Best Automatic Savings (& Investing) Apps to Round Up Savings

Saving money has a lot in common with flossing: you know it’s important, professionals wag their fingers at you when they find out you’ve been neglecting it, and it seems like a major pain to get in the habit of doing.

Luckily for reluctant savers, technology has come to the rescue in the form of automatic savings apps. (Unfortunately, automated flossing technology is still years away.)

Even the most budget-averse user can automatically begin growing their wealth using one of these apps to round up savings.

Each of the following savings apps has a different approach to automating your finances and helping you achieve your savings goals. Some will round up your savings (aka “keep the change”), some use sophisticated algorithms to understand your ability to save, and some simply let you have full control–set it and forget it.

While many will give you the push you need to beef up your savings, some savings apps offer you the opportunity to invest your savings as well.

We’ve tried to make a note of which apps let you invest, save, or both. We’ve also made a note of which platform the apps are available on: iPhone and/or Android.

Read on to see which one will work best for your wealth-building needs.

Table of Contents

Best Automatic Savings Apps

These are the best automatic savings apps around today to help you get started saving money for an emergency fund, travel expenses, house down-payment, or any of your other financial needs.

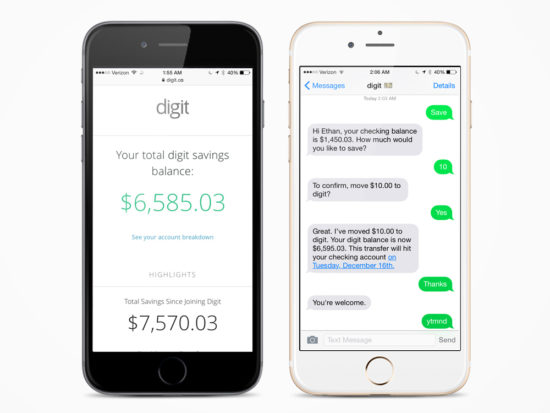

Digit

If you want to save money without ever having to think about it, Digit is for you.

This program syncs with your bank accounts and analyzes your cash flow. Every two to three days, it will determine an amount of money (between $5 and $50) that is safe to transfer into an FDIC-insured Digit deposit account.

This program syncs with your bank accounts and analyzes your cash flow. Every two to three days, it will determine an amount of money (between $5 and $50) that is safe to transfer into an FDIC-insured Digit deposit account.

Digit is so confident in its safe-to-withdraw algorithms that it offers to reimburse the fees for up to two instances of overdraft if any transfers leaves you overdrawn. You can request money from your Digit account anytime and you will generally receive it the next business day.

Digit communicates with you via text message, and you must sign up online, as it is technically not an app. Digit started as a text tool only but now has iPhone and Android apps.

For those simply texting, you will receive a text message once per day with your current bank balance. You also have the option to receive more detailed text check-ins, which allow you to see recent debits. This can give you a no-effort daily snapshot of your finances

Digit recently started paying customers a 1% annual bonus (paid out every three months) on the balance of the account. Nice!

The big downside to Digit is the monthly fee of $5. $6,040 is what you’ll need to keep in the account on average to earn enough bonus to negate the monthly fee.

Digit App Summary

- Pros: Saving is not only automatic but also painless. Your money is easily accessible if you need it and you earn 1% bonus on your savings.

- Cons: The monthly fee makes it tough to really grow wealth with Digit.

- Fees: Free for 30 days, then $5 per month

- Platform: iPhone and Android

- Best for: Beginner savers or those who hate dealing with money.

- Check out PT’s review of Digit.

Empower

Empower goes above and beyond, automating your savings. With features like budgeting, financial coaches, and cash advances, they make it simple to make smarter financial decisions.

Automated saving is a major feature of Empower. Get started by setting up an account, link your checking account, and then let the app know your savings goal.

Automated saving is a major feature of Empower. Get started by setting up an account, link your checking account, and then let the app know your savings goal.

After that, they analyze your checking account looking at your income and expenses to determine when and how much to save. Empower automatically saves your money, so you don’t have to.

Budget tracking with the app is made easy by providing budget categories and spending limits to help create a plan for your money.

The app reviews your spending and gives recommendations to reduce or cut expenses. Empower monitors your account and alerts you of late payments or bill increases.

A big upside to Empower is personal financial coaches. As a subscriber, you can talk to a financial coach and get personalized advice for your situation. Financial guidance is useful to have but can be particularly helpful if you’re facing money challenges.

Empower also provides cash advances for their app subscribers for life’s unexpected expenses. You can receive a $250 cash advance that you can pay back later. If you’re eligible and have Empower’s checking account, you’ll get the advance instantly.

External checking accounts won’t receive the money until the next business day. Eligibility is determined by your account history and your average monthly direct deposit. You pay back the advance when you receive your next direct deposit.

Empower App Summary

- Pros: Automated savings combined with financial coaching gives you personalized advice as well as smart recommendations to reduce bills and the option of cash advances.

- Cons: The $8 monthly fee and customer support is limited to email or chat. Also only available on mobile, there’s no web version.

- Fees: Free for 14 days, then $8 per month for all its features.

- Platform: iPhone and Android

- Best for: Beginner savers who want personalized advice and to be more mindful of their money.

Learn more and get started with Empower.

Eligibility requirements apply. Minimum direct deposits to an Empower checking account, among other conditions, are necessary to qualify for instant delivery and advances greater than $50.

Banking services provided by nbkc bank, Member FDIC. 0.01% Annual Percentage Yield (APY) may change at any time. APY as of Oct. 1, 2021. Empower charges an auto-recurring monthly subscription fee of $8 for access to the full suite of money management features offered on the platform after your first 14 days

Marcus by Goldman Sachs

In addition to its basic banking products, Marchs also allows you to set up automatic savings through their ClaritySavings Account.

You simply select the amount and frequency of your preferred withdrawal, as well as the goal that you are saving for, and activate the automatic savings.

Since everything is done within the app, creating and funding your savings account—not to mention pausing recurring withdrawals and closing the savings account—can all be accomplished with a couple of finger taps.

The money in your Marcus account is FDIC insured up to $250,000, and the program currently offers interest on the money in this savings account.

It’s also important to note that the app will provide you with a daily summary of your spending, which includes automatic categorization of your purchases. A simple and easy-to-read daily breakdown of your spending habits will help you to improve those habits and take better care of your finances.

Marcus’ mission is to be a service that will both watch your back when it comes to your money choices, and help you take control of your financial life.

After you download the app onto your Android, your iPhone, or other Apple device, you then connect your accounts to Marcus, and the program analyzes your spending data before making suggestions to you on how you can optimize and save your money.

There is also an algorithm on the app that will help you to find lower interest rate credit cards and/or personal loans. You can also get your credit score for free through the app, which works with Experian and uses the VantageScore model.

Finally, the program identifies wasteful recurring charges and will cancel those services for you.

Marcus will not make a recommendation that does not objectively improve your financial well-being, so you can feel secure that your finances will improve by acting on the app’s recommendations.

Marcus Summary

- Pros: Marcus takes care of everything within the app, which makes it easy to act on their recommendations. The app offers a fairly global look at your money, helping you lower your bills, cancel unnecessary recurring expenses, save more money, and understand your money habits better.

- Cons: Marcus shelved their bill negotiation service.

- Fees: Very limited fees.

- Platform: iPhone and Android

- Best For: Newbie budgeters or anyone who wants their money management to be easy and all in one place.

Related: Best Passive Income Apps

SaverLife

If you know you need to save and have no idea how to build the habit, SaverLife may be able to help.

Their focus is on helping people create strong saving habits to help them build their “rainy day fund” or whatever they are saving for.

The program is aimed at helping lower income families create a larger financial cushion in the event of an emergency, since nearly half of Americans do not have enough money set aside to pay for a $400 emergency.

SaverLife is run by EARN, a nonprofit that helps working families save and invest for their futures. This program was specifically created to give every American the opportunity to build and sustain a financial future.

SaverLife is a free program that gives you the opportunity to win prizes when you save money. The prize offerings change regularly, which helps keep you excited about saving your money.

Prizes are also offered for users who make pledges (such as a pledge to save your tax refund) or share their savings stories. You could win anywhere from $5 – $1,000 in cash prizes by simply boosting your savings. You must save at least $50 in order to enter to win a cash prize.

All you have to do is link the program to your savings accounts, so it can track your savings amounts. You must be at least 18 years or older, have a valid email address, and have a savings account located within the United States.

If you are worried about security, SaverLife uses the identical type of encryption and privacy policies that other banks use. They do not store your banking information; they are simply tracking your transactions.

They also back up your data with an encryption form, so you can feel safe and secure using their platform.

You will also be paired up with a financial coach that gives you weekly savings tips to help stay you on track. Saundra Davis is their in-house financial coach. Her award-winning work and experience has helped her build coaching programs around the nation.

Getting into the habit of saving money can be challenging, so SaverLife provides a community for support. They provide blog posts and additional resources to support you with your savings progress.

SaverLife Summary

- Pros: SaverLife is a free program and you can win prizes for saving your money, pledging to save money, and sharing your story.

- Cons: There is no guaranteed earning and the application must track your transactions.

- Fees: Free

- Platform: No app, web-based

- Best for: Beginner savers or those who struggle to save on a monthly basis.

Learn more and get started with Saverlife, go to SaverLife.org.

CoinOut

![]() If you struggle with credit card spending but still want to save money effortlessly, the CoinOut can turn your receipts into savings.

If you struggle with credit card spending but still want to save money effortlessly, the CoinOut can turn your receipts into savings.

The app has partnered with companies like Taco Bell, Chipotle, Dollar Tree, Subway, Speedway, McDonald’s, and more. All you need to do is download the app and then scan your receipts to earn cash back on your purchases.

You can also earn cash back from your online purchases. Just start your online shopping from the CoinOut app and press one of the merchant buttons on the homepage–or visit the rewards section of the app to see the full list of participating merchants.

When you click on the retailer you want, CoinOut will automatically direct you to the app or mobile website of the store. Any purchase you make at that point will be counted towards your cash back.

CoinOut essentially acts as your digital wallet and uses bank-grade technology with encryption methods, and multi-verification to keep your money safe. Funds are only transferred one-way. If someone tries to hack your account, their only choice is to send money to you.

Coinout App Summary

- Pros: CoinOut gives you the opportunity to receive cash back offers from your favorite retailers for free.

- Cons: You need to keep track of receipts and scan them in for each purchase. If you forget, you could miss out on offers.

- Fees: None.

- Platform: iPhone and Android

- Best For: Savers who struggle to save extra cash and enjoy a good deal.

Learn more and get started with CoinOut, visit Coinout.com.

WinWin

![]() WinWin brings the brain-hacking motivation of gamification to your savings account. If you struggle to save money, the game-like WinWin may be able to give you a little nudge in the right direction.

WinWin brings the brain-hacking motivation of gamification to your savings account. If you struggle to save money, the game-like WinWin may be able to give you a little nudge in the right direction.

To get started, just download the app, enter your bank information, and you’re ready to play.

Then transfer $1 into your WinWin savings account to play a fun one-minute game like whack-a-mole or word finder to reveal your prize of up to $100 in cash. You can play up to 25 times every single day.

The WinWin savings account is with Wells Fargo bank and FDIC insured. You can transfer your WinWin funds back to your bank account any time you would like. You can also cancel WinWin at a moment’s notice.

WinWinSave is entirely free—for the moment. Their website does specify that there are no fees “for now.” If you enjoy playing games on your phone, consider WinWin as your go-to gaming platform, since it will help you save up to $25 per day (instead of giving money to those in-app purchases in traditional games), and give you the chance to win more money.

WinWinSave App Summary

- Pros: WinWinSave adds gamification to savings. This helps encourage you to have better savings habits.

- Cons: WinWinSave keeps your savings in a separate account in order to track your progress. Multiple accounts may become confusing.

- Fees: Free

- Platform: iPhone

- Best For: Beginning savers and/or budgeters or anyone who enjoys playing games on their phone.

Learn more and get started with WinWin.

Best Automatic Investing Apps for Beginners

Want to get started investing? These are the automatic apps you need to check out. They make it easy to understand the basics of investing and help you to set up automatic transfers to get started with just a little amount. No big minimums required.

Stash

If you are looking for a way to not only save money but invest in a portfolio you are passionate about, Stash might be your solution.

It is nice to have an automated deposit into a savings account but it might be more beneficial to allow that money to work for you in an investment account.

For a small fee, you can choose a portfolio that matches your risk tolerance as well as an investment strategy that works best for you. Fill out Stash’s investment guide and they will help you choose a portfolio that is appropriate for your needs.

Your investments are protected against institutional failure by Securities Investor Protect Corporation (SIPC). Your holdings and cash are held at APEX Clearing Corp.

Stash Invest App Summary

- Pros: You can start your account with any amount of money. Stash allows you to buy partial shares so you can invest in the market for little capital. Also, Stash uses dollar cost averaging to help reduce risk and market timing.

- Cons: Stash is automated, so there is minimal control in the investments you acquire.

- Fees: The Stash Beginner plan is $1 per month, Stash Growth is $3 per month, and Stash+ is $9 per month.

- Platform: iPhone and Android

- Best For: Newbie investors or anyone who wants to dabble in the market but doesn’t want a large commitment.

- Our Review: Be sure to read our full review of Stash Invest.

To learn more, claim your $5 bonus, and get started with Stash visit www.stashinvest.com.

Acorns

This app introduces users to the world of investing—effortlessly. There are three tiers to the Acorns app: Acorns Core, Acorns Later, and Acorns Spend.

Acorns Core links to all of your spending accounts, including credit cards, checking accounts/debit cards, Paypal, and the like, and rounds up each transaction to the nearest dollar.

Once you have reached a minimum of $5 in roundups, the money is transferred into an investment portfolio.

In addition to the roundups, you can also take advantage of Found Money from more than 200 retailers. Shop with any of the participating retailers, and they will deposit up to 10% of your purchase in your investment account.

You can also shop with Found Money partners using a chrome extension on your laptop or desktop. These deposits take anywhere from 60 to 120 days to show up in your investment account.

The Acorns app helps you to choose an appropriate portfolio for your needs by asking you a series of questions. The five portfolio options include index funds from investment firms such as iShares, Pimco, and Vanguard.

You have the option of withdrawing your funds from your Acorns Core investment account at any time, and the money will arrive in your checking account within five to seven business days. There is no limit on how much you can withdraw.

Acorns Later offers you all the benefits of the Core app, plus an easy way to save for retirement.

The program will recommend an IRA and portfolio that’s right for you and allows you to set up an automatic recurring contribution–which is not available to Core users.

Acorns Later also assists you with rollovers and automatically rebalances your account as you get closer to retirement.

Acorns Spend gives you all the features of Core and Later, plus a checking account and debit card that automatically rounds up your purchases and invests the change. The checking account has no overdraft or minimum balance fees and offers unlimited free or fee-reimbursed ATMs nationwide.

Each Acorns level has a different fee. Acorns Core users pay $1 per month, Later users pay $2 per month, and Spend users pay $3 per month—but remember, users who choose the more comprehensive programs get access to the lower-tier programs as well.

Acorns App Summary

- Pros: Using the roundup aspect of Acorns’ savings platform can make saving (and then investing) money painless. The investment portion takes the confusion and intimidation out of investing, in addition to lowering the cost threshold. Additionally, the customer service is reported to be excellent.

- Cons: You do still need to keep track of your finances to make sure the roundup feature or recurring transfers do not overdraw your accounts or overload your credit card.

- Fees: $1 per month for Acorns Core, $2 per month for Acorns Later, and $3 per month for Acorns Spend

- Platform: iPhone and Android

- Best For: Those new to investing who have a good handle on their budgeting.

- Check out our review of Acorns.

To learn more and get started with Acorns, visit www.acorns.com.

Bumped

The founders of Bumped want you to own stock in the brands you love, without the intimidation of day trading.

This recently-launched app offers a painless and 100% free way for you to start investing via the purchases you already make.

With the Bumped app (which is available for Apple and Android), you link your debit or credit cards to the app, choose which brands you would like to partner with, and then spend as you normally do.

Every time you make a purchase on your linked card with one of your partner brands, you will earn a percentage of share (generally between 1% and 5%) based on your purchase amount.

Picking brands you already spend money on means that you are receiving free money in the form of fractional shares. When you earn your share portion, it is automatically placed in a linked Bumped brokerage account.

Since Bumped helps to promote brand loyalty, brands, retailers, and other companies are eager to partner with the app, and there is a thriving list of companies for you to choose from.

The app is free, and there are no additional fees. However, Bumped will have access to your transaction history, and this data is collected and shared with affiliated third parties. If you’re uncomfortable having your data shared, Bumped may not be the right app for you.

Consumers interested in Bumped must join the waitlist, although as the company is growing and scaling up, the wait time continues to shrink.

Bumped App Summary

- Pros: Bumped makes investing completely automatic and free. If you are already brand loyal, this can be an excellent way for you to own a piece of the companies you love.

- Cons: You may have to wait a little while to get your invitation to join. If you are uncomfortable with sharing your transaction data, this app may not be right for you.

- Fees: None (It’s $0 all the way down the list.)

- Platform: iPhone and Android

- Best For: Newbie investors who are intimidated by traditional stock market investing, anyone who can’t afford traditional investing right now (especially young adults).

To learn more and get started with Bumped, visit Bumped.com.

Banks with Automatic Savings Programs

Some full-service banks come with the ability to set up automatic savings programs. Why go to an app if your bank will do the same thing, right?

Chime

Now banking is even easier with Chime. With no monthly fees, minimum balances, foreign transaction fees or overdraft fees you can rest assured that you won’t be overcharged.

Chime makes it simple and effortless to save money with their automated savings plan. They are also passionate about making you feel secure. They have automated transaction alerts as well as daily customer support for all your banking needs.

Every time you make a purchase or pay a bill with your Chime Visa® Debit Card, you will be adding to your savings account. The Save When You Spend feature automatically rounds up transactions to the nearest dollar and transfers the difference from your Spending

Account into your Savings Account app. Chime members can also automatically transfer 10% of every paycheck directly into their Savings Account on payday, making it easier to grow their savings without feeling the pinch.

Chime’s mission is to help you create a healthier financial life for you and your family. By pairing technology with a strong mission, they are able to give their members an outstanding banking experience.

They also charge no fees, with one exception: There is a $2.50 fee for over the counter cash withdrawals or using an out-of-network ATM that is not part of Chime’s fee-free network of 38,000 ATMs. This fee should be easy to avoid, however.

Chime App Summary

- Pros: There are no fees and no minimum deposits required. You can also be rewarded for using their Visa card. You can receive cash back or points on your everyday purchases or bills.

- Cons: If you like the idea of having a bank branch that you can walk into, Chime might not be the bank for you. This application is 100% automated and that may be a little intimating to some.

- Fees: None, except a $2.50 for using ATMs outside of the fee-free network of 38,000 ATMs, or for over the counter cash withdrawals.

- Platform: iPhone and Android

- Best For: Anyone who is comfortable with automating all of their banking efforts.

To learn more and get started with Chime visit www.chimebank.com.

Qapital

Qapital motivates you to save by having you set up a goal to achieve. Once you have linked a checking account to your Qapital account (an FDIC-insured Wells Fargo savings account), you pick any goal you want to reach.

From there, you set up savings rules to help you achieve your goal. There are eight different types of savings rules you can follow with Qapital:

- Set & Forget: This is simple automation, where you can save a set amount on a daily, weekly, or monthly basis.

- Roundup: This is similar to all of the roundup options in other apps, except you can round up to the nearest $1, $2, $3, $4, or $5.

- Spend Less: When you spend less than your target budget amount, you can save the difference. For instance, if you spend less than $15 at Starbucks per week, this rule will save the difference toward your goal.

- Guilty Pleasure: If you struggle with a certain type of spending, you can set up an automatic savings amount to go into your account if you give in temptation. So you could save $10 every time you make a purchase at McDonald’s.

- Apple Health: (Not available on the Android app). Pay yourself for working out. If you hit a fitness goal, Qapital will save money towards your goal. For instance, you could save $25 towards your vacation every time you take 10,000 steps in a day.

- IFTTT: IFTTT stands for If This Then That, and you can decide whatever you want that will cause a triggered savings–like saving $20 every time you fill your gas tank or saving $0.50 each time you like a video on YouTube.

- Freelancer: Every time you get paid, put aside money towards taxes.

- 52 Week Rule: Save $1 the first week, $2 the second week, and so on for 52 weeks

To protect you from potential overdrafts, Qapital pauses any transfers that will leave you with less than $100 in your funding account. That pause also applies to any rules that might be triggered–until your account balance has gone up again.

As of November 2018, there are now three membership tiers with three different pricing amounts: Basic, Complete, and Master. The Basic plan costs $3 per month and gives you access to Qapital’s goal-setting program and the customizable and automated rules.

You can set unlimited goals with the Basic plan. The Complete plan costs $6 per month and offers users access to Qapital’s saving, spending, budgeting and investing tools, including the Qapital spending account that comes with a Visa debit card.

With this account, you can write e-checks and receive 0.1 percent interest. The Master plan, which costs $12 per month, offers you everything in the Complete and Basic plans, as well as access to webinars and in-app money-saving challenges.

Qapital Summary

- Pros: Qapital leverages your behavior to increase your savings. The customizable and automated savings rules can help you stay motivated to reach your goals.

- Cons: You need a checking account to fund your Qapital account. You cannot use a savings account as your funding account because there is a minimum of eight Qapital transactions per month, which would go over most banks’ free savings withdrawal policies. There are no physical banks to speak to a customer service representative in person. You’re limited to $1,000 per day in ATM withdrawals. Qapital doesn’t cover ATM fees that other banks may charge.

- Fees: $3/month for Qapital Basic, $6/month for Qapital Complete, and $12/month for Qapital Master

- Platform: iPhone and Android

- Best for: The person who is goal-motivated, enjoys conducting banking via an app, and wants to effortlessly save using automation.

To learn more and get started with Qapital visit www.qapital.com.

Bank of America’s Keep the Change

![]()

Bank of America’s Keep the Change savings program is the granddaddy of modern automatic savings apps. Keep the Change was launched in 2005 for Bank of America customers, and it is still going strong.

In order to qualify, you must have a Bank of America checking account, debit card, and savings account.

Like Acorns, Keep the Change rounds up each purchase you make with your Bank of America debit card, and places the change in your savings account.

For instance, if you spend $4.17 on a cup of coffee and a muffin, $0.83 will automatically be placed in your savings account, and your checking account will be debited for a full $5.

If you do not have enough funds in your account to cover your Keep the Change roundups for the day, Bank of America cancels the Keep the Change transfer for that day in order to protect you from overdraft.

Also, if you end up returning an item or having a purchase canceled, the Keep the Change transfer associated with that purchase does remain in your savings account.

The Bank of America savings account where your money is transferred does accrue interest, although the current rate for a regular savings account is quite low. You can access your money in that savings at any time.

Bank of America offers a mobile app that will allow you to monitor your Keep the Change savings, along with your other banking.

Keep the Change Summary

- Pros: Automatic transfer allows for painless savings, and checkbook balancing becomes easier because every purchase is a whole number. Bank of America cancels Keep the Change transfers that would overdraw your account.

- Cons: Keep the Change is only available for Bank of America customers. The interest rate is very low, and you might need to transfer money occasionally to higher interest-bearing accounts.

- Fees: None

- Platform: iPhone and Android

- Best for: Bank of America customers. If you already bank with B of A, it makes sense to try the in-house automatic savings app.

To learn more and get started with Bank of America, visit www.bankofamerica.com.

Why Save Automatically?

We all know that saving money and investing regularly is an important part of a health financial life. The reason to make these processes automatic is that it takes the decision making out of our hands.

When we don’t have to think about either of these options is ensures that our saving and investing gets done. If you are a hyper organized and driven person this may not be necessary, but for the rest of us, saving automatically is one of the best ways to help our finances.

Great article! Round-ups can be such a mindlessly effective way to build up savings. I really like digit, but I don’t love the monthly fee they charge for the premium version. It feels pretty counterintuitive to spend money on a savings app.

There is another app called Peak Money that is really similar in how it works, but it does not have the monthly fees. It is definitely worth checking out if anyone here loves digit but is tired of paying for it!

Nice list of apps and an overview of them. I like Digit the best from this list given the ease of automating savings.

There is one gripe I have with Digit though.

Today, Digit does not allow you to link to an external robo-advisor like WiseBanyan, Betterment, Wealthfront or the like.

This means you have to withdraw the savings from your Digit account back to your bank and then transfer it to your brokerage or Robo-advisor of your choice to invest your savings.

It takes two steps when it should actually take only one.

I have been persuading Digit to allow establishing external links.

I would greatly appreciate if the PF community puts the same pressure on Digit so that it is a win-win for everyone.

–Michael

Automating money is such a new concept to me. I’m old school with my excel sheet! Definitely will have to look into these. Great list!

These are definitely becoming more popular ways to save money. I love that they automate things for you and make it easy.

Thank you.

Surprised to not see Mint here.

Also when discussing apps that link to your personal financial information, details about security and who owns and runs the apps and servers should be discussed.

Great point about security, Philip. We’ll include that in our next update.