Liberty HealthShare Review

Important: We’ve received a large number of negative comments about Liberty Healthshare, and their legal troubles are not a good sign. If you’re looking for another option, we recommend you consider our full list of healthshare plans.

Stratospheric health insurance premiums have become practically cliche in recent years. So much so, that even eight years into the rollout of Obamacare, millions of Americans continue to go without health insurance.

If you can get health insurance through your employer, that is usually the cheapest option. But if you are self-employed it can be difficult to find affordable options.

Christian health sharing ministries are one of the very best alternatives to traditional health insurance. And one of the most well-known health sharing ministries available is Liberty HealthShare.

Participation in the ministry could enable those who can’t otherwise afford health insurance to get coverage, and many others to get it at much more affordable rates.

About Liberty HealthShare

Based in Canton, Ohio, and started in 1995, Liberty HealthShare is a health care sharing ministry sponsored by The Gospel Light Mennonite Church Medical Aid Plan, Inc. It’s based on the Biblical directive to bear one another’s burdens (Galatians 6:2).

Health-sharing ministries are not insurance in the true sense. They’re actually faith-based plans in which individual members pool their funds, to pay for the medical expenses of those within the group who incur them. This is similar to what insurance does, but it lacks a lot of the more technical and specific provisions of actual health insurance.

However, the net effect of health sharing ministries is very close to traditional health insurance, which is why they’ve become so popular in recent years. Because they are lower in cost than traditional health insurance, they’ve become even more popular since the rollout of the Affordable Care Act (aka Obamacare), and its attendant high premiums.

Keep in mind that health sharing ministries are exempt from the Affordable Care Act penalty (which was due to expire in 2019 anyway).

Related: Medi-share Review: The Affordable Alternative to Expensive Health Insurance

How Liberty HealthShare Works

Each participating member makes a monthly contribution (“monthly share”) to an online ShareBox. Through the ministry’s ShareDirect bill payment, the amount in a member’s ShareBox is automatically transferred directly to another member’s ShareBox, to pay for any eligible medical expenses for that person.

One of the benefits of this ministry is that you’re free to choose your own doctor. There are no networks that are typical with traditional health insurance. But the ministry works with both members and their medical providers to keep costs fair and reasonable.

If you have a medical procedure coming up, you can check with the ministry and they’ll help to find the best provider while eliminating unnecessary costs and procedures. In a fact, it’s set up as a self-pay system, but one supported by the ministry community.

When you submit your medical bills, the ministry has a team of professionals that will advocate for you with your service providers to keep costs reasonable.

Unlike many traditional health insurance plans, the ministry does not require referrals and only limited pre-notification. But you will be issued an ID card that will have all the necessary information for the plan.

Since Liberty HealthShare is a health sharing ministry and not traditional insurance, services are handled a bit differently. You must explain to the provider that you are self-pay, but part of a community of people who have pledged to share expenses.

(They will almost certainly be familiar with the health sharing ministry concept.)

Present your ID card, and explain that your bills should be sent either electronically or by mail according to the instructions on the card. Reimbursement will come from the ministry.

Related: Christian Healthcare Ministries Review: Save Thousands Per Year on Healthcare

Liberty HealthShare Eligibility

To be eligible for the ministry, you must be healthy and leading a healthy lifestyle, and not use tobacco, or abuse alcohol, illegal drugs, or prescription drugs. You must also strive to live in accordance with biblical principles and participate regularly in worship or prayer.

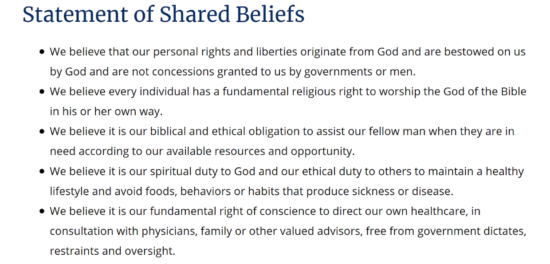

As a member of the ministry, you must pledge to abide by the Statement of Shared Beliefs, then truthfully disclose information about yourself, both when you join, and when you submit medical expenses for sharing.

The Statement of Shared Beliefs is as follows:

Liberty HealthShare Features and Benefits

Pre-existing conditions. These are excluded from coverage for the first 12 months of participation. Limited coverage (up to $50,000) is available for the first 13 to 36 months of participation. After 36 months, pre-existing conditions are eligible for full sharing.

Prescriptions. Tier 4 prescriptions used for acute illness for the 45 days following each related medical incident are eligible. However, tier 1, 2, and 3 prescriptions are not. (Tier 4 drugs are high cost prescriptions, which do not have generic equivalents. Tiers 1 – 3 include generics, non-preferred generics, and preferred brand name medications.)

Provider network. There is no network, and you can use health care providers of your own choice. However, the ministry does have a list of more than 23,000 preferred providers nationwide.

HealthTrac. This is a special provision for those with pre-existing health conditions. This program was developed so that qualifying members can improve their health. It’s specifically designed for those with pre-existing conditions that can be positively affected by making certain lifestyle changes. Those conditions include diabetes, hypertension, heart disease, high cholesterol, obesity, and even tobacco use.

Participants are assigned a health coach, who helps to develop a personal plan to achieve goals related to the condition. Participants are required to check in at least once each month to track progress through the program.

The health coach will help to set realistic goals, provide tools and resources to help achieve those goals, send motivational and inspirational tools, and provide diet recommendations, including designing a balanced menu per the participant’s request.

HealthTrac has a participation fee of $80 per month, over and above the regular monthly share amount. But once the participant reaches their program goals, the fee is removed.

Example: Family of Four Using the Three Different Liberty HealthShare Plans

Liberty HealthShare offers three different program options. We’re going to take a look at all three, and then we’re going to look at two plans from the health insurance exchanges for comparison sake.

I’ve done a profile of a fictitious family of four to compare coverage between all three Liberty HealthShare plans, and two from healthcare.gov.

The family profile is as follows:

- Husband, age 40

- Wife, age 40

- Child, age 12

- Child, age10

- Household income, $100,000 per year

- Location, Fulton County (Atlanta metro area), Georgia

For each of the five plans listed below, we’ll calculate the cost of coverage for this fictitious family.

Liberty Complete

This is Liberty HealthShare’s most popular plan. It covers eligible medical costs up to $1 million per incident. It also provides the entire range of medical and pharmacy discount services.

The annual unshared amount (deductible equivalent) is $1,000 for an individual policy, $1,750 for a couple, and $2,250 for a family.

Under the Liberty Complete plan, the cost of coverage for our fictitious family of four is $529 per month, with a $2,250 deductible equivalent.

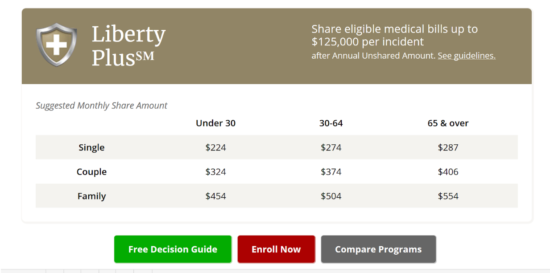

Liberty Plus Plan

This plan covers medical costs up to $125,000 per incident. It also includes the full range of medical and pharmacy discount services. The annual unshared amount Is $1,000 per individual, $1,750 per couple, and $2,250 per family.

Under the Liberty Plus plan, the cost of coverage for our fictitious family of four is $504 per month, with a $2,250 deductible equivalent.

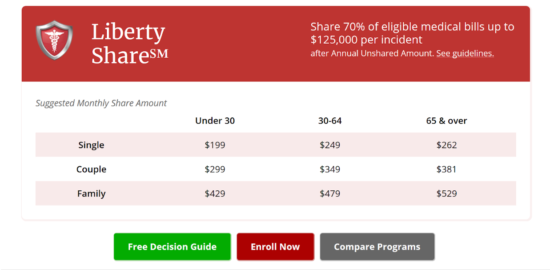

Liberty Share Plan

The Liberty Share Plan covers up to 70% of eligible medical costs, up to $125,000 – which tells us this is NOT a cost-effective plan. The slight savings in the monthly share amount doesn’t justify the much greater liability the family is assuming.

Medical expenses are met on a per person, per incident basis, when treated by physicians, urgent care facilities, clinics, emergency rooms, or at both inpatient and outpatient hospitals. There is no pharmacy discount service with this plan.

The annual unshared amount is $1,000 for an individual policy, $1,750 for a couple, and $2,250 for a family.

Under the Liberty Share plan, the cost of coverage for our fictitious family of four is $479 per month, with a $2,250 deductible equivalent.

Now, let’s shift gears, and look at two plans from the health insurance exchange for Fulton County, Georgia.

Example: Family of Four Using Two Different Obamacare Plans

Healthcare.gov provides a site where you can get estimates of health insurance plans in your area without having to go through the full application process. I’ve pulled up two that are most comparable to the plans offered by Liberty HealthShare.

Both plans reflect a $600 per month tax subsidy. But be aware that if the family’s household income goes above $100,000, the tax subsidy will decline, and eventually disappear. By contrast, health sharing ministry plans don’t have a subsidy, and aren’t restricted by income level.

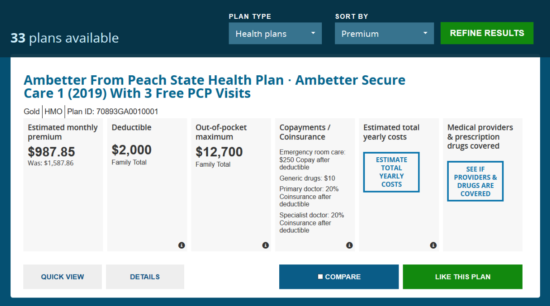

The first is a Gold plan, offering a low deductible of $2,000. The low deductible is the reason for this quote. But the out-of-pocket maximum is $12,700, which includes deductibles, co-payments, and co-insurance provisions. Under the co-insurance provision, you’re required to pay 20% of your medical costs beyond your deductible. Once you reach the out-of-pocket maximum, services are covered at 100% of cost.

The monthly premium is about $988, with the potential out-of-pocket maximum of $12,700. But notice the cost of the plan will be $1,588 per month if the $600 per month tax subsidy goes away.

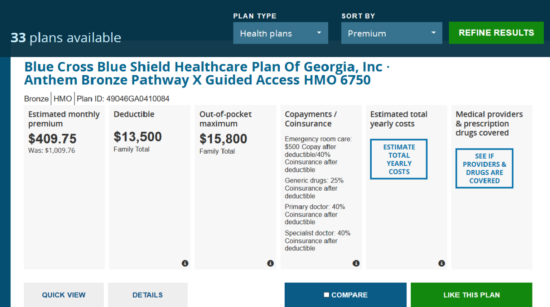

The second is a bronze plan. With this plan, we’re looking at the lowest cost plan, but that comes at a cost of a much higher deductible.

With the monthly premium of $410, the annual cost of the premium is $4,920. But if you have an unfortunate year, where you reach the out-of-pocket maximum of $15,800, your total cost for the plan for the year will be $20,720.

The premium is certainly reasonable on this plan. But should the worst happen, the high deductible means possible medical expenses of over $20,000. That could bankrupt a family of four. What’s more, if the $600 per month tax subsidy is removed, the actual cost of the plan goes to $1,010 per month. And that still includes the $15,800 out-of-pocket maximum.

Liberty HealthShare vs Obamacare: Who Wins?

Showing five plans was just for comparison sake. The best “head-to-head” example though is between the Liberty HealthShare Liberty Complete Plan and the Healthcare.gov Gold plan.

With the Liberty HealthShare Liberty Complete Plan the monthly premium is $529, and the deductible equivalent is $2,250. Plus, you won’t be at risk of losing a premium subsidy for a higher income.

Under the Gold plan, the monthly premium is $988 with a $2,000 deductible. But you also have an out-of-pocket maximum of $12,700, as well as the possibility of losing some or all of the tax subsidy if your income increases.

If you go with the Liberty HealthShare Liberty Complete Plan, you’ll save $359 per month, as well as avoid up to $12,700 in out-of-pocket costs.

This is the reason why health sharing programs are becoming so popular.

Liberty HeathShare Pros and Cons

Pros:

- Ministry plan costs are about half what they are for traditional insurance.

- The deductibles and maximum out-of-pocket costs are much lower than traditional health insurance.

- Provider reimbursements are faster and less bureaucratic than traditional insurance, a winning point with hospitals and doctors.

- There is no out-of-network limit. Traditional health insurance often restricts out-of-network reimbursements to 60% o 70%.

- Health sharing ministries have become one of the most popular alternatives to high cost health insurance.

Cons:

- The plan is not available to the general public. You must be a practicing, Bible-believing Christian to participate.

- Liberty HealthShare is not an insurance plan, and does not guarantee payment of medical bills (though they do have an excellent record of payment).

- There are no benefits available beyond the limits of each plan.

- There is a possibility that a provider won’t accept participation in the ministry.

Should You Join Liberty HealthShare?

No. They simply aren’t in good standing with many customers and they are experiencing legal challenges to their business.

If you’re currently going without health insurance, or you have it and the payments are breaking your budget, joining a health sharing ministry is one of the best possible alternatives. Though it’s not traditional health insurance, it provides nearly equivalent benefits. And it does so at about half the cost of traditional health insurance.

Liberty HealthShare is one of the largest and most highly regarded health sharing ministries in the country. If you decide to go the health sharing ministry route, however, try Med-Share.

Looking for a second option? Consider Medishare and read our founder’s success story with their program.

What’s your health insurance situation like? Have you ever tried a health sharing program?

I have been a member of Liberty Healthshare since 2016. Although not perfect, I was happy and referred several family members. It has always taken way too much time to be reimbursed or pay providers but I could live with it. As of March 1, 2022, this has been SHATTERED!

In Nov. of 2021, program changes were announced and large increases were imposed. I wanted to keep the program I had been on up to this time was ok with the increase in premium and chose a new program that kept in line with what I had paid for since 2016. I had to make a decision prior to March 2022. On March 1, 2022, the CEO posted a letter that basically says they will not pay for anything above what they deem to be “fair”. My experience in the last 5+ years is that what they consider “fair” is about 10% of what the providers are billing. At that time, you must send in for a Balance Bill negotiation. After all is said and done, this is usually about 30% of what the providers are billing. On routine things, this doesn’t seem to be the case. But, when hospitalized, it has IN EVERY CIRCUMSTANCE, been the case. Routine things will no longer be covered if the bill is less than $200. It appears, then they will not be covering ANYTHING. This WAS not part of the program I signed up but yet I am locked into it and cannot make a change until next year.

Now, they knew these changes were coming yet didn’t announce until after you have made your plan choices which cannot be changed for another year. Totally SLEAZEY!

FAIR WARNING–THIS IS NOT WHO YOU WANT TO TRUST WITH YOUR HEALTH NOR THE HEALTH OF YOUR LOVED ONES!

I have been a $500/mo paying member if Liberty for over 10 years and needed their services for the first time 11 months ago. After jumping through all the hoops for negotiating cash prices for

a major surgery and going to great pains to satisfy the hospital up front, not one dime has been received from Liberty. ELEVEN MONTHS of waiting.

I am a fan of healthsharing but not of Liberty… just fyi.. they recently reached a settlement with the OHio Attonry General demanding a restructuring and assessing fines for them and their vendors, They have had a class action lawsuit filed against them and have over a thousand recent complaints with the BBB and close to 300 with the Ohio AG recently…Go to google and type in Liberty Healtshare reviews and go to any page not controlled by them and see what you think… huge problems

Hi Lisa,

We are sorry to hear that. Healthsharing is unique and special and requires our members to become familiar with a different way of caring for their health.

Many of our members enjoy the freedom of healthsharing. However, we understand that it’s not for everyone.

Thank you.

I do not recommend Liberty Health Share. I was with them for 3 years, and had nothing but trouble trying to get reimbursed.

You can find better plans that are less money per month and give better service.

Please pay attention to the other reviewers here.

If I could do 0 stars I would. This company is the absolute worst. If you ever plan on using your benefits plan for it to take a year or longer to get it resolved. My accident was on May 5th, 2020, and I was told that I would be responsible for $1,000 and then everything else would be covered.

Fast forward more than a year and two lawyers later. I had to babysit each medical bill and if they are sent to collections Liberty Health Share does nothing to help. They don’t care about how it impacts my credit or my life. This company is the most un-christlike company I have ever worked with. What they do to people is borderline criminal. If you sign up with them do it at your own risk.

Hi Jared,

As a healthsharing ministry, our members do not ‘cover’ one another’s medical expenses. Instead, they are committed to the sharing process, such as making wise health choices, receiving fair prices, working with their providers to manage their expenses, and sending in contributions to other members in need. In the previous 4 years, our healthsharing members have shared more than $1.2 billion in medical costs and continue to share millions of dollars in medical costs each month.

Do not go with Liberty Healthshare under any circumstance. Their payments are now a MINIMUM of 180 days after services are provided – if paid at all. Per their customer service specialist – “no one knows when a check will be cut” – that was the entire response we received when we inquired about reimbursements to us for out of pocket medical costs in excess of $8,000 that were paid by us in November of 2020. When my husband needed to get kidney stones broken up we couldn’t find anyone that would provide the service unless they were paid in advance because they have had so many instances of non payment for approved services by Liberty Healthshare. This is not a good program for anyone and you risk personal bankruptcy if you have any serious issue. We went with this due to it’s Christian affiliation. In no way have I seen any Christian handling of anything – seems it’s just there so they can limit what they cover.

I recently filed a complaint with the Better Business Bureau against Liberty Healthshare because after 180 days they still haven’t paid all my medical bills.

State Attorney General’s from across the country have received complaints about Liberty Healthshare for not paying out medical bills.

I do not recommend this organization at all. Stay away. They will gladly take your monthly payment but when it comes time to pay your medical provider, good luck.

So much for them claiming to be “a Christian organization.”

P.S. Liberty Healthshare recently announced their CEO is leaving. Lost count how many CEO’s they’ve been through in the last 2-3 years. Total mess.

“They have an excellent record of payment.” Seriously? Apparently you have not dealt with Liberty recently. I’m in Liberty hell. SO many outstanding bills. I have literally scores of them, totally well over 100K. I’m losing sleep at night. Trying to figure out my options.

I do NOT recommend Liberty HealthShare to anyone.

I also have been waiting for the to process a total of ten (9) claims for payment now going on seven (7) months. Out of nine (9) bills that my husband had was for a Hospital and today received Final Notice or collections….He was in the hospital in December of 2018. Sadly I do not have the money to pay this bill. For a fact they can’t even process a claim for a total of $129.00 for an clinic. I had to pay that one cause that one was also being sent to collection.

I also have had same services as below unhappy customers…Reps do not know anything. They said they have a new computer system. They cannot find me in the system with the ID number from the ID card. They give me their fax numbers to have providers fax claims to them. The last one I have an advocate with an ext. number I call and he does not call back, etc.

I chose this company mainly because is Christian based. The way they conduct themselves is anything but in a Christian way. I am quite upset that they got to me by one thing that matters to me which if my faith.

It is quite interesting that they were getting my premiums right on time out of my checking account. It is amazing how their new or new computer system did not failed them when it came to taken my premiums.

My wife and I concur with all the commenters as well. My wife was diagnosed with the big C, double lung cancer, stage 4. We advanced our personal funds to help us hurry up and find out what was wrong with my wife. We paid cash prices that had substantial discounts thinking we were also helping Liberty. We submitted expenses in March and on June 7th we found out they have not even entered our bills (even though our assigned senior provider relations advocate said she could see them in their system) that we faxed to them nor have they paid the majority of medical services invoices submitted to them. On the one hand they were forced to pay for my wife’s very expensive chemotherapy medication because the drug company would not release it unless Liberty paid cash; for this Liberty has been a blessing to us. However, they give us the run around regarding all other providers and for reimbursing us. Their ShareBox portal tells us very little and is a very poor system. Calling and listening for months automated attendant say “please be patient as we are upgrading our systems…” then to be placed on hold for ever. They are full of misleading statements via e-mail communications and on the phone. My wife and I have grown so discouraged that we would not recommend Liberty to anyone looking to sign up with a health sharing ministry. Shop and use other services first. Disgusted and let down in Idaho!

I concur with all the commenters here who are dissatisfied. Read the many YELP reviews and mine is there too. I have waited 15 months for a single reimbursement of $1100 and they literally tell me the check has been mailed. And I have called 3 times a month for over a year. The customer service team starts anew every time, with each phone call, because they do not save prior phone call information. And the hold time is magnitudally long.

Liberty is a shell game, a scam. I have LONG outstanding bills and cannot get answers on the phone nor replies to my many emails. Do not endanger your health nor your financial situation by doing business with Liberty Health Share.

I’m not sure where you are getting your information but I cannot imagine this company being able to continue for very long unless some changes are made. I have had outstanding charges since July and August of 2018 and a wellness check bill from September of 2018 that is yet to be paid. I was told this morning that they JUST BEGAN the processing of my September expenses last week, and that it would take another 60 days to process. Really? Also, I have also not come across a doctor anywhere that wants to work with them. They have all refused so far. I really wanted them to work out for us but I can’t handle their inefficiency much longer unless things drastically change. My advice to anyone at this point is look elsewhere. If anyone from Liberty reads this review I would love for you to answer these issues. Nobody I’ve spoken to at your office has any helpful information for me. They all just say “I’m sorry, I do understand your frustration”, which doesn’t help AT ALL. It’s just a platitude.

The bill ($300+) of my wellness check in August 2018 was not fully settled and the balance bill turns out being followed up by the collection company. It’s going to crash my credit rating if not settled within 30 days. It’s still outstanding now.

Great idea, except they don’t pay – They are in violation of their own shared beliefs. I understand growing pains but lack of truth handling my issues is unacceptable.

By the way, this article is outdated, The annual “deductible” or unshared amount for a family of four is now $4000, not $2250 as this article states. That amount was doubled per individual in 2018 with 3 months warning for members. And no provider will accept Liberty anymore because of their poor reputation in the medical community, so you have to pay everything up front except I’ve had minor success with some hospitals that will still try to bill “insurance” directly for surgeries, or outpatient treatments, etc.

Liberty used to be great, but they have gone down hill severely. Couldn’t handle the growth. I do not recommend them as a current member. I will be switching as soon as I can.

Liberty HealthShare raised my rates in September of 2018; Unfortunately, it’s hard for a customer to do anything about it….it’s like you just have to take it.

Anyway, I searched for healthcare on the government site and found that I actually qualify for a reduced rate so I called them to cancel my Liberty Healthshare as soon as I knew I was accepted, but unfortunately they didn’t care. They told me I had to pay another full “voluntary” donation because I called after their “cancel by the 20th rule” that was in the contract I had apparently signed when I joined a couple years ago when their rate was lower.

I asked them to please waive the required “donation fee” since they had my credit card on file and that it wasn’t going to be charged for another week or so. They told me to write an email stating my case (which was that I could not afford to double pay insurance that month), but they apparently never intended on considering my plight and just answered me by stating the rule and sending me a copy of the contract I had signed a couple years prior. Anyway, this is how I feel about Liberty Healthshare:

They are a great example of heartless customer service during the holidays (it was right after Christmas and New Year’s when I was accepted into my new healthcare program) when they conveniently already have my credit card on autopay (and could have easily taken me off since I alerted them well enough before their credit card charge date). I feel like they are a sad example of a Christian “organization” and it shows what really matters to them, the almighty dollar. Funny that it says it is a voluntary donation, yet I cannot voluntarily withhold my donation (fully knowing I wouldn’t be covered by them that month) once they had my credit card, even though I cancelled before they ran it. They have their “by the 20th rule” so no reason to ask for any favors from them. I feel like their motto is “Screw the person by rule.” They have No compassion as an organization which is interesting coming under the guise of a supposedly compassionate “religious” organization.

I had asked for some leeway and they won’t even hear it. The person on the phone just barked at me the page number of the rule and what paragraph. It felt very rude.

I would never deal with this Organization again. No humanity. Just business folks!

PS. don’t bother disputing with your credit card company when they steal your money. Maybe it’s better if you don’t use the autopay, so you have some control of your money and don’t feel robbed like I did. Never again.

I am very sad to say Liberty Health Share has not met my expectations. Yes, I’m pleased with the low monthly cost, but in this case you get what you pay for. I have been diligent about following the rules of how to submit medical bills/claims –including the well woman visit they say they will cover. Well, the appointment was on 11/5/18 and it’s 2/20/19 and I still have not been reimbursed. The labwork that did the standard bloodwork at that appointment is now threatening to put me in collections (which has never happened to me in my life!) b/c of non-payment. I submitted the lab bill as requested so they could negotiate it down so I could pay it. The lab tells me 4 months later-they have NEVER been contacted by Liberty. I call Liberty at least once a week and am told “We are handling this/that and expediting.” Yet, no reimbursement happens and no action on their part is taken. I am fearful what would happen if we ever have a serious medical condition. We are going to switch to another company–as soon as I can get my money out of Liberty. I feel like they just play a waiting game and hope you’ll just give up and accept their non-payment.

the monthly is not low if it is not up to your expectation. I’m so disappointed. The collection process is going to crash my credit rating.

Same problem here. They used to pay all claims quickly, but I had shoulder surgery in November of 2018 and most of the the bills have still not been paid. For some reason, they paid my physical therapy bills very quickly, probably because they were relatively low compared to those for the hospital and surgery. I’ve been on the phone with them several times and it appears they they are way understaffed. I am now getting “final notice” bills for this event and will probably have to pay portions of these out of my pocket so they won’t go to collections and ruin my perfect credit rating. If I had to do this all over again, I would have gone with a different HSM. It pays to read real reviews like this when considering this type of coverage.

I would suggest NOT going with Liberty Health Share. My wife and I have been customers and used them as our Health care providers for 3+ years now and they have gone down hill tremendously. They boasted about having 45 day turn times, and intitially that is actually what was happening. My wife and I were pleasantly surprised to see how great their service actually was.

Recently, however it has been a different story. My wife and I are currently expecting and she is 5 months along. We were so excited and thrilled to have Liberty because of their great maternity healthcare. This is not the case currently. It has been 5 months since we submitted bills to be reimbursed and we have still not received a DIME. $5000+ of medical bills that should be shared and covered completely that we have had to pay out of pocket for that they have not processed.

When asked why it was taking so long, the only answer we have gotten was “We are very busy.” One employee even told us that they were behind on over 100,000 medical bills. 100,000 bills that they had yet to process and could not keep up with. Because of their inability to hire and have their staff process bills in a timely manner, we have had to pay upwards of 5 grand. The best part is that they still sure love taking money from our account every month for coverage we don’t even get the benefit of!

Beware of going with this company, they do not seem to want to appropriately hire the staff to handle their growth and because of this their customers are paying for it.

I am a social worker living in New Mexico. I have had a patient with this insurance, and it has absolutely no mental health benefits at all. Not for counseling, psychiatry, intensive outpatient, or inpatient care.

Thanks for this overview. My wife and I are self-employed (with three boys) and we do not qualify for a subsidy with ACA plans. Needless to say, costs were getting out of hand. We transitioned to Liberty for 2018 and chronicled our experience at our website. We tried to be practical, detailed and factual so others could learn from our experience. We’ve seen some pros but many cons as well. I think it’s important that balanced research is done with all decisions. Hope others gain some benefit from our details.

Hello Dan – I would be most interested in reading about your experience – we are a healthy family of three trying to navigate the process. Can you guide me to your website ?

many thanks

Okay….website????