Budgeting for Couples: The Complete Guide for Your Marriage

Budgeting for couples may require more effort and attention than budgeting on your own. But it’s a habit many couples desperately need to learn.

A recent Magnify Money survey of over 1,000 Americans revealed some alarming facts about marriage and money.

One in five couples who responded to the survey regretted combining finances with their spouse. And 21% of respondents cited finances as the primary cause of their divorce.

It’s clear money can cause a lot of contention and strife in marriage relationships. But when couples are able to communicate openly about their financial goals and work together to accomplish them, it can truly draw them closer emotionally, as well.

Being totally honest and working as a team is the best way to handle your finances as a couple. Tools like Zeta can help keep everyone on the same page.

Tired of fighting with your spouse about money?

Eager to stop butting heads and start working together to achieve your financial dreams?

Here are four steps which can make budgeting as a couple just a little bit easier.

Communicate With Your Spouse About Money

It may be difficult to talk to your spouse about money. But it’s a non-negotiable if you want a healthy marriage. But how you do engage in conversations about money without igniting World War 3? Here are some tips which

could help your marriage (and your money) for many years to come.

Tell Your Partner Everything

Whether you are still in the midst of wedding planning, or you’ve already celebrated several years worth of wedding anniversaries, it’s imperative you and your spouse share all of your financial information with each other.

This includes any outstanding debt as well as assets like savings, retirement and even life insurance policies.

This conversation is important because it’s not possible to move forward financially if you don’t know where you are. In addition, keeping money secrets from your spouse is a recipe for marital resentment. You and your spouse need to bring it all to the table.

Even if you’ve been married forever, this is something that’s worth going over every few years.

Just like periodic weigh-ins can keep your weight from creeping up on you, periodic net worth check-ins will keep you from losing track of how your money is faring.

Adopt a Team Mentality for Your Money

It’s really easy to point fingers and say, “Well, he’s the problem because he won’t stop buying things,” or “She’s the problem because she won’t stop going out to eat.” +

The truth is neither of you are the problem; the debt is the problem. Stop blaming each other.

Instead, team up against the debt and you will solve this problem quicker than you ever imagined.

Working together as a couple on your finances will also help you plan for major purchase, taxes, and most importantly, retirement.

Related: Everything You Need to Know to Get Out of Debt

Continuing to see money in terms of “yours” and “mine” after marriage is a good way to start arguments and bean counting. That’s why it’s important to find a way to look at your money as something you share—which also means sharing your decisions about it.

While some couples simply mingle all of their money in a joint checking account, others find that setting up a yours-mine-and-ours system works best for them.

No matter how you manage the logistics, it’s important to start looking at the majority of your money from a team perspective.

Set Goals for Your Marriage and Money

One of the best ways to adopt the team mentality for your money is to make some life goals together. Not only will this help you both get on the same page, but it’s the fun part of the money discussion.

Sit down with your spouse and talk about what’s important to you.

What do you value as a family? Write these things down.

It’s a time to listen to your partner and write down matters what the most to them. Share why your values are so important and why you want them to be central to your family.

Then take a look at your bank accounts and see if your spending matches your values. If there is a disconnect, then it’s time to make some changes.

Next, spend some time discussing your short-term and long-term goals. If you want to plan a summer vacation next year, buy a cabin in 10 years, or save $20,000 for your child’s education, these are important things to talk about so you can start planning for them.

Don’t bite off more than you can chew with this exercise. Determine which 3-5 goals are most important to you and focus on them.

And revisit these goals regularly, so you can determine if you are still on track and if your goals still fit with the life you are building together.

Checking in about once a year on your goals will help you to achieve them, and tweak them where necessary.

Read More: 101 Money Skills Every Money Nerd Should Have

Maintain Some Financial Independence

It might sound like the complete opposite of adopting a team mentality, but it’s important for each spouse to have some financial independence. No two people will entirely understand each other’s spending habits.

And completely merged resources can lead to fights.

For instance, a husband may not be able to comprehend how his wife can drop $75 each year on a perfectly personalized paper agenda. Meanwhile, his regular purchases of artisanal beer may leave his wife scratching her head.

Allowing each spouse some “me” money to spend however he or she chooses can help both spouses be happier. You will each know you can treat yourself to small luxuries without it hurting your marriage’s bottom line.

Of course, you each should have respectable, and equal, amounts to spend.

Track Your Spending and Create a Budget

It’s great to know how much you’re worth and what your goals are, but you also have to know what’s happening to every dollar that passes through your hands. Without this information, budgeting for couples is nearly impossible.

There are many tools available for money tracking (we’ll cover two popular budgeting tools later).

Try different systems until you find one that works for you. No matter what system you use, track your spending for at least a month (and ideally for three months) each year so you have an accurate view of where your money goes.

Many financial gurus like Dave Ramsey or Suze Orman offer budgeting advice, in addition to the thousands of budgeting websites available online.

Just as with the spending tracker, you will want to find the system that works best for you. The most important aspect of budgeting for couples, however, is consensus.

Both spouses must agree to the budget or it will go unused.

Delegate

Whether you have a joint checking account, separate accounts, or a mix, it’s likely that one spouse will be the money manager in the marriage.

Decide ahead of time who will be the one to pay bills, balance the checkbook, keep track of financial records and make day-to-day money decisions.

All financial work doesn’t have to be made by the same individual, as long as every money decision is covered.

If you’ve decided ahead of time who will take care of each aspect of your finances, you won’t have a month where you each thinks the other has paid the mortgage.

Set Up Regular Money Meetings

Part of what makes money decisions so difficult is the fact there is no natural time to bring them up. That’s where regular money meetings come in.

Whether you hold your meetings on a weekly or monthly basis, you should plan a time for the two of you to sit down with your financial information to have a conversation. This is especially important when only one spouse is the delegated money manager.

Your agenda should include a discussion of:

- upcoming bills

- how the budget is looking

- where you are with various financial goals

- things you might do differently

If this kind of regular meeting sounds about as romantic to you as his-and-hers dental surgery, try making a date of it. Look over your budget with a couple of beers and plan on watching a movie when you’re done.

This is a great way to focus on the positive changes you are making on your finances instead of dwelling on the negative.

Perhaps you could consider investing in your relationship by going on “financial walks and talks” together. It could be a great way to discuss the big picture items like goals, values, upcoming expenses, in addition to your future dreams.

This could do wonders for your relationship and your savings account!

Plan for Emergencies

Unfortunately, married life is not always smooth sailing.

It’s important to have money set aside for when things aren’t going great financially. This starts by putting together an emergency fund.

Most experts recommend setting aside a 3-6 month reserve of cash in case of emergency—aiming for 6 is ideal—and maybe even more if you don’t work steady jobs with a known salary.

However, in addition to an emergency fund, you should also plan for the worst. No one wants to think about death, but it’s important for married couples to make sure they have enough life insurance and an updated will.

Think of it as the most loving thing you can do for your spouse.

Related: How and Why to Start Building an Emergency Fund

Bring On a Third Party

If having a conversation with your partner about money always leads to arguments, then maybe it’s time to seek some advice from a trained therapist or counselor.

It may also be beneficial to find a Certified Financial Planner who you can help formulate a comprehensive financial plan to help you reach your goals together.

Learn More: What You Can Expect from a Financial Planner

Understand Your Personal Money Style

One of the best things you can do for yourself is to understand yourself. This advice is often given to those preparing to embark on a personal relationship with someone else.

However, this advice also applies to the way you deal with money. Your relationship with money needs to be divined by who you are. And that means that you need to understand your personal money style.

Beyond Saver vs. Spender

In many cases, we tend to label others (and ourselves) as spenders or savers.

However, your personal money style goes beyond that. Scott and Bethany Palmer, authors of First Comes Love, Then Comes Money, identify five money personalities:

- Spender: Likes to spend.

- Saver: Pinches pennies.

- Risk-Taker: Is willing to take a risk if s/he thinks it will pay off big.

- Security-Seeker: Would rather make money moves based on safety.

- Flyer: Doesn’t really care about money (or managing it).

Your personal money style can even go beyond those five more nuanced categories. In order to understand your personal money style, you need to know what’s important to you and what you consider “worth it” when you spend your money.

For example, some people prefer experiences over things. If that’s you, you’d probably rather go out to eat at your favorite restaurant than buy a new trinket.

Or you’d rather have a 32-inch TV and go on a mini-getaway than purchase a huge 60-inch TV. Understanding this about yourself helps you make decisions that you’re happier with.

Your personal money style also includes how you feel about the purpose of money.

Is money itself an end? Do you define your status and worth by how much money you have amassed?

Or perhaps you believe that your financial resources should be directed at helping the less fortunate.

Money Motivations

There is a lot that goes into your personal money style. It can be difficult to categorize your money style.

But labels are less important than understanding your personal motivations for the way you spend (or save) your money.

Take a look at what motivates you and how that fits into your future financial goals and your present spending.

Honestly evaluate how you feel about money and how you think your financial resources should be used. Don’t answer with what others think is the “right” response.

Instead, make an effort to look at what you are doing with your money and what you would like to do with your money.

If you don’t like what you see, you can make changes so that your personal money style matches who you want to be.

How to Get You and Your Spouse Back on the Same Page Financially

So what can you do when you and your spouse are no longer on the same page financially?

Try these ideas to keep your sanity and get back to seeing eye-to-eye on your finances.

Remember That Honesty is the Best Policy

Let’s start by saying you can never get on the same page and work through money matters unless you’re completely honest with your spouse. Everything must be put on the table.

No secrets!

This is one reason why combining checking accounts after you’re married could be a smart move. You become one in marriage, so why not become one with managing your finances?

If there are deep trust issues, you may want to see a professional counselor. Work on the marriage first. Secure a solid foundation and the money management will come easier down the road.

Get Financial Values Straight

Assuming you can both be honest in your relationship; you then need to look at values and background. Is your spouse a spender and you’re a saver?

If so, have an open conversation about this and be honest about your financial strengths and weaknesses. Look for ways to work together.

Why is budgeting for couples so important? Because it helps both the saver and the spender. Spenders can have money to spend (as long as it’s in the budget). And savers can have money to save and not squeeze every penny from the budget for their savings goals.

Use the Right Tools

Many people get into heated abstract discussions. “You always spend too much money!” What does that mean, anyway?

The best way to deal with financial challenges is to get them on paper.

Tracking your spending each month (which only requires about 5 minutes a day if you use money management software) provides a record of where all the money is going.

Creating a spending plan with your spouse insures you both have a plan you can agree to at the beginning of the month.

Think someone is spending too much money?

Have the conversation by reviewing the spending record. If it exceeds the budget you both agreed to then you have to work through the matter together without an attack.

How to Encourage the Spender to Save Money

If you want to get your spouse on board with saving, you’re going to need to take a more subtle approach–ne that allows your spouse to catch the vision as well.

Here are a few steps which might help.

Work to Truly Understand Your Spouse

First of all, it’s important to understand why your spouse is not interested in saving in the first place. Does he or she believe that you have plenty of money to cover everything?

Perhaps your spouse doesn’t want to curb some of his or her spending now in order to be in a better position later.

Or, maybe, your spouse just doesn’t understand why you want to save.

Have a calm discussion about money, explain your money personality, and then listen carefully to your spouse. Once you understand the ‘why’ behind his or her lack of desire to save, you can begin helping him or her understand why it’s important to you.

Set Common Goals

In some cases, your spouse might feel as though your desire to save will only benefit you. This means that you need to get your spouse involved in the financial planning process at your home. Talk about what you both want to accomplish and discuss how you can reach your shared goals.

If you both want to go on a vacation, or buy a new car, or build a retirement nest egg, that is something you can do together.

Then, together, you can make a plan to achieve it.

This makes budgeting for couples more enjoyable. If your spouse feels involved in the decision-making and planning process, he or she is much more likely to get on board with saving.

Start Small

There is no reason to overwhelm your spouse with huge plans to set aside $800 per month immediately. Indeed, it’s probably best to start small.

Suggest that instead of going out to eat twice a week, you go out to eat twice a month.

You take the money you save and set it aside in a joint savings account. Go through your spending with your spouse, and look for ways you can cut costs. Start with the small things.

Make sure that you replace the items you cut with something of value.

For example, if you aren’t going to go out to eat as much, plan meals together and consider cooking together, or doing the grocery shopping together. You still get to spend quality time together–without spending the money.

Once you and your spouse are comfortable with saving, it’s possible to increase the amount that you save. You can even embark on some sort of home business or way of earning supplemental income that can augment your efforts to save more.

The key, though, is to do it together.

Pay Attention to Your Tone

Throughout this process, it’s important to pay attention to the way you say things.

Try not to be accusatory. Use “I” language to describe how you feel. Avoid telling your spouse that it’s his or her fault that you can’t do any of the things you’d like–even if you feel like it’s true.

Respectful speech and language that describes your feelings is important.

And inclusive phrases that helps your spouse feel a part of the process, are likely to have better effect than complaints and accusations.

Use Tools That Make Budgeting For Couples Easier

Over and over again, we’ve talked about the importance of budgeting for couples. But working on a joint budget can be more difficult than following a personal budget. Using a budgeting tool that both spouses can access at any time and anywhere can be very helpful.

Zeta and Empower are two popular budgeting tools that you may want to try out. Zeta is a great day-to-day budgeting tool, especially if you have separate bank accounts.

And, Empower can give couples a global view of their finances and investments.

Let’s a closer look at how Zeta and Empower work.

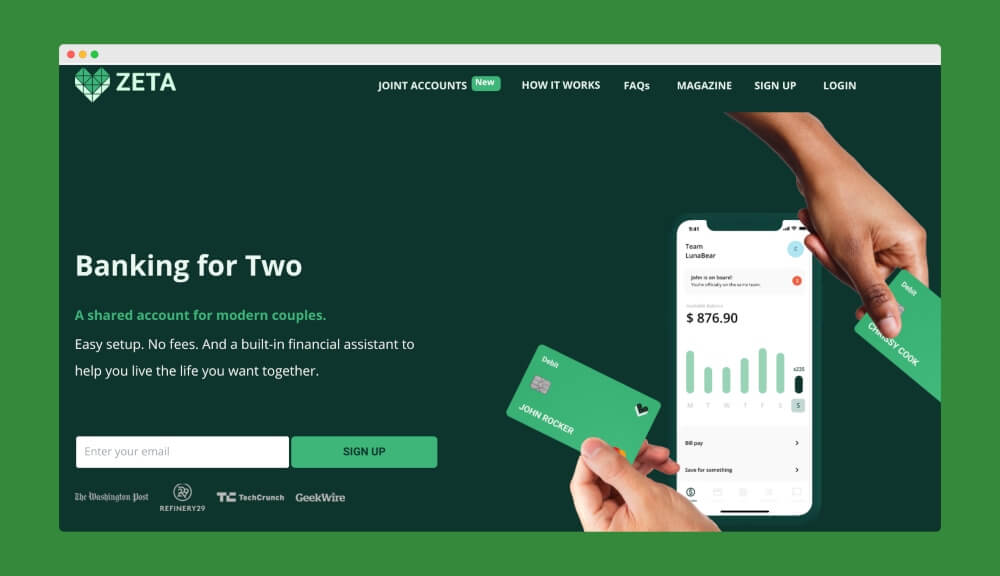

Zeta

While joint bank accounts can make it easier for couples to share their funds and set goals, some couples simply aren’t ready to take that step. With Zeta, that’s not a problem. Using Zeta’s budgeting for couples tool, you can create shared budgets and goals — even if you don’t have joint accounts. Here’s how it works.

What is Zeta?

Zeta is a budgeting for couples website and app. It’s truly a personal finance tool designed from the ground up for couples. After connecting your bank accounts to Zeta, you can select certain accounts as “personal” and others as “shared.” When you designate an account as “shared,” your spouse will be able to view its full transaction history.

However, only you can see the activity in accounts marked as “personal.”

In like fashion, each spouse can set personal and shared budgets. This design gives couples a high level of control over what is shared and what is kept private.

Zeta proudly refers to itself as the “personal finance tool for the modern-day couple.”

How to Sign Up for Zeta

Signing up for Zeta is quick and simple. Simply create your Zeta account and link your personal and shared bank accounts.

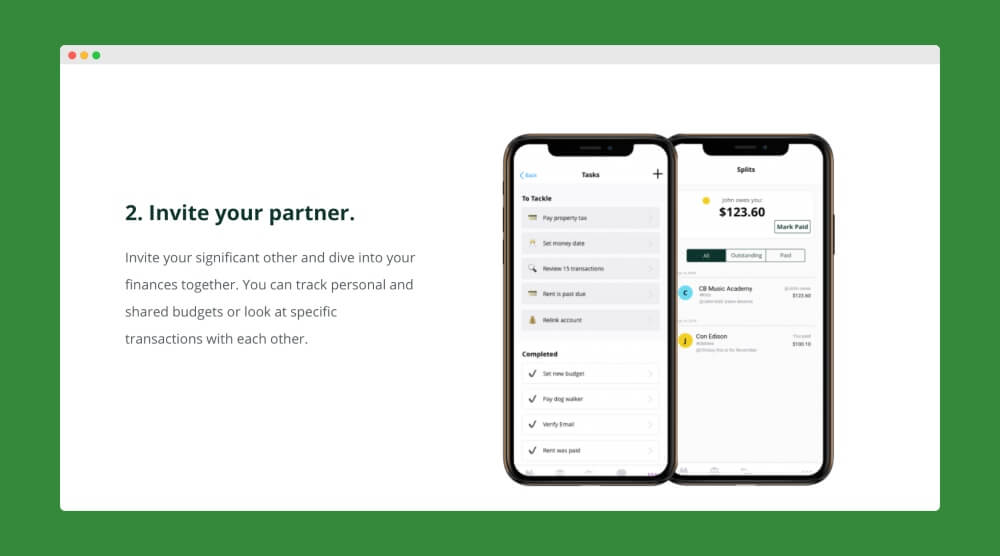

Once you’re all set up, you can invite your partner to join you on Zeta. After your spouse has accepted your invite, they can add their personal and shared accounts as well.

Now that both of your accounts have been added, you can get to work creating shared budgets and goals.

Each of you can create personal budgets as well. After you’ve set up your budgets and goals, Zeta will regularly send you updates on where you’re money is heading.

And they’ll even remind you about upcoming bills.

Features of Zeta

Shared and personal accounts and budgets are just the tip of the iceberg when it comes to Zeta’s feature set.

Here’s a quick list of additional features they offer that makes budgeting for couples easier.

- Sharing Controls: You always control what your partner can see. For example, you could select to allow your spouse to the balances of your personal accounts, but not the individual transactions.

- Split Transactions: Quickly split up transactions to show the portion that each spouse owes.

- Memos: Make notes or ask questions about certain transactions.

- Custom Categories: Create any category you want and track the expenses that matter to you.

Zeta also recently launched a “Joint Account” feature. Now couples can create a Shared Account inside Zeta within 5 minutes.

These accounts are FDIC-insured and they have no fees or account minimums.

Zeta truly takes a lot of the hassle and frustration out of budgeting for couples with separate accounts. And the best part is that their tool is completely free to use.

Empower (formerly Personal Capital)

While Zeta is a great budgeting tool, it’s not as strong at helping you track your investments or your net worth.

However, this is an area where Empower excels. If you and your spouse are looking for a tool that can give you a 360-degree view of your money, you may want to give Empower a try.

Let’s take a look at what Empower has to offer.

What is Empower?

Empower makes it easy to sync up all your financial accounts in one place. You can not only keep tabs on your bank accounts, but you can also track your investments and even the value of your home (through Empower’s partnership with Zillow).

Like other tools, Empower makes monthly budgeting for couples quick and simple. And their Cash Flow feature will show you exactly how much money has gone in and out of your accounts in the past 30 days.

But where Empower really shines is in tracking your investments and net worth. Their Net Worth calculator will automatically subtract what you owe from what you own to give you a true picture of where you’re at financially.

And Empower offers a bevy of investment tools, including their Retirement Calculator, Fee Analyzer, and Education Planner. These tools make it easy to track your long-term financial goals and uncover hidden fees.

Read our full review of Empower.

Teach Your Kids About Money

It’s important when children come along that they develop an appropriate appreciation for how mom and dad budget, save, spend and invest money. Instead of just saying “No” or “We can’t afford that” when kids ask for things, explain why you choose to limit your spending in certain categories.

Obviously, if your kids are too young to read or understand math, you won’t be able to have a full budget breakdown.

But there are things that you can do at each age level to help your kids gain a proper perspective on money.

In our Complete Guide to Teaching Kids About Money, you’ll find a year-by-year plan (from under age 3 to college-age) to helping your kids develop smart money habits.

As your kids grow older, make it clear to them that your money isn’t being spent “willy nilly.” They need to understand you and your spouse have purposefully set (and are following) a financial plan.

By teaching your kids about money while they’re still living at home, you’ll help them avoid financial mistakes after they’ve left the nest.

Next Steps

Budgeting for couples may require more work than budgeting solo, especially making the time to keep doing it.

But the potential benefits are worth the effort. Not sure where to start with creating a shared budget?

One idea would be to have both of you write out your short-term and long-term goals and then discuss them as a couple.

See where it goes from there.