave me some forms for future contributions and sent me on my way. A few days later, I received a debit card for out-of-pocket health care expenses.

The great thing about the HSA is that, unlike a flexible spending account (FSA), the contributions do not have to be used within the year. The balance rolls over each year, so you can continue to use that money for qualified medical expenses.

Related: HSA vs. FSA: Which is Better?

HSA Contribution Limits

If this is your first year to have an HSA, contributions are further limited by the number of months you’ve been on an eligible plan. Read more about HSA contribution limits.

Where to Open a Health Savings Account

Start with your goals when trying to figure out where to open an HSA. How will you use the money you deposit?

Do you plan to use your contributions for only covering health care expenses, or do you also want to save and invest in excess contributions?

Your goals will help you pick the best HSA provider that aligns with how you want to use your money.

If you plan to save more than you spend, investment account options and interest rates will be determining factors when selecting a provider. Versus if you use your account to pay for out-of-pocket costs.

Your health insurance company may have a preferred HSA provider with which you can sign up. Banks, credit unions, insurance companies, and financial brokers are other places you can open HSA accounts.

For convenience, if you like your bank or credit union, that might be the place to start. My banks won’t cut it. I use Chase and

After doing little more research on HSAs, what stuck out to me, was the monthly fees associated with the accounts for smaller balances. No thanks!

That’s when I decided to call my local credit union to find if they had an HSA free of monthly fees. They did. Because they charged zero monthly fees, we decided to go with our credit union to open my HSA.

If an HSA pays an interest rate and you like to keep a high balance in your account, it might make sense to pay a monthly fee. We’re just starting our HSA, so I’m sticking with a no-fee account.

How to Pick an HSA Provider

There are hundreds of places to open an HSA. Most HSA providers have similar fees and features, so it’s best to find one that works for you. Here are some things to consider when selecting a plan provider.

- Account fees

- Minimum balance requirements

- Banking options (do they offer debit cards for spending)

- Investment options and associated fees

- Customer support (can you call someone for help)

- Easy to manage (is it convenient)

- Interest rates

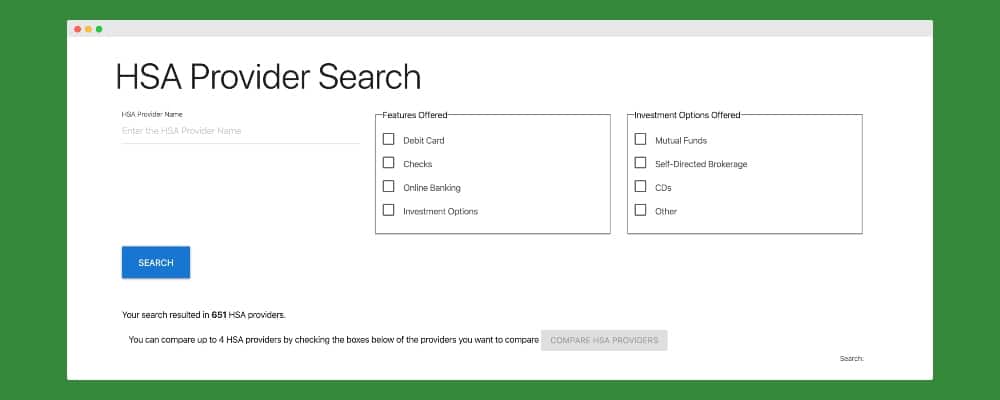

You can search for an HSA using HSA Search to compare providers. Their search tools give you the option to search by your preferred features like debit card availability, online banking, and investment options.

Once you filter the features, you’re looking for. You can review and compare different providers. They give you reviews that include user ratings, feature lists, interest rates, fees, and investment options. Comparing plans can help you make an informed decision to reach your HSA goals.

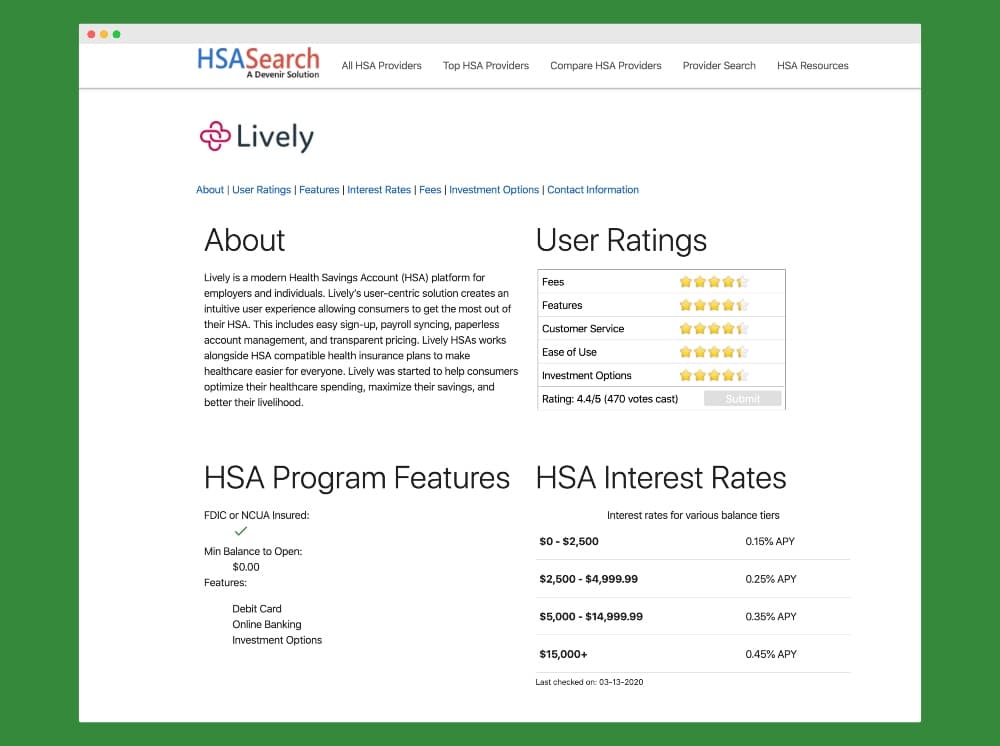

Use Lively Health Savings Accounts

One of the best HSA accounts for both spending and investing is Lively. Lively is an online provider of HSA accounts for individuals and families.

Their mission is to make it easy for people to save on health care costs now, so they have more money for future expenses.

Their accounts are free for individuals and $2.95 per employee per month, with no minimum balance required to open a Lively HSA.

They make it simple to pay for health care expenses like doctor’s visits and medicine with their debit card. Their mobile app lets you track and manage your HSA spending from anywhere.

It’s available for iOS and Android. The app allows you to view your account activity, manage your debit card, and upload receipt photos.

Open an account with Lively here.

With Lively, you can also invest your HSA funds with TD Ameritrade. You can amplify your savings with investment options like stocks, bonds, and ETFs.

One thing to note is you will need to set up a TD Ameritrade Self-Directed Brokerage Account. Even if you have an existing TD Ameritrade account, you must set up an account through Lively.

The good news is TD Ameritrade does not charge fees for online stock and ETF trades. Some fees do apply, like a $25 charge for no-load mutual funds. You can also set up automatic transfers making it easier to invest.

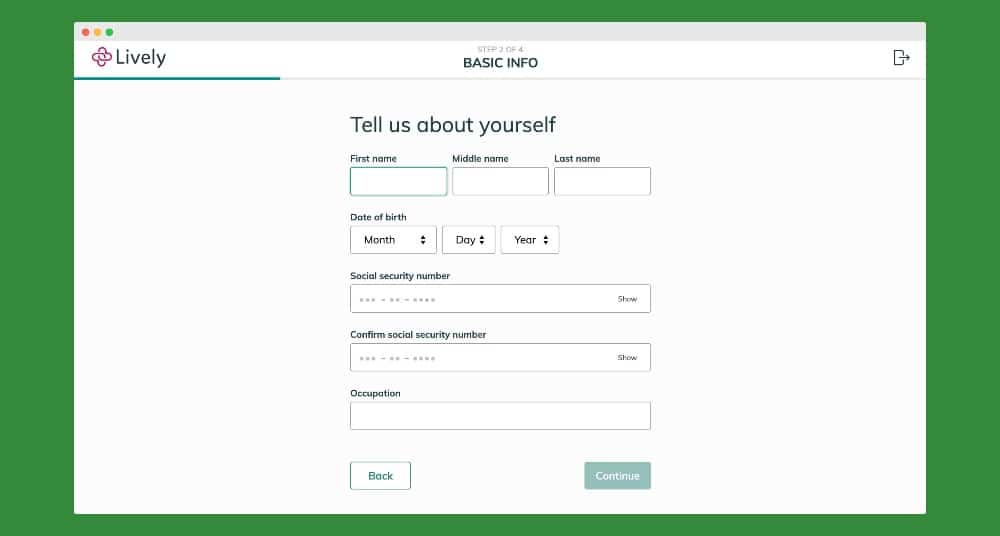

Opening an HSA with Lively is simple and takes less than five minutes. To begin the set-up process, they ask you the necessary information about yourself and your contact information to start the account set-up.

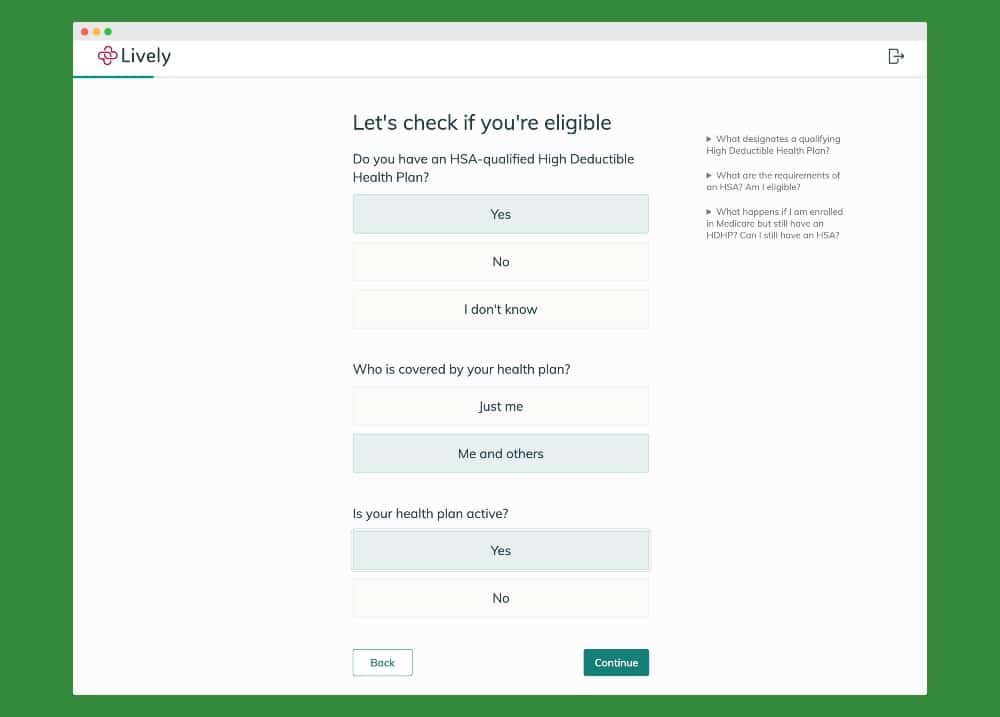

Once that’s complete, they ask questions to confirm you’re eligible to set up an HSA.

After your account is created, they make it simple to link your bank account and either set up recurring contributions or a one-time contribution to fund your HSA.

If you have questions about how much to contribute, Lively has a resource section with guides and calculators to assist in your decision-making.

You can transfer your account to Lively if you have an HSA with another provider. Lively’s customer support is available by phone, email, and chat to help you set up your account or resolve account problems.

Lively is an easy way to get an HSA account started and funded right away. The customer support, resources, and mobile app make getting help and managing your account convenient.

Bottom Line

When opening an HSA account, begin with the end in mind. Will you use the account primarily for spending, or will it be more like a savings account or investment account?

Knowing what you want from your HSA will help determine where and how you will start an HSA.

Have you funded an HSA? Where did you open it?

![Save Money on Healthcare Without Using Obamacare [Our 2019 Liberty HealthShare Review]](https://ptmoney.com/wp-content/uploads/2018/11/Liberty-screenshot-2-768x383.png)

Like Philip I went with a local Credit Union. They do have a small monthly charge, but having it local has been nice. Other people I know use HSABank and Alliant Credit Union has had good rates on HSA accounts in the past.

cd :O)

I have my HSA through Chase because it was convenient for me even with the $2.50 monthly fee. My company did not offer funding of the HSA so I had to find my own carrier and since I have Chase cards and a checking account I wanted the easy access of that. I just started the HSA so my balance is low but it looks like the best bet would be for me to stay with Chase for now and then move to the second one in the image as they waive the monthly fee AND offer a higher rate of interest.

Good point that you bring up, Jenna. Another good post idea: new changes for 2011 with FSAs and HSAs due to the new healthcare law.

I didn’t get an HSA, because I don’t have a co-pay through health care provider and HSA won’t cover non-prescriptions next year. Since I don’t have many perscriptions I didn’t think it was necessary.

I’m usually not a fan of using non-retirement accounts for retirement purposes (or vice versa), but it’s worth a look.

I think it would make for a great follow-up post. My financial planner friends tell me they often recommend this strategy to clients, but I don’t think very many people would think of it otherwise.

Good point, Matt. I guess I need to do some investigating into using it as an extra retirement account. Would make for a good follow-up to this post.

We have our HSA at First American Bank in the Chicago area. For their basic account, there is no minimum balance requirement and there are no fees. For their HSA Plus account, which offers more investment choices, there’s a $4/month fee. Since we tend to use all the money we put into the account every year, we’re happy with the no-fee basic account. For those who treat their HSA as added retirement savings, it may be worth it to go with the Plus account.