Inflation Sucks! Here’s Why You Shouldn’t Panic

We’ve heard the numbers – a lot. Inflation is running at about 7% – the highest rate in 40 years. “Transitory” was the word first used to describe it, but this past November, Fed. Chairman Jerome Powell stated, “I think it’s probably a good time to retire that word.”

Fair enough, let’s retire it – but what will the impact of this non-transitory inflation spike be? For those of us who are thinking about our long-term financial future, what should we do to compensate – and just how much compensation is required?

Current consensus seems to be that inflation will return to a more normal rate (that is, 2-3%) some time in 2022 – but what if, like “transitory,” that’s also wrong?

Furthermore, what should I do now, are there changes I should make to protect myself and my savings? Let’s run some numbers and see what this spike may mean in terms of our ability to save for the future.

Visualizing Inflation’s Impact on Your Savings

Let’s take a quick example.

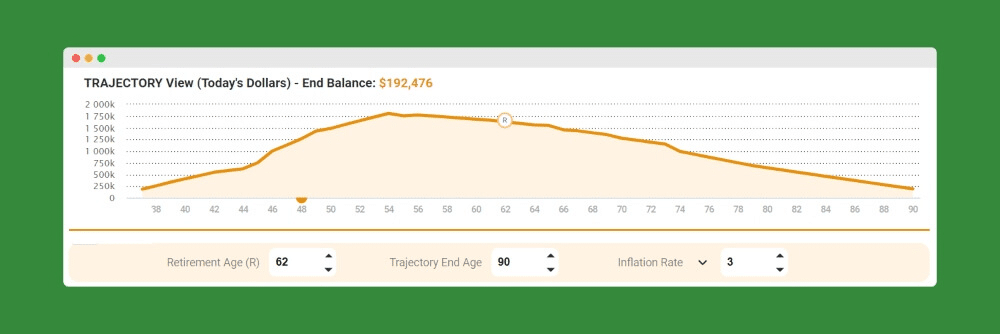

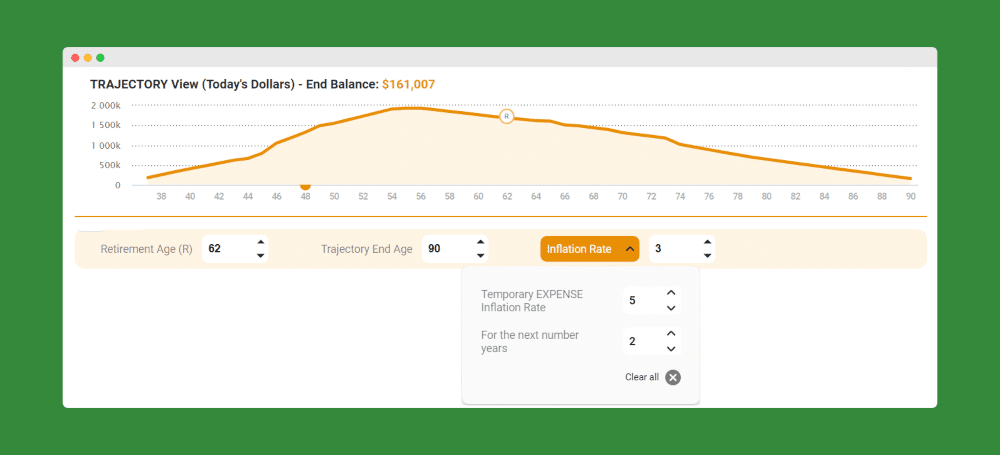

Our subject is 35 with two young kids – they’re hustling to earn and save extra cash in hopes of achieving ”financial Independence”. As you can see in the illustration below, they’re projected to have about $200,000 left-over at age 90 – a pretty comfortable cushion:

Source: OnTrajectory

But, in this model, we’ve set overall Inflation at 3%, meaning both income and expenses will rise, on an average, 3% per year.

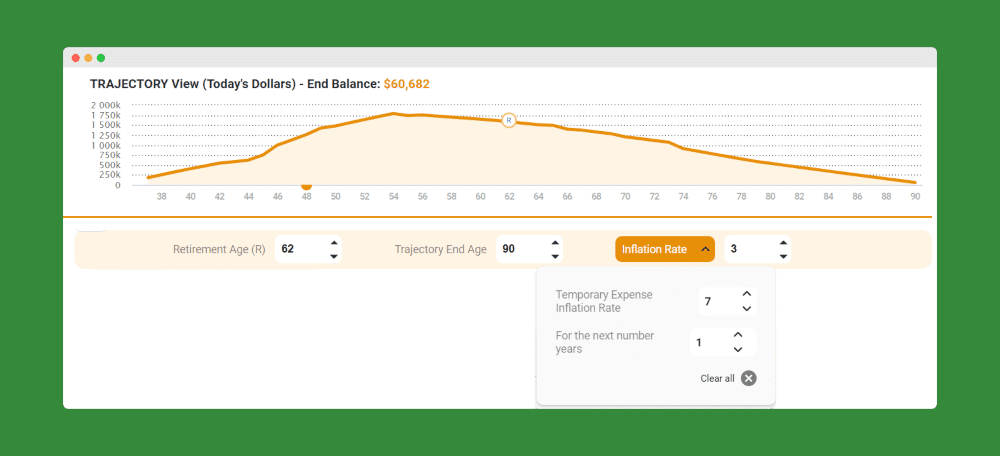

Clearly, this is not what is currently happening in the US economy. How do current trends impact this individual’s ability to save, and what effects may they have in the long term?

Let’s build in a 1-year, 7% spike in inflation for expenses. As shown below, that sustained 1-year rate of 7% is projected to wipe away $130,000 in savings over the next 40 years. This shows precisely how impacting and potentially life-changing inflation can be:

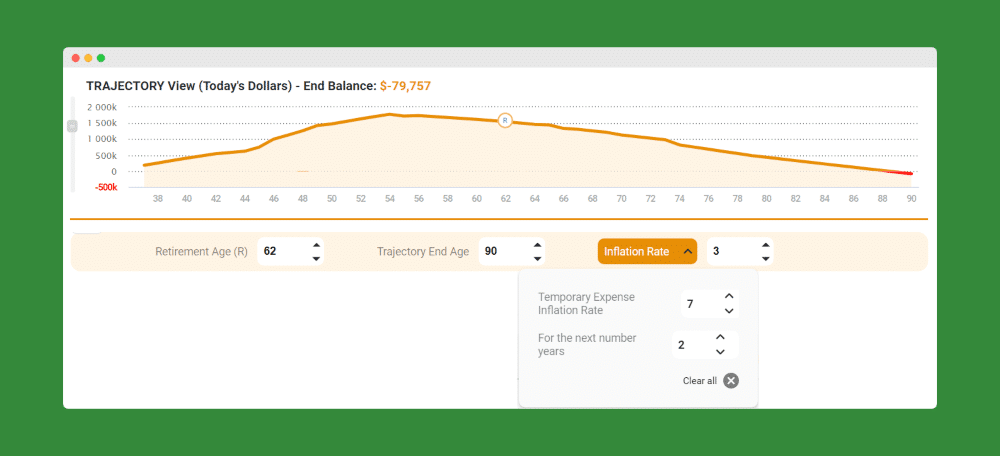

But let’s see what happens if the spike in expenses lasts 2 years, continually without any cessation. Our 35-year-old’s cushion has vanished, leaving them with an $80,000 deficit after 2 years of our current inflation rate.

This is huge, and maybe a little disturbing. How can we prepare for our future when the winds of change can have such devastating effects – but the real question is, do these illustrations show the whole story?

Current Inflation in Context

First, let’s look at not just the past 40-years, but at the past 50:

As you can see, although today’s inflation rate is significantly higher than it’s been during the past decade, there have been periods when the annualized rate approached today’s – most recently during some months of 2008.

Compared to the unprecedented, long-lasting inflation of the 1970s, current rates seem far less scary.

However, saying, “At least it’s not like the ‘70s” may be cold comfort. It’s a little like being lost at sea and saying, “At least this isn’t the Titanic.”

So I’d like to raise another important aspect of inflation – and that is human behavior. Should we buy all the things now before the prices go up even more?

- The truth is, when the price of beef goes up – people buy pork.

- When automotive dealers charge more than MSRP, folks do put off buying cars.

The “real” impact of inflation may hit us a little less in the wallet, and more in our levels of frustration and consumer confidence.

People tend to shift their spending in reaction to inflation, rather than blindly spend on inflated items (assuming other options are available and inflation has not become entrenched).

Furthermore, should we succumb to the notion that we should make purchases now before costs go even higher, it can lead to an inflationary self-fulfilling prophecy.

“As consumers spend more and save less, the velocity of money increases, which increases inflation and further contributes to the issue.”

Finally, there’s the reality that inflation does not affect expenses only – during periods of increased inflation, we often see increased wages, although not necessarily at the same rate.

Let’s go back and apply these considerations by applying increased growth to wages and curbing the inflation rate based on changes in spending patterns:

As you can see, this is a far less impactful result. Yes, savings over the next 40-year period did decline by about $40,000 as a result of the 2-year sustained spike – but by and large, the cushion has been preserved.

So This Means What?

Reality is messy. During the 1970s inflation became entrenched to the point folks who had been savers – suddenly stopped. Credit became the strategy of smart investors.

At that time, more types of loan interest were tax-deductible and with inflation at 15%, the buying power of saved funds quickly diminished. Paying later and deducting the interest on your credit cards and even student loans became a hedge against quickly shriveling nest eggs.

But we’re not there yet. You can see it in the math and models above, and viewing the impact of current trends as we’ve done here should inform both our short-term behavior as well as our long-term plans.

And of course, other variables are certain to pop up over time.

As many readers will know, the Federal Reserve is slated to raise interest rates several times in 2022 beginning in March. These changes will pull other economic levers, and our models will need to be refreshed once again – and so the cycle continues.

Having the ability to create these types of models and make adjustments as necessary is certainly important, but we should always keep in mind that math is not the whole story.

As the famous statistician George Box said, “All models are wrong, but some are useful.”

So in this time of hyper-awareness of inflation’s threats and vagaries, let’s not panic – but maybe let’s not pull the trigger on that new truck after all.

Editor’s Note: This article was contributed by Tyson Koska, founder of OnTrajectory, and these models were created using the OnTrajectory tools. You can test your own assumptions about inflation and retirement savings using OnTrajectory’s 14 day free trial.