Here’s What You Should Do When You Pay Off Your Car Loan

Did you just pay off your car loan?

That’s awesome! Fist bump to you, my friend.

When I paid off my car, I was so excited I announced it on Twitter:

https://twitter.com/ptmoney/status/1121228868

Felt good, man!

In response to my tweet, a friend tweeted back with this excellent point about car insurance:

Consider evaluating your insurance coverage. Requirements are higher when there’s a lien on the vehicle. Now, you can decide!

And you know what? This is a great point.

It got me thinking about all the other things you should do once you truly own your car.

What To Do When You Pay Off Your Car Loan

Paying off a vehicle loan means you have opportunities to make some financial changes. Some of the steps you should take once your car loan is paid off include reviewing your budget and insurance, obtaining the title, and checking your credit score.

Before I dig into these next steps, however, give yourself a good pat on the back for knocking out this debt.

Heck, maybe consider a celebratory car wash and a photo op next to your car with the title in your hand. 😉

Now, here are all the things you should do next:

Table of Contents

1. Review Your Budget

Since you no longer have a car loan payment, make sure you designate a new purpose for the monthly payment you were making.

Don’t just let frivolous spending absorb your extra money—you wouldn’t want to let it go to waste!

Decide whether you want to:

- pay off other debts

- build up some savings

- invest in your future

If you already have ample savings, I’d suggest continuing to pay off other debts using the snowball method.

Also, if you’re using a program like Empower, YNAB, or any one of the other budget software options, you’ll want to update your budgeting allocation to show you’re no longer paying against your old car note.

Related: The Best Personal Finance Budget Software With Apps

2. Put Your Old Payment To Work, First

If you decide to start saving or investing the funds you’ve recently freed up, be sure to find a good, safe home for them.

But also consider how to make your money work for you, instead of it sitting idly by.

A no-brainer approach would be to store some of this newfound cash in a high-interest savings account designated for an emergency fund or special savings account.

Consider CIT Bank Savings Builder

The CIT Bank Savings Builder account is a terrific option for you if you’re ready to earn decent interest on your savings.

CIT Bank Savings Builder offers two ways to earn a high-interest rate.

You can get the top rate by:

- maintaining a minimum balance of $25,000 in this account

- making a $100 minimum deposit each month

This is a great choice for many of us since not everyone has enough cash lying around to keep $25,000 in the account, but most of us could save $100 a month. It’s likely the car payment you just eliminated from your budget totaled more than $100 a month, so you should easily be able to reach this minimum!

It’s pretty exciting to think about—instead of sending your hard-earned cash to the loan company each month, your cash is going towards more savings, knocking out debts, or heck, a little splurge here and there!

Of course, another option is to begin investing your extra dollars.

Maybe you already have a robust emergency fund and you want to start participating in the stock market. Investing your money comes with risks, but by diversifying your investments and dollar-cost averaging, you can reduce some of the risk and see your money grow.

If you’re interested in more of an active investing approach, using an online stock broker might be a good fit.

If you’re more into a passive approach, robo-advisor options might be a good choice.

3. Lower Your Car Insurance Costs

Your car insurance premiums won’t just go down because you paid off your car loan, but it’s possible.

However, it’s probably still a good time to review your insurance coverage, especially if you think you can lower your coverage details, where it makes sense, to lower your monthly bill.

In some instances, if your car is really old and not worth much, it might make sense for you to drop comprehensive coverage—I’m not an agent though, and I don’t know your particular situation, so please consult an insurance professional or agent.

The biggest point to note is the finance company (i.e. the lienholder) doesn’t get to tell you what to do here anymore!

You can get any type of auto insurance you want as long as you meet your state’s minimum requirements.

I highly recommend also getting a few quotes (from someone other than your current insurance agent/company) to learn whether you could purchase more affordable auto insurance elsewhere.

I recommend getting quotes from different providers and comparing them to see how much you can save. I suggest:

- eSurance (an Allstate Company)

- Gabi (an online broker)

- Liberty Mutual (one of the most trust insurance companies)

Gabi shops for your car & home insurance - saving you $865 on average! No fees, no forms, no spam.

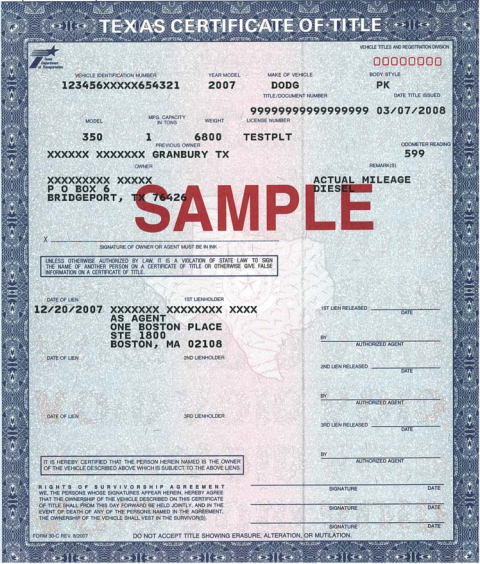

4. Get Your Title and Store It (Safely)

Getting your title once you pay off your loan can actually take a long time.

It’s best to go ahead and initiate the request to avoid putting yourself in a situation where you need it in a hurry (like when you decide to sell the car).

Some states have the lien holder (the company who you made loan payments to) physically hold the title.

If you reside in one of these states, you’re likely to get your title back pretty fast (as soon as your payment clears and they have time to notify the department of motor vehicles in your state.)

It should look something like this (varies by state, of course):

Once you get your title, store it in a safe at home.

DO NOT just put it in the car itself. In the event of a fire, or even theft, you’d have to seek out getting a replacement, which can be a real hassle.

I suggest snapping a picture of the title, too, so you can keep a digital copy for quick reference.

5. Check Your Credit Score

Be sure to check your credit report with a service to review your note is recorded as paid.

The primary reason is to ensure your car loan is listed as fully paid off and reported to each credit reporting agency as such.

The secondary reason is to double check you actually paid it off—you’d be surprised how many people make a final payment but miss a small amount of interest. More often than not, lien holders make you request a “final payoff amount” in which is calculates these interest accruals, but it’s worth checking twice.

Now, be aware paying off a loan can actually cause somewhat of a dip in your credit score.

The credit bureaus each look at how well you manage credit and debt in the present, not debts you’ve paid off in full.

However, thankfully, the impact should even out eventually. I suggest using Credit Sesame or Credit Karma to provide the info you need to monitor your credit.

Credit Sesame

You can get a free credit score from Credit Sesame.

They pull your credit information from TransUnion to get your VantageScore, which is similar to (although not exactly the same as) your FICO score. You’ll receive monthly updates of your score.

Credit Sesame is easy to use, especially if you log into their apps for either Android or iPhone.

Another perk of Credit Sesame is their free Identity Theft Protection valued at up to $50,000.

Credit Karma

Credit Karma works much like Credit Sesame in that it provides free credit score updates.

One key difference is Credit Karma provides your VantageScore from both TransUnion and Equifax.

Plus, you can receive a full credit report (not the same as your credit score) from both of these credit agencies for free.

Credit Karma updates your credit score weekly, whereas Credit Sesame updates monthly. So if you prefer more frequent updates, it’s something to consider.

Credit Karma, however, does not offer any financial coverage in case of identity theft.

In either case, just remember: getting your credit score updated to reflect the paid-off auto loan may take some time, so don’t stress about it if it takes a few months.

Related: The Best Free Credit Score and Monitoring

6. Turn Your Car Into a Money-Making Machine

Since you own your car free and clear now, you could consider using it to start a little side hustle to bring in extra money!

I love this idea because you’re really flipping the script on your finances—going from debtor to cash flow positive, baby!

You could start driving with Uber or Lyft, for example.

Your car does have to meet a minimum year model depending on the city you drive in, but I know a lot of people who do this simply on their commute.

If you are looking for something a little more passive, consider a service like Turo, where you turn your car into a rental car. You decide when you want to rent it out.

Here are some other ways:

Drive for Doordash

Doordash enables you to earn money with your car if you’re willing to deliver food around town. It’s available in over 4,000 cities in the U.S., Canada, and Australia.

What’s great about Doordash is you can deliver and earn extra cash whenever and however often you like.

Plus, it’s easy to qualify; as long as you’re 18 and have a vehicle, you can drive for Doordash. There are no model or year restrictions on the car you can use.

Check out our Doordash review here.

Is it Always Good to Pay Off Your Car Loan Early?

There are a few good reasons to pay off your car loan early:

- save money on interest

- free up the monthly car payment for other uses

- the extra payments are earning a guaranteed return equal to the interest rate of your loan

- eliminating the responsibility of the payment if something were to happen

There is one good reason to not pay off your car loan early, though:

- you could potentially earn more money by investing the extra money

What do I mean?

Let’s say you have a $5,000 balance left on your car note at 4.7% and you have $5,000 sitting in savings. Should you take the money and pay off the debt?

Paying off the car loan would earn you a guaranteed 4.7% which is pretty good, certainly more than you are earning in a savings account.

But could you earn more money by say… investing in the stock market?

Maybe. Maybe not.

Let’s take a look at some actual numbers.

If you had a loan with a balance of $5,000 at 4.7% being paid off over two years, you would pay $248 in interest. That is the guaranteed cost of that loan, so paying it off today would essentially earn you a guaranteed $248.

If you could earn more than $248 by investing the $5,000 then you could argue it would be a better financial decision. The trouble is the $248 in interest savings is guaranteed.

If you are comparing paying off the loan against investing in the stock market then you are not comparing apples to apples—you are comparing an investment with risks to a guaranteed return.

Not the same thing at all.

Yes, on average the stock market earns about 11% per year, but that’s over a long period of time—like 30 years!

Two or three years is too short to be able to make any assumptions about what the stock market is going to do.

Considering the other benefits, such as eliminating the car payment from your budget and freeing up cash flow, to me this is a no brainer.

I believe you should pay off your car loan early if you have the opportunity to do so.

Now, Enjoy Your Paid Off Vehicle

Lastly, I’ll just add you should count your blessings and soak up that paid-off-car feeling. It’s a great financial milestone to have reached.

With your new extra income, maybe you can now afford to buy something you’ve been putting off, like a fun vacation, a big donation to charity, or a thoughtful gift for a loved one.

Can you think of some other smart moves to make when you pay off a car loan?

First, PT, congratulations on paying off the debt!

Sorry to be the conspiracy realist, but you still do not own the vehicle. In fact, you own nothing. No American citizen taxpayers own any property, period. The illusion of ownership exists, but in reality, you do not own your vehicle.

Well, then who does own it?

Refuse to pay your car taxes, and you will quickly discover who really owns the automobile. Ownership implicitly implies complete control of and possession thereof. How can you own something, but the local/state/federal government can seize it, and possibly attack your character, fine you with financial penalties, and potentially even arrest you and hold you against your will?

What if you refused to pay fines from parking tickets? What if you refused to pay moving violation fines? What if you decided you would rather not pay for a registration of your vehicle, refuse to pay for emission testing, etc.?

Please stop and consider this. Now, apply what I just stated above, to your home.

You own nothing, because slaves are not allowed to own property.

This is not an argument about the “moral obligation” to pay property taxes, so roads and schools and fire fighters and police can function, all considered necessities for a civil society. The argument is ownership. And if you refuse to do something (exercising your free will, disallowing coercion), in this case, paying money to an government entity, and as a result of your free will decision, your property can and will be confiscated; in plain words, stolen. This can not possibly be true if you are the owner.

Peace be with your spirit, please consider my words.

This comment has no place on a financial advice website. It’s political propaganda.

It is also false. And illogical.

Should you payoff a 2.49% $6,500 car note that is scheduled to be paid off in 14months? not strapped for money right now. Just trying to decide whether to put my cash in my investment accounts or pay off the note then make these payments towards my investment accounts. Decisions, decisions?

@YR Yeah, that’s a tough call. I think you need to factor in things like how happy you’d be to be debt free of the car note. There are more emotional factors here than technical/financial ones. Dave Ramsey says to help sort this out in your mind, ask yourself if you would take out a 2.49% loan to invest with? If you wouldn’t, then you probably should get rid of the debt.

@Philip Taylor Thanks. I have been visiting a few other website by far this is the easiest to understand from my perspective. I appreciate the reply. I will be paying off the car loan and sending the payment directly to my investment accounts.

I found this blog by searching Google for “What happens when you’re done paying off a loan”. I see from your blog that there are no additional steps to do for that loan after it’s paid off… i was sure there would be, considering all the crap you have to do to get it. Maybe a “Good-bye!” or “Congrats” from the lender 😛

Anyway, congrats on your loan payoff!

I’ll be done paying my car loan in November, can’t wait. But I hate that I’m already thinking of leasing a new car which will drain more money than my current car payment.

Thanks, Elliot!

Way to go. I think so many people forget that a car is an expense. That is a nice burden to not have to pay every month.

re titles – they should be registered with your state or county. You can request a certified or replacement copy for a nominal amount. When you get it, there should be a place that lists any lein holders. Be sure that area is blank. If not, contact the lein holder to get a lein release.

Funny story. Paid cash for my last car, using a cashier’s check from my credit union. The dealership paperwork showed that there was a lein to the credit union. So AFTER the title was processed, I had to haul it to the credit union to get a release for a lien that never existed in the first place.

Another reason to bank at a local CU – bet I couldn’t have taken care of it over a lunch hour if I banked with a national ‘chain’ bank.

I would call my State’s dept of motor vehicles and ask them. They should have a process for this.

I paid off my Saturn yrs ago and never received the title to the car. We are trying to get rid of car but need title to do so.The place we financed with is no longer around. What can we do???? It frustrating. Thanks

Congrats! You must feel fantastic and I bet it just got a little bit easier to breathe.

1. I would give it a nice car wash and wax, complete detailing, unless you live in the great white north of winter and then I would give a nice car wash to get rid of the salt.

2. Fill it up! I bet all of sudden your miles per gallon will increase with out that payment.

3. Check the insurance to raise my deductibles or even get rid of the collision coverage depending on the age of the car.

Congratulations to you again! Very inspired by your success!

Gooooooooooood work son! It’s a might fine day in your neck of the woods – soak it all up 🙂

Ummm….that was the second most awesome rap I’ve ever heard (first place goes to PTMoney’s PYF challenge rap, of course).

Congratulations! That’s terrific!

When I paid off my car loan I continued to make a payment, but this time it was to myself. My savings account grew large enough that I’ve been able to pay cash for our last two cars (though I did put as much as possible on credit cards so I could get the reward, then paid it off immediately).

Because you do have a baby on the way I agree with your plan to not earmark the additional money towards paying off other debt yet, but I’d still likely throw an extra $25 a month towards principal while you wait and see (that is, if you have a sufficient emergency fund). You likely won’t miss it, and every little bit helps.

About changing your insurance coverage, remember that the only two coverages that have anything to do with the type of car you have are Comprehensive and Collision, as those are the only two coverages that are on the car itself. You don’t want to reduce your liability or uninsured motorist coverage, as they have nothing to do with the type of car you drive; you can do just as much damage with a brand new car as an old clunker!

You need to find out how much you pay for each of those coverages, and determine your deductible. Get quotes for raising the deductible and for eliminating the coverages altogether.

I suspect you’ll find that you won’t save as much as you think, especially with Comprehensive coverage. And if you remove them you will be completely out of luck if you get into an accident that is your fault, if it’s a hit and run or if the at-fault party doesn’t carry enough coverage to fix your car. Also, you’d have no coverage if it’s stolen, damaged in a hurricane, etc.

That’s almost an entire post right there, but believe it or not I have more to say on this subject. I’m going to write a post about this on my own blog, so look for it!

And once again, congrats for paying it off!

We paid off my car in August of last year. But we ended up going into debt on my wife a newer car so we’re only saving an extra $100 a month which goes into paying off student loan debts.

Congrats! My advice it to take the (former) car payment and split it between paying off debts and saving/investing.

You are so right about the lien! Make sure you get it either in your name or with a letter stating your loan was paid in full. I didn’t realize I was missing my lien when I traded in my car. The dealer was able to get it for a small cost but it was something that could have held up my purchase.

When I paid off my last car the money all went into savings each month. That felt great!

Awesome PT. We have been driving paid for cars for over 4 years and it is great.

You might want to think about saving for a replacement depending on the age of the car. It is much easier to save $50 a month for 5 years and have 13k rather than wait till the car is on its last legs.

I love the idea of a celebratory car wash. I tend not to have my car washed because I don’t want to spend the money, but I know that it is good for the car to be clean once in a while. What an appropriate way to celebrate!

Thanks, that’s excellent advice.

Yay! That’s so awesome that you’ve paid that off. Looks like you’ll be able to take your baby home from the hospital in a paid-for vehicle! I’m jealous!

We have about $6k to go on our car loan, and then we’re done. Soon enough! And I’ll definitely take it for a celebratory car wash 🙂

Congrats! We paid off our car last year, and it felt great. We take the money and put it in a “car fund.” When our car dies, or needs repairs, we can just take the money from the car fund. What we’re really hoping for is that the car lasts long enough that we will be able to pay entirely with cash from the car fund when the time comes to purchase again.