My Medi-Share Review | 10 Years of Healthcare Sharing

I‘ve been with Medi-Share for ten years. This is my review of the Christian healthcare sharing program, updated for the new enrollment.

I’m currently paying ~$430 per month to cover my family of five.

Prior to joining this healthcare expense-sharing community, I was paying a staggering $1,100/month for a health insurance plan through Humana!

This is a monthly savings of around $650 per month. That’s more than $78,000 in savings over eight years!

Keep in mind, however, Medi-Share is NOT health insurance (nor is it charity), but it’s a great alternative to expensive healthcare coverage for some.

Medi-Share Review Snapshot

Medi-Share makes sense for my family because:

- We are self-employed Christians and don’t mind being obligated to the coverage restrictions related to lifestyle.

- Our income will likely exclude us from being subsidized in the federal government’s health insurance marketplace; Medi-Share gives us considerable monetary savings.

- We don’t have pre-existing conditions and we don’t plan on having any more children (i.e. we don’t have maternity care needs).

I’ve been with them for eight years and I believe his health insurance alternative will continue to be a great option for my family for years to come…and could be for yours, too.

Medi-Share is a non-profit, medical expense sharing program for Christians. Members share in each other's health expenses.

Full disclosure, I’m an affiliate for Medi-Share and make money for referring you to them. Now for the full review…

Table of Contents

What is Medi-Share?

Medi-Share is a healthshare plan where Christians share financial resources to pay for each other’s medical expenses. Since 1993, over $875 million has been shared and discounted among Medi-Share members. It’s a proven biblical model of healthcare–Christians helping Christians.

Medi-Share is a non-profit, medical expense sharing program for Christians. Members, quite literally, share in each other’s health expenses (hence the name). Essentially, each month, everyone places their monthly share (like a premium) into one big pot (technically a credit union account,) and those with expenses use the money to pay their bills.

However, it’s not insurance. But for some, it can be an ideal replacement for health insurance, its high premiums, and impersonal service.

Read on to learn more about how Medi-Share works, its advantages and disadvantages, as well as my lengthy personal experience so you can know what to expect if you think it’s a good option for you or your family. Learn more about Medi-Share here.

How Does Medi-Share Work?

If you’re unfamiliar with Medi-Share, here’s a nice video sharing the basics of how their healthcare sharing ministry got started and works today.

Annual Household Portion

Members choose an annual household portion (AHP), which is similar to an annual deductible. The size of your portion determines how much you will have to pay out-of-pocket for covered medical expenses before the health share kicks in. You get to choose both the AHP and the monthly share from the provided chart.

The size of the AHP you choose will determine your monthly share.

Here’s what a sample chart might look like for a middle-aged couple with at least one child living in Texas:

*All options shown include eligible care for hospitalizations, emergency room, urgent and primary care visits, and FREE telemedicine consults. Discounts on prescriptions, dental, and vision needs are also included.

For my family of five, we chose a $10,500 AHP, which is high, but it means a lower monthly share. Note that this is a grandfathered level, essentially equivalent to the $12,000 level today.

In the case of an emergency, we could handle having to pay $10,500 out of pocket from our emergency fund, and we enjoy the savings the lower monthly share affords us.

If your family would struggle with such a high AHP, you should choose a lower AHP—just be prepared for higher monthly portions.

Start here or call 800.772.5623 to get your pricing.

Provider Fee

As with traditional insurance, you will still pay a provider fee (like a co-pay) of $35 for doctor visits and $200 for emergency room care.

Routine well-patient care—such as annual physicals—and dental and vision care are not covered by Medi-Share, so you need to be prepared for those expenses throughout the year.

Preferred Provider Organization (PPO)

Medi-Share is partnered with the preferred provider organization Private Healthcare Systems, Inc., or PHCS, and members are encouraged to seek care from providers within the PHCS network.

Though you are free to choose treatment with an out-of-network doctor—but if you do, a penalty may be applied for going out of the network.

Here’s a quick video I created to show you how to see if your doctor is in the Medi-Share network:

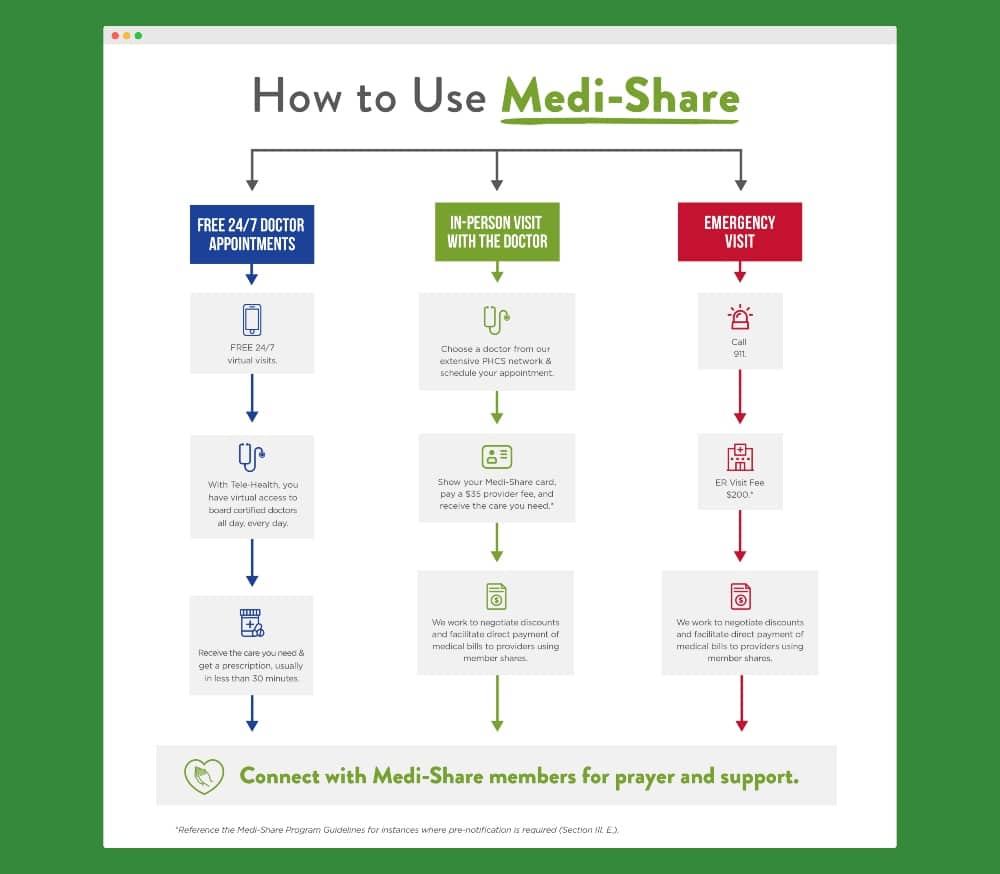

Doctor Visits

When you need medical care, you will hand over your Medi-Share card and pay your provider fee; then, the provider will bill Medi-Share the remainder.

After the medical bill is processed and discounted your doctor will bill you for the amount you owe.

Once the amount you pay meets your AHP for the year, your eligible medical bills will be approved for sharing.

Health Incentive

Families may take up to 3% off their monthly share amount by qualifying for the health incentive.

To qualify, all adult Medi-Share members in the household must meet certain health criteria, including:

- Blood pressure under 121/81

- Abdominal circumference of <38″ for men and <35″

- BMI between 17.5 and 25

You need to complete an online health form at the time of application (or upon re-review) in order to secure the discounted rate.

It was this health incentive that has helped spur me to lose some weight over the past couple of years—and it put money back in my pocket in addition to improving my health!

Medi-Share Coverage

Below is a quick breakdown of what Medi-share will and will not cover.

More details about Medi-Share coverage can be found in their guidelines. The member-approved guidelines detail the program requirements, qualifications, and what sharing is covered. Visit this page to get started and see their full guidelines.

What Medi-Share Does Cover

Here are a few of the medical expenses that are eligible for sharing with Medi-Share.

- Doctors visits

- Medi-Share offers free telehealth access. Talk to virtual doctors at absolutely no cost to you via MDLIVE.

- If you need to see a doctor in person, choose a physician that is a member of PHCS, Medi-Share’s preferred primary provider organization (PPO). You’ll pay a $35 provider fee that does not count towards your AHP. And you’ll also eligible for in-network discounts.

- Emergency room visits: Members must pay a $200 provider fee that does not count towards your AHP.

- Hospitalizations: Members must pay a $35 provider fee per hospital visit that does not count towards your AHP.

- Prescriptions: Up to 6 months of FDA-approved prescription drugs per eligible treatment.

- Maternity:

- Sharing is limited to $125,000 for any single pregnancy event.

- To be eligible, your AHP must be $3,000 or higher and you must have faithfully shared from the month of conception through the month of delivery.

- Well-child care: Sharing for routine well-child care is eligible until the child reaches the age of six.

- Professional Counseling Services: Free mental health counseling is available through a Medi-Shares preferred provider. Mental health calls are limited to 30 minutes but you are allowed unlimited visits.

- Physicals: Each member is allowed one physical per year for sharing. The physical includes sharing for two labs—a basic Lipid panel and Hemoglobin A1C.

- Adoption costs: For members who meet certain criteria, up to two adoption events can be shared per household.

- Senior assist: Seniors with Medicare Parts A and B can enjoy the benefits of healthcare sharing of medical bills that Medicare doesn’t pay, including copayments, deductibles, hospitalization and out of country urgent care.

- Disability expenses: Through their Manna program, Medi-Share is able to replace up to 80% of lost income for up to a year for Manna members.

- Final expenses: Up to $5,000 of funeral expenses are eligible for sharing.

What Medi-Share Does NOT Cover

Ok, so now let’s take a look at a few of the expenses that aren’t eligible for sharing with Medi-Share:

- Dental, vision, and hearing: While these expenses aren’t eligible for sharing, Medi-Share does give members savings cards that provide exclusive discounts.

- Dental: Save 20% to 60% on most dental procedures.

- Vision: Save up to 30% on eye exams, glasses, contact lenses, and LASIK surgery.

- Hearing: Save 30% to 60% on hearing aids.

- Routine and preventive care: Including physicals, immunizations, vaccines, mammograms, some lab studies, and colonoscopies.

- Fertility/infertility care: Including birth control, infertility testing, and sterilization.

- Alternative care: Including vitamins, acupuncture, and experimental treatments.

- Some Counseling: Including dietary counseling, diabetic counseling, lactation counseling, or genetic counseling.

- Behavioral or mental care

- Cosmetic procedures

- Non-prescription drugs

- Hearing aids

Medical Expenses Eligible for Limited Sharing

The following expenses are eligible for sharing under certain situations, such as when ordered by a certified physician, when medically necessary, or when supported by current medical treatment standard of care.

- Ambulance (or other medical transport services)

- Cardiac rehabilitation (up to 36 sessions)

- Chiropractic care

- Durable Medical Equipment (DME)

- Genetic testing

- Home care (limited to 60 calendar days)

- Non-hospital admissions

- Outpatient speech therapy (up to 10 visits)

- Physical therapy (up to 20 visits)

- Prostheses

- Psychiatric or primary care evaluation

- Sleep apnea studies

Advantages of Medi-Share

Let’s explore some of the positives of this sharing program.

Escape the Market Altogether

Before Obamacare came along, I used to pay $300 a month for a $10,000 deductible health insurance policy.

I am self-employed and make a solid income. However, once the law was passed, my monthly premiums shot up to $1,100 a month!

With the future of American health insurance still being unclear, you may feel uncomfortable with a system that is being tinkered with in real-time and Medi-Share allows you to leave it all behind.

You Can Join Anytime

That’s right. You can apply for Medi-Share and join it anytime during the year.

With the implementation of Obamacare, you were forced to join within their open enrollment period, which runs from November 1 to December 15, unless you have a change in status (moving, having a baby, etc).

You may be looking at this review during open enrollment but understand you can jump on Medishare anytime during the year. And you don’t need one of the special exemptions to make the move.

It’s Significantly Cheaper

Compared to unsubsidized health insurance under Obamacare (Healthcare.gov), Medi-Share is a huge money saver.

My own family’s switch has shown very significant savings (see below for details).

Medi-Share is affordable compared to health insurance because they can be more discriminate in who they serve.

Direct Primary Care

Medi-Share gives members access to Direct Primary Care (DPC) by allowing DPC fees to be submitted for sharing.

To be eligible, you must be under the new $12,000 AHP (see below for the new AHP program options). Only $1,800 of your DCP fees are qualified for sharing.

DPC is a way to receive primary medical care for a fixed monthly or quarterly fee. The fee can range from $50-$100 per month and be applied to your AHP. Fees vary based on if you are single or have a family and your location.

Services provided under a DPC will depend on your provider and include office visits, vaccines, lab work, and annual physicals.

The focus of DPC is primary care and usually does not cover emergency or specialty medical services.

It’s a good fit to save money on routine primary care with the higher $12,000 AHP option. I personally haven’t found the DPC necessary because our family just doesn’t use medical care very often.

Disadvantages of Medi-Share

However, there are some disadvantages to Medi-Share, too:

No Health Savings Account (HSA) Contributions

Since Medi-Share is not insurance, you can’t qualify for a health savings account, or HSA.

HSA’s as you know, require you to have a high-deductible health insurance plan. This was a major bummer for me. I was really enjoying the annual tax deduction from contributions to our HSA.

Now, Medi-Share is working with Congress on a bill that might allow HSAs to be used with sharing programs. I’m contacting my Representative to ask him to support this.

Also, don’t worry if you already have funds in an HSA. You can still use them for qualifying medical expenses.

We plan to use ours for expenses that aren’t covered by our particular Medi-Share plan until we run out of funds.

No Tax Deductions

Health insurance premiums are tax-deductible. Medi-Share contributions are not.

That said, medical expenses are still deductible, subject to a threshold based on a percentage of your adjusted gross income, or AGI.

Have a business with a few employees? You may be able to deduct the cost of reimbursing them for their Medi-Share monthly share.

I did this myself by creating a flat-rate benefit that I give to my employees each paycheck.

Medical Providers May Not Want to Bill Medi-Share

There have been a few anecdotal cases of doctors and hospitals refusing to bill Medi-Share, and instead, asking the patient to pay out-of-pocket. In some cases, this may stem from the fact the PHCS network Medi-Share uses is not the universal PHCS provider network.

It’s incumbent on Medi-Share Members to call PHCS directly to confirm the provider you want to see is covered under the Medi-Share PHCS system.

That said, the anecdotes of providers being unwilling to bill Medi-Share have still had happy endings. In particular, this mother’s cancer treatment was prepaid by Medi-Share at self-pay rates after the provider initially refused to accept the plan.

The health share ministry made sure to come through for her.

However, receiving a huge out-of-pocket bill from a provider can come as a shock to a family who has already paid their full portion.

Since you want to be focused on getting well rather than on finances, this bears keeping in mind.

Is Medi-Share Good?

Yes, Medi-Share is good. It works to meet the needs of my family’s medical expenses, but it’s important to understand how Medi-Share works to make that decision for yourself.

My tithe to the Church or individual giving through certain charities is how I take care of that.

Medi-Share is simply sharing among believers. To have the right to share, you have to be a believer and live an active Christian lifestyle.

1. No coverage for medical expenses related to unbiblical (i.e. not Christ-like) activities

- Get injured in an accident where you were driving drunk? No coverage.

- Get an STD from an extra-marital affair? No coverage.

- Use tobacco? No coverage.

When you join Medi-Share, you agree to live your life according to biblical principles.

2. You must have a Christian faith and be attending church regularly

To participate in the program you’ll need to sign a form professing your faith and share your Church information.

3. Restrictions for maternity expenses

Expecting? Don’t expect to just jump on Medi-Share six months in and get full coverage.

You can have children on the plan, but to get full coverage you will have to be participating in the plan before you get pregnant.

Otherwise, coverage has limitations.

4. Restrictions for pre-existing conditions

Common sense dictates to make Medi-Share work, you can’t just have people jumping on the program after they discover a major medical need.

But Medi-Share members can receive up to $100,000 per year for pre-existing conditions once they’ve been faithfully sharing for at least 36 consecutive months.

And, they can receive up to $500,000 per year once they’ve been sharing for 60 consecutive months.

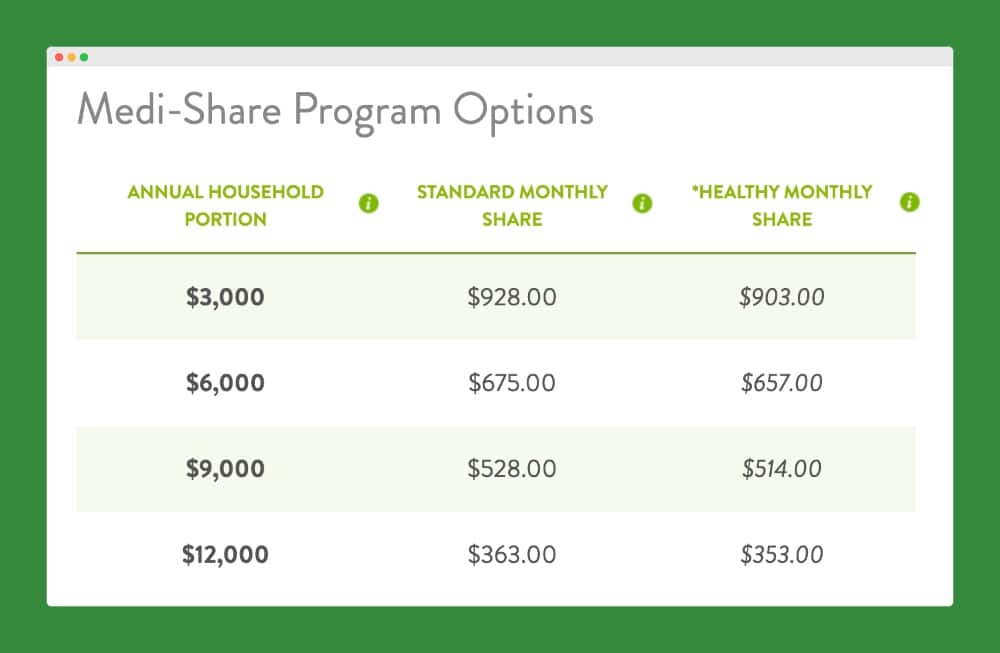

What Does Medi-Share Cost?

The cost of Medi-Share depends on your age, family size, marital status, the AHP you select, and the state you live in.

I’m in my mid 40’s with a wife and three kids. As a family, we pay ~$350 a month and have a $10,500 Annual Household Portion (i.e. our Medi-Share “deductible”).

For a lower deductible, like $3,000, then your monthly payment would be $928.

Here’s a chart based on my age and number of people on the plan:

We used to pay $1,100 a month with Humana.

So in just the first few months of being with Medi-Share, we had already saved over $4,000! And now, as I shared above, we’ve amassed over $70,000 in total lifetime savings.

Here’s how that first few months breaks down:

- With Obamacare (Healthcare.gov), we would have paid a minimum of $7,700 ($1,100 x 7 months) in premiums.

- With Medi-Share, we’ve paid $2,450 ($350 x 7 months) in premiums.

- Copays are roughly the same under both plans.

- With Medi-Share we’ve paid roughly $70 each for five sick visits for the kids, and $475 each for the two well visits (six months and nine months) for our son. This totaled up to roughly $1,352.83. The well visits were a shock, but still not as shocking as an Obamacare premium.

Here’s a screenshot of our deductible (annual household portion) usage as of our first year with Medi-Share:

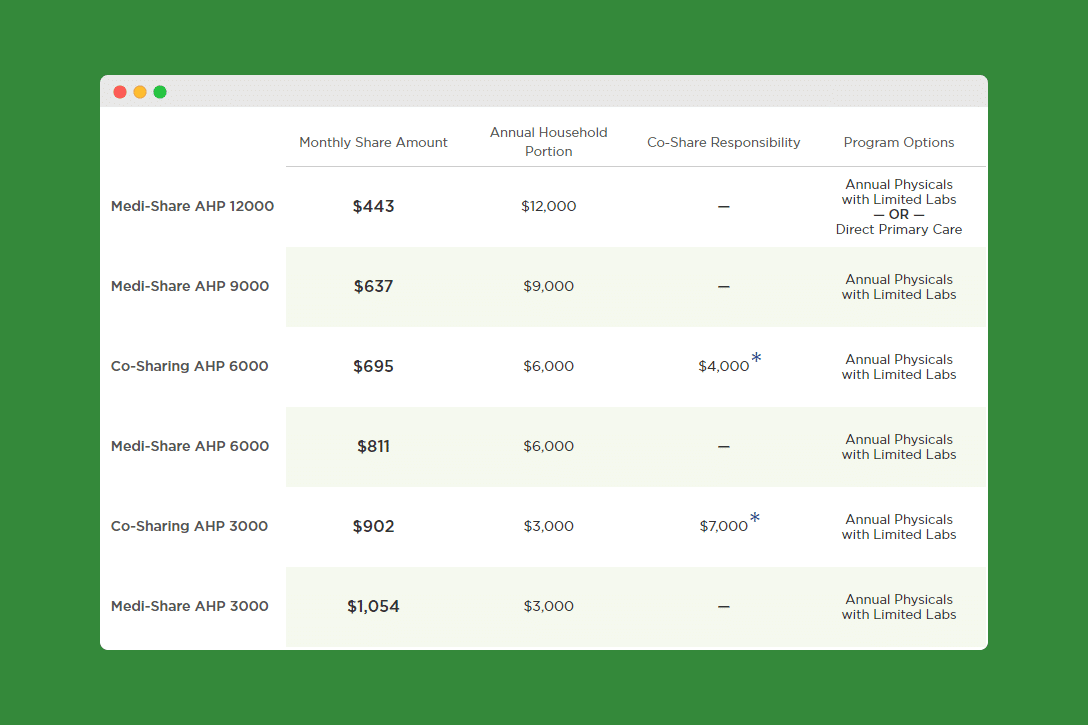

New Medi-Share AHP Levels

Medi-Share is offering new AHP levels. The updated AHP options are for new and existing members. However, current members must elect to change their AHP to a new level. There are now only four AHP program options.

- $3,000

- $6,000

- $9,000

- $12,000

You can review the potential pricing and program levels to compare your options using the Medi-Share calculator. Get started with Medi-Share here and begin calculating your pricing.

Medi-Share Fees

There are other fees associated with becoming a Medi-Share member to consider in your budget. Here are some of the additional costs.

One-Time Fees

- $50 application fee

- $120 new member fee (paid with your first share payment)

- $2 administrative (set up new accounts) fee

Monthly Fees

If it’s determined that you’re at a higher risk for disease, you could be required to become a Health Partner, which is an additional cost of $99 per month.

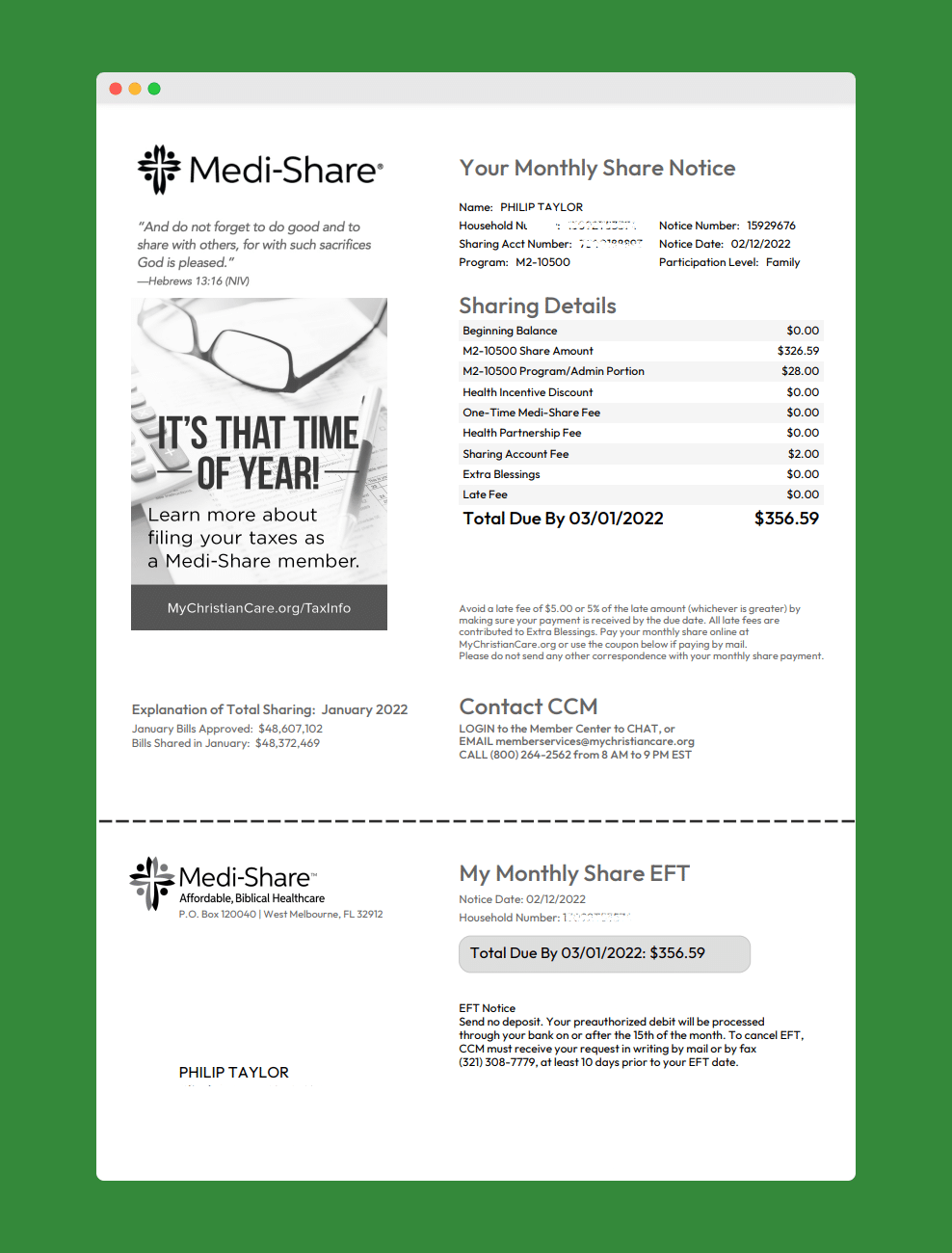

I also pay a program/admin portion fee of $28 each month. Here’s a snapshot of my current monthly share notice/bill.

Medi-Share Mobile App

Available on iOS and Android, the mobile app gives you access to your membership information anytime, anyplace.

It may not be the smoothest running app, but there are basic features that can come in handy.

With the Medi-Share app, you can:

- Search for providers

- Access your member cards

- Schedule telehealth appointments

- Visit and chat with telehealth doctors

- Connect and interact with community members

- Track medical bills

- Get customer support

Medi-Share vs. Traditional Health Insurance

Medi-Share operates closely to how traditional health insurance works but with some differences. Often healthcare sharing programs have similar features but just with different names to avoid confusion with traditional insurance.

There are some key features of traditional insurance plans that Medi-Share does not have and vice versa. Here’s how Medi-Share compares to traditional health insurance.

Medi-Share and Traditional Insurance Similarities

- PPO network – Both offer access to a network of providers to reduce care costs. Like traditional health plans, Medi-Share members pay more if they go out of the network for care.

- Deductibles – Just like traditional deductibles, Medi-Share AHP is what you will pay before you can share covered expenses.

- Monthly payments – With Medi-Share, you’ll pay a share amount, which is equivalent to a monthly premium for traditional health insurance.

- Visit fees – Copays – Medi-Share calls them provider fees – are paid when you visit the doctor.

- Telemedicine – Many traditional plans also offer virtual doctor visits at no cost, similar to telehealth with Medi-Share’s MDLive.

Medi-Share and Traditional Health Insurance Differences

- Enrollment – There is no enrollment period for Medi-Share. You can join their healthcare sharing program anytime.

- Biblical standards – Medi-Share members must live under Biblical standards, which is not a requirement under traditional health insurance.

- Preventative care – Traditional plans are required with Obamacare to cover ten essential health benefits (EHB) at no cost. Preventative and wellness services is one of the EHBs. Medi-Share has the $35 provider fee for preventive care appointments. Sharing is not available for immunizations and lab work that might typically fall under a wellness checkup.

- Pre-existing conditions – Medi-share covers some pre-existing medical conditions, but it may have limits on sharing eligibility. Medical conditions diagnosed before joining Medi-Share are eligible for sharing if you haven’t had symptoms or treatment in the last three years. If you require treatment for the pre-existing condition later, there may be limits to your sharable amount. Traditional health insurance does not allow you to be denied coverage or charged additional costs for preexisting conditions.

- Health Partner – Medi-Share charges an additional $99 per month if you are deemed to be at higher risk for health problems. Under Obamacare, your health and medical history cannot increase your monthly premium.

- Tax deduction – Under traditional health insurance, monthly premiums are tax-deductible. Medi-Share’s monthly sharing contributions are not deductible. However, that could change in if the Certain Medical Care Arrangements passes. But for now, remember, you can deduct medical expenses based on a percentage of your AGI.

- HSA – Since it is not insurance, you cannot qualify for an HSA with Medi-Share. The good news is, funds already in an HSA, can still be used for qualifying expenses.

Medi-Share vs. Short-Term Health Insurance

Short-term health insurance is a temporary solution to meet your health care needs.

It provides you with insurance coverage when you are between health insurance or when you need insurance, but are outside the enrollment period.

Medi-Share and Short-Term Insurance Similarities

- Temporary health insurance is similar to Medi-Share because neither falls under the standards for Obamacare.

- Neither Medi-Share nor temporary insurance has to meet the requirements of minimal essential coverage.

- They both also have higher deductibles or AHP.

- Enrollment in both Medi-Share and short-term health insurance is available all year.

Medi-Share and Short-Term Insurance Differences

- Short-term insurance typically only lasts 1 to 12 months, while Medi-Share does not end.

- Temporary health insurance usually only covers preventative, urgent, and emergency care and not maternity coverage or mental health. Medi-Share does cover pregnancy and offers free mental health counseling through telehealth.

- Term health insurance does not cover pre-existing conditions but Medi-Share does with some limitations.

Medi-Share vs. Concierge Plans

Concierge healthcare or concierge medicine is similar (but different) to DPC in that you pay a monthly fee for medical care.

But concierge plans can accept insurance payments and Medicare where DPC does not.

Direct Primary Care focuses on saving money while concierge medicine costs more but provides more personalized medical care and premium services like longer office visits and shorter wait times. Because concierge medicine accepts insurance, they will submit claims to Medi-Share.

Is Medi-Share Right for You?

There’s a lot on the line when it comes to your family’s medical needs.

Take plenty of time to evaluate all of the pros and cons of the program and don’t forget to consider your long-term plans.

- Are you having more children?

- Will you be getting married soon?

- Are you about to retire and qualify for Medicare?

All these things and more make a difference.

How to Join Medi-Share

It takes a while to go through the application process so leave yourself plenty of time.

Here are the major steps:

- Visit this page and complete the form or call 800.772.5623.

- Use the Share Calculator to pick the best AHP for you.

- Apply.

- Complete the medical forms and testimony of faith.

- Complete the power of attorney for the share account (set up with a credit union).

- Make your first share payment.

The Bottom Line

While Medi-Share isn’t insurance, it could be a great way to save on healthcare costs this year. If you qualify for subsidized health insurance, your monthly payments may already be affordable.

But if you’ve been paying high premiums for unsubsidized health insurance, Medi-Share could save you a ton of money.

Medi-Share is a non-profit, medical expense sharing program for Christians. Members share in each other's health expenses.

Are you a Medi-Share member? If so, please share your review in the comments. Not a member yet? What questions do you have?

![Buy the Best Life Insurance in 7 Easy Steps [The Ultimate Guide]](https://ptmoney.com/wp-content/uploads/2019/02/Buy-the-Best-Life-Insurance-in-7-Easy-Steps-The-Ultimate-Guide.png)

Medishare also does not cover any genetic testing or treatment for genetic illness. I am a dedicated Christ follower and have a hard time believing that Jesus would disqualify anyone due to a genetic illness. Therefore, I have a really hard time considering Medishare to be truly a Christian organization.

I currently have Medishare and have $11,000 in bills submitted, only $2,000 have gone towards my $12,000 AHP, large portion of each bill is written off or negotiated down, and waiting on a $13,000 hospital bill to be considered. Do most hospitals and doctors (out of network) just accept Medishare’s reduction? If the hospital or doctors don’t accept the reduction, then am I billed for the full amount since it seems I will never reach my AHP at this point with all their reductions? Worried because I am scheduled for surgery in a month and have no idea if it will be covered even if I reach my AHP.

Hi Patricia, my husband and I are considering joining metí-share. It would be a supplemental since I am 74 and he is covered by the VA completely. So this would just be for me. I am worried about you and your recovery. How are you doing? And have you been satisfied with Medi-share? Did they help you meet all the needs that you had plus I see that you had surgery as well. Nancy

I recently joined Medishare. I was trying to get an idea of cost for services with Medishare. I was met with rudeness as the customer service rep did not want to continue to answer my questions as I was seeking clarity. I am shocked that even if I provided the doctor and the EOS code, Medishare will not tell me what the discounted agreement is with the said doctor for the said code. It is like ordering a steak and having no idea what it will cost you until after you have eaten it and get the bill. Who does that? I find it very impossible that Medishare can not provide any information regarding this. It is like taking a flight, getting to your destination and then being told how much you owe.

We had medishare. My wife’s routine mammogram cost us over $800 and medishare paid nothing. Great deal right? The monthly premiums keep rising but the part they pay is 0 wasted my hard earned money. I back to BCBS. They take care of the family for less than we paid for my wife only.

We are considering Medishare next summer (2021).

Question: Our son is due for vaccinations at the next annual visit in August. Since it appears they are not covered by sharing, would the cost count toward the family AHP? His school requires an updated vaccination record for enrollment in fall.

I was a member for 4 years and had a great experience with Medi-Share. Unfortunately, the 2 largest providers in the Columbus Ohio area (Ohio Health and Ohio State) began refusing to see patients that had Medi-Share or other share plans. It seems big health and big insurance are teaming up against private plans. I had to go back to a group plan at 4x the cost. Really stinks.

I have been a member for 4 years. Medi Share directed me to an in network facility for colonoscopy implying it would be covered due to prior medical condition. After the procedure they would not help with the cost leaving me with a $6000 bill. I could have gone out of network and had it done for $1500. They repeatedly placed the blame on the facility for using incorrect codes. Medi Share has a Christian response for this: Coverage is determined at the time of processing bills. The bottom line is this company is deceptive, use caution and go out of network.

Ive been a member for 3 years. A family of 4 and good standing member. First 2 year were ok, didn’t have a lot of needs and this is what this plan excels at. 3rd year my doctors of 18 yrs for my kids dropped us, as well as my doc for 6 yrs. Furthermore, I tried to take my son to urgent care listed on their website and when I arrived they said nope, we don’t take it. BTW, my docs are still listed on their website also and they dont take it.

I called medishare, took an hour to get through. They have me a lame excuse about how their website is run by a third party and information is owned by them. I need to call and make sure doctor take it? I ask why? I mean in an emergency you need good information to make decisions. Furthermore, they gave us push back on being covered by preexisting after three years since we were coming up on 3 yr anniversary. That was it. We are in the process of cancelling. This company can not be trusteed in my opinion.

Long story short, save yourself the headache. I really wanted it to work especially helping other Christians but its really not a well run organization. And several of their practices are ethically questionable. Do yourself a favor and look else where for healthcare. My 2 cents after being on the plan for three years.

Does Medishare not pay for diagnostic testing ordered by a primary doctor – ultrasound, xray, blood tests?

We’re self-employed and ACA ruined our self-paid insurance. I’ve been thinking of medishare or something like it for years, but their website seemed really confusing to me, and the cons make me hesitate – insurance was insanely expensive, and they would try to wiggle out of paying claims, but it was straightforward about what services it covered, which doctors would accept it, etc.

Between the website being confusing, the provider has to want to take it ( I have to try to convince them), and if they don’t pay for diagnostic tests, which are among the most costly expenses necessitating things like insurance, I’m not sure what the benefit is.

Do not use Medishare.

They will not process bills in a timely way.

They will not follow up with you for information if any information is missing to process a bill.

They will expect you as the member to do their job for them throughout processing, claims, and follow up continuously to make sure they are still doing their job.

Medishare gives only a ’90 day’ grace period before dropping your claim (read your fine print!), so make sure you are checking your online portal religiously for months on end for any updates for work you need to do, or you may not have your bill shared. No emails, phone calls, or paper mailers informing of more needed information…subpar service to say the least!

Stay away!

After four years as loyal members, we are switching to a different company with honesty and better communication!

Hello Lydia,

Just curious if you switched to a different company and if so what company and what are your thoughts so far? My wife and I are considering MediShare but after reading some of the reviews we are having second thoughts

Hi..I have a question…When I look at Medishare pricing at their website, they seem to only offer 3000,6000,9000 and 12000 plans. Did they ‘force’ you into one of these plans on your renewal and if not, what was your rate increase this last year ? Thank you

Eat right, get to the gym, do heavy squats, deadlifts and kettlebell swings. Stay healthy at all costs

Love it!

So, I was totally on board until I read on a different website that the insurance does not cover preventative care. Wow. Crushing. PLEASE tell me this isn’t true. This is seriously disappointing considering how far we have come in medicine to discover major illness before it becomes a true problem.

According to Medi-Share FAQs… “The primary purpose of Medi-Share is to help share members’ burdens. Burdens are those unexpected medical bills you are unable to plan for (ie. broken bones, cancer, etc). Low monthly share amounts enable you to budget for your family’s routine care, which can be planned. There are exceptions for well-baby care…”

Just take your monthly premium savings and apply it to your own preventative care services, which you can easily negotiate on your own. No one is preventing you from taking care of yourself.

My husband is retiring in 4 months at age 67, I am 62 and a homemaker. Does Medi-share accept retirees and does it work with Medicare? Thank you.

Hi Philip,

I enjoyed your article and thank you for sharing. I am assuming your 10K “deductable” AHP, is for the entire family and not per person?

That’s right. The entire “household”. Good question.

How long can you cover your adult kids in college?

Is diabetes and heart murmur unqualifying pre-exsiting conditions?

I have been listening to this infomercial on the radio forever. I cringe each time it comes on because the actors/people can’t finishing a sentence without …all… of the… hesitations. What the heck is the matter with all of them? Even my coworkers notice it. I might actually take the time to read all of this if they could speak with a fluid ……

Haha! Don’t like the ads, eh? I can see that. I find the guy comforting…like a good buddy neighbor who’s shooting me straight. There’s always Liberty HeathShare: https://ptmoney.com/liberty-healthshare-review/

What happens if you get in an accident or get cancer and need to spend a lot of time in hospital care…what is the life time coverage or deductible for such catastrophic cases?

They have no lifetime limits. See their guidelines: https://mychristiancare.org/globalassets/media/medi-share/medi-share-guidelines.pdf I should add this to the review.

hi all

thanks for the educational, respectfull and friendly discusion.

does medishare deductible counts canada drug expenses? ( planetdrug) we have changet to planetdrug for our medications, as it is canadian meds, at less the

an 1/2 the us price, which my bc/bs anthem never covered any way due to high deductible

any updates on getting an HSA with medishare? I am thinking of going the medishare route after taking ACA in part of 2016 and dropping it in 2017. The cheapest ACA went for me from $272 in 2016 to $402 in 2017 and will be $566 in 2018 so that’s out of the question. But the penalty for me would be about $1,000 and I am learning there are medishare plans that would cost only a little more than that.

It’s been included in many of the proposed tax laws under the new Admin, but obviously, nothing has passed.

very helpful article!

This was a very helpful article. Thank you! I have a question for you: You mentioned that you cannot pay for your monthly premium w/funds you already might have in an HSA, but how can I find what would be covered? Where can I find what possible medical expenses *would* qualify? Is there any way to use my HSA funds if I sign up for this? Blessings!

Teresa,

I’m a Medi-Share member, too. Here’s a link to find what’s covered and what’s not:

https://ptmoney.com/medisharereferral/

While you can’t pay your monthly share cost with your HSA, you can use your HSA for any medical expense not shared with other Medi-Share members. Examples: Any medical expense not eligible for sharing, any eligible expense applied to your Annual Household Portion (AHP is like the deductible for insurance).

We’ve had a good experience for two years with Medi-Share and have saved a lot of money. It is, of course, not technically insurance, but instead, a modeling of the early church’s example of sharing in one another’s needs.

Feel free to email me if you have any other questions for a current Medi-Share member.

John

Hi, Teresa. Yes, you can use your HSA funds (previously contributed) to pay for qualifying medical expenses incurred while on Medi-Share, just not the monthly share (aka premium). I did it for 3 years until my HSA ran dry.

Are you saying that you can’t open an HSA and use Medi-share to pay your out of pocket expenses, but if you already had and HSA that was coupled with a previous high-deductible insurance, you can use that account until it has a zero balance, but can’t add anymore to it?

That’s correct, Alice. We’ve spent the last 3 years spending down our HSA from before we had Medi-Share. Now it’s empty. 🙁

I was told that medishare is not regulated so they don’t have to pay claims. Like if I was in a accident an hospitalized and my bill was 70,000 they are not under any obligation to pay. Is this true??? Really interested in medishare but……

Yes, true. But they are not in the business of messing people over. Not sure they’d be in business long if they treated people that way.

We can see on the Medi-Share website the costs that are being shared for all the families. There are routinely (weekly) costs being covered in the range of $50,000-$100,000. We were facing $1100 premium on BCBS, switched to MS – same ‘deductible’ for $390 (including $80) for wellness ‘penalty’ due to my weight.

I have a question about Medi Share and was wondering if you would know. I tried checking on the website and got a little confused. My wife takes medication for her anxiety. Would medical costs such as this be covered under the sharing?

Hi, Ben. Great question. I don’t see why not. If your current doctor prescribes this then there’s no reason that I can think of that it wouldn’t be covered and shared. Of course, the best way to know for sure is to give Medi-Share a quick call. Their live customer service is excellent.

Awesome! Thanks for the quick reply. I was hesitant on calling because you never know what you will get with customer relations. Glad to hear positive things, I will give them a call!

Ben,

Medi-share will only potentially share the first 6 months of any medication and maybe not at all for the pre-existing drug your wife is taking. GoodRx.com is great option to discover potential discounts in your area – we’ve had great success using it (GoodRx is free!). With the significant savings in your monthly “premium” cost, it may still be cheaper overall to pay for the medication on your own. We’re with Medi-share and have found that to be the case for some on-going medications.

John

I travel a lot for work. Many times outside the US. Are there any provisions for this in Medishare?

Jon, I would think any medical needs overseas would be in the emergency variety and Medishare would treat it as such… i.e. those needs are shared. If you are planning on living overseas and getting routine care I would probably check with them first.

PT,

I saw you were featured in the Medi-Share email recently! Thanks for spreading the word about a great program. We’re now finishing up our second year with Medi-Share and plan to be members in the future.

John

Oh yes that was nice to be featured. Been a big win for our fam too.

How long did you have to wait for approval once you submitted your medi-share application?

Kelly, for me it was just a few days. That was in 2014 over the Summer. But this is the extremely busy time for them and they are more popular than ever so I’m sure it’s possible it could take longer. I remember someone emailing me and outlining all the steps I needed to take to complete the full on-boarding process. Has anyone reached out at all?

Thank you for your quick reply! I haven’t submitted an application yet. I was gathering information on medi share last night as I was waiting on obamacare’s website to load last night. 🙂 I appreciate your review and it’s convinced me that’s the direction that our family is headed. Thank you.

Rosie,

Congratulations on applying for Medishare. I hope the underwriting goes well and your family is able to join us!

Regarding the HSA contribution, per the IRS regulations, you have until April 15, 2017, to make the contribution for the tax year 2016. If you have the cash available, I’d make the contribution now, if for no other reason than to shelter more of the income.

I haven’t heard anything about Medishare coverage making one eligible to contribute new money to an HSA. There was a bill introduced (in 2011, I believe) to broaden the rules for HSA contributions to include medical sharing ministries, but it died in committee. I’ve followed up with my Congressional representatives, but thus far have only received form letter responses! I’d encourage others to speak to their representatives, too. In the meantime, you can continue to invest the money you have in the HSA, but not add to it after 2016.

John

Thank you so much! I am going to take care of that 2016 contribution this afternoon!! I appreciate your quick response!!

Happy to help! Hope everything works out with your Medi-share application. It’s such a great program!

John

I am considering Medi-Share and my app has been submitted. I had already decided to drop Blue Cross Blue Shield after this month and risk no insurance and pay the penalty. My question is I have an HSA and the money does not have to be contributed until April 14th of the following year for the prior year. Should I deposit the money for the HSA this year to receive my tax exemption since I will no longer have insurance after December 31 2016. And if I am accepted into Medi-Share, is there a possibility that HSAs will soon be accepted as a tax deduction. I pray that I will be able to be a part of the Medi-Share family. I have always had insurance but my premium will be 1000.00 monthly with a 5500.00 deductible. A 35% increase…

Other choices to get a trade group that offers a less expensive substitute for a person medical

health insurance policy. The outcomes of this research obviously have dietary implication for the people fighting cancer.

Generally, the higher a deductible you select, the low reasonably limited

you’ll pay each month.

Hi everyone my husband and i have been on Medishare for almoat a year now an we will be staying with them going into 2017. I too was a little nervous making the switch from the ACA to medishare ..so i want to tell people it was so worth making the change. My husband ans and I pay 264 a month with a 5000 share. My husband had some test done that went towards our 5000 share but even with us paying for them we still saved so much money. I even used the video Dr for a sinus infection and that is a free service the Dr called in a antibiotic and that is all i had to pay for which cost about 10 dollars. We also get the healthy lifestyle discount which will give you a lower monthly premium. So we have had a positive experience so far and we are very pleased.

I am strongly considering joining Medishare, but have one question that I haven’t been able to get an answer to: In our Grand Rapids, MI region, we have three large hospital networks available. But none of them belong to the PHCS network. If we were to have a big emergency we would likely have to go to one of these local hospitals. The Medishare rep said that they would be able to accommodate bill payments if something like this were to happen to us (it sounded like worst-case-scenario I might get billed, and then have to submit the bills to Medishare for payment). But I also talked to the billing office of the largest of the three hospital groups, and they said that since Medishare is not “insurance” they would not be able to work with them. They were also not familiar with PHCS or the Multiplan billing system. So I am concerned as to whether my family would be properly covered in a catastrophic claim. Does anyone have experience with this type of situation? Thanks for all your information!

John P,

It’s my understanding that using a provider not on the PHCS list means that you would be responsible for any amounts above the allowable charge that Medishare would provide if you used a PHCS provider. Using a PHCS provider mean the doctor MUST accept the agreed to charge. A non-PHCS provider may, or may not, accept that fee amount and you’d need to negotiate with doctor/hospital if the did not. I haven’t had this exact situation, so hopefully someone else can share an actual experience.

Medishare guidelines do say you would have an additional responsibility payment of the lesser of 20% or $500 for using a non-PHCS hospital, but it can be waived if there are no PHCS hospitals within 25 miles (which sounds like it may be the case for you) (per Section V of the guidelines).

John

Thank you Philip! I’ve been hesitant to do anything that will negatively impact my family but as I ponder this, I realize I would give the same advice you gave me to someone else. I will contact medishares to see if I would still be eligible depending on the outcome.

Thanks so much for taking the time to respond to me!

Kim

Thank you for all the great info! We are a healthy Christian family of 5 (ages 44, 44, 13, 9 and 4) and the affordable care act is crushing us. For 2017 we will have to pay $1531/mo for the highest deductible plan. We could go slightly less if we omit children’s hospital but that seems foolish in case there was ever an emergency or a major change in one of our children’s health. My tubes are tied so maternity coverage is not needed but we are having trouble deciding what to do. My husband is a little weary of potential (unknown) risks with Christian health share accounts and is toying with reducing our tithe and sticking with an ACA. We’ve always tithed 10% and I’m struggling with that idea. My family has been complaining about my hearing and I’m scheduled for a test on 12/14. I’m afraid to pursue this tho in case of creating a pre-existing condition. If you have any recommendations I’d appreciate hearing them.

Definitely put your health first and get your hearing checked regardless of your insurance situation. Medishare is really good about talking through these potential issues and questions. Request the packet from them and then call them up for advice is what I’d do. Good luck, Kim.

Our church does not provide group health insurance to our 2 FT pastors. We can no longer pay their personal insurance premiums so we’ve increased their pay by $10,000 to help cover the premiums. This also increases the payroll taxes, etc. Since medishare isn’t insurance, do you know if the church could pay the premiums?

Gretchen, I see no reason why the church couldn’t either pay the monthly share or reimburse the pastor for it. And since it’s a benefit, the church should be able to deduct it as an ordinary and necessary expense.

Hello,

I am considering the medishare. I am also self employed with a HSA account that I have built up over the last few years. Can I still contribute to a HSA even though I do not have a ACA medical plan? I am kind of confused on this. I know the medishare does not qualify me to get a HSA but since I already have a HSA can I keep contributing? Even If I can not, I am pretty sure that I am coming out ahead with the medishare with the low premiums.

Joe,

You can only contribute new money to an HSA while you have an HSA compliant high deductible insurance plan (your contributions are pro-rated if you have eligible insurance coverage for part of a tax year). Medishare does not qualify since it is not “insurance”. You can, of course, continue to manage the funds you already have in the HSA, you just can’t add to it.

For us, even losing the deduction for the insurance premiums and HSA contributions, we came out far ahead with Medishare.

John

Dear Philip, you mention that you are paying $277.00 a month with a $10,000 Annual Household Portion for Medi-Share. You say that your Medi-Share contributions are not tax-deductible – but can your Medi-Share contributions be listed as a charitable deduction on one’s tax returns? If not, is there any way to deduct one’s Medi-Share contributions on a tax return? Thanks in advance for letting me know, Karen

Hey, Karen. While you’re waiting for PT to respond, I can shed a little light on your questions (I use Medishare and am a CPA). Medishare payments are not deductible. There is no way to make them so. As it’s not “insurance”, even self employed taxpayers (like myself), cannot deduct the payments. Medishare does have an “extra blessings” program to help pay non-covered medical bills of others that may be deductible depending on how they are processed. But these are extra, optional payments….not what you are required to pay to participate (like PT’s $277/mo., for example).

I wish we could deduct the payments, but I’ll have to “settle” for only paying about 25% of what I was with traditional coverage!

John

Great answer, John. Agree. Thanks for jumping in!

Hello! I appreciate your insight as a CPA. We are self-employed & our United Health plan is cx our coverage next July. It’s a high deductible HSA. Thankfully they’ve given us plenty of notice. I’ve been researching other insurances & am intrigued by the many health share options like MediShare. Do you find that it is better for you financially to go with MediShare than to take the insurance premium deductions allowable with traditional insurance? We are very healthy & rarely need to see a doctor aside from annual check ups. Thanks!

Stephanie,

For our family, it was definitely financially worth switching to Medishare, even though we lost the ability to contribute to an HSA and deduct the contributions and insurance premiums. Our monthly coverage cost dropped by about 75%, although a small amount of this savings was lost in higher out of pocket cost for wellness checkups (covered under ACA plans). In fact, the savings are enough to virtually eliminate our Annual Household Portion we would have to pay if we had a large claim (which, fortunately, we haven’t had this year). I hate to lose the tax savings, but marginal tax rates aren’t nearly as high as the monthly payment reductions!

John

Thanks for the info, John! We met our deductible for 2016 (which is a rarity), so I’m squeezing in ALL tests & visits before the end of the year. Prior to this year, the last time we met our deductible was in 2000 when we had our 2nd daughter. Medishare definitely sounds like a better option for us given our overall healthy track record. Being self-employed has its perks, but not with insurance. Again, thanks for your CPA insight. It is indeed very helpful. Merry Christmas!

You’re welcome,Stephanie! Glad you found it helpful.

Medishare doesn’t work for every family and situation, of course, but for many it’s a great option to consider.

Merry Christmas to you as well!

John

Thanks for sharing. This is the first time I heard about Medi-Share and I think this is a great idea. I am thinking of joining. However I have some questions.

1. The FAQ on ‘https://mychristiancare.org/medi-share/what-is-medishare/faqs/’ says “We do not collect premiums, make promise of payment, or guarantee that your medical bills will be paid. Sharing of medical bills is completely voluntary.” This means unlike a traditional insurance there is no guaranteed coverage. One questions that I always ask while getting an insurance policy is “what is total cost in the worst case scenario?” So with Medi-Share what is the “worst case scenario cost”?

2. My employer offers an MEC (minimum essential coverage – HSA eligible) plan. If I get Medi-Share and also enroll into my employer offered plan, will I be eligible to make contributions to HSA?

A small correction to the first questions – “With Medi-Share what is the “worst case scenario cost” for person who abides by all life style and faith based restrictions?

A_Fellow_Believer_NG: While I am sure PT will respond to this as well, here are my thoughts in regards to your questions:

1. The reason Medishare can’t use those terms is that it would imply that the coverage is insurance, which it obviously is not. Regarding the “worst case scenario cost”, I suppose it would be that any cost above your Annual Household Portion (think “deductible”) that should have been shared with other members, won’t be shared and you would be on the hook. If you used a network provider, the fees should still be written down to the allowable charge (as this wouldn’t require anything out of Medishare). If you hadn’t hit your AHP, you are no worse off as you would have to pay the written down charge anyway. Is there more potential risk than traditional insurance? Yes! But they have a long history of 100% payment of covered expenses. You will have to get comfortable with this potential “worst case”, as well all have to do.

2. Not sure why you’d want both MEC and Medishare, but my understanding is that you could contribute to the HSA because of the MEC coverage (if, like you mentioned, it is an HSA eligible plan). Also paying for Medishare shouldn’t disqualify you from contributing to an HSA (if you have the MEC coverage, too). But again, why are you considering having both??

John

1. What John said. Also, see my response to Denise above.

2. While that might allow you to contribute to an HSA it might also affect your payouts. If Medishare knows you have coverage somewhere else it might affect your ability to use the share. I would call them about this.

We have been with Medishare for almost one year. It’s been a great success so far! It can be initially frustrating paying for some services formerly covered by traditional insurance, but then I remind myself of the $10k savings per year in insurance premiums!

The MDLive tele-health feature is great, too, and it’s free for Medishare subscribers!

A worthy option for consideration. Thanks for the review – and updates, PT.

John

Thanks for the tip, John. I haven’t checked out the MD Live thing yet. Will come in handy.

We are ready to sign up for Medishare but I am still reading reviews and trying to get as much information as I can. Currently we have ACA and our deductible and premiums have skyrocketed. Our plan is to finish out this year with our current insurance and to start with Medishare at the 1st of the year. It is either this or we go without insurance all together and just pay the penalty. At least with this we are covered for catastrophic. My question is this. I understand that there is no “guarantee” that your bill will be covered. What does this mean? Suppose we pay into the program for years and then something happens that we have to use the coverage. Can they just randomly decide that they don’t want to cover? This makes me a little nervous.

Well, they are a not-for-profit and run by Christians. So I don’t think they’re in the business of randomly taking advantage of people or failing. They have a proven track record with their customer base and major complaints are either non-existent or few and far between. I’m not sure if the no guarantee disclaimer is there because of their “lifestyle” requirements or because of some type of underlying regulation they need to follow. I’m planning an interview with them soon and will ask this question.

I think they can’t use the word guaranty as that would imply it’s insurance. They have been in existence for a long time and have always paid the “covered” items. Plus they have grown significantly since the ACA became law and that can only serve to make them stronger (as the pool of people paying in is larger).

I, too, was a bit worried about not have insurance guarantees when we first began our Medishare coverage, but after much prayer and research we began our coverage 1/1/2016. No regrets!

John

I’m looking into applying for Samaritan Ministries (a similar health sharing organization) and after reading this will look into MediShare. If it’s not too nosy can you share why you chose one over the other? Thanks!

I didn’t look into Samaritan that much. Some friends were already using Medishare and so their testimonial did a lot for me.

We chose Medishare as it operated in a manner more similar to traditional insurance.

With Medishare, we go to a doctor (on their provider list!), give them our Medishare card, pay a “co-pay”. They send their bill to Medishare for processing. The charge is written down to the allowable charge. If you’ve reached your “annual household portion” (think: deductible), they will pay the amount due. If not, your doctor will bill you the balance due (after writing it down to the allowable charge). Your monthly share amount goes straight to Medishare and they will pay the doctor.

With Samaritan (as I understand it), you go to a doctor of your choice and negotiate a cash price. You will pay the bill when services are rendered. If the bill is above your “deductible” amount (ex. $300), you can submit it to Samaritan and they will pass it along to specific members. Those members will then send you checks for the amount over your “deductible.” In other words, members pay each others bills directly, instead of going through a central clearinghouse (like Medishare).

The principle is the same for both, but the execution is very different.

John

I’m more attracted to the Medishare way of doing things since it is more like insurance, but whenever I plug my zip code into their provider search there are none in my area. And since Samaritan’s HQ is fairly close to us hopefully the local doctors/hospitals are used to dealing with it. Thank you for both your answers.

We are joining a ministry for 2017 and have it narrowed down to 2, with Medi-Share as one of them. We’re probably leaning towards medi-share, because we like the fact that preferred providers submit claims for sharing. Our family doctor is in the network. Our current plan is from the ACA in 2016, but Aetna is leaving the exchange. So I’m shopping the market, but the quotes I’m finding for health insurance for my family of 4 are starting at $1300/month for $12000 deductible, and what I’m finding is many of these plans are NOT compatible with health savings accounts anymore. Not sure why that is being taken away!

Sharing ministries are a completely different model and it will take a little getting used to, but we are being led in this direction, because we can’t afford the traditional health insurance model anymore.

Have a friend that has Obama Care. Not happy with it. She has two questions:

1. Do most of the physicians accept this insurance?

2. If she would be diagnosed with cancer in the first six months would this insurance cover her?

Thanks!

Hi Teresa! 1. All my physicians have, but I don’t think all do, no. You can use the tool on the Medishare site to check your physicians and the ones in your area. 2. I don’t see why not. But I would grab the info packet and then call Medishare to talk about different scenarios.

Could you provide detail as to why you chose the 10K plan as opposed to a lower one? Just for a lower monthly payment? Considering making the switch too.

Hi Caroline. Yes, I chose 10k because it significantly lowered by premium/share and because we have that amount and more in an emergency fund to cover it. Our actual out of pocket medical expenses each year are around $1500-2000 (mostly doctors visits and well checks), so we’d have to have a <1500 deductible to actually use it. Medishare offers the $1250 deductible, but it would take our monthly share to >$500. That’s $250 more than we pay now. So we’d be paying $1750 more in monthly share/premium total each year to save $250-750 in deductible savings. Doesn’t make sense. Obviously if you’ll expect more out of pocket expenses and/or if you don’t have a big emergency cushion (aka self-insured) then my choice might not be right for you. Hope that makes sense. Good luck!

Philip,

I SO appreciate it. We have run the numbers in a variety of ways and I wanted to ensure our thinking was along the same lines. Thank you. Also, do you happen to know if a doctor/hospital is not approved, do we have the option to use them and them submit the bill after we negotiate rates?

Thanks for sharing your experience, Phil. My wife and I are planning to change our insurance. We looked at this before, but didn’t do it. We will give it more consideration this time around.

How does it work for significant medical expenses like a long hospital stay?

Hi Eric, I can’t speak from personal experience, sorry.

My husband and I also signed up for Medi-Share when Oabamacare came along. We love it because of the Christian community and support feel and also because there is no annual or lifetime limit and they gave us a $23/mo discount because we met their health incentive requirements.

Your Medi-Share premium could fluctuate some but you will save big over the years. The pool is administered well with little if any admin costs. I have clients that have used this Christian pool over the years and had big savings for the family.

Makes you think that if a simple Christian pool can handle a medical program with little admin., then why cant we do better at the Federal/State program level.

Big question; what will ACA be like in the coming years as a cost to taxpayers?

While I think it’s great that these options exist, I take issue that I don’t have access to a similar resource just because I don’t subscribe to a faith. Luckily, I qualify for Medicare under the ACA.

I only wish we could all know God the way He deserves to be known. And while I am always getting to know him better, I hope with all my heart that you will give him the research that most give to their health care. From all I know now, I can honestly say that no one has done more for us, while allowing his identity to be stolen, misused, slandered, and yet SO gracefully continues to offer himself as our payment for his heaven!! What a precious gift!!

An old neighbor just had their 4th child and the first through this program and they were very pleased with it. It’s intriguing, though I’d be concerned about the financial stability of the underlying organization. The same risks apply for standard health insurance, but it seems like they’re more quantifiable.

I respect your posting, PT, about this “outside the box” method of being able to receive medical care. Through the Affordable Care Act, I have to say that I am finally, FINALLY able to get health care for my pre-existing condition (chronic pain). This after either being turned down on a continual basis by insurance companies or paying unreasonable premium rates and deductibles with riders attached.

I guess I am grateful for the little things. You may have had exceptional healthcare prior to the President’s implementation of his signature ACA, but I didn’t. Respectfully speaking, it’s a reasonable trade-off, I’d have to say.

My druthers? Universal healthcare and medical marijuana. And before I am accused of being a socialist/communist, I’m a centrist, with leanings to the right for the military might and to the left for the social nets. I believe in balance so everyone can benefit, and that includes healthcare. Just sayin’. Thanks for an informative posting. I always enjoy reading them.

How are your rates now 2 years in? Mine are more than double form the first year, with annual maximums going form an initial $2500 to almost $7000.

RetiredBy40 Thanks, I can’t take much credit. Bob from Christian PF was my guinea pig. He’s been on it for almost 5 years now and they now have a little one. If it was a good fit for him, it’s likely a good fit for me.

Plantingourpennies I think you’ll definitely see it happen.

I think it’s great that this exists as an option for people, I only hope that by the time we’re out of traditional employment there will be similar options without the faith-based requirements. We don’t mind the lifestyle restrictions as we probably comply with them all in our normal lifestyle anyhow, but as agnostics we’d be excluded.

Totally makes sense! We are lucky enough to have tricare, but if we didn’t, espeically with this whole ACA craziness, we would definitely be considering doing something like Medi-share or one of the other Christian cost-sharing options. Way to go thinking out of the box!