PeerStreet Review | Did My $50,000 Experiment Pay Off?

Update: Sadly, Peerstreet has filed for chapter 11 bankruptcy. I’m disappointed. But I can’t say I was completely shocked by this news. Real estate and interest rates have changed a great deal over the last year.

If you’re looking for an alternative to Peerstreet, see this list of real estate crowdfunding sites.

If you have funds invested with Peerstreet I suggest you log in and check out the information regarding the bankruptcy filing. There’s a helpful FAQs here that sheds some light on the decision, the next steps, and how you can make a claim.

Are you an accredited investor looking for a way to get involved in real estate investing without actually owning and managing a rental property yourself?

I have my own rental property (pictured to the right), but I can’t imagine taking on another one at this point. And the turnkey stuff either seems shady or too involved. So I’ve been looking at all of the various options and asking some friends.

I have my own rental property (pictured to the right), but I can’t imagine taking on another one at this point. And the turnkey stuff either seems shady or too involved. So I’ve been looking at all of the various options and asking some friends.

“Coach” Chad Carson, the author of Retire Early with Real Estate, suggested I look into PeerStreet. So I did. I liked what I found so I got started with them.

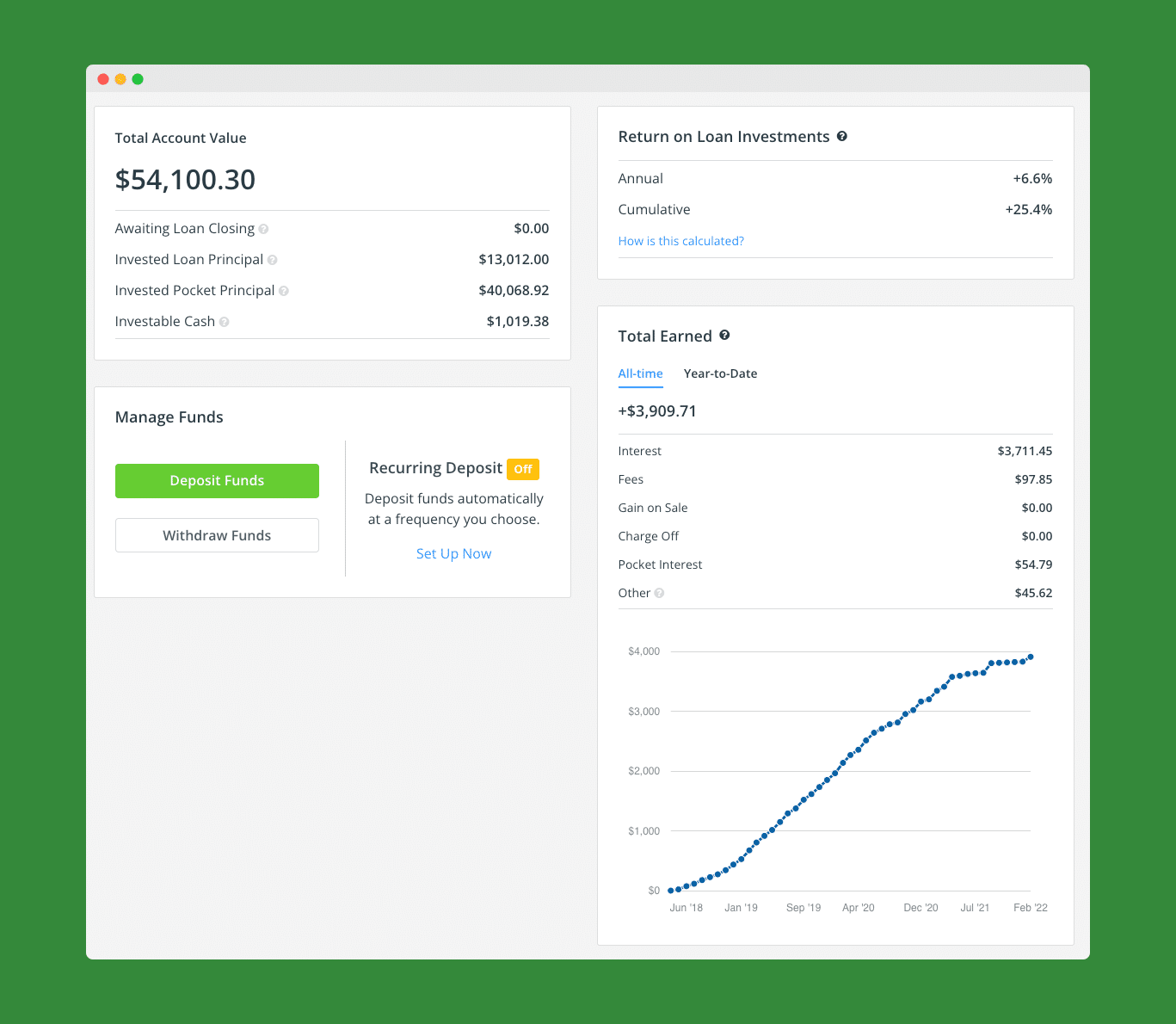

I now have over $50,000 invested with Peerstreet and have earned almost $4,000 in interest over the last 4 year!

Below is my full experience with PeerStreet. The good, the bad, and the ugly. They’ve definitely helped me scratch my real estate itch – all while earning ~6% annual return.

Table of Contents

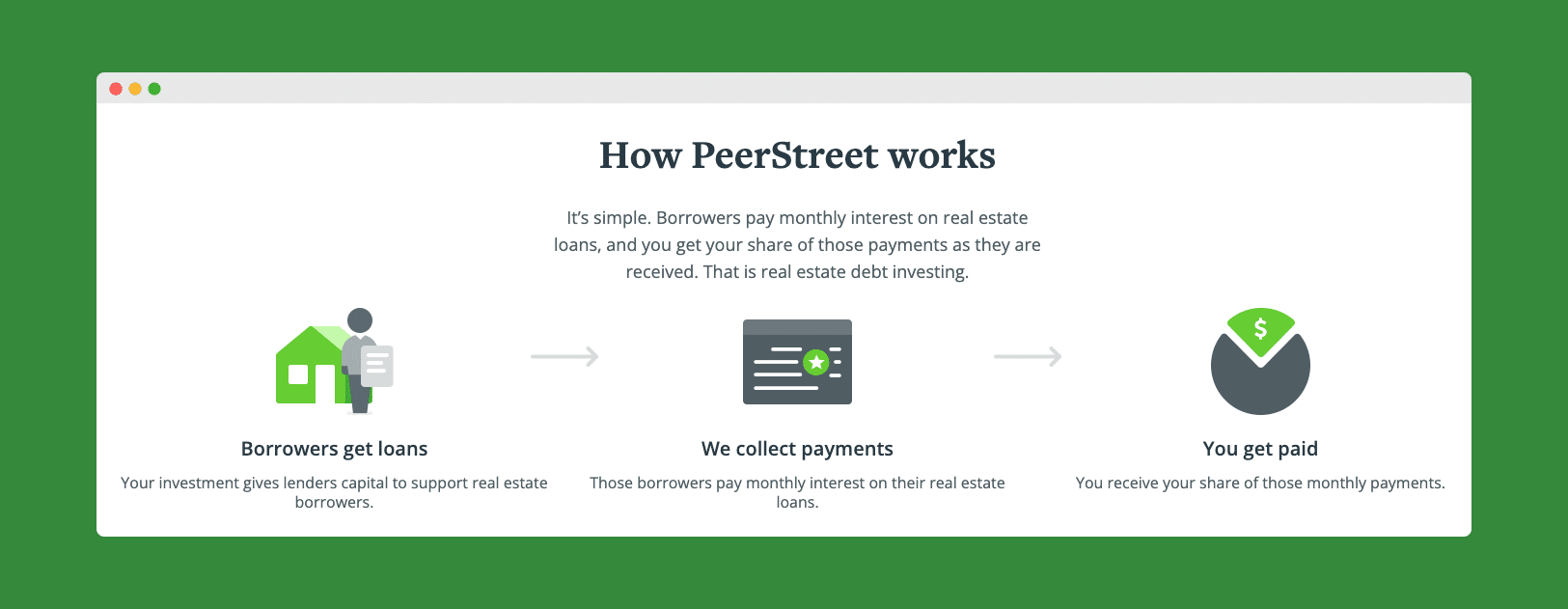

What is PeerStreet?

PeerStreet is a peer-to-peer lending or crowdfunding platform for real estate. It provides a stage that connects investor-lenders (you) with borrowers looking for short-term loans for real estate.

The borrowers are “real estate equity investors,” meaning they are professional investors who purchase a home or property, fix it up quickly, and sell it again at a higher price.

The lenders who invest in PeerStreet put their money in real-estate-backed loans and are offered a first-lien position. A first lienholder is the first person to get paid back if a deal goes sideways, which means your money is more protected in case of default or other significant problems.

This investment type is different from a more traditional real estate investment trust because it provides more transparency into the deals and more flexibility for the investor/borrower.

With PeerStreet, you can select from various portfolios of real estate loans. These loans are constructed of different property types, geographic locations, loan maturity dates, and more.

PeerStreet also claims to have a lower fee structure than a traditional REIT, which allows the investor to capitalize on the higher returns offered by PeerStreet. You can expect to pay a servicing fee of between 0.25% and 1.00% with PeerStreet for each loan you invest in.

The fee – which is just the spread between what you earn and what the borrower pays – is always disclosed.

All real estate loans through PeerStreet have been selected from vetted private financial institutions in the United States. The borrowers you will be lending to are proven experts in the real estate industry.

PeerStreet is not an investment platform for everyone. There are extensive criteria for the investors with whom they work – aka, accredited investors only.

What is a PeerStreet Accredited Investor?

To invest with PeerStreet, you must qualify as an accredited investor. According to the SEC, to be an accredited investor, you must earn an income that exceeds $200,000 a year or $300,000 if jointly filing with a spouse.

If you don’t meet the income requirements, you can have a net worth that exceeds $1 million individually, not including any equity in your primary residence.

Not yet accredited? Check out these other real estate crowd-funding platforms.

How Does PeerStreet Funding Work?

PeerStreet works with trusted private lenders to source real estate loans. Before they bring the loans to the investors, they review the private lenders’ loan history as well as run each loan through their underwriting algorithms, in addition to traditional underwriting methods.

Once the private lenders and loans have been vetted, then investors can select their investments.

You have the choice of looking through the options individually to choose your investments, or you can specify investment criteria like the loan rate, the loan-to-value ratio, the loan term, and the amount you will invest per loan.

What are PeerStreet Loan Returns?

According to PeerStreet, the average mortgage rate is about 5%. However, they claim to offer an average APR of 6%-9%. This is because they are using private money lenders, which tend to offer higher interest rates.

Borrowers will take higher rates from lenders because these loans may provide more flexibility and quick access to the money. Here’s a snapshot of my dashboard on PeerStreet, showing my actual returns.

New: PeerStreet Pocket

PeerStreet now offers an interest-bearing account if you just want to lend them your money as an alternative to investing in the loans on their platform. This account, called Pocket, pays 2.5% annual interest.

The downside to this new feature: it isn’t FDIC insured and you are required to notify PeerStreet of your intent to withdraw your funds before the 15th of the month if you want your funds by the 1st of the next month.

I’m currently using Pocket as one of the places I’m keeping my emergency fund cash.

PeerStreet Features and Fees

Some of the traditional features you can expect to find with PeerStreet include:

Diverse Real Estate Investment Options

The majority of loans offered by PeerStreet are short-term loans, generally about 6-24 months.

However, when you open an account, you can select different criteria to meet your diversification requirements. These preferences include geographic locations, maturity dates, property types, investment risk, and more. This is excellent for trying to diversify.

Automated Investing

Another way that PeerStreet allows you to fulfill the diversification of your portfolio is to automate your investing. If PeerStreet doesn’t currently have a loan available that meets your preferences, you can choose to be placed on a waiting list.

When that loan becomes available, PeerStreet will automatically invest your funds into that specific investment. Your balance must be over $1,000 to participate in automatic investing.

Turn on automatic investing, and PeerStreet will place you in their next available property, based on your criteria. Unfortunately, they don’t allow you to designate geographic regions when you auto-invest – this is the main reason I don’t use this feature.

Self-Directed IRA

You can choose to open a taxable account or a self-directed IRA. Your self-directed IRA will act as a retirement account. You can transfer funds from your previous 401(k), 403(b), or a 457 plan to fund your account.

Integrations

PeerStreet has recently announced its integration with Betterment and Empower. This will now allow you to view all of your investments in one location and see the entirety of your portfolio and asset mix.

Account Security and Protection

Your account with Peerstreet can be secured with two-factor authentication. You can also designate a beneficiary.

What about protecting your cash? The cash funds you put into your Peerstreet account are held in trust accounts with a bank, which is FDIC insured up to $250,000. Once you invest in a loan or in PeerStreet Pocket, this protection goes away, of course.

Loan Defaults

If a default should occur, PeerStreet works on behalf of the investor to make sure the process will maximize the investor’s proceeds. They claim to work to protect the investor’s best interest at every step of the default process.

Additionally, the program reassures investors that if PeerStreet itself were to go out of business, a third party would step in as a “special member” and manage all remaining loan investments as a trustee.

I’ve had four of my loans go into default. One was eventually closed (after a year delay) and I received all of my principle back. The other 3 are still pending the default process, which takes a long time – going on almost two years for one of the loans.

To their credit, Peerstreet has communicated all throughout the default process and I always know where I stand with my loans.

PeerStreet vs. Alternatives

PeerStreet isn’t the only real estate crowd-funding platform available. Let’s look at a couple more.

PeerStreet vs Groundfloor

Groundfloor is probably the platform most similar to what PeerStreet does – they both lend money to real estate investors and cut you in on the interest earned on these loans.

With Groundfloor, however, you can get started with as little as $10 – and you don’t need to be accredited. Participation is allowed across the U.S. except for Nebraska. Funds can be held in a Self-Directed IRA.

PeerStreet vs. Fundrise

Another popular competitor to PeerStreet is Fundrise.

Both companies are available to investors in all 50 states. They also both allow investments through IRA accounts. Beyond that, they are very different companies.

While PeerStreet focuses strictly on residential properties, Fundrise offers residential and commercial investment opportunities.

Another big difference is that you do not have to be an accredited investor to invest with Fundrise. Anyone can get started with as little as $500. Fundrise’s fees are all at 1% of every investment.

Investments made through Fundrise are typically set up with a long-term focus in mind, as they charge a fee if you withdraw your money before it has been invested for five years.

Check out our full review of Fundrise here.

Each peer-to-peer lending company may vary. Do your research and compare all companies before moving forward with your financial decision.

PeerStreet Pros and Cons

- Pro | Low Minimum Investment Requirement: PeerStreet requires a $1,000 minimum investment.

- Pro | Opportunity to Diversify: All of the investments at PeerStreet are real estate loans; however, you can select various geographic locations, property types, maturity dates, and more within this investment class.

- Pro | Limited Risk: PeerStreet investments are closer to bonds than stocks. This minimizes some of your exposure to volatility and risk. Essentially, you may be less likely to lose your money with this type of investment.

- Pro | Short-term Maturity: All loans have short-term maturity rates between 6-24 months. This can offer a better option than an investment in a fixed asset. With fixed assets, you run the risk of interest rates rising above your locked-in rate without being able to liquidate your investment without penalty. Investments with shorter-term maturity give you more flexibility to make changes to your investment strategy as rates change since your money will never be tied up for more than 24 months.

- Con | Non-Liquid Asset: Though the short-term maturity is a big selling feature, it’s important to remember that once you invest in one of PeerStreet’s real estate loans, you will need to stay invested until the loan matures (or longer – even as long as 2-3 years if the loan defaults). Unlike similar bonds, there is no secondary market (yet) for you to sell your asset. If you need liquidity, this may not be the right investment choice.

- Con | Must Be an Accredited Investor: The accredited investor requirement removes a lot of smaller investors from the PeerStreet platform. Many investors may not meet the SEC requirements.

My Approach with PeerStreet

Here’s how I went about investing in real estate through PeerSteet.

First, I opened my account, verified my accredited status, and deposited $10,000.

Over three months, I invested $2,000 at a time in various deals. My goal was to diversify a portfolio of five investments by geography (East Coast, West Coast, Heartland), time horizon (three months, six months, twelve months, and eighteen months), and loan type (acquisition vs. refinance).

Here’s a snapshot of my portfolio six months later (you can see some of my original loans have closed, and I’ve picked up more):

| Loan | Status | Investment | Rate | Matures | Outstanding Principal | Interest |

|---|---|---|---|---|---|---|

| Washington, DC Acquisition | PAID OFF | $2,000.00 | 3.00% | 5/7/2018 | $0.00 | $5.00 |

| Capitola, CA Acquisition | PAID OFF | $2,000.00 | 7.25% | 6/6/2018 | $0.00 | $19.33 |

| East Hampton, NY Cash-Out Refinance | PAID OFF | $2,012.00 | 3.00% | 6/11/2018 | $0.00 | $5.03 |

| Sacramento, CA Acquisition | CURRENT | $2,000.00 | 7.25% | 4/1/2019 | $1,635.43 | $24.38 |

| San Antonio, TX Acquisition | CURRENT | $2,000.00 | 7.00% | 4/1/2019 | $2,000.00 | $48.62 |

| The Colony, TX Acquisition | CURRENT | $2,000.00 | 7.00% | 5/1/2019 | $2,000.00 | $58.74 |

| Beverly Hills, CA Cash-Out Refinance | CURRENT | $2,074.00 | 8.25% | 1/1/2020 | $2,074.00 | $46.11 |

| Edmond, OK Refinance | CURRENT | $2,000.00 | 7.00% | 3/1/2020 | $2,000.00 | $65.74 |

Friends might notice I picked one of these properties near my hometown so I could see the property if I wanted. All in all, I made $272.95 in interest on my total investment of $10,000 in the first six months. That’s around a 5.5% annual return. Not bad.

Since that initial 6-month trial period I’ve become really comfortable with PeerStreet platform. I’ve participated in over 51 loans (41 closed and 10 currently active). I also have a lot of my emergency fund cash with PeerStreet Pocket earning 2.5%. I love this platform!

Am I afraid that a default could happen? Not anymore. Defaults have happened and I’ve still been paid back my original investment. Remember, in case of default, you are the first lien holder, which means you’ll be first to receive the funds from a future sale of the property.

To date, no one has lost their original principle with PeerStreet.

But there are always risks with any investment like this. So do your own research – maybe do a little test run with a few loans – and get comfortable with the platform.

Long-term, I see PeerStreet as a way to raise the interest rate I’m earning from my excess cash and remain somewhat involved in real estate beyond my one rental property.

At some point, I may turn on automatic investing and let PeerStreet do its thing, but , I’m happy sifting through the options for now.