How to Invest Money: What You Need to Know to Get Started

Making investment decisions can be a scary and overwhelming process. We are constantly bombarded with conflicting information about the market. One moment everyone’s excited, and a few hours later they are all disappointed.

We hear that investing is inherently risky, but also that it’s the clearest path to wealth. And then there’s the alphabet soup of investing lingo, from IRAs to ETFs.

So just how are you supposed to feel comfortable investing your hard-earned cash?

Investing your money does not have to be nerve-wracking. First, understand your goals and how much risk you are willing to take. Then familiarize yourself with a few different investment options and get help when you need it. Whether you have $50, $500, $5,000, 0r $50,000 to invest, you can feel confident about making your money grow.

Here is everything you need to know about growing your money with savvy investments:

Table of Contents

- How to Invest Money

- Investment Vehicle Options

- Investment Strategies

- Tax-Advantaged Investing vs. Taxable Investing

- Will Social Security Be Enough in Retirement?

- Where to Open a Taxable Account

- What Undermines Your Investments

- Summary

How to Invest Money

How to invest your money is often the first question for newbie investors. You can’t show up at the NYSE with your extra cash and start shouting “Buy!” and “Sell!” So where do you get started?

Create an Investment Policy Statement

As with any big project, it’s always a good idea to figure out what you want before you get started. That’s why it’s a good idea to start by creating an investment policy statement for yourself.

Such a personal statement can help you clarify your objectives and organize your financial planning. Whether you intend to handle your own investing or work with a financial professional, your statement can give you a roadmap.

Morningstar has a great outline to help you get started.

Here’s what your investment policy statement will include:

1. Your investment experience.

The policy should establish your investment knowledge base.

Are you an experienced investor, or are you still learning? A financial advisor who understands this will have a better idea of how to communicate information effectively. And if you are doing your own investing, then establishing your experience can help you figure out what homework you need to do.

2. Your investing goals.

The next step is to define your financial goals: what are your goals, how much will they cost, and when will you need the money? For example, one goal could be to have one million dollars at retirement in twenty years.

Related: How to Invest for Passive Income

3. Your desired asset allocation.

The final part of the document should focus on your asset allocation decision. Based on the discussion on financial goals, you can outline your risk tolerance and select investments that match your objectives and appetite for risk.

Less experienced investors should consult a financial advisor to help them complete this section. If you have done a good job defining your financial goals, a professional and ethical financial advisor will have the right pieces of information to make the proper choices on your behalf.

In addition to helping you understand your financial picture, an investment policy statement also has some legal advantages. Your financial advisor must take your investment policy statement into consideration when choosing your investments. Though some financial advisors may try to sell investments that improve their commissions, rather than your bottom line, a well-crafted investment policy statement can help prevent this unscrupulous practice.

Ultimately, getting started with investing means figuring out what you want, before you make a single investment transaction.

Investment Vehicle Options

There are a number of different types of investment vehicles available, and it’s important to understand what they each offer. Here is a breakdown of the types you are most likely to encounter:

Savings Vehicles

By default, savings rates are lower than investing rates. It’s a classic case of risk vs. reward. But the fact of the matter is that saving money is investing.

When you save you are investing in the US dollar. So, even if you only have a savings account and no true equity account (i.e. stocks, mutual funds) you are an investor.

Even high-yield savings accounts and other savings vehicles will generally not see the same kind of growth that investments can expect over similar investment horizons. But even with their dismal rates, savings vehicles like money market accounts, CDs, and savings accounts can still be a good option for certain situations.

They provide liquidity (as long as you use no-penalty CDs) and protection (via FDIC). For many short-term savings goals, like an emergency fund, these tools still make sense. But they aren’t going to grow your money anytime soon.

However, since savings vehicles are a type of investing, make sure you’re thinking like an investor when you choose one. Know your objective and risk tolerance when shopping for the right savings vehicle. Consider your asset allocation, which includes sub-classes of bank savings, money market accounts, certificates of deposits, actual gold, and even cash.

Commit to getting solid returns (and moving your money if you can get a better return elsewhere,) and keep track of your savings balance and rate.

See also: The Best High Yield Online Savings Accounts

Mutual Funds

A mutual fund is an investment company that pools the money from several different people (investors like you) and then buys into stocks, bonds, money market accounts, or other assets, like commodities. Shares of this company are then offered for sale.

Mutual funds, therefore, have to be managed by a fund manager, who collects all this money and makes sure to buy and sell all the right stocks, bonds, etc.

One thing I learned recently when studying mutual fund basics is that these funds can make money for you in three different ways: dividend payments (from the stocks owned within), capital gains (when stocks are sold within the fund), and increased net asset value (NAV).

When I typically think about mutual funds, I just think in terms of increased NAV. I forget that some stocks pay dividends and that managers are constantly selling winning stocks to lock in gains. I guess because these gains and dividends remain in the fund, you don’t really think about it.

Why Invest in Mutual Funds

There are several reasons to like mutual funds. Mutual funds allow the beginning investor to own a diverse set of stocks, bonds, etc. without having to use large amounts of money to buy into each asset class or stock. Instant asset allocation.

For instance, with the American Funds Mutual Fund (AMRMX), you can pay $250 and get several shares. In each share of this fund, you’ll be buying into U.S. stocks, fixed income, cash, and international stocks. And within your stock purchase, you’ll own pieces of Merck, AT&T, Microsoft, IBM, and many, many others.

To get this kind of diversity with your own money, you’d need a heck of a lot more than $250 (the fund minimum). And you’d need a lot of time on your hands. Mutual funds don’t just sit around on the same mix of investments. They are constantly moving in and out of different stocks and bonds to try to maintain a good performance and to hold true to the fund’s original goals.

So with a mutual fund, you get a full-time professional manager to handle all of this. The trade-off with mutual funds is, of course, that you have to pay this professional to manage all this for you. James Dunton has been managing the AMRMX fund for 39 years. I’m sure he’s paid well for his services.

Risk Involved with Mutual Funds

Risks involved with mutual funds are the same as any other security investment. The investment can lose value. There is also the risk of too many expenses. Mutual funds are often heavily managed. Therefore they come with a cost. When these costs are too high, and your investment return is too low, you could be losing money.

Different Types of Mutual Funds

The three main types of funds are money market funds, bond funds, and stock funds. Money market mutual funds generally try to preserve value. This is considered the safe haven in most portfolios.

Although, as we’ve discussed before, they are not FDIC insured like a money market account. Bond funds are more risky funds, and they aim for a low return. Stock funds are the most popular and diverse mutual fund category. They come in all shapes and sizes.

Four common examples of stock funds are growth funds, income funds (dividend stocks), index funds, and sector funds. Another hybrid type of mutual fund is the target-date fund, which invests in cash, bonds, and stock, getting more conservative as I age.

I currently use the Vanguard 2040 fund. What type of stock funds do you own in your 401K?

Mutual Fund Expenses

The fees break down into two basic categories: shareholder fees and annual fund operation expenses. Shareholder fees are usually charged when you buy or sell. Annual Fund Operation Expenses are charged on an annual basis just for holding the funds.

If funds are described as no-load, they are referring to the shareholder fees. When you compare “expense ratio” know that they are referring to total annual fund operation expenses. Fund companies don’t make it easy to locate the expenses and fees associated with funds, so be prepared to research this before buying into a fund.

How to Invest in Mutual Funds

Mutual funds can be purchased at a mutual fund company directly like at Vanguard or Fidelity. They can also be purchased at a stockbroker, a bank, or even with a CFP.

Reading Your Mutual Fund Prospectus

A prospectus is a document that provides investors with information about the investments that make up the mutual fund, as well as other details of the company’s business.

You can obtain prospectuses online–either directly from the company’s website (generally found within the Investor Relations section) or on the SEC’s Electronic Data Gathering, Analysis and Retrieval System (EDGAR) site. The EDGAR website allows you to search for specific companies’ prospectuses and other filings.

There are two types of prospectuses: statutory and summary. The statutory prospectus is the long-form, traditional prospectus that most investors are familiar with. The summary prospectus, on the other hand, provides key information on the fund in three to four pages. While both types offer important information, you will be able to get more detailed information from the statutory prospectus.

When reading a prospectus, you want to look at the following information:

1. The investment strategy

If your personal investment strategies and objectives do not match those listed, it’s time to move on to the next prospectus. Since every prospectus can be written a little differently, you may find this listed in the table of contents as Risk/Return, Investment Objectives, Primary Strategies, or Primary Risks.

2. Investment returns

This information is often found in two tables in a prospectus: one that compares the returns of fund in question to the 1-, 5-, and 10-year returns of index funds (like the S&P 500), and one that shows the annual or quarterly returns for the past 10 or so years.

3. Fees and expenses

You can find the information on these expenses in a section generally titled Fees and Expenses. Look for the Net Annual Fund Operating Expenses, and you will find the expenses expressed as a percentage. In addition, check to see if there is a section listed as Investment Adviser and Management Expenses. This will let you know if there is a performance bonus to the investment manager in years when they outperform their benchmark.

Finally, check the turnover cost. Higher turnover–when the manager buys and sells securities more often–can mean additional costs and additional taxes if your fund is in a taxable account.

Mutual funds come in a number of different flavors, so it’s a good idea to understand what each type is meant to do:

Dividend Mutual Funds

Dividend-paying investments are those that provide a little extra money. In the case of dividend-paying stocks, every so often (usually each quarter, but it can be monthly or annually) a company will take a portion of its profit and distribute it among its shareholders.

If you own stock in a company that pays dividends, this is extra money that you receive just for owning shares. You can spend it as you like (but remember you have to pay taxes on it). Many companies have reinvestment plans that allow you to automatically use dividends to buy more stock. This is like getting free shares.

With dividend mutual funds, the idea is the same. Every so often, the investments in the fund pay dividends, and the fund then distributes them to those who invest in the mutual fund. Many dividend mutual funds, though, simply use the dividends to help you buy more shares of the mutual fund, boosting your holdings — and your potential earnings.

Considering Dividend Mutual Funds

Beginning investors (and others) might do well to consider dividend mutual funds for their portfolios. It is true that many dividend-paying stocks don’t experience the kind of short-term returns that you can see with growth stocks, but in many cases a dividend-paying investment is one that is solid, offering regular profits.

While you won’t see huge returns, you won’t be subject to the same risk of loss. You are likely (but never guaranteed) to see regular, if modest, returns. Mutual funds provide you a way to start investing without having to risk a great deal on any one stock. Stock picking is not as easy as it seems, and if you choose a dud, you could regret it. At least with a mutual fund, you are spreading the risk a bit.

If a few investments in the fund tank, there are likely to be winners that make up for it. In Dividend mutual funds, the nature of dividend-paying investments helps protect you further from complete losers. Plus, you get the added bonus of extra money every quarter — money that can be used to boost your returns.

Money Market Mutual Funds

Money market mutual funds, or money market funds, are different than money market accounts. A money market fund is a type of mutual fund that invests in non-long-term, liquid assets like US T-bills, which provide a safer, more-stable investment. The goal of the fund is to maintain a price per share of $1.

Not to be confused with money market accounts. Money market accounts are a short-term savings product offered by banks that are FDIC insured.

Who Uses Money Market Mutual Funds?

Money market mutual funds are typically where investors keep the funds that they want in “cash”. So, when you see an asset allocation pie chart and see the small portion for cash, this is typically where those funds are kept. Most mutual fund companies (places where you’d typically have your 401k or IRA) like Fidelity and Vanguard have money market mutual funds as the safe haven account.

And even at the best online stock brokers, active traders move their funds in and out of money market funds to go from a safe investment, low-reward investment to a more volatile, potentially more rewarding investment.

Are Money Market Mutual Funds Safe?

While they aren’t insured by the FDIC like the money market account, money market mutual funds are regulated by the SEC against “breaking the buck” (i.e. dropping value below $1). And Congress is currently in the process of trying to legislate a way to strengthen consumer confidence in these funds. There is a debate as to how that can best be accomplished.

Why Not Just Use a High-Yield Savings Account?

So why are these funds used over money market account and online savings account? It used to be that money market funds could provide a better return for your cash that savings accounts. True. But nowadays, the high-interest online savings accounts provide equal returns for your cash.

So what’s keeping investors from moving all their cash into these savings account? The main reason is flexibility. The money market mutual fund is housed under the same roof as the other mutual funds they are invested in. Moving money between accounts (even within an IRA or 401K) is a snap. Also, online savings accounts have limits on the number of monthly transfers you can make in and out of the account. Thus, the money market mutual fund is still around.

The Best Money Market Mutual Funds

So how do you find the best money market mutual fund? Well, my own opinion is that you’d be short-sighted by picking a mutual fund company based on how good their money market mutual fund is. You’re with a mutual fund company because you like their stock funds, not money market funds. But, if you have to make that decision, I’d let expense ratio be the deciding factor. Luckily, you can typically find low-expense money market funds at places where you find low-expense stock mutual funds. I’d start with Vanguard and Fidelity. Here are a couple of their top-performing, low-cost money market mutual funds:

- Vanguard Prime Money Market Fund (VMMXX) – $3,000 Minimum, Expense Ratio 0.16%, 5-Year Return 1.22%

- Fidelity Money Money Market (SPRXX) – $o Minimum, Expense Ratio 0.42%, 5-Year Return 1.07%

If you’re strictly looking for a high return on your cash (you don’t need to move the money a lot), while maintaining the top-notch security that the FDIC provides, just go with a high-yield savings account or money market account.

Index Funds

This type of mutual fund is set up so that the performance of the fund should match the performance of a specific market index. For instance, an index fund that is matched with the S&P 500 should mirror the growth (or potential losses) of the S&P 500.

Index funds offer lower risk because they have built-in broad market exposure. They are also lower-cost than other types of mutual funds because they do not require hands-on maintenance from a fund manager and they have little turnover within the portfolio.

Because of all of these benefits, retirement accounts often use index funds as the core of their investing strategy.

Target-Date Funds

Target-date mutual funds automatically adjust their asset allocation as the fund ages.

For example, a target fund might be invested in 90% stocks/10% bonds right now, but by the time you retire, it might be invested in 40% stocks/40% bonds/20% cash. This means investments are automatically balanced appropriately for their time horizon and risk tolerance. You no longer have to manually rebalance your asset allocation.

See also: (VFORX) The One Beautiful Fund I Use to Invest for Our 2040 Retirement

Exchange-Traded Funds (ETFs)

ETFs are a group of investments put together and usually tied to an index (like index funds) that you can buy shares in and trade like stocks. This means you get the diversification that comes with grouped investments, the low-cost that comes with “passive” funds, and the flexibility of someone trading in stocks.

In addition to the broader funds that make up the bulk of ETF trading, you can invest in commodity ETFs (i.e. Copper ETF), small-sector ETFs, foreign ETFs, etc. Not all ETFs are created equal. Some are more actively managed and thus, more expensive.

ETFs are often compared with index funds, but unlike index funds, ETFs usually require you to pay a broker commission, don’t generally allow for an automatic investing plan, often have fewer “internal” expenses, can help you avoid capital gains taxes in taxable accounts, and can usually be purchased in smaller amounts.

You can purchase shares in ETFs at one of the discount online stock brokers or at a mutual fund company like Vanguard.

See more: The Best Online Stock Brokers for Cheap Stock Trading

Stocks

These investments are what most of us think of when we talk about investing.

Owning a stock means you own a piece of the company that issued the stock. So you have a claim on a portion of the assets and earnings of the company whose stock you own. When the company’s valuation goes up, the value of your stock goes up. As we all learned from Trading Places, the goal of buying a stock is to buy low and sell high.

Bonds

Unlike stocks, bonds do not represent ownership of a company. Instead, when you purchase a bond, you’re buying the company’s debt. You have effectively loaned the company money when you buy a bond.

In exchange, you receive interest payments and the promise of repayment in the future. That repayment date is known as the maturity date.

Real Estate

Investing in real estate has long offered a solid path to investment growth. Not only does real estate offer you the possibility of ongoing income via rentals, but your investment property can also appreciate over time. However, investing in real estate can be a bit more complicated than simply choosing stocks, bonds, mutual funds, or ETFs.

Traditionally, real estate investment means making a direct purchase of a rental property. This requires a healthy down payment and may also need some on-the-ground work, especially if you plan to manage your property yourself.

Read more: The Very First Thing You Have to Do When Getting into Real Estate

Real estate investing has become somewhat easier now that you can invest in REITs, or real estate investment trusts, with as little as $10 for your minimum investment. REITs include a wide range of offerings that invest in a broad range of real estate. The best thing about REITs is that you can simply buy into them through your brokerage account.

Read more: 6 Ways to Invest in Real Estate (from $10 to $100,000)

Finally, real estate crowdfunding with platforms like PeerStreet has made it possible for accredited investors (those with an annual income of $200,000 or a net worth north of $1 million) to invest their money in real-estate backed loans. This investment type is different from a more traditional REIT because it provides more transparency and flexibility for the investor.

In addition, crowdfunded real estate often has a fairly low minimum investment of around $500 to $1,000, depending on the platform.

Read more: My $10,000 Real Estate Crowdfunding Experiment with PeerStreet [Review]

Investment Strategies

Simply knowing what your options are for investing may not help with putting together a plan for your own investment portfolio. That’s where investment strategies come in. Understanding how various strategies can affect your money, your investment timeline, and your tax burden, can help you determine the best choices for your portfolio.

Dollar Cost Averaging

Dollar cost averaging is the act of investing your money on a set schedule, with a fixed amount or percentage, regardless of market conditions. For instance, you decide that you are going to invest in a stock, mutual fund, or other investment each month with a contribution of $100 until you reach some goal or pre-determined date.

Using this method, your $100 buys more or less depending on the current value of your investment.

If dollar cost averaging sounds a lot like what you already do with your company 401K, you would be right. Most people already take part in this “strategy.” It aligns perfectly with the goals of the long-term, buy-and-hold investor, who is only able to invest a certain amount each month.

By investing on a schedule, you are intentionally ignoring day-to-day market prices, and putting trust into the idea that over time (a long time), a diversified portfolio will win more than it loses. The person investing with this strategy doesn’t panic when he/she sees a down market, they just enjoy the fact that they can now buy more with their money.

This strategy also reduces the risk that you’ll pay too much for investments. If we’re talking about a single investment made by a short-term investor (less than five years,) then dollar cost averaging (over a 1 or 2 year period) reduces the risk that you’ll buy too high.

Does dollar cost averaging mean a better return on your investment? No. But it does mean you’ll be paying less than the average price for your shares across a set period of time.

Asset Allocation

Though we briefly discussed asset allocation above, it’s important to talk about how strategic asset allocation can affect your portfolio.

Asset allocation is the process of splitting up your investment portfolio into the different asset classes. Chiefly, this involves putting different amounts of money into the major three classes of assets: stocks, bonds, and cash. Other asset classes include real estate, commodities, precious metals, other alternatives like wine investments, and equity holdings.

You can also split your assets up even further into different types of stocks. Or cut it the other way and split it up between different industries. If you keep drilling down, you can allocate your funds across thousands of different asset types.

However, you should remember that asset allocation doesn’t equal diversification (i.e. not putting all your eggs in one basket.) Diversification is the act of spreading out your investments into different asset classes, industries, and even countries to achieve a balance of risk and reward. A better way of explaining the difference might be to say that you can have an asset allocation strategy that is not diversified.

To make sure you have an asset allocation strategy that works for you, make sure you incorporate the following steps into your portfolio management:

- Understand the asset classes. Learn about stocks, bonds, and cash. Understand the risks involved in each.

- Get to know your risk tolerance. Take one of the many tests online to determine your risk tolerance. Be sure to retake the test every five years as your assets grow and situation changes.

- Look at examples of “proper” asset allocation. Study the different strategies out there. Take note of what you like and dislike.

- Make sure your portfolio is allocated according to your risk tolerance. Finally, make sure your portfolio matches up with what your goals are. Re-balance your portfolio each year to ensure you stay in line with your goals.

Tax-Advantaged Investing vs. Taxable Investing

Mitigating your tax burden is an important part of savvy investing. So it’s a good idea to understand the difference between tax-advantaged and taxable investing.

Tax-Advantaged Investing

Whether they know it or not, most people are already doing tax-advantaged investing through their 401(k), which is great. 401(k) accounts and traditional IRAs are tax-advantaged because they offer a tax deferment.

What that means is you can deduct your annual contributions to these accounts from your yearly taxes. This lowers your current tax burden and can help you free up money in the budget for investing. Your money also grows tax-deferred, so you will not have to pay taxes when your account gains capital or earns dividends. But you will have to pay ordinary income tax on your withdrawals from these tax-deferred accounts once you reach retirement.

Tax-deferral is not the only way to enjoy tax-advantaged investing, however. You can do even more tax-advantaged investing through a Roth IRA (which uses after-tax dollars.) The advantage of investing in a Roth IRA is that its earnings are tax-free, provided you wait to make withdrawals until after you have reached age 59 1/2.

Read more: What Is a Roth IRA and How Does It Work?

When it comes to tax-advantaged investing, I recommend the following sequence:

- 401k to Get the Employer Match

- Roth IRA to the Max

- Back to the 401k to the Max

See also: Traditional and Roth IRA Contribution Limits for This Year

This approach will help you avoid taxes now and in the future. The government, via the IRS, is trying to encourage you to save for your retirement so you won’t simply rely on Social Security. That’s why we have these types of accounts. And that’s why most of these accounts come with stipulations about leaving the money where it is, for its intended purpose.

Read more: Roth IRA CD: Tax-Advantaged Retirement Investing without the Risk

Taxable Investing

Taxable investing is taking your after-tax dollars and investing it without a tax-advantaged account. Simple, right?

The key thing to remember is to only invest money here after you’ve exhausted your options in the tax-advantaged areas. These investments will be taxed before you put the money in and the earnings on the investments will be taxed.

Taxable accounts can be opened up at the same places as tax-advantaged accounts, at banks and investment firms. But the best places are the ones who’ll let you trade cheaply since you’ll theoretically be doing that more often (because of no limitations by the IRS.)

For the most part, you are able to invest in the same types of investments in or out of tax-advantaged accounts. The account, like a Roth IRA, is just a place to put your investments.

So when exactly should you plan on investing in taxable accounts? There are several reasons you might be interested in starting with taxable investing:

- When You Max Out Your Options: When you’ve maxed out your annual 401K contributions, your Roth IRA contributions, and your SEP IRA contributions, if any are available to you, a taxable account comes next.

- When You Reach Income Limitations: Secondly, if you earn above a certain amount of money, you will not be able to invest in a Roth IRA. Therefore, after you maxed out the 401K, the next best choice is probably taxable investing.

- When You Want Flexibility: Unlike a 401(k) or IRA, with taxable investing, you can move your money in and out as you please. You do not have to wait for retirement to access the money.

- When You Want to Invest in Tax-Free Investments: Lastly, there are some investment types that are tax-free (i.e. tax-free bonds) that you can only get in a taxable investment account.

Should You Have Both Tax-Advantaged Accounts and Taxable Accounts?

There’s no harm having both types of accounts.

If you’ve reached one of the milestones listed above then it’s probably time for you to begin with a taxable account. However, make sure you have your debt situation under control and a decent emergency fund built up prior to shoving a bunch of extra money into one of these accounts.

Will Social Security Be Enough in Retirement?

I can’t believe I’m trying to tackle the subject of social security right now. It’s super complex in its history, very controversial by nature, and the future of its solvency and makeup are unknown.

But, regardless of all of that, you and I both pay into the Social Security system. So it’s worth it to look close enough to at least provide an estimate of how much of your money you’ll be getting back, right?

- When people use the term social security they are actually referring to the social insurance program, the Federal Old-Age, Survivors, and Disability Insurance program established by the Social Security Act of 1935.

- Social Security is collected through FICA payroll taxes, which is 7.65% of your earnings up to $106,800.

- The current normal retirement age for full Social Security benefits is 67.

- The average monthly benefit for current retirees is around $1,503 a month.

- Social Security is the single biggest expenditure of the federal government.

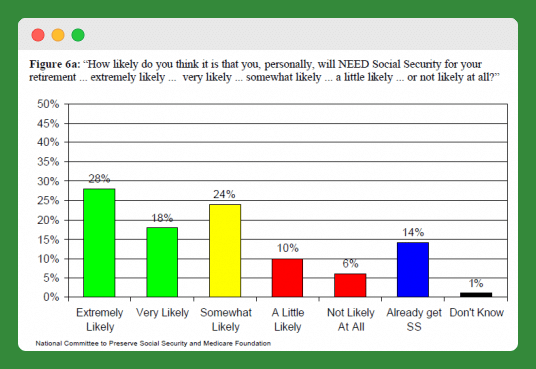

From my understanding, Social Security started out as a social program to help those with the most dire needs in our country. Now it seems that social security has become the retirement program for just about everyone. Check out this chart from a recent Social Security survey put on by the University of New Hampshire Survey Center.

That’s crazy. Almost 50% say they are at least very likely to need Social Security in retirement. What about 401Ks, IRAs, etc. Is all this just lost on everyone? Maybe I’m misinterpreting what “need” means in this survey. But I don’t think I’m misinterpreting the fact that Social Security has grown to be more than it’s original intention.

How Much Are You Estimated to Get?

If you want to know how much you can expect in retirement from Social Security, visit the SSA’s estimator page.

They also have a life expectancy calculator there. Puts me at 86 when I finally croak. You should also be receiving an annual statement from the SSA. You’ll be able to tell from that statement what you can expect in retirement.

But all this depends on the future solvency of Social Security. Will they continue cost of living increases (no increases for the last 2 years)? Is it possible they will start paying only a % of your benefit? Will they have to change the normal retirement date?

The Future of Social Security?

You hear a lot of hype about how Social Security is failing, or that it won’t be around by the time I retire. What’s the truth? Well, by the above chart I’d say that American’s won’t let it fail. When you have that many people depending on it, it’s going to remain a priority.

I just don’t see Social Security ever going away. It’s a ponzi scheme of sorts in that the earnings of the currently employed are needed to pay those receiving the benefits. That being the case, everyone who has paid in at least 10 years of Social Security feels like they deserve to get those funds returned to them as benefits. So, once you work for 10 years, there’s no way in heck you’d say drop the whole thing. You put your money into the system, therefore, you don’t want it canceled.

The Trustees Report

Enough of my ramblings. What do the actuaries say? The Social Security trustees put out an annual report opining on the future of social security. They are required to do this just like any other investment house. Here’s what they said in their 2020 report.

“In 2019, Social Security’s reserves were $2.9 trillion at the year’s end, having increased by $2 billion. The Trustees project that under the intermediate assumptions, the Old-Age and Survivors Insurance (OASI) Trust Fund will be able to pay full benefits on a timely basis until 2034, unchanged from last year. The Disability Insurance (DI) Trust Fund is now projected to be able to pay full benefits until 2065, 13 years later than indicated in last year’s Social Security report. Disabled-worker applications have declined substantially since 2010 and the number of disabled-worker beneficiaries in current payment status has been falling since 2014. Accordingly, the Trustees have again reduced the long-range disability incidence rate assumption in this report.

The projected reserve depletion date for the combined OASI and DI funds is 2035, the same as in last year’s report.1 Over the 75-year projection period, Social Security faces an actuarial deficit of 3.21 percent of taxable payroll, increased from the 2.78 percent figure projected last year. The main causes are (1) the repeal of the excise tax on employer-sponsored group health insurance premiums above a specified level (commonly referred to as the “Cadillac tax”), which slows the projected growth in real covered earnings and results in less payroll tax income, and (2) changes in assumptions including lower anticipated fertility rates, consumer inflation, and interest rates. The actuarial deficit equals 1.1 percent of gross domestic product (GDP) through 2094.”

Can You Count on It?

If you go by the 2020 report, it looks like if you are retiring in less than 14 years (age 40 or older) you will receive your full benefit.

But let’s say you do get your full benefit. Is the future equivalent of $1,503 a month going to be enough for you in retirement? If that’s all you have at that time, then you’ll likely still be poor. Studies show that 12% of those on Social Security still live below the poverty line. Not a dream retirement for sure.

The moral of the story is that there are a lot of moving parts here, but most of us can probably count on the future equivalent of at least $1,503 in retirement from Uncle Sam.

My advice is to play it ultra-conservative and forget about Social Security. Don’t count on it. If you get it, great. If not, no worries because you have your retirement set using your 401K and your IRA.

Where to Open a Taxable Investing Account

In the past, it was next-to-impossible to become an investor without partnering with a financial professional. These days, however, the internet and financial technology have lowered the barriers to solo taxable investing. Specifically, there are now a number of online discount brokers and robo-advisors available.

A discount broker offers limited investment services, allowing you to invest with lower commissions. Many discount brokers charge a flat fee for trades that you make. Discount brokers often offer a limited selection of investment options, though. You may be limited to stocks, mutual funds, CDs, ETFs and other basic investment products.

You do have the option, with many discount brokers, to call and talk with a professional, but such sessions will cost you.

Robo-advisors, on the other hand, are automated online investment platforms. These platforms are designed to keep your costs low because they use computer algorithms to manage your portfolio. Robo-advisors are more likely to be the set-it-and-forget investment option, while discount brokers are more geared toward DIY investors.

You can easily get started as an investor with any of the following online platforms:

Ally Invest

Ally Invest is a relative newcomer to the online discount broker world, but it stands out because it offers both self-directed and cash-enhanced managed accounts with low minimum balances. It also offers low-cost stock trading ($4.95.) It’s a great option for active traders and offers forex and options trading.

Check out our full review of Ally Invest here.

Betterment

As one of the first ever robo-advisors, Betterment has a long history of success in helping people invest their money. Betterment offers goal-oriented investing tools that help investors build a diversified portfolio and save for the future.

Betterment Digital charges 0.25 percent of your account balance and has no account minimum.

Check out our full review of Betterment here.

M1 Finance

If you not only love the idea of DIY investing but also want to choose your own investments (rather than have them suggested to you, as other robo-advisors do), then M1 Finance might be for you.

This self-directed robo-advisor has you choose your investments, then manages your portfolio for you, including periodic rebalancing and dividend re-investing.

Check out our full review of M1 Finance here.

Empower

Though it offers everything from budgeting to account aggregation, Empower’s biggest claim to fame is its investment advice.

Once your investable assets reach $100,000 (the minimum investment,) the platform assigns you a personal advisor. If you choose to invest with Empower, your money is placed in a diversified portfolio of exchange-traded funds (ETFs) with access to their “Smart Weighting” technology which creates greater diversification.

Check out our full review of Empower here.

What Undermines Your Investments

When you invest, it’s important to make sure that you are doing your best to maximize your earnings.

Many of us think only of whether or not the investment account is doing well. However, there are some other things to pay attention to. Here are a few things that might undermine your investment earnings:

Fees

You might be surprised at how fees can erode your investment earnings. Any investment is going to come with fees. All brokers — including online discount brokerages — charge transaction fees when you buy or sell.

All funds come with fees. However, there is no need to pay more in fees than necessary.

You might pay 2% or more on managed mutual funds, but if you choose an exchange-traded fund or an index fund, you could likely pay less than 1%. Compare brokerage transaction fees as well. Some brokers charge a flat fee for all trades, and others have different fee structures.

Make sure you understand the fee structure and choose investments that come with lower costs. Editor’s Note: I actually pay 0.19% in expenses with my target date mutual fund through Vanguard. So even some managed funds can be cheap on fees.

Inflation

The issue with using savings vehicles for investing is the cost of inflation. If your money does not grow at the same pace as inflation, then the same number of dollars will buy less in the future. Inflation is the general rise in the price of goods and services over time.

So, over time, inflation reduces the value of the exchange currency. This explains why you could buy a can of coke for $.25 when I was a kid. But now they cost $1.00.

Inflation is measured by watching the change in an index, like the Consumer Price Index (CPI). Historically, the inflation rate has been around 3%. We had a high period of inflation in the 1970s here in the US, with annual inflation rates for some years more than 10%.

For the calendar year of 2019, the inflation rate was approximately 2.3%. That means $100 you put in a safe on January 1, 2019, could only buy $97.70 worth of goods by December 31, 2019. This is why it’s a good idea to find savings and investment vehicles that can keep up with inflation since the inflation rate compounds over time. This is why prices for goods can double in as little as 20 to 30 years.

Here’s an inflation calculator if you want to play around with it.

Taxes

Your tax strategy can cost you down the road. You will have to pay taxes, of course, but you want to make sure you aren’t paying more than you have to.

Look at where your money is going. Try to put as much money as possible in tax-advantaged accounts if you want to put off paying taxes. In Roth accounts, your money grows tax free (although you have to pay taxes on your income up front, before you invest).

Also, consider whether or not long-term investments might work for you. The tax you pay on long-term capital gains is different from what you pay on short-term capital gains. If you hold an investment for a year or less, your gains are taxed as regular income when you sell.

Summary

There are a lot of options when it comes to investing. But before you begin, get a clear understanding of your goals and risk tolerance.

When you are ready, the first place to get started is your 401(k) up to the point where you take full advantage of your company match. If you are taking full advantage of the match, or don’t have access to a 401(k) start funding your Roth. Once you’ve taken full advantage of the tax-advantaged accounts available to you, start investing in taxable accounts.

Choose your investments and asset allocation based on your goals and risk tolerance. Adjust these over time as your risk tolerance and time horizon changes.

Thanks for the post and the link to the Morning Star PDF is a great tip and starter resource!