The Best Robo Advisors | Automate Your Investing?

Here’s the thing. Investing should be for everyone. It shouldn’t just be for people who are already rich and can (and want to) pay for expensive advisory services.

Robo advisors have helped more people get into investing and saving for their future without the costs of standard financial advisory services.

According to a BI Intelligence, “robo-advisors manage around 5% of total global assets under management (AUM). This equates to around $4.6 trillion.”

This is good news!

The Best Robo Advisors

Here’s our quick list of the best robo advisors. See more detail below.

- Best Overall: Betterment

- Best for Costs: M1 Finance

- Best for High Balances: Schwab Intelligent Portfolios

- Best for Traders: Ally Invest Cash Enhanced Robo Portfolios

Check out our detailed list of the best robo advisors to get a better idea of what’s available, their fees and more.

1. Betterment

Based on your timeline, goals and risk tolerance, Betterment offers an automated service to build a customized investment portfolio.

The founders created Betterment based on a desire for investment services that would deliver the best possible results while saving time and money. There is no minimum investment or balance requirements. Management fees are .25% to .40% depending on your balance.

Invests in globally diversified low cost ETFs and has free tax lose harvesting for all accounts. Get started with Betterment.

Check out our full Betterment review.

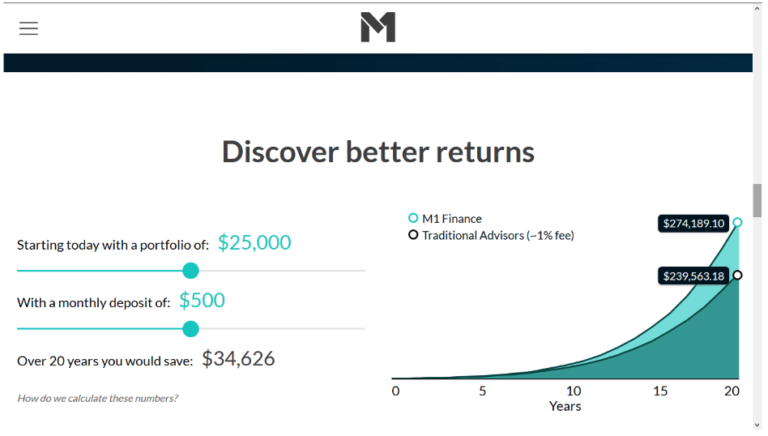

2. M1 Finance

With M1 Finance, you can create your own portfolio with their Expert Pies, which help guide you in selecting the amount to invest in particular stocks.

With the Pie visual, you will easily be able to see all of your holdings as “slices,” and you can choose the weight of each slice.

Slices that outperform their target weight will grow and underperforming slices will shrink. M1 Finance also lets you trade fractional shares.

You can use M1 Finance free of charge with a $100 minimum investment for standard accounts.

Check out our full M1 Finance review!

3. Ally Invest Cash Enhanced Robo Portfolios

Ally Invest Cash Enhanced Robo Portfolios is really a robo advisor that offers cash-enhanced managed accounts. This is perfect for people who want to invest, but don’t have time to learn everything about investing or to actively monitor investments.

There’s a $100 investment minimum and no advisory fees when you keep 30% of your portfolio in an interest-earning cash account–that’s the ‘cash enhanced’ part.

There are also no rebalancing fees or annual charges.

There’s an option for every need with

Sign up with Ally Invest Cash-Enhanced Robo Portfolios.

4. Schwab Intelligent Portfolios

An automated investment advisory service that builds and rebalances your portfolio. The minimum investment is $5,000 and there are no advisory fees or account service fees. Invests in a diversified portfolio composed of ETFs handpicked by the CSIA team.

Tax-loss harvesting is available to clients with $50,000 or more invested.

5. Rebalance 360

A passive IRA investment strategy is used to meet your retirement goals. Rebalance 360 recommends a portfolio and long-term plan and transforms your assets to meet this plan with your investment platform of choice (Fidelity, etc.).

They handle the rebalancing of your portfolio as well. The minimum size portfolio is $100,000. Fees are .7% per year and there is a one-time setup charge of $250 per account.

Other fees include ETF fund fees of less than .2% and trading costs between $50 and $70 when rebalancing.

Check out our full Rebalance 360 review!

6. FutureAdvisor

FutureAdvisor is an online financial advisor and investing advice service that provides automated investing, rebalancing and tax loss harvesting.

They offer three services: Free DIY investing, automated investing and rebalancing (.5% management fee) and free investment management service for educational accounts like 529s, Coverdells and UTMAs. New accounts have a $10,000 minimum initial deposit.

They invest in low fee and commission-free ETFs and seek a passive long-term return strategy.

7. Market Riders

Market Riders is a web-based investment management software to build a globally diversified low-cost retirement portfolio. They work with any brokerage.

They provide recommendations on what to buy and their fees are $14.95 per month or $149.95 annually. Your portfolio is based on six asset classes that align with different ETFs. You’ll receive alerts and provide guidance when it’s time to rebalance.

8. SigFig

SigFig creates a portfolio based on your goals and keeps it balanced and diversified. There are no annual fees for accounts under $10,000 and .25% annually for SigFig managed accounts over $10,000.

There is a minimum balance required of $2,000 to get started. ETFs are purchased through Fidelity, Charles Schwab, and Ameritrade brokerages.

Their investment philosophy is to decrease investment risk while using low-cost funds.

9. Wealthfront

Wealthfront is an automated investing service that does all the management and rebalances for you. Their strategy includes investing in ETFs that track indexes for 11 major asset classes.

The minimum investment amount is $500 and accounts are held with Apex Clearing Corporation. Fees are charged on a monthly basis based on the annual fee rate of .25% with minimal ETF trading fees are in addition.

Related: Betterment Vs. Wealthfront: Which is the Better Robo-Advisor?

10. Axos Invest

Axos Invest believes investing is a right and not a privilege and people should be able to invest for free. Money is invested in a selection of stocks and bonds through ETFs. There are no fees based on account size.

There is also no minimum investment amount required! Axos Invest earns its money based on the products and services you choose that meet your needs.

11. OnTrajectory

OnTrajectory is a financial planning and advising application. It allows you to enter your current financial plan and see if you are on track for your future financial goals. You can create goals and adjust your current contributions to see the difference it will make in your net worth.

There is a 14-day free trial and then the program is $9 a month, or $60 per year. This program is great for forecasting how simple adjustments in your spending habits can make a large impact on your future.

12. Nest Wealth

Canadians pay some of the highest fees in the world for investment services, and Nest Wealth wants to fix that.

Depending on the size of your portfolio, Nest Wealth charges $20, $40, or $80 per month. These flat fees can save you hundreds or thousands of dollars over what you would pay with a comparable portfolio of mutual funds.

Signing up with Nest Wealth gets you a customized portfolio of ETFs, diversified asset allocation, consistent monitoring, automated rebalancing, support from a registered advisor, and transparent fees.

Nest Wealth is only available for investors in Canada.

13. Wealthsimple

Wealthsimple allows Canadian investors to create personalized portfolios of low-fee ETFs.

Services include automatic reinvestment of dividend income, automatic rebalancing, auto-deposits on your preferred schedule, payment of any transfer fees your bank charges to transfer your account to Wealthsimple, automatic tax-loss harvesting for accounts over $100,000, and options for socially responsible investing.

Balances up to $100,000 have a flat 0.5% annual fee; balances over $100,000 have a flat 0.4% annual fee.

Check out our full Wealthsimple review!

Note: We try to keep this list updated but a downside of the FinTech space is that some Robo-Advisors can and will go out of business.

Compare the Top Robo Advisors

Invest Robo Portfolios | |||

While the concept and investment strategies (and thus, performance) are very similar across robo-advisors, they’re not all the same as far as fees, minimum investments, and level of service for investing. Therefore, we highly recommend you spend some time investigating on your own.

That’s why we created this handy table to get you started. Just follow each link for the robo-advisors that interest you the most and learn more at their website.

Don’t forget to read our more in-depth reviews where available. Also, if you’re using a robo-advisor today, be sure to share your experience in the comments.

What Exactly is a Robo Advisor?

While there are different flavors of robo advisors, they all rely on technology and online portfolio management to reduce costs for the investor.

For a small fee and sometimes no minimum initial investment you can receive professionally based portfolio recommendations in minutes.

Many of the technologies will automatically rebalance your investments when the time is right (a hassle for most people) and use tax harvesting strategies to reduce your tax liability. More than that, they provide user-friendly websites and mobile apps.

Should I Use a Robo Advisor?

At this point you may be asking, “should I use a robo advisor?” I answered this question for myself by answering two other questions:

- Do I believe in the idea of low-cost, diversified, long-term investing vs actively managed investing? Yes, I do. If you believe in this too (meaning, you think this approach is going to give you the best chance at long-term investing success), then a robo advisor may be for you. But you then have to ask yourself a second question…

- Do I want to outsource the picking of those low-cost funds and rebalancing the asset allocation through the years? I said no to this question. Sort of. I chose to pick my own funds over at Vanguard. And the single fund I chose was VFORX, which is a target-date fund (made up of three index funds) that automatically balances itself as I get older.

Learn more about why I chose VFORX.

So in essence, I decided that it wasn’t worth the additional cost of a robo advisor to pick funds for me.

I do, however, still use a robo advisor, Betterment, as an emergency fund overflow account. When my emergency fund (in a simple savings account) reaches a certain limit ($10k), Betterment pulls the overflow money into their account.

This is called SmartDeposit and you can read more about it in my full review of Betterment.

Robo Advisors vs Financial Advisors

One last question you might have is, “what’s better? robo advisors vs financial advisors?” And to that question I say–you don’t have to choose. You can use both. I plan on using both in my life to achieve financial success.

“Robo advisor” is such an unfortunate name for these tools. It makes it sound like you don’t need another human to help you make financial decisions. That’s just not accurate. It should be named robo investor or robo trader.

A financial advisor can do much more for you: help you get rid of debt, teach you to properly manage your money, advise you on insurance, social security, estate planning, and the list goes on.

In fact, many financial advisors are using robo advisor software now to actually manage your specific investments for you. So even if you try to choose one over the other, you may eventually end up using both anyway.

People looking for help forming a more comprehensive financial plan may want to seek out the services of a Certified Financial Planner. CFPs go through a rigorous process to become certified, including a long education process, a grueling exam, years of work experience, and continuing education after certification. They are also required to act in the best interest of clients, even if it earns them less money.

I personally use a financial advisor every five years or so in a one-off meeting to check my progress towards my goals. I pay a one-time fee.

There are many different types of financial advisors and planners. Learn more about financial advisors and planners here.

Got an opinion on Robo Advisors? Let us hear from you in the comments below.