Betterment Review: Robo-Advisor Investing

When it comes to investing, growth and capital appreciation are key.

Therefore, it’s important to find a good balance between cost and an easy-to-use interface which simplifies investing.

In my experience, the harder it is to figure something out, the less likely you are to use it. This is where robo-advisors shine, taking the guesswork out of achieving the right portfolio allocation for your risk tolerance.

In this Betterment review, we’ll look at one of the first robo-advisors who came to market and how it stacks up against the competition.

Betterment Review

Betterment offers goal-oriented investing tools that help investors build a diversified portfolio and save for the future. If you have a taxable account, you will love the tax loss harvesting feature.

Betterment Digital charges 0.25% of your account balance and has no account minimum. Betterment Premium charges 0.40% and has a $100,000 minimum but offers unlimited phone access to certified financial planners.

Betterment’s goal is to get more people to invest their money instead of parking it in savings accounts.

The company offers an ultra-simple, discount brokerage focused on passive investing and wrapped in a Mint.com-like interface.

Editor’s note: Betterment is offering up to 12 months free to new users who open up an account with at least $250,000 within 45 days of signing up with Betterment.*

Here are the details about Betterment and how it stacks up against other robo-advisors:

Table of Contents

About Betterment

Betterment is a broker from a legal perspective just like any other online broker.

They are a Securities and Exchange Commission (SEC) Registered Investment Advisor. Their broker company, Betterment Securities, is a broker-dealer regulated by the Financial Industry Regulatory Authority (FINRA) and the SEC.

The money that you have invested with Betterment is protected by the Securities Investor Protection Corporation (SIPC) on balances up to $500K.

Like other investment brokers, SIPC doesn’t mean you can’t lose your money if the market tanks. It means you can’t lose it to fraud or failure by Betterment (i.e. SIPC isn’t the same as the Federal Deposit Insurance Corporation (FDIC) so it does not entitle you to the same protection).

Betterment opened its virtual doors in May of 2010. It was founded back in 2007 by Jon Stein, former bank industry consultant turned chartered financial analyst and Columbia Business School graduate.

Betterment Fees

Back in the day, Betterment used to charge 0.3% to 0.9%, depending on your account balance.

Now they are charging from 0.25% to 0.40% (this is on top of investment expenses). Here’s why investment fees are important.

Investors above the $100,000 minimum balance mark also qualify for next-day transfers and a custom portfolio for that flat 0.25% fee. If your balance is too low to receive the services you want, you can pay a monthly fee instead of the percentage fee to access those services.

Two other considerations:

- Existing customers can opt to stay put in their old pricing plan.

- New investors can qualify for up to one year free just for signing up with a new account, depending upon your initial deposit level. An account opened with a $15,000 deposit earns you one month free, $100,000 earns you six months free, and $250,000 earns you one-year free management.*

New customers with balances greater than $2M will be given a 0.10% marginal discount for the portion of their balance above $2M.

- For Betterment Digital, customers will pay 0.15% for the portion of the balance above $2M.

- For Betterment Premium, customers will pay 0.30% for the portion of the balance above $2M.

*Deposits must be made within 45 days of opening a new account with Betterment.

How Betterment Works

One reason that Betterment appeals to investors is that it simplifies creating a diversified portfolio.

Many people are too busy to deal with researching investments, finding diversified securities and building a mix that aligns with their risk tolerance.

A robo-advisor takes the guesswork out of when to buy and sell securities, which funds have better P/E ratios and if they should buy or sell at a certain time.

There is also no need to keep tabs on your portfolio because Betterment ensures it’s balanced and allocated based on your preferences.

Here’s a quick video that goes over how Betterment works:

When you open an account, they will ask you a series of questions to help determine how much risk you’re willing to take on and your investment goals. Betterment has its own proprietary algorithm that allocates your investments based on your risk tolerance and builds a corresponding portfolio.

Betterment also offers different account types and other features that simplify the process for the average investor.

Account Types

Betterment customers can invest in an IRA (both traditional and Roth), and the company even supports SEP IRAs and SEP 401(k)s.

This means you can also roll over your 401(k) or existing IRA to one with Betterment. Here’s more information on how to do that.

The ability to invest in an IRA through Betterment is important for those who prefer to invest their money via tax-advantaged accounts.

In addition, you can use it to open individual and joint taxable accounts and trusts.

Tax Loss Harvesting

If you have a taxable investment account, you can offset some of the taxes you’ll pay on gains through tax loss harvesting.

If done incorrectly, it can cause penalties, so it’s not something you want to try without understanding it.

However, Betterment takes the guesswork out of the process by doing it for you automatically. They help you reduce the tax impact of your taxable investments by buying and selling assets at the best times to offset the taxes on shares that have increased in value.

Automatic Rebalancing

Creating a diversified portfolio with the right mix of assets for your risk tolerance is only the first step. Since markets go up and down, your asset allocation will shift over time, throwing off your portfolio mix.

To avoid this, you have two options:

- You can monitor your portfolio and rebalance it regularly to keep your asset allocation consistent, or

- You can let Betterment handle this for you, saving you the headache.

It can be a great time-saver and allows you to focus on other important tasks.

RetireGuide

One feature that makes Betterment shine is their retirement planning section.

Their proprietary algorithm will help you pinpoint how aggressive you need to be with your asset allocation and how much you need to save every month to reach your goals.

The financial outlook tools help you project how much you will have in retirement based on your current savings habits and how changing the variables alters this equation.

It’s a great way to visualize how the amount you contribute or your risk tolerance can affect your income in retirement.

Flexible Portfolios

If you want to have more control over your portfolio’s asset allocation, Betterment allows you to create your own flexible portfolio. You will need to have at least $100,000 in your account to access this feature.

If you reach this threshold, you can choose your individual asset classes and the percentage to invest in each one instead of going with the mix suggested by Betterment.

You will still get feedback from Betterment, but the ultimate asset allocation is up to you.

Charitable Giving

Betterment gives you the option to donate to charities directly from your account. This can be helpful with capital gains taxes since they are waived on donated shares.

To be on the safe side, check with a tax advisor or a financial planner who can advise you on the best course of action when balancing taxes with charitable giving.

Financial Advice Package

Sometimes you need a financial advisor for significant life events but don’t know where to turn.

Betterment has stepped up to fill that need by offering the ability to connect with a certified financial planner to get advice on particular questions.

Betterment offers these packages as a supplement to its other services. There’s something for every situation – from getting started with investing to retirement planning.

Package options include:

- Getting Started – $149

- Financial Checkup – $199

- College Planning – $199

- Marriage Planning – $299

- Retirement Planning – $399

How to Invest with Betterment

This is where Betterment differs greatly from a traditional brokerage.

After you open a Betterment account and connect a bank account, you choose your investing goal and timeline. Then you choose your asset allocation.

At that point, Betterment takes over and handles the rest. You are free to move on and let Betterment do their work.

At that point, Betterment takes over and handles the rest. You are free to move on and let Betterment do their work.

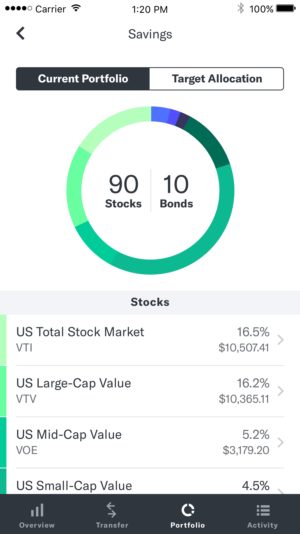

They invest your money in a mix of stock Exchange-Traded Funds (ETFs) and/or treasury bond ETFs. Here is more information on ETFs.

If you set up an automatic investing transfer (highly recommended) then Betterment will pull the money each month and invest it using the original asset allocation.

They also periodically re-balance your investments so you maintain the proper asset allocation. Here’s what you need to know about asset allocation.

The complete list of Betterment funds:

- VTI: Vanguard Total Stock Market

- SCHB: Schwab U.S. Broad Market

- ITOT: iShares S&P 1500

- VTV: Vanguard Value

- SCHV: Schwab U.S. Large-Cap Value

- IVE: iShares S&P 500 Value Index

- VOE: Vanguard Mid-Cap Value

- VEA: Vanguard Europe Pacific (EAFE)

- SCHF: Schwab International Equity

- IEFA: iShares Core MSCI EAFE

- VWO: Vanguard Emerging Markets

- SCHE: Schwab Emerging Markets Equity

- IEMG: iShares Core MSCI Emerging Markets

- VBR: Vanguard Small-Cap Value

- IWS: iShares Russell Midcap Value Index

- IJJ: iShares Mid-Cap 400 Value

- IWN: iShares Russell 2000 Value Index

- AGG: iShares Core U.S. Aggregate Bond

- BND: Vanguard Total Bond Market

- MUB: iShares National Muni Bond

- TFI: SPDR Nuveen Bloomberg Barclays Municipal Bond

- VTIP: Vanguard Short-Term Inflation-Protected Securities

- HYLB: Xtrackers USD High Yield Corporate Bond

- JNK: SPDR Bloomberg Barclays High-Yield Bond

- HYG: iShares iBoxx $ High Yield Corporate Bond

- SHV: iShares Short Treasury Bond

- NEAR: iShares Short Maturity Bond

- BNDX: Vanguard Total International Bond ETF

- EMB: iShares J.P. Morgan USD Emerging Markets Bond

- VWOB: Vanguard Emerging Markets Government Bond

Is Betterment Right for You?

While Betterment is a good option for some people, it’s not the right fit for others.

Active, sophisticated traders may say that Betterment dumbs down investing and does nothing to educate investors. However, the simplicity of their offerings can be a boon to busy business owners who want someone else to handle their investing.

Betterment lays out their philosophy very clearly on the site.

They also provide details about each of the ETFs they used to build your portfolio. Even seasoned traders can’t consistently beat the stock market.

Trying to time the market is nothing more than gambling with your money.

Simple, passive investing can be your friend, and not enough people use it to help grow their investments. Too many people are trying to day trade, or worse, not investing at all.

Betterment helps to bring more people onboard with the passive investing style.

Another common gripe is the pricing structure since Betterment used to be considered pricey.

At their old price point, it was easy to beat Betterment by going to a low-cost ETF provider like Vanguard.

But now that Betterment has lowered their fees, they are very competitive.

While avoiding fees in investing is important, it’s better to have people invest with a simple solution to investing (even if it costs more) rather than avoid investing because the complexity makes them nervous.

Betterment Checking and Cash Reserve

Betterment is no longer just a “robo-advisor”, they are a smart money manager.

Betterment Checking has no fees. No monthly maintenance fees, no minimum balances, and no overdraft fees. They will also reimburse ATM fees directly to your account.

With Betterment Checking you can seamlessly move money between all of your Betterment accounts, including Investing and Cash Reserve. The app allows you to sign up for an account, transfer funds, activate your debit cards, and more with complete ease.

Find all the details for Betterment Checking.

Betterment Cash Reserve is a no-fee, high-yield cash account designed specifically for the money you save every day. There are no limits on how often you move your money and there are no fees when you move your money.

Cash Reserve doesn’t offer a set rate like a bank. It tracks the rate set by the Fed, and at 4.20% APY* (variable) is earning more than the national average.

Read more about Betterment Cash Reserve.

Betterment vs Wealthfront

If you’re comparing robo-advisors, chances are you will run across Wealthfront as another option. Since they are both automated online investment platforms, they are good options for those looking to get started.

Both Betterment and Wealthfront offer professional portfolio management for a reasonable, low cost.

But which one comes out ahead? Check out this comparison of Betterment vs Wealthfront to help you decide which robo-advisor better fits your needs.

Betterment vs Vanguard

When it comes to low-cost investing, Vanguard is the name that pops up everywhere you look.

Founded by John Bogle, it offers low-fee index funds that funnel your money toward growing your portfolio instead of paying people to manage your investments.

You can invest in Vanguard’s target-date funds and pay less than with Betterment. As a bonus, these funds re-balance automatically but keep in mind that they force you into one of a few five-year increment plans.

What Betterment is counting on though is that the Vanguard account and choice of funds are too complex for some investors. Their website is not very user-friendly or simple to use.

The statistics show that not enough people are investing in their future. Here are common reasons people don’t invest for retirement.

Vanguard is geared toward the do-it-yourself investor looking to minimize costs while maintaining full control of their portfolio.

Betterment takes the guesswork out of portfolio allocation and helps you invest your money consistent with your goals and risk tolerance.

Which one is better? If you want to find out more, head over to see the full comparison of Betterment vs. Vanguard.

Related: Our Vanguard Personal Advisor Services Review: Have a Human Advisor Review Your Plan

Quick Recap

Here’s a quick summary of why Betterment can be a good option for you:

- They are built for the 21st century – slick interface with little complexity in their setup.

- They limit their fund choices to arguably the best choices for the passive investor: broad index-based ETFs.

- They highly encourage automated investing, the best way to ensure you keep investing.

- They offer retirement investing through IRAs.

- They promote the idea of passive, long-term investing.

- They are transparent about their fees, and they keep fees simple.

- They are highly liquid. You can move your money in and out of the brokerage without fees.

Who Should Use Betterment

If you aren’t investing at all or don’t have an IRA, consider Betterment since it can simplify the process for you and get you on the right track. Betterment can also be a good option if you’re looking for a place to roll over your 401K or existing IRA.

If you’re already doing passive investing with ETFs, compare your expenses with Betterment’s fees Betterment and services to see which one is a better deal. What makes the robo-advisor shine is the simplicity of its offering, which makes it accessible to the average investor.

Try Betterment today and put your investments on auto pilot .

Excellent post. I plan to use betterment after I finish paying off my debt.

You don’t lose money in a traditional savings account?

One reason I invest with Betterment is because I am one of those people that just can’t get it or figure out investing. I am above average in some areas but finance is not one of them.

That said, I have figured out that if you put your money in a savings account that pays less than the rate of inflation, you lose money from day one. Unfortunately, all the savings accounts I qualify for do not pay more than the rate of inflation. Maybe someone can explain to me how losing money in that fashion is OK?

I am guessing there is something I am missing because, apparently, most people don’t see it that way?

what don’t you like about betterment?

I was in the “savings in a mattress” account category. We are good savers and max out the tax-preferential accounts. Have the nest egg covered (6 months). But after a kick in the pants from Mr.Money Mustache I decided I needed to move to actual investing and get the rest of the money working. Went to Betterment for the ease of use. Feet wet now trying find some advice for passive, don’t know a whole lot “investor” — What is advantage over date specific Vanguard fund? I do have several betterment “pots” (vacation, car fund, and such) and those were really easy to put together and auto fund.

I think that Betterment is great for someone who doesn’t have an idea of the specific investments they want to put their money toward. I love that they focus on Index ETF’s but I prefer to have a little bit more control over my specific investments. This is a great review, and for people who aren’t investing at all Betterment is a great place to start. Thanks for the post.