Liberty HealthShare vs Medi-Share | Which is Best?

Important: At this point there are too many consumer complaints and legal issues surrounding Liberty HealthShare for us to even give them consideration. Point blank, we don’t recommend them.

With the explosion in the cost of health insurance in the past few years, Christian health sharing ministries are becoming increasingly popular.

At the time of this original article, two of the most popular were:

- Liberty HealthShare

- Medi-Share

Which is the better of the two?

It really comes down to your personal circumstances and the specific types of coverage that work best for you and your family.

Historically, Liberty has been better for monthly costs but Medi-Share has been better for lifetime limits (they don’t have one). Philip Taylor, the founder of this website, has used Medi-Share for several years and wholeheartedly recommends it.

But let’s take a look at both ministries side-by-side, analyzing both the cost of each, as well as the individual benefit provisions they offer.

Table of Contents

What Liberty HealthShare and Medi-Share Have in Common

Neither Liberty HealthShare nor Medi-Share plans are traditional health insurance policies in the usual sense.

Instead, each is a faith-based ministry in which members pool their contributions to pay the medical expenses of any participants who have a need.

The concept is actually very close to insurance—but neither is legally considered to be insurance in any sense of the term. Instead, as a ministry member, you’ll make monthly contributions, and have access to funds to cover your medical expenses as needed.

In each case, you’re actually considered to be a self-pay patient. But one who participates in a group shares medical costs.

For the most part, health sharing ministries have been easily accepted by most medical providers. It’s often easier for the providers to receive payment from them than from traditional health insurance plans.

Healthcare sharing ministries also have many of the usual components of traditional health insurance.

For example, they have deductible equivalents, though they’re usually referred to by a different name. Also, they issue their members ID cards for reimbursement purposes, very similar to those provided by health insurance plans.

But let’s take a detailed look at the specific provisions offered by each ministry, as well as the plan costs.

Application Process Comparison: Liberty HealthShare vs Medi-Share

Let’s start by comparing the application process, their associated fees, commitments, and other on-boarding tasks you’ll need to complete.

Liberty HealthShare

You must be healthy, and leading a healthy lifestyle. Also, you must not use tobacco, or abuse alcohol, illegal drugs, or prescription drugs.

And, as is typical with Christian health sharing ministries, you must live your life consistent with biblical principles, as well as participate in worship or prayer.

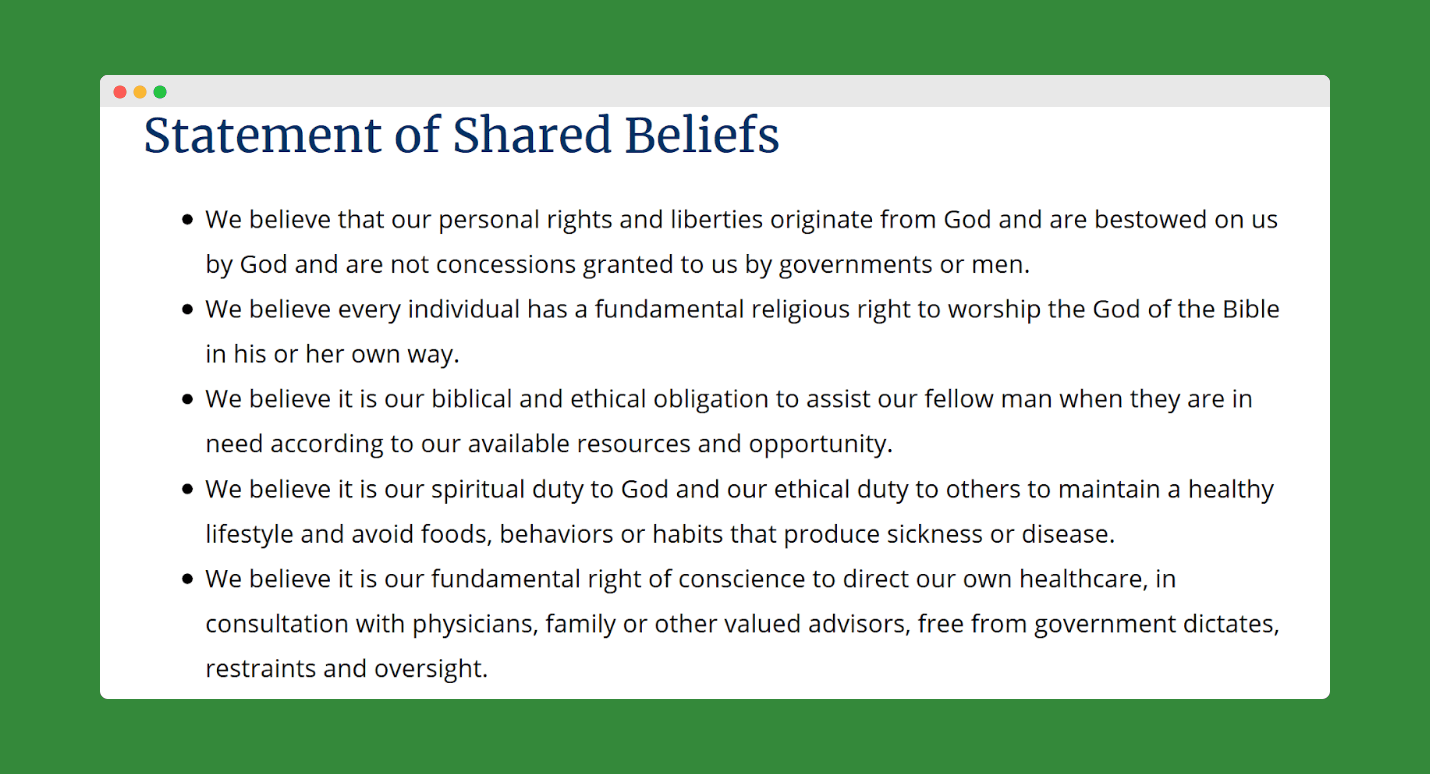

Liberty HealthShare has a Statement of Shared Beliefs that you must agree to:

Liberty HealthCare also has a First Annual Membership Fee of $135, then $75 per annual renewable.

Medi-Share

You apply by phone and must pay a one-time non-refundable application fee of $50.

You’ll also be required to complete three forms:

- Health History Questionnaire

- Testimony & Commitment Form

- Statement of Faith

The Testimony & Commitment Form is a three page PDF, and it’s quite detailed. You’ll be asked your specific denomination and you’ll need to agree or disagree with certain faith positions.

It includes certain technical information you must acknowledge, and you must certify you will not engage in certain non-biblical behaviors, such as sex outside of marriage, use of tobacco, or abuse of alcohol, or legal or illegal drugs.

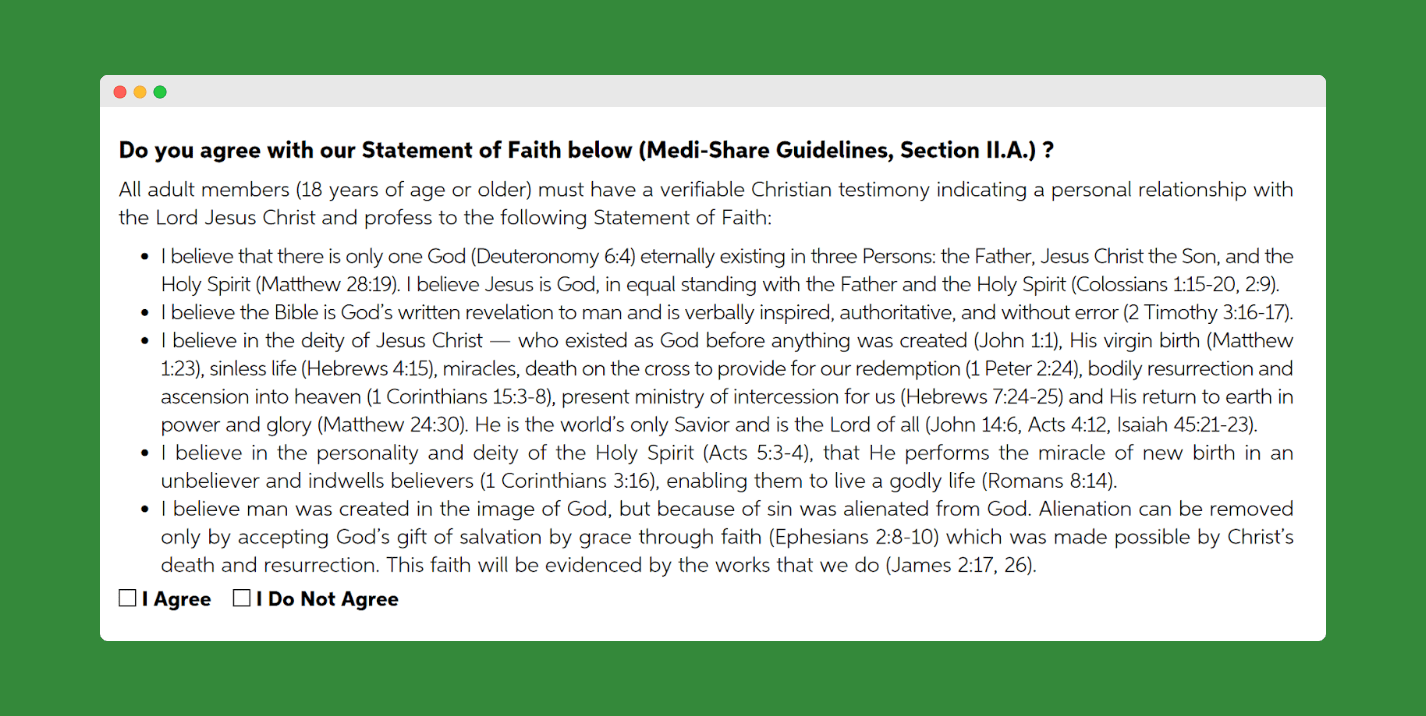

Here is the Statement of Faith (a church leader may be interviewed to verify your testimony):

Once your application is approved, there is a one-time $120 new member fee payable with your first month’s share.

Then, you open a personal sharing account, which will require a $2 one-time membership fee for setting up the account. The purpose of the account is to facilitate the transfer of funds between the member sharing accounts and to deduct program fees.

Winner: Liberty HealthShare, with what appears to be a simpler application process and fewer restrictions.

You can check out our full review of Liberty HealthShare here.

Health Sharing Program Details: Liberty HealthShare vs Medi-Share

Let’s take a closer head-to-head look at Liberty HealthShare and Medi-Share program details.

Below, we cover the nitty-gritty line items of each healthcare sharing ministry, what they cover, and what they don’t.

Deductible Equivalents

- Liberty HealthShare refers to these as the “unshared amount” (unshared by the group—you pay this yourself). They have three different unshared amounts on their plans (single, couple, family, respectively):

- $1,000

- $1,750

- $2,250

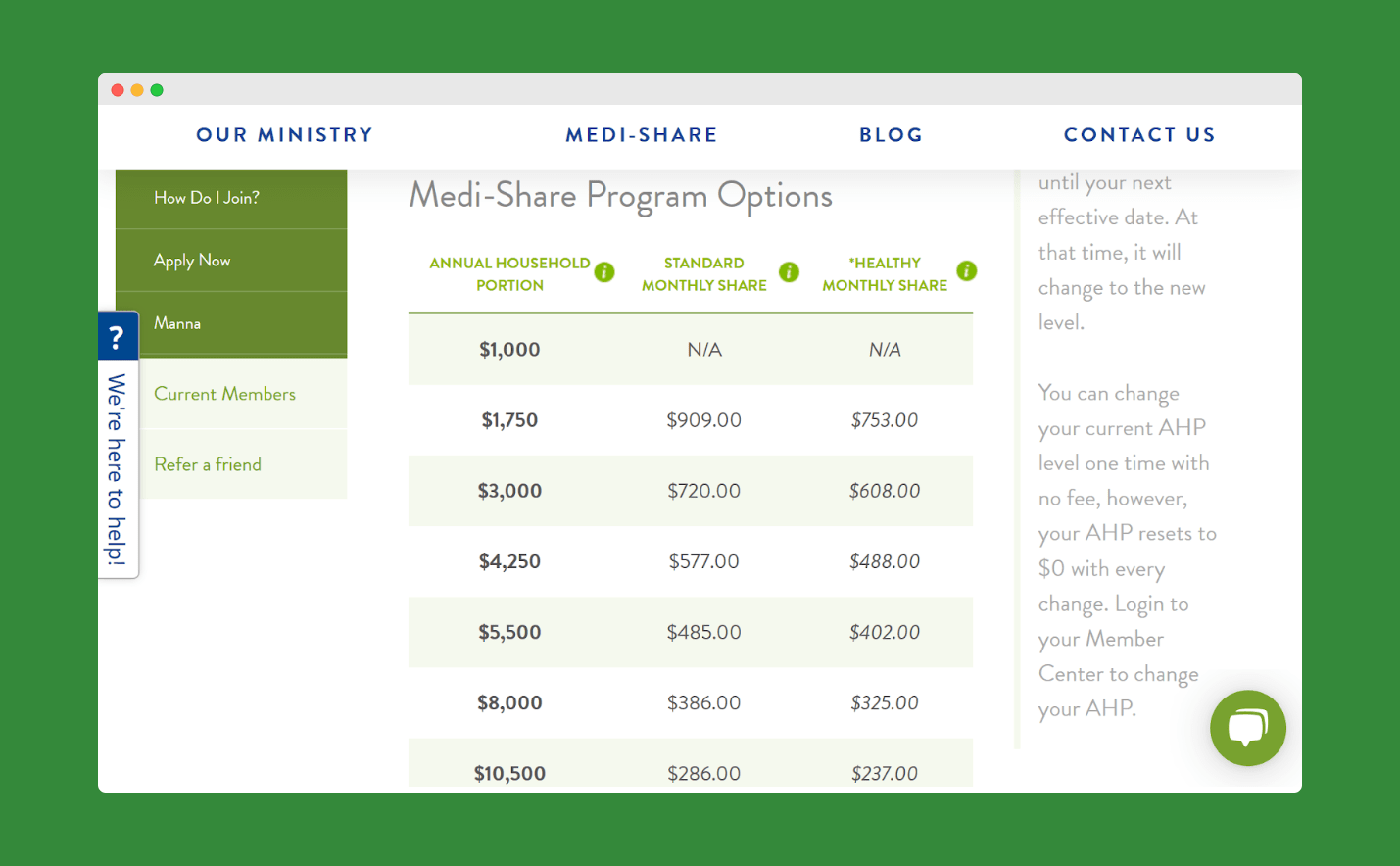

- Medi-Share refers to deductible equivalents as “annual household portion” (AHP). They have seven amounts:

- $1,000 (available only to unmarried individuals, 18-29 years old)

- $1,750

- $3,000

- $4,250

- $5,500

- $8,000

- $10,500

Winner: Medi-Share, due to the larger number of deductible equivalent options.

You can check out our full review of Medi-Share here.

Healthy Incentives

- Liberty HealthShare. Not offered.

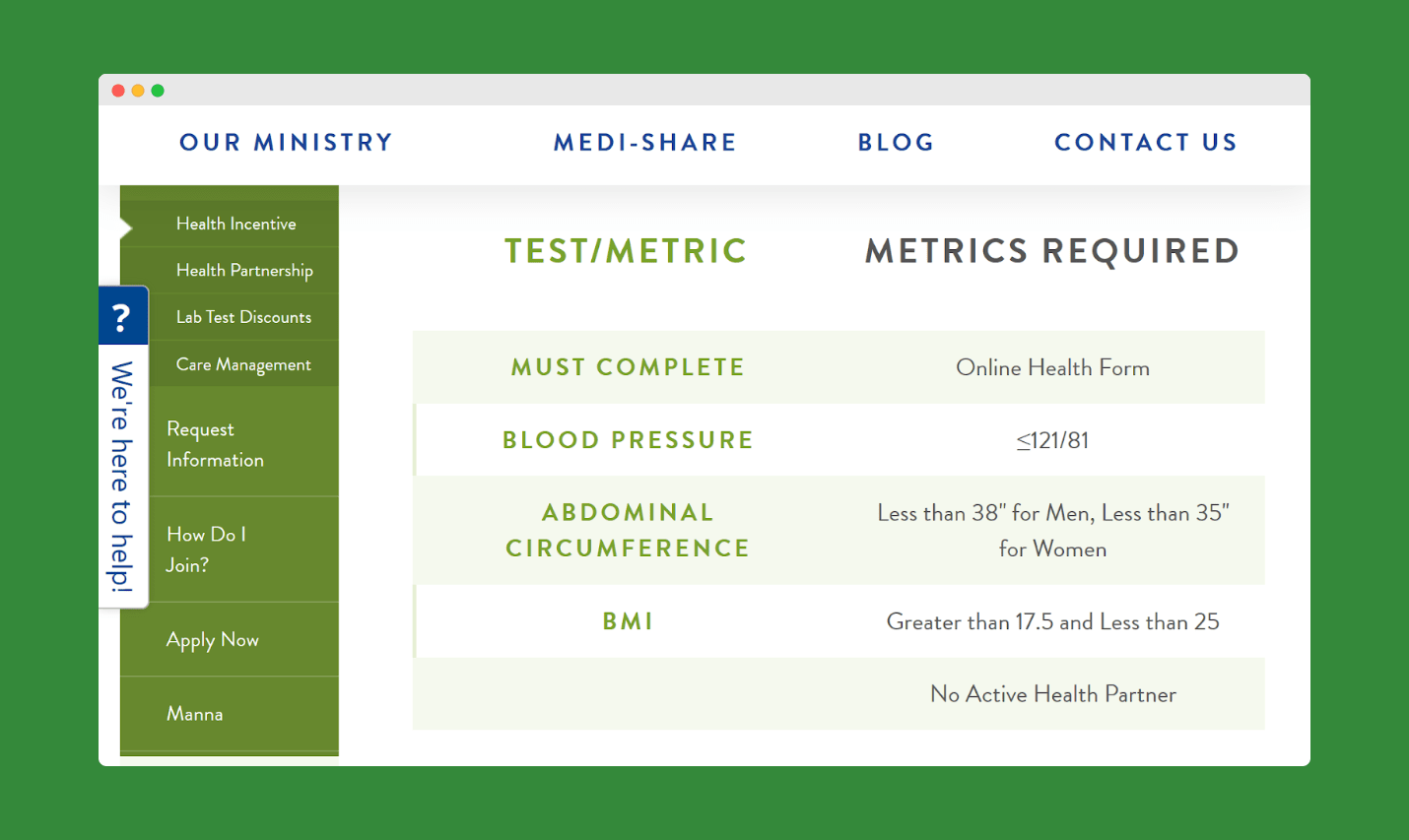

- Medi-Share offers a 20% reduction in your monthly share amount for households who meet their Healthy Incentives standards.

- If you qualify, a $1,000 monthly share could be reduced to $800.

- A $500 monthly share could be reduced to $400. To qualify, you’ll have to meet the following standards:

Winner: Medi-Share, since Liberty HealthShare has no incentives to reduce monthly shares.

Health Partners

- Liberty HealthShare. For pre-existing conditions, Liberty HealthShare requires members to be enrolled in their HealhTrac program. It’s designed to help members improve their health conditions, particularly diabetes, hypertension, heart disease, high cholesterol, obesity, and tobacco use.

- Members are assigned a health coach, who works with them to develop a personal plan to improve their condition. This includes setting goals, providing tools and resources, and diet recommendations.

- There is an additional fee of $80 per month for participation in this program. Once the member’s goals have been met, the fee is eliminated.

- Medi-Share. If you’re judged to be at higher risk for disease, you may be required to become a Health Partner. That will give you access to unique online healthcare content and personalized telephone-based coaching.

- Through the plan, you’ll develop a personal plan for achieving health goals.

- An additional monthly fee is added to your monthly share if this is necessary.

Winner: Tie.

Age 65 and Over

- Liberty HealthShare. Members 65 and over are eligible for participation in each of Liberty HealthShare’s three plans, though at a somewhat higher monthly contribution rate. Do not offer a Medicare supplement equivalent plan.

- Medi-Share. Applicants 65 and older are not eligible for regular Medi-Share. However, they are eligible for Senior Assist, which works with Medicare part A & B.

- Senior Assist is similar to a Medicare supplement, covering bills that Medicare allows, but does not completely pay. These include copayments, deductibles, hospitalization, skilled nursing facility care, and out-of-country urgent care

- Senior Assist has a deductible equivalent of $1,250 per person, with monthly shares as follows:

- 65 – 70 years old, $70

- 71 – 75 years old, $85

- 76 or older, $95

- Senior Assist has no sharing limitations on pre-existing conditions, and your membership cannot be terminated due to medical reasons.

Winner: Liberty HealthShare if you don’t qualify for Medicare; Medi-Share if you do. So let’s say Medi-Share since most people over 65 do qualify for Medicare.

Pre-certification

- Liberty HealthShare. The ministry describes it as “limited pre-certification,” but it looks to be comparable to other health plans.

- Members must provide a pre-notification so they can be advised how to avoid unnecessary services, hospitalizations, short and in-patient confinements, and also improved quality of care and reducing expenses shared by members.

- This requirement applies only to non-emergency medical procedures. Although emergency procedures must be reported within 48 hours of admission.

- Medi-Share. Members must direct their providers to notify Medi-Share before undergoing in-patient hospitalizations, non-emergency surgeries, elective cardiac procedures, cancer treatment, or organ tissue transplant services.

Winner: Tie.

Financial Hardship

- Liberty HealthShare. Not indicated.

- Medi-Share. Monthly Shares may be waved for up to three months per 12 month period if the member’s illness or injury causes loss of income.

Winner: Medi-Share.

Maternity or Adoption

- Liberty HealthShare. Covered up to per-incident limits, as long as the mother has been a ministry member prior to conception.

- Medi-Share. These services are eligible for sharing up to $125,000. However, they are not covered if you have a deductible equivalent of less than $2,500. You also need to be faithfully sharing from conception until delivery.

Winner: Liberty HealthShare, since they don’t put any limits on coverage or deductible equivalents.

Maximum Sharing Limits (Benefits)

- Liberty HealthShare. There are no lifetime benefit limits with any of Liberty Healthshare’s plans. The maximum annual benefits for each of their plans are:

- $1 million per incident: Liberty Complete

- $125,000 per incident: Liberty Plus

- 70% of eligible medical expenses, up to $125,000 per incident: Liberty Share.

- Medi-Share. There are no annual or lifetime limits.

Winner: Medi-Share, since they have no limits whatsoever.

Co-payments

- Liberty HealthShare. None indicated.

- Medi-Share. $35 per doctor visit, and $200 for emergency room visits.

Winner: Liberty HealthShare, since no copayments are required once you meet the deductible equivalent.

Preferred Provider Organization (PPO)/Network

- Liberty HealthShare. Offer a provider network, listing more than 23,000 preferred providers nationwide. However, Liberty HealthShare does not require you to use those providers, and there is no reduction in benefits if you don’t.

- Medi-Share does make use of PPO providers whenever possible. These are providers who have agreed to discount their fees for plan members. If you use a non-PPO hospital or other facility, you will have an additional responsibility of either 20% of the total charges, or $500 per eligible bill, whichever is less. However, the non-PPO requirement may be waived if there is a life-threatening emergency.

Winner: Liberty HealthShare, since there’s no penalty for going outside the PPO.

Prescriptions

- Liberty HealthShare covers Tier 4 prescriptions used for acute illness for the 45 days following each related medical incident. Tier 1, 2 and 3 prescriptions are not covered. However, Liberty HealthShares provides members with a SavNet Prescription Drug Plan discount card, offering reduced rates on prescriptions at major pharmacy chains, as well as other retail pharmacies.

- Medi-Share. Covers drugs prescribed by a doctor, dentist, optometrist, nurse practitioner, physician’s assistant, midwife, or certain other professionals for up to six months.

Winner: Medi-Share for covering meds up to six months, rather than 45 days. They also seem to cover more types of prescriptions.

Pre-existing Conditions

- Liberty HealthShare. Excluded for the first 12 months you’re enrolled in the plan. In months 13 through 36, Liberty Healthshare limits coverage to $50,000 per year.

- After 36 months, pre-existing conditions are fully covered.

- For pre-existing conditions, Liberty HealthShare also requires members to be enrolled in their HealthTrac program, which is described above.

- Medi-Share. They define these as signs, symptoms, diagnosis, treatment, or medication for a condition prior to membership. Cover these medical costs up to certain limits:

- Up to $100,000 per year, if the member has been in the plan for 36 consecutive months, or the medical records state the diagnosis or condition has gone 36 consecutive months without signs, symptoms, treatment or medication.

- Up to $500,000 per year, if the member has been in the plan for 60 consecutive months, or the medical records state that the diagnosis or condition has gone 60 consecutive months without signs, symptoms, treatment, or medication.

- They don’t consider high blood pressure or cholesterol that’s controlled through medication or lifestyle as a pre-existing condition.

Winner: Liberty HealthShares, since they offer some benefits in months 13 through 36, and unrestricted thereafter.

Routine and Preventative Care

- Liberty HealthShare. Covered, subject to annual deductible equivalents.

- Medi-Share. Physicals, immunizations and vaccinations, lab studies, screening mammograms, screening colonoscopies, and vision and dental services are not eligible for sharing. However, routine well-child care is eligible until the child reaches the age of six.

Winner: Liberty HealthShare, since Medi-Share specifically excludes routine and preventative care services.

Final Expenses

- Liberty HealthShare. Pays up to $10,000 per primary applicant, $5,000 per dependent spouse, and $3,000 per dependent child (to age 26).

- Medi-Share. Members are eligible to receive up to $5,000 for final expenses upon death. The benefit extends to stillborn children.

Winner: Liberty HealthShare, with higher benefits.

Related: Christian Healthcare Ministries Review: Save Thousands Per Year on Healthcare

Dental, Vision, and Hearing

- Liberty HealthShare. These services are not eligible for sharing. But members are given access to the SavNet Health Savings Program which provides discounts for these services.

- Medi-Share. These services are not eligible for sharing. Medi-Share does give members savings cards that provide discounts for each service.

Winner: Tie since neither allows their members to share dental, vision, and hearing but both help their members save money on these services.

Chiropractic Care

- Liberty HealthShare. Up to 12 chiropractic visits are eligible for sharing per membership year. Members can also access discounts on chiropractic care through Liberty Healthshare’s partnership with SavNet.

- Medi-Share. Limit chiropractic care sharing to cases that have been diagnosed by a licensed physician (M.D. or D.O). When approved, up to 20 visits are eligible for sharing within a six week period.

Winner: Liberty Healthshare since they don’t require an M.D. or D.O diagnosis and also give members access to in-network discounts.

Ancillary Therapies (Physical Therapy, Speech Therapy, Occupational Therapy, Respiratory

Therapy)

- Liberty HealthShare. Up to 12 visits for each type of therapy, with the possibility of an additional 8 visits after reassessment for a total of 20 visits.

- Medi-Share. Up to 20 visits combined for Physical Therapy (PT), Occupational Therapy (OT), and Osteopathic Manipulation Therapy (OMT). Up to 10 visits per referral for outpatient speech therapy.

Winner: Liberty Healthshare, since you get up to 12 visits for each type of therapy.

Mental Health

- Liberty HealthShare. Not eligible for sharing

- Medi-Share. Counseling and therapy are not eligible for sharing, but psychiatric evaluations may be eligible for sharing

Winner: Medi-Share, since testing may be eligible for sharing.

Liberty HealthShare vs Medi-Share—Head-to-Head Comparison

We ran the numbers for both plans, based on a family of four, in which the oldest person in the household is 40. And here were the results under both plans.

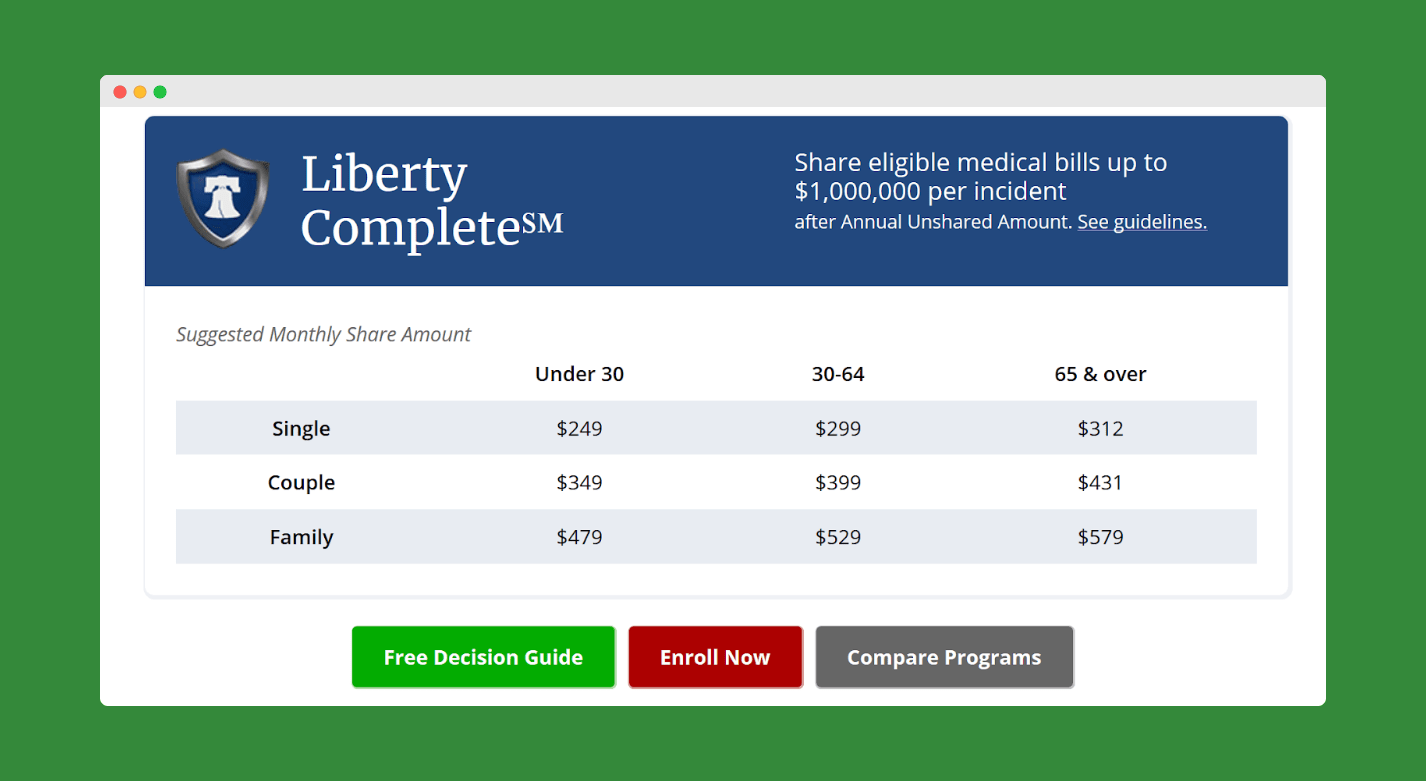

Liberty Complete

This is Liberty HealthShare’s most popular plan. It covers eligible medical costs up to $1 million per incident. And it provides the entire range of medical and pharmacy discount services.

The annual unshared amount (deductible equivalent) is $1,000 for an individual policy, $1,750 for a couple, and $2,250 for a family.

For a family of four, where the eldest member is 40, the cost of coverage is $529 per month, with a $2,250 deductible equivalent.

Medi-Share

Medi-Share doesn’t have specific programs the way Liberty HealthShare does.

Instead, you input your information, and they provide you with the table that describes the program options available. And within each, you have the option to select one of the seven deductible equivalents, in exchange for a different premium.

Also, Medi-Share gives you the option for the Healthy Share price reduction (the 20% monthly share reduction), if you qualify.

In this comparison, Liberty HealthShare comes out as the less expensive option. The family will pay a monthly amount of $529, with a $2,250 deductible equivalent.

The closest Medi-Share comes is the deductible equivalent of $1,750, with a monthly share of $909. To get close to the monthly shares paid, select the Medi-Share’s $5,500 deductible equivalent and get a monthly share payment of $485.

In a head-to-head comparison, you’ll either have to accept a higher monthly share, or a much higher deductible equivalent with the Medi-Share plan.

Which Should You Choose—Liberty HealthShare or Medi-Share?

When it comes to health care plans of any type, it’s generally not possible to say one plan is categorically better than another. Liberty HealthShare is clearly the less expensive of the two, based on monthly share amounts.

But Medi-Share is superior in important categories, like lifetime benefit limits (they have none). Next to cost, it might come down to the details of each plan.

For example, if you have a pre-existing condition, Liberty HealthShare is the better choice, since benefits will apply earlier. If you need prescriptions, Medi-Share looks like the better plan.

But if we have to declare a winner, on balance it looks like Liberty HealthShare. The lower cost, in combination with their being the winner in more categories, tilts the decision slightly in their favor.

Important Editor’s Note: It’s clear at this point that given the large number of customer complaints and legal issues that Liberty HealthShare is experiencing, they are not this winner of this comparison. If you can’t trust a company to do what they say or to exist within the confines of the law, it doesn’t matter how cheap they are.

If you’re considering Christian healthcare ministries, take a close look at the details of each program. What may be the better choice for someone else may not be the best for you.

Do you have any experience with either Liberty HealthShare or Medi-Share?

Want to compare more healthshare plans? Check out our list of the best healthshare plans available today.

![Save Money on Healthcare Without Using Obamacare [Our 2019 Liberty HealthShare Review]](https://ptmoney.com/wp-content/uploads/2018/11/Liberty-screenshot-2-768x383.png)

![Buy the Best Life Insurance in 7 Easy Steps [The Ultimate Guide]](https://ptmoney.com/wp-content/uploads/2019/02/Buy-the-Best-Life-Insurance-in-7-Easy-Steps-The-Ultimate-Guide.png)

I am also getting very frustrated with Liberty, it takes far to long to get claims paid, I’m fortunate that I’m able to get by financially , I feel for those families that are on a tight budget and are counting on the reimbursement, Liberty really needs to get their act together or their days are numbered.

I just thought you might want to check out Mr. Money Mustache’s new article about DPCs and Sedera Health. We switched to Sedera over a year ago (after going through hell w/Liberty, plus never liking the religious part – Sedera is secular) and it’s been night and day better! They paid out on my wife’s recent specialist visit – less than a month between treatment and the reimbursement check!

Thanks, Miles. I’ll check that out!

well gee…i thought “Liberty sounds great,” then I read all the negative comments and followed up on their BBB rating. I hate to say it, but it sounds like someone is about to run off with a lot of peoples money. Or they simply don’t have any to pay bills. Scary. Not sure who to choose now. Need coverage for 6 for basically emergencies.

Last year my doctor told me I needed carpal tunnel surgery before I permanently lost feeling in my hand. I called Liberty and got preapproval to have the procedure for a fixed cost. A week later I had the surgery. That was 10 months ago. Liberty ignores my emails, so I’ve spent endless hours on the phone with them – to no avail. Every Customer Service Agent I talk to admits Liberty owes me the money, but they can’t do anything. I decided to bypass the telephone agents by sending queries through the mail to specific managers. They returned the first 2 letters, marked “Addressee Unknown”, so I sent one Registered Mail. They signed for it, but never answered to it either. The telephone agents will apologize all day long, but they’ll never pay your claims.

Do not give Liberty your money. THEY ARE A SCAM! THEY WILL TAKE YOUR MONTHLY DUES BUT THEY WILL NOT PAY YOUR CLAIMS! I’ve already launched fraud complaints with the Ohio Attorney General. Check the Better Business Bureau and you’ll see the situation at Liberty had been bad and is getting worse. The pattern of malfeasance and complaints are accelerating.

Same problem. Have had submitted bills to Liberty for 7 months nearly $9000 out of pocket. Now I’m afraid to go to a doctor because they’ll make me pay up front and I’ll never get payed from Liberty.

Same here. At least they paid the first half of my knee replacement surgery. I’m on a payment plan for the rest – physician, hospital, anesthesiologist, physical therapy – but the interesting part is that my payments to these people, along with my family’s monthly share amount, is still less than the basic insurance I was offered through my company. So disheartening….

My wife and I have been with Liberty for about two years. We are considering going elsewhere however since Liberty is having problems paying members submitted medical expenses. One of our bills Liberty tells us they are paying is from February 2018! The status says it is ready to pay and has a check number assigned, but that’s the way it’s been for at least 2 weeks. I am surprised the provider has not sent us to collections by now. Fortunately,

they ARE a faith based healthcare provider.

Liberty has no problem taking our monthly share amount though. I could not in good conscience recommend Liberty Healthshare at this time anyway.

Same here 🙁 I thought it would get better after 4 years. Nope.

We have been with Liberty for several years. Sounds good on paper…good luck getting your claims submitted and then paid. I have one for a wellness visit that is over a year old…Horrible customer service and long wait times on the phone trying to get things straightened out. Their representatives are not always truthful, disappointing in that they claim to be a christian organization. Just filed my second complaint with the BBB.

Neither program is actuarially sound when it comes to pricing. Both are selecting the healthiest risk via tight underwriting and applying strict pre-existing condition limitations. As long as membership continues to grow and they keep adding new business, they will do fine. The problem is they cannot grow forever and 2019 may be a turning point in that membership in both programs may likely decline ( due o elimination of ACA mandate). Both programs are headed for what actuaries call a ‘rate spiral’ as underwriting wears off and the underlying morbidity gravitates toward the mean….As far as Medishare deductible goes, one ought to buy the highest deductible available; the lower deductible pricing makes no sense.

PS. I was in Medishare but have been in Liberty for last 3 years

We have MediShare but since our Daughter is turning 23 (full time student) we have to purchas a separate policy for her – so the costs are getting too high..how do you like Liberty? What has your experience been?

We have been with Liberty for several years. Sounds good on paper…good luck getting your claims submitted and then paid. I have one for a wellness visit that is over a year old…Horrible customer service and long wait times on the phone trying to get things straightened out. Their representatives are not always truthful, disappointing in that they claim to be a christian organization. Just filed my second complaint with the BBB.

You can check out other complaints on the BBBs website as well.

Yes this is exactly our experience. We even had one bill go to a collections agency. That is not how we operate!!!!! I am looking into other options.

Outstanding post! As someone that’s going to be moving to one of these plans soon, you just did a whole bunch of research for me Kevin!

Thank you!