How to Save 20% of Your Income (Consistently) Each Year in Your 30s

Listen to this post, courtesy of the team at Optimal Finance Daily.

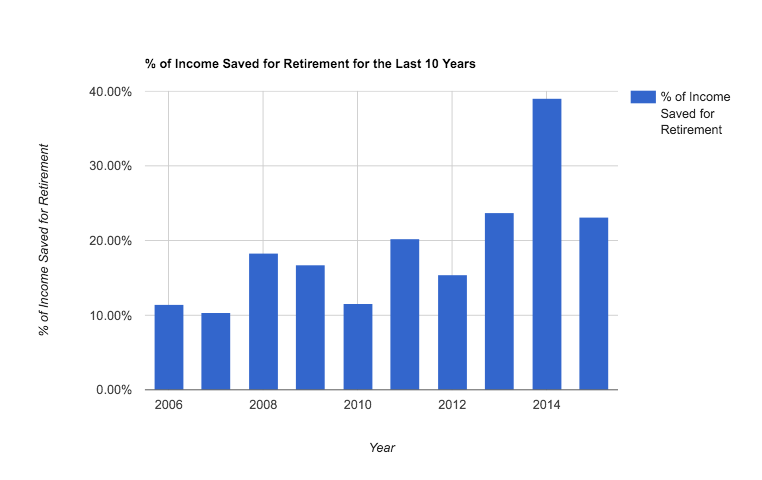

Today I want to show you how over the ten years of our marriage (my 30th through my 39th year) we’ve saved an average of 20% of our pre-tax income towards retirement.

In our worst year, we saved 10%, and in our best, nearly 40%! Not bad, right?

20% just happens to be one of the most commonly recommended percentages for retirement savings. Total coincidence, I swear.

Regardless, saving this much money has led to us to look at our balances and ask the question, “should we stop saving for retirement altogether and start focusing on other goals: the mortgage, college, fun, etc.?”

I’m by no means taking a victory lap here – we’re not prepared to retire early. But I do hope this article will give you a snapshot of what’s possible over a ten year period. Here’s an actual snapshot:

Today I want to share the why and the how of our retirement savings history.

But first, some caveats:

- We didn’t blow the other 80%. This is only retirement savings, not all savings (see all of our savings goals). Over these ten years we’ve also saved up for 20% down payments on two homes, paid for a new van with cash, started some taxable investing, and paid off large debts, like our student loans and old car notes. If I had to calculate our actual living cost % after taxes, tithing/charity, and non-retirement savings goals, I would put it at around 55-60% of our income.

- I became self-employed in 2010. Which allowed us to open up Solo 401K accounts and significantly increase our annual tax-advantaged retirement savings abilities. This, in combination with getting rid of debts has led us to be able to save more and more each year.

- Finally, I’m not sharing our income here, but I can give you some examples of what saving 20% for ten years might look like for certain incomes (assumes a 6% return):

– Someone with an income of $25,000 saving 20% would be able to amass $69,858.21 over ten years. That amount would turn into $224,044.74 over the next 20 years without saving any more.

– Someone with an income of $75,000 saving 20% would be able to amass $209,574.64 over ten years. That amount would turn into $672,134.26 over the next 20 years without saving any more.

– Someone with an income of $125,000 saving 20% would be able to amass $349,291.07 over ten years. That amount would turn into $1,120,223.78 over the next 20 years without saving any more.

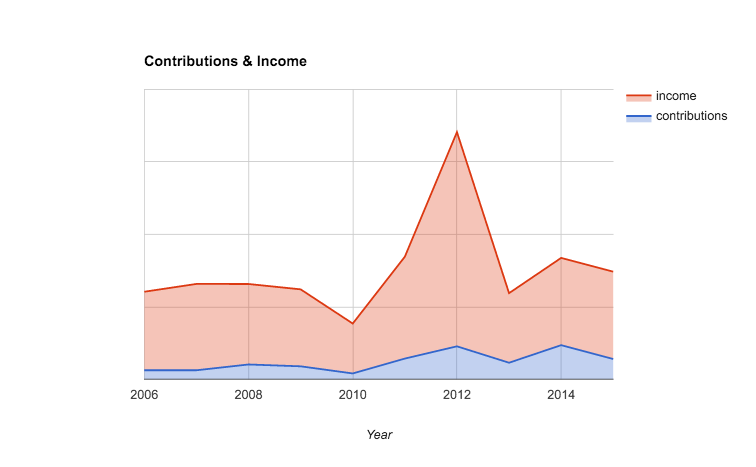

So as you can see, saving 20% in your 30s will have you well on your way to a healthy retirement account. Here’s a quick snapshot of our income compared to our contribution:

Why We Saved the Percentage We Did

My motivation for saving for retirement in our 30s was two-fold:

First, and maybe surprisingly so, I don’t like paying federal income taxes. Any chance I get to escape a few taxes I’ll take it, even if temporarily. So, when I started earning good money through my job, I saw my company 401K as a way to reduce my current tax bill. Sounds crazy, I know. But it’s honestly a big part of my motivation.

Much of this passion was driven by reading personal finance blogs in my late 20s and early 30s and being inspired by those stories – which is why I’m sharing this post today.

Secondly, I value security, personal responsibility, and my independence. I don’t want to depend on anyone for assistance when I’m old and too tired to work for myself. Having a nice retirement savings will allow me to rest a bit easier in my older age, knowing I’m not a burden on my fellow man.

For Mrs. PT, she’s simply more conservative financially and values security even more than I do. So she never lacked any motivation to save for the future. She’s frugal by nature.

We didn’t set out to save 20%. In fact, we’ve never sat down to determine an actual percentage. Our approach has always been about saving as much as possible and at a minimum, getting our employer matches and hitting our maximum annual contribution limits.

20% is probably a great percentage for anyone to aim for if you’re considering building up enough savings to comfortably retire (possibly a bit early). But don’t think you need to start out there.

We started around 10% (and I was saving even less than that when I was in my 20s). Just get started saving now and you’ll find that as you mature financially, you’ll want to save more.

How We Saved 20% of Our Income for Retirement

While 20% isn’t a mind-blowing percentage of savings (there’s a new movement of 50% savers out there, which I highly applaud), it is consistent and significant for our long-term financial future. Here’s how we did it:

1. We used the tax-advantaged accounts available to us. When I was working in corporate (2006-2009) I used the company 401K (and match) while Mrs. PT used her 403B. When we “maxed” those options out, we opened up Roth IRAs (in 2008) to place additional savings. And when I became self-employed (2010), we opened up Solo 401Ks. Each account has different rules, but we usually were able to use two or more in tandem. For the extra curious, we use this one fund in all of our retirement investing.

2. We automated our savings deposits where possible. Nothing has led to more consistent savings for us better than the automatic savings approach. It just works. If you aren’t automating your retirement savings, go right now and start it up. There are also apps that can help you automate your savings.

3. We saved the increases. When we got more income, either because debt reduction freed up more money in our budget, or simply because I started making more with my business, we always put that extra money towards more savings. We didn’t let our lifestyle creep up to match our new disposable income.

4. We did a few crazy things. Over the years we’ve made some sacrifices and lived an unorthodox life in pursuit of a more frugal existence. We’ve:

- cut the cable,

- built our own furniture,

- done some DIY home repair,

- kept the same car for 10 years (I need to write about this apparently),

- gone on a week-long spending freeze,

- and most recently switched to a medical sharing program.

I share those things to spice this post up a bit and give you a little something interesting to take with you. But my beliefs about frugality have evolved since first setting out to “save money” by doing some of these things.

I think frugality it great, and the practice of it has led to a healthier, happier life. But frugality really hasn’t moved the needle for us in our ability to save as much as we have. We’ve saved consistently because we’ve focused on #2 above. It’s the most important thing to do.

Takeaways For Your Retirement Savings Journey

- A decade of saving consistently can have a significant impact on your retirement.

- It’s important to find your motivation, but relying on a system of automatic contributions is key.

- 20% is a great goal for those in their 30s, but you don’t have to start there. Start at 10% like we did.

- Getting rid of debt and building that side income can help you get to your goals faster.

What percentage of your income are you saving for retirement?

After I got married my saving percentage went down dramatically to 10% because my wife doesn’t contribute to our family, I’m a solo warrior.

Before getting married, I was saving between 60 to 90% in any giving years from 20 when I finished school till 32 when I got married.

Saving is crucial and the only way to financial freedom if you aren’t born with the silver spoon… and of course, hard work.

My savings (which currently includes debt payments) averages around 50% of my income. I did not shoot for that percentage. It just sort of happened. I’m looking forward to destroying the debt and sending all that savings to retirement savings. That will be amazing progress.

Hi PT,

I was reading your tip about using the Digit app. First, I have a problem with all the apps ‘everyone’ wants you to use and the memory they take up. Second, I’m nervous about sending my money somewhere I don’t know. Can I retrieve it? How quickly? Third, I am on a tight budget and I watch my account carefully to be sure I have enough to pay all my bills. Having said all that, I do save $10 every month. I transfer it to my savings account without fail. I now have about $400. Hopefully, I will be working soon and able to save more.

You are asking the right questions. Digit’s bank account is FDIC insured. You can get your money back at anytime. The Digit app is careful not to save too much of your money, leaving you short. It will gradually increase your saving as it gets more familiar with your monthly spending needs. It’s a genius app.

TECHNOLOGY CAN HELP—WHY NOT USE IT?

My wife found a great software to money management- Geltbox money – its Simple to use, quick and intuitive.

automatic download from any website (banks,credit cards) , high level of security (Your financial data is securely stored and encrypted only in your personal computer)

I think people should also focus on saving more tomorrow. Make a commitment to save a percentage of every salary increase, studies have shown it’s a great way to save more.

Yeah boy! And you wanna hear the crazy thing? I’ve been reading your blog for almost 10 years now! It’s a good thing we’ve been saving the whole time – we’re old men! 😉

Great article though… don’t be surprised if it shows up on a site that sounds like Boxtar Winance.

Impressive, PT.

I really like your strategy.

I see so many people who do not save at all for retirement.

So sad, in my opinion.

Thanks for sharing 🙂

Being financially successful in the long run really is as much (or more) motivation than knowledge, but it always comes back to the simple principles you suggested of starting early, taking advantage of the accounts and opportunities right now, automating the process and not living a lifestyle above what would allow you to save. 20% is a great average-I know want to go back over the last 10 years and see what our percentage is!