Improve Your Credit Score with Our Ultimate Guide to Credit

This post is brought to you by Experian. While this was a sponsored opportunity, all content and opinions expressed here are my own.

Have you ever wondered exactly what it takes to build a good credit score? Maybe you’ve made some credit mistakes in your past and you’re wondering how to fix them. Or perhaps you’ve wondered if your credit score even really matters. No matter what questions you have about credit, you’re sure to find the answers in this guide brought to you by Experian.

Your credit score is a 3-digit number that helps reflect your creditworthiness. FICO® and VantageScore® are the two most popular credit scoring models. They both base your score on the credit report data provided by the three major credit bureaus–Transunion, Equifax, and Experian. You can improve your credit score by paying attention to the factors that make up your credit score: payment history, amounts owed, length of credit history, types of credit, and new credit inquiries.

In this guide, we’ll give you credit-building tips, discuss how to fix credit errors, and talk about ways to protect yourself from identity theft.

But first, let’s discuss why your credit score even matters in the first place.

Table of Contents

- Why Your Credit Matters

- What is a Good Credit Score?

- Get Started Building Your Credit

- Steps to Improve Your Credit Score

- Experian Boost™

- Experian Credit Educator Session

- Common Credit Report Errors

- How to Fix Errors and Identity Theft

- Getting Help to Fix Your Credit

- Help Your Kids Get Started with Credit

- Common Questions

Why Your Credit Matters

There are people in your life who have a bias against you and your poor credit.

The mistakes that you have made with debt will put blemishes on your credit report and lower your credit score. But those mistakes also let people in your life hold your bad credit over your head in some way.

A bad credit score or report can reach much farther than simply costing you a higher interest rate on a new loan. It can cost you the apartment you live in or even your job.

It does not have to be that way. You can recover.

While it may take awhile to raise your credit score and improve your report, you can begin to quickly ease the damage you have done with a few simple ideas.

Below are the five entities that can access your credit score or report (and potentially use that against you), and what you can do right now to help set the record straight and mend some bridges.

Car Insurance Companies Can Use Your Credit Score Against You

Many people are not aware that car insurance companies use your credit score in their formulas when they determine your auto insurance premium.

There are a host of factors that go into the car insurance company’s proprietary calculations, and your credit score is one of them.

Car insurance actuaries have found that folks with a lower credit score are more likely to file claims. That’s why a poor credit score will cost you a higher car insurance premium.

Potential Fix: Shop around for your next car insurance quote. Far too many people simply continue using the same car insurance company they have used for years without discovering if a better rate is out there.

Your Future Landlord Will Ping Your Credit Score

One of the first pieces of information on rental applications for an apartment or a house is your Social Security number.

Oftentimes, a rental application for a new apartment is immediately followed by another form that allows the landlord access to your credit report and credit score. For this reason, if you’re planning to rent soon, you may want to check your credit score for free with Experian.

Potential Fix: One thing that you can do to help alleviate your future landlord’s concern about your low credit score may be to offer to pay a higher security deposit. While we all hate the idea of volunteering to pay more, this may be the icing on the cake you need to sway the landlord to rent to you.

Some Employers Look at Your Credit Report

Many employers request your permission to look at your credit report before they hire you. This can especially be true for government employees.

For example, members of the military have their credit report examined before they are granted any type of security clearance.

Potential Fix: As in all cases, you should be honest and upfront with your employer, or future employer, about your troubles with debt or issues that you have had in the past. If you bring it up first, before your employer pulls your credit report, you can ease some of the tension.

Are You Being Truthful with Your Spouse or Significant Other?

When I was dating my wife, I found out the hard way just how dangerous hiding debt and financial problems can be to your relationship with your spouse or significant other.

I was ashamed about the amount of credit card debt I had accumulated during college. I didn’t want to share the information with her, and it hurt our relationship in the beginning.

It actually took her years before she stopped worrying about creditors calling the house, bouncing checks, and the like because of the poor initial interactions we had together about my credit.

Potential Fixes: Be upfront with your significant other about your spending and finances. Bad news never gets better with age, so don’t wait too long before you spill the beans about your financial past and mistakes. Then show your loved one that you have a plan to stop racking up debt or to fix issues in your credit report.

You will one day want to buy a house, and you will want to be able to title it jointly or not have to worry about depending solely on your spouse’s credit score to help you earn a lower interest rate.

Even Utility and Cell Phone Companies Use Customers’ Credit Scores

Like your landlord, most utility companies, cable companies, cell phone providers, and even oil delivery companies will pull your credit report and your credit score before they let you sign a contract with them.

As with most purchases, having a lower credit score will cost you either in higher fees and/or interest rates.

Potential Fix: Utility and cell phone companies are another great example of companies where you may be able to ask for a larger than normal security deposit to ease their concerns. You may also be able to ask for a probationary period of time that you can use to not only build your credibility with the vendor but also help to rebuild your credit score.

What is a Good Credit Score?

I was talking with a friend the other day and they mentioned that they thought they had a really good credit score.

What number pops into your head when you hear that? 750? 825?

I really didn’t have a specific number. I guess something in the high 700s was what I thought of. But is that “really good”?

A credit score is a numerical representation of what’s in your credit report. The FICO® credit score is the most widely accepted credit scoring model. In the United States, FICO scores range from 300-850, with 723 being the median FICO score of Americans.

With that, I think you could assume that above 723 would be a good score and above 780 would be really good. If you’re over 800, you shouldn’t have to worry about your score. In fact, most lenders view a FICO score of 700 or above as “good”.

There is no consensus on what defines “really good” when it comes to credit scoring.

Get Started Building Your Credit

Shortly after college was the first time I think I ever thought about my score. I headed out to buy a new car and was told I didn’t have great credit. I didn’t know really what that meant or how it could be changed, but I did see that my interest rate was ridiculously high.

Fast forward several years later and I’ve now improved my score. I’ve also now learned quite a bit about what makes up a score and how to raise my credit score. Armed with that knowledge and with a little help from the National Foundation for Credit Counseling (NFCC), I’m prepared to give anyone new to this some information about building credit right out of the gate.

1. Carefully Apply for Credit

Applying for too much credit can actually harm your credit score. It’s tempting when you get your first job to run out and put a bunch of things on credit. After all, you have this new income to support payments you’ll need to make.

My best advice is to slow down and do your research to find the best loans to be associated with. Particularly with credit cards, do some research and find a card that is going to suit your needs. You don’t want to be applying for a new card every month because the one you have isn’t working out.

2. Use Credit Wisely

Next, and likely most important, become a responsible borrower. Always pay on time. You really can’t afford a late payment on your record right now (or ever). Also, try and pay your balances off each month.

At a minimum, keep your balances below 30% of your overall available credit. Lastly, try and develop a diverse set of credit types on your file. The NFCC recommends at least three different loans in your credit file.

Lenders like to see that you are capable of handling the different types of credit: revolving (credit cards) and installment (personal loan, car loan, mortgage, etc.)

3. Find a Co-Signer or Go Secured

If you are having trouble getting a loan or a credit card initially, consider wearing the credit crutches for a little while. Getting a co-signer or a secured credit card are two common methods for building credit history when credit isn’t freely available to you.

You could also look into a builder loan from a credit union or from a company like Self Credit Builder Loans (formerly Self Lender). Look at this as a temporary move to help you get over that first hurdle. I’ve seen reports that it takes about a year to move from a secured card to an unsecured one.

Check out our full review of Self Lender here.

Steps to Improve Your Credit Score

A recent Citi survey found that over half of all Americans have admitted that they have paid a bill late at some point in their lifetime. And, over 80% of that survey’s respondents made a late payment within the last 12 months. If you need to rebuild your credit, you are not alone.

1. Pay Your Bills on Time

Paying your bills on time is the biggest factor that the credit scoring models use when it comes to determining your credit score. And rightfully so. Most lenders are most concerned with whether you’ll pay them back on time. It’s important not to miss any payments if you want to have a good credit score.

If you’ve shown a good track record with this in the past, then you’ll be trusted in the future.

Also, review your free credit report and ensure you don’t have payments that were incorrectly reported as late. A late payment on an account that isn’t yours shouldn’t be on your report. Be sure to dispute any errors you find on your credit reports. Here’s some more information on how to do that.

If your late payments are legit, then there’s nothing you can do but try and make good payments going forward and work on the other areas.

2. Keep New Credit Requests to a Minimum

Requesting new credit often can lower your credit score. Apparently, the lenders see it as a sign that you’re desperate for cash if you’re always requesting new credit.

Keep requests to a minimum if you’re planning on needing your credit score soon. Also, review your credit report and look for any “hard” inquiries that have been made on your file. If you don’t recognize an inquiry, check with the creditor listed to see what the inquiry was for. If you still don’t recall applying for credit with that creditor and are worried you may be a victim of fraud, contact the credit bureaus.

3. Grow Your Credit History

Easier said than done, right? This is obviously the biggest hurdle for most people starting out.

The longer your history with credit, the more comfortable lenders are with relying on that history to determine credit-worthiness.

You can help your credit history by not canceling old credit cards. Even if you pay off a credit card completely, cut it up and plan to never use it again, but don’t close the account.

The history and available balance are actually helping your credit score. Don’t forget you can get a free credit report on Experian.com if you want to see which accounts are currently being reported.

If you’re a business owner, you may be wondering how to build business credit. Nav.com can assist you in that since they provide free personal and business credit score updates. They also offer thoroughly researched advice on the best financing options for your business. You can build your business credit score through the various services Nav has to offer. Learn more about Nav here.

4. Keep Your Credit Balances Low

It’s recommended that you keep the amount that you borrow at or below 30% of your available balance. In simple terms, if you have a $1,000 credit limit on your credit card, you need to only ever show a balance of $300. You can read more about credit utilization here.

This should apply to all your revolving accounts. Consider using a 0% balance transfer credit card to move your credit usage around, if necessary.

5. Use Revolving and Installment Debt

The key here is to have a decent mix of both revolving (credit cards and lines of credit) and installment (mortgage, car loans) type credit.

I was once told I didn’t get the best interest rate on a deal because I didn’t have a mortgage (limited installment credit history). At the time I wasn’t ready to buy a house. So I just had to take the best they would give me.

However, if you don’t have a credit card, you may want to consider getting one to help your credit score. I don’t recommend you go into debt.

The most beneficial way to use the card would be to use it for a recurring monthly bill (e.g. your electric bill) and then immediately pay off the balance.

In closing, I think it’s good to remember that your credit score isn’t everything. Don’t obsess over achieving the perfect credit score. It’s not going to kill you to have a 740 versus a 760.

But it doesn’t hurt to be aware of the factors that make up your score. And with that knowledge, you can slowly start to improve your score over time.

Experian Boost™

Experian says that some 62 million people have a “thin credit file.” This means that they have very few if any credit accounts listed on their credit report.

If you’re young and new to credit or you haven’t used credit in a long time, you may have a thin credit file. To be clear, thin credit is better than bad credit. But you still may have a hard time being approved for a loan or mortgage.

However, if you’re living on your own, you’re probably paying lots of bills every month, like your phone and electric bill. Why shouldn’t you get credit for that? Experian thinks you should and they’ve introduced a new product called Experian Boost that’s intended to do just that.

How Experian Boost™ Works

Here’s how Experian Boost™ could increase your FICO® score instantly, for free.

You simply give Experian access to your banking account history and permission to add your utility and phone bill payments to your credit file. That’s it! Experian says you’ll see your boost results instantly.

If you have missed utility or phone payments, don’t worry. Experian says that they will only add positive payments to your credit file. In a recent study, Experian found that 90% of thin file users raised their FICO® score, with an average max boost of 13+ points.

If your credit score could use a boost check out this free service.

Experian Boost™ Disclosures: Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost.

The Surprising Results of My Experian Credit Educator Session

Back when VantageScore® used a scoring model that went up to 900, I was able to fairly quickly raise my score from 834 to 865. Follow along to see how.

I’m not big on obsessing about one’s credit score. You shouldn’t be either. But if a few small changes can have a significant impact on your score, then I don’t see the harm in taking a stab at making those changes.

After all, I do plan on doing some more real estate investing and credit card bonuses in the next couple of years. Having a solid score means I get the lowest interest rates and qualify for bigger limits.

The problem is that it’s hard to know exactly what changes you can make that will have the biggest impacts. Above, I’ve instructed you to look to the five key factors that make up a credit score to determine what to fix. That’s still solid advice, generally speaking.

Recently, however, I discovered a service from Experian that sheds, in my opinion, significantly more light onto what you can do to improve your score.

Experian Credit Educator Session

The service is called Experian Credit Educator. It’s been around for a few years, but it was recently improved.

It involves a 35-minute phone consultation with a representative with Experian. In this consultation, you review your credit report, VantageScore®, and specific things you can do to potentially improve your score.

You also run through different scenarios to test the impact on your score. Cool, right?

The service costs $39.95, but I was able to get a freebie to check it out for a potential review. The results of the session were surprising and that’s why I’m sharing this post with you today.

Below, I share what I learned in the consultation.

The Experian Credit Report

I’m already familiar with the credit report format and individual components. You’ve got your personal information, accounts, credit inquiries, and bad items (bankruptcy, etc). But it was nice to review it with someone else just to be sure I understood it all.

I did learn that negative items can stay on your report for 7-10 years. And positive items can remain on your report for 10 years after you close the account.

I had one negative item on my report: a 30-day late payment. I also had a few credit inquiries. I learned that these drop off the report after two years.

My score turned out to be 834. I was told this was roughly a B on a grading scale, and higher than 72% of U.S. consumers. Definitely room for improvement.

Key Factors Affecting My Score

This is where the consult starts to get interesting. I was shown the exact factors that were affecting my score. Here’s what they were:

- The amount paid on my open real estate accounts is too low.

- The balances on my open accounts are too high in comparison to their credit limits.

- The available credit on my open revolving credit accounts is too low.

- I have too many inquiries on my credit report.

My mortgages are affecting my score? I never would have imagined this. We put 20% on both our rental property and our home mortgages. Why is the amount paid too low?

Well, it turns out, Experian looks at the initial loan amount vs. the current balance. We may have been better off not putting down 20% and then using that 20% to instantly pay down the mortgage.

Bizarro World, right?

Taking Action

So, based on these factors, here are my action steps.

- Pay down some of my mortgages (around $7,500 on my rental property–see below).

- Ask my credit card issuers for higher limits and hold off on applying for new credit till one inquiry drops off.

Here’s where the consultation gets really interesting. I was able to then test different scenarios to see how that might potentially affect my score.

- Scenario 1: Pay $10,000 towards my debt. The simulator applied $7,629 to my rental property mortgage and the rest to my home loan. This took my score from 834 to 865.

- Scenario 2: Pay $20,000 towards my debt. The simulator applied $7,629 to my rental property mortgage and the rest to my home loan. This took my score from 834 to 869. Not much more of a change, and you can see the culprit–our rental property loan.

- Scenario 3: Aim for a 900 credit score. To achieve this score I would have to pay over $100k off my loans. Not something practical.

As you can see, the scenarios were helpful in determining the amount of payment that is needed to really move the needle on my score. This gives us just one more reason to start doing some work on paying down our real estate debt.

Common Credit Report Errors

When you start looking at credit report error statistics it’s easy to quickly get frustrated.

There’s a ton that could and that does go wrong with the reporting of your credit information. Did you know that studies have shown that as much as 79% of credit reports contain errors of some kind?

With 25% containing big enough errors that would lead to denial of a loan!

Crazy.

Why the Errors in Your Credit Report?

Why does something so crucial to your financial success have to be so darn complicated and just plain messy?

Reminds me of the IRS tax code. Except in the case of credit reports, we don’t have CPAs to help us figure it out.

But you can’t just leave your credit report alone and expect everything to be okay. Unless you’re debt-free and don’t need a loan. (Hey, there’s a thought!).

Chances are, based on the number above, something is wrong with your report and that something could be lowering your score by enough points to cost you a lot of money, sooner or later.

My Credit Report Errors

I can’t say I’ve ever found a major error on my credit report. I also can’t say I’ve looked really closely at it. Every year I visit annualcreditreport.com and pull one or two of my free credit reports.

I scan the report to make sure my personal information is correct and that the credit accounts listed on the report all belong to me.

I also scan the report for any reported negative items. Honestly, once I realize there are no big, glaring issues, I move on.

The last time I checked my credit report I did find one small error. The report states that one of my aliases is my middle name, followed by my first name initial as the middle name, and then my last name.

I don’t think I’ve ever signed up for credit or gone by that name when applying for credit or holding a job so I don’t know where they got the name from.

I’m not terribly worried about this particular error, though, because there were no accounts that I didn’t recognize. “TP” Money has yet to sign up for any bogus credit accounts. 🙂 Still, the stat above suggests I should check my reports a bit more closely next time.

Common Major Errors Seen in Credit Reports

So, what are the most common types of serious errors seen on credit reports? I put together a quick list for you based on the information I’ve been reading in Liz Weston’s book, Your Credit Score:

- Names that are not you (not just misspellings)

- Social security numbers that aren’t yours

- Address where you’ve never lived

- Accounts and delinquencies that aren’t yours

- Negative items older than seven years

- Hard credit inquiries that you didn’t authorize

Obviously, the biggie is the fourth item there: accounts that aren’t yours. If you have that on your report, you need to get that off as soon as possible. If it’s an active account, it’s a ticking time bomb.

How to Fix Errors and Identity Theft

So what do you do when you have incorrect information on your reports?

This incorrect information could indicate fraud, and/or could lead to you not getting a loan (or at least the best loan you can.)

Someone I know was recently denied a loan because of some negative history on his credit report. It turns out that when he reviewed his report, his Dad had used his SSN to apply for some credit cards a long time ago and then defaulted.

This is essentially identity fraud against your family. Sad. My point in sharing this is to stress the importance of reviewing your credit report periodically, as you never know who is going to use it and screw it up.

You can also protect yourself by using protection services like the identity theft protection offered by Experian. It provides identity theft monitoring, alerts, and dark web surveillance. Experian’s identity theft protection also makes it easy to lock and unlock your credit file with Experian CreditLock or IdentityWorks.

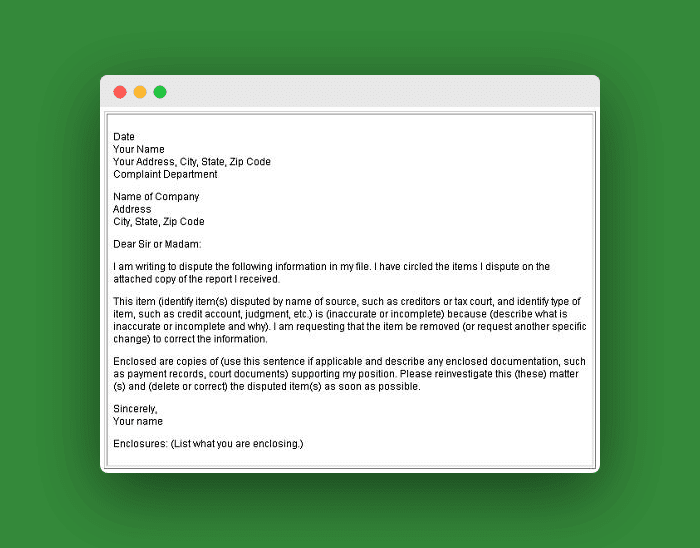

How to Dispute Credit Report Errors

If you have a simple error on your report here’s how to go about getting it corrected:

Tell the reporting agency (TransUnion, Experian, or Equifax), in writing, what information you think is incorrect. Send them copies of evidence of your claim. Keep copies of everything you send and send it certified mail, return receipt requested.

Unless they think it’s bogus, they must send it to the creditor or information provider to investigate your claim (takes about 30 days.) If they agree they will inform the other two agencies. Once they correct the mistake, you can have them send corrected copies to everyone who got one in the past six months.

Next, you need to tell the creditor or information provider. I guess this step is in there to ensure that the information provider sees your complaint, as the reporting agency could have considered it frivolous and tossed it. The same rules apply on copies and mailing methods. Here’s some more information from the Federal Trade Commission about this.

Sample Dispute Letter

But What if it’s Identity Fraud?

If someone stole your identity, you need to step it up a notch and take the following extra steps according to the FTC:

- Place a fraud alert on your credit reports.

- Close the accounts that you know, or believe, have been tampered with or opened fraudulently.

- File a complaint with the Federal Trade Commission.

- File a report with your local police or the police in the community where the identity theft took place.

But What if it’s Family?

Like the story I shared above, there are several people who have their identity taken by their own family members. Dr. Phil had a show once on identity theft within the family.

One segment was on a 23-year-old girl named Mattie, whose Mom had been stealing her identity and wouldn’t stop. Dr. Phil’s expert on the show was Tom Syta, an FTC Director.

Tom says to treat family members the same as a criminal. During the show “Tom suggests that Mattie, and other victims of identity theft, go to the FTC’s Website and fill out an identity theft affidavit to take to the credit reporting agencies.”

Tom also suggests filing a police report, which may or may not be effective, depending on your jurisdiction and the dollar amount involved. Wow, that would be tough to have to file a police report against your own family. I don’t know that I could have done that at 23 years old.

Getting Help to Fix Your Credit

There’s a lot of bad advice floating around out there, and for some time now I’ve wanted to share some truths about finding help with fixing your credit problems.

I turned to Personal Finance Columnist and friend, Liz Pulliam Weston, to help track down a pro.

Liz introduced me to Gail Cunningham, Vice President of Public Relations at the National Foundation for Credit Counseling. Gail was kind enough to share some solid advice on finding help with your credit problems, as well as her take on the current state of the credit world. Check it out:

1. Where can someone go to find trusted, free assistance with fixing their consumer debt problems (i.e. can’t make the payments, in collections, don’t know what is owed, etc.)?

Consumers should reach out to a legitimate credit counseling agency for help. I’ve attached the NFCC Fact Sheet so that you can know a bit more about us, as well as a document I created on How To Select a Legitimate Credit Counseling Agency.

Unfortunately, there are some bad actors in our industry who are more interested in their bottom line than the consumers’. It is incumbent upon the consumer to do their homework before engaging in business with an agency.

2. How will a legitimate credit counselor be able to help someone with consumer debt problems? What will they actually do?

The trained and certified counselor would do a thorough intake of all income sources as well as debt obligations, probing to find out the cause of the financial distress as well as the consumer’s short and long-term financial goals. After reviewing living expenses, a new budget would be created if necessary.

Next, they would look at the debt load. After the budget has been adjusted, there may be enough money remaining to address debt repayment. If not, the counselor will explore resolution options with the consumer.

If it is the right option, the consumer may elect to go on a Debt Management Plan (DMP). If so, the counselor negotiates with the creditors for a reduced monthly payment and to have interest, late fees, and over-limit fees stopped or reduced. The overall objective is that the consumer be able to pay his living expenses in full while still addressing debt reduction.

3. If someone gets rejected on a loan and they’re told it’s because they don’t have a credit history, what should they do? How do they go about establishing credit history fast and improving their credit score?

If someone doesn’t have credit, the best way to establish it is with a gasoline card or a store credit card. Those are considered easier to get. They also shouldn’t try to get too much credit all at once. Doing so puts too many inquiries on their credit report and makes them appear as though they’re desperate for credit. Not good.

They will have to build a good credit history by responsibly handling their credit obligations in order to create a good credit score. This may take time, but it’s well worth it.

4. Is bankruptcy ever a good option for someone in serious debt? And what advice would you have for those contemplating bankruptcy and wanting to start over?

Bankruptcy is the right answer for some, but I’d make it my last stop, not my first. I’d certainly sit down with a credit counselor before I considered bankruptcy to see if there was any other way out.

Help Your Kids Get Started with Credit

Your little one is all grown up! He might be heading off to college in the fall, or she might start working full-time after high school graduation. In either case, your job as a parent isn’t quite done.

If you want to make sure your teen gets a good start financially, here are five moves you can help her take to start building credit.

1. Make Sure Your Teen’s Credit is His Own

Identity theft of minors is a serious problem, affecting tens of thousands of children and teens each year. Since teens have a clean slate credit-wise, they make an attractive target for identity thieves.

Parents can request their minor child’s credit report from the three bureaus, and it’s a good idea to do this. This is particularly true if you have reason to believe your teenager’s identity has been stolen.

In any case, it’s difficult for your teen to build a good credit history if there is fraudulent activity under her name. So it’s worthwhile to request a credit report just to ensure that every credit decision she makes is her own.

2. Make Your Teenager an Authorized User on Your Credit Card

If you have good credit, allowing your teenager to become an authorized user on your account will allow them to “piggyback” on your credit while making it impossible for them to overspend without your knowledge.

In addition, you have the ability to limit the available credit for any authorized users, so this can be a great way for your teenager to put a toe into the water of responsible credit use.

The only downside to this strategy is the fact that the bill will still come to you. So while your teenager will benefit from your good credit, and will learn not to use plastic for every transaction (at least, not without having to face the wrath of Mom and Dad), being an authorized user will not give her a real sense of the responsibility facing her.

That fact may be enough to tempt parents into co-signing a credit card for their teen–but, except in very specific circumstances, parents simply should not do that. Co-signing for a loan will enable your teen to make poor decisions while you will still be on the hook for the consequences.

There are better ways to teach your teenager how to pay her bills–ways that can’t potentially hurt your credit. We discuss one of those ways below.

3. Have Your Teenager Pay For His Own Utilities

While on-time payments for utilities are generally not reported to the credit bureaus, delinquencies often can be. According to Investopedia:

“[Utility companies] will report delinquent accounts much more quickly than other institutions.”

Paying for utilities may not directly help your teen build good credit, but it will give him an opportunity to learn good budgeting and bill-paying habits while the stakes are still relatively low.

For example, when I was living in the dorm my freshman year in college, my parents elected to have my phone bill (which also happened to be my only utility bill) sent directly to me.

They also made it clear that they would not bail me out if I had a particularly high bill. (This might have been a bluff on their part, but it was enough of a threat to keep me sweating through some lean months).

This helped me to learn very early how to budget, how to schedule my bill-paying and the painful repercussions of making a late payment. That meant I was ready for the responsibility of a credit card when I applied for one or two years later.

4. Encourage Your Teenager To Get a Job and Apply for His Own Credit Card

The issue of a job can be a pretty good litmus test for your teen’s readiness for responsibility. Ideally, Junior will want to work and either contribute to his own education expenses or earn his own money.

If he balks at the suggestion of working (gasp!), he’s clearly not ready for credit and it’s time for you to start showing some tough love.

But if your teenager is earning his own income, he can apply for credit on his own even if he is under 21. But he will still need some guidance from you. Make sure that he only takes on as much credit card as he can handle.

Both retail credit cards (which can be easier to get with no credit history) and secured credit cards can limit the amount of trouble your teenager can get into while giving him an easy introduction to credit. An alternative to consider is SelfLender.com (Check out our full review of SelfLender here.)

If your income-earning teenager is ready to apply for his own credit card, be sure to help him find the one that will best fit his needs.

Related: 39 Summer Jobs for Teens and College Students

5. Have Your Home Address Remain Her Main Residence

This is particularly helpful for college students. Lenders like to see stability in terms of living arrangements, and college students will often change their address at least once a year.

Your child can still use your address on credit card applications, which will appear much more favorable on her applications than four different residences in four years would.

However, if you do allow your teenager to do this, make sure that they are signing up for paperless bills or statements so that they cannot claim they didn’t receive bills in time to pay them.

The Credit CARD Act in 2009 was created to help protect young adults from predatory lending practices and from stumbling into huge credit problems through ignorance. As much as I believe in the importance of this legislation, it only takes care of one side of the equation.

Parents have the responsibility to teach their children how to handle credit, and young adults must take the time to learn the ropes before mistakes become disasters.

Even parents who have struggled with credit themselves can help their teenagers to get a good start with credit, as long as they set reasonable boundaries and limits, and take the time to educate themselves and their kids.

Common Questions

Here are some common questions we see about credit scores and reports.

What is FICO®?

FICO® is an acronym for a company named the Fair Isaac Corporation. They were the first company to produce a credit scoring model in 1989 and their scores have been the most widely used ever since. FICO says that 90% of top lenders use FICO scores when making lending decisions.

If your bank or credit card issuer provides you a free credit score each month, there’s a good chance that the score they are using is your FICO®score. MyFICO can help, too.

What is VantageScore?

In 2006, all three major credit bureaus, Experian, TransUnion, and Equifax, joined together to create their own scoring model, calling it VantageScore. Since then, they’ve iterated upon their model several times. Their latest version is called VantageScore 4.0 (released in 2017), but many lenders still use VantageScore 3.0.

Does your VantageScore matter? Yes, and no.

The VantageScore model shares a ton of similarities with FICO®. They are so similar, in fact, that FICO sued VantageScore in 2010 claiming the childhood version of “you copied us!”

The lawsuit failed, but the overall point is that if you have a good FICO® score, you’ll undoubtedly have a good VantageScore as well. Will the exact 3-digit numbers vary slightly? Yes. But they should always be in the same ballpark.

And if you had to pick one score to focus on over the other, stick with your FICO® score. For now, FICO is still king.

Can You Have a Perfect Credit Score?

Your credit score is a numerical representation of what’s in your credit history file. It’s supposed to represent how creditworthy you are.

Why should you care? Well, lenders use your credit score as a factor when considering you. So, it’s not a stretch to assume that you would want to raise your credit score if you want to access credit in the future.

But should you aim for perfection? What is the perfect credit score? For both the VantageScore and base FICO® score models, the lowest score is 300 and the highest credit score is 850.

But are these perfect scores even possible? A perfect score is possible. Apparently, about 1% of the population have a perfect 850 on the FICO® scale. Getting there takes years of positive credit history (up to 30 years), and a diverse mix of revolving and installment credit.

Should You Care About a Perfect Credit Score?

With a credit score, there is perfection, and then there is good enough. Good enough meaning, good enough to get the best rates. After all, that’s what you are after right?

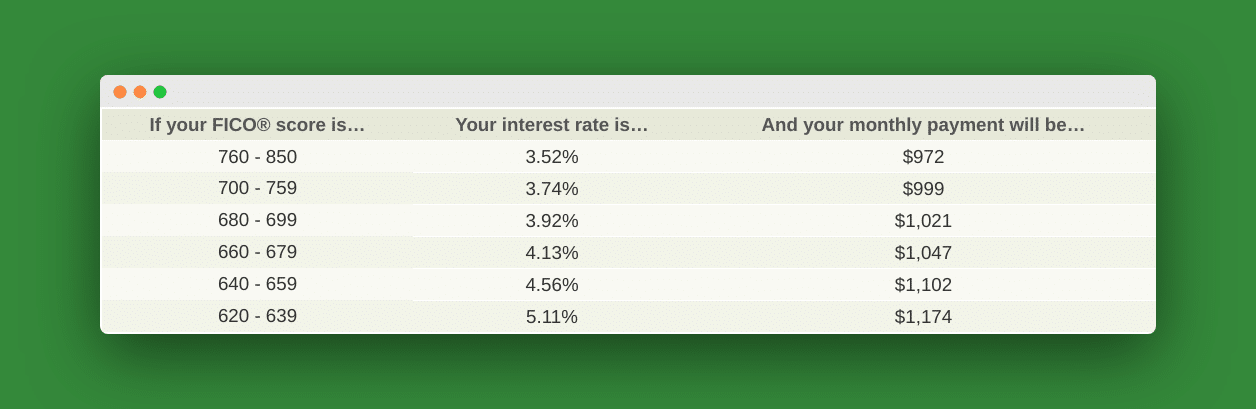

The best interest rate when borrowing. FICO® sheds some light on this by offering up this table of different interest rates available today on a 30 year fixed rate mortgage. You can see the difference in payment and interest over time based on your FICO score.

So as you can see by this chart, 850 shouldn’t be your goal. Your goal should be to get to the 760 mark.

So how do you get there? You improve your credit score by paying attention to the factors that make up your credit score: payment history, amounts owed, length of credit history, types of credit, and new credit inquiries.

Your takeaway from that should be to always pay on time, keep your credit card balances low or at $0, don’t apply for too much credit, and try and develop a diverse mix of credit use (a car loan and a few credit cards should do the trick).

Will Closing Accounts Help Your Score?

Back when I was getting rid of my excess credit card debt, I did a stupid thing. I closed my oldest credit card down. I didn’t know or didn’t care at the time that this move would actually hurt me in terms of building a better credit score.

We all know the importance of a good score: better loan rates, better insurance rates. Closing down credit accounts harm your credit score in two major ways.

1. It Raises Your Credit Utilization Ratio

When you close down an active account, the available credit from that account gets removed from your credit file. Therefore, to the credit agencies, you appear to have less available credit at your disposal. They translate this into not as many people are lending to this person, so they must be a higher risk.

It’s important to keep your credit utilization ratio low. To do this you need to have a lot of credit available to you, but only be using a small amount of that credit. So, if your available balances all add up to $10,000, you need to be using $1,000 – 2,000, not $9,000. From what I hear, this is the case whether you pay it all off each month or carry a balance.

2. It Makes Your Credit History Look Younger

The second thing closing an account will do is make you look younger in terms of credit history. One of the keys to a good credit score is a long track record of responsible borrowing. So it’s important to leave those old accounts intact, even if you’re not using them.

But What if You’re Struggling with Debt?

Honestly, the reason I called and canceled my old credit card accounts back in the day was that I was sick of going in and out of credit card debt. I’d had enough and just wanted to force myself to quit falling back into those bad habits of spending money I didn’t have.

So, if the whole reason you’re closing those old accounts down is to free yourself from debt and you won’t need your score for a home or auto loan in the near future, then closing them might be the best choice for you anyway.

Also, if the card is charging you an annual fee, that may be enough to justify closing it.

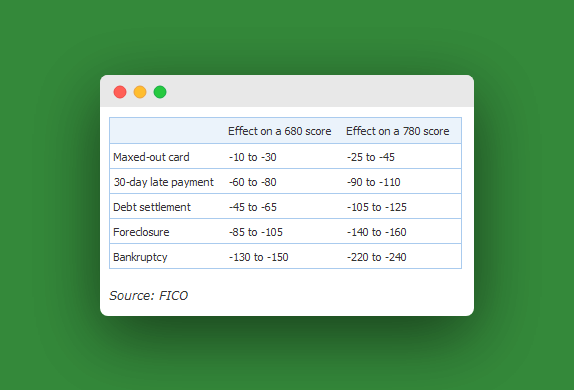

How Much Do Negative Marks Affect Your Score?

We’ve known for a while now what actions will negatively affect your credit score and what steps to take to improve your score. But what we haven’t known is the specific number of negative points you’ll be hit with for certain actions.

Here’s how the points break down:

Here are some things I noticed about the recently released FICO® info.

1. Progressive Punishment from FICO®

The negative action (late payments, maxed-out card, etc) will affect those with higher scores more drastically than they will someone with a lower score.

This seems unfair to me. But who says FICO® has to be fair, right? They get to make up their own rules.

2. Multiple Dings Not Addressed

What the chart doesn’t explain is how the scores are affected when you hit a couple of these actions at the same time, or within the same month.

For instance, let’s say you max out your card and then you pay it late by 30 days. Will you take a 150 point hit if you have a 780?

Then, what happens if you have a 60 day late hit the next month? Another -100 points? I would assume that the scores wouldn’t compound on each other directly like that. But that’s just my assumption.

3. Bankruptcy Evens the FICO® Score

Notice that where the other dings don’t necessarily reduce the 680 and 780 score to the same levels, the bankruptcy pretty much puts them both around the 550 mark.

I guess this shows how important bankruptcy is to FICO®. They’ll simply flatline you if you do it, regardless of your history.

4. What This Means in Dollars

Dings to your credit score only really matter if you’re going to be using that number in the future. Will you need a home loan, car loan, or credit card? Your FICO® score will affect your ability to get a good interest rate on that loan.

The higher your score is the better the interest rate you’re likely to get. And the better the interest rate, the less you’ll pay in interest charges throughout your life.

So how do these damage points translate into dollars? Jeremy Simon at CreditCards.com put together a great analysis that shows how much the FICO® damage points cost you in dollars. Check that out here.

5. Look at the Positive

It’s not all negative. What I take from this chart is that FICO® is likely to also reward me for consistently doing a couple of things right: paying on time and keeping my credit card balances low compared to my available credit.

What Happens to Credit When You’re Debt Free?

Most people I know are debt-free except the mortgage, or they want to get there very fast. The question then arises,” Will you be able to maintain a good credit score if all you are doing is paying on a mortgage?”

If you are in this situation, the term that you need to familiarize yourself with is “credit mix”.

Credit mix is the different types of credit that you currently have. For instance, you could have revolving credit, like a credit card. You could also have installment credit like a car loan or mortgage.

All else being equal, the more types of debt you have the better your credit mix and the better your score.

Given that, when you pay off everything but the mortgage you are reducing your credit mix unless you keep your credit card accounts open.

Even though you’ve paid off your credit card, if you keep the account open, your available credit line will still be reflected on your credit report and in your score.

Related: 17 Winning Tips and Tricks to Legally Eliminate Credit Card Debt

But What if You Get Dropped?

Of course, there is a possibility that if you aren’t using your credit card, the issuer could drop you or reduce your limit, reducing your available credit. At that time, you’d have more than credit mix to worry about, you’d have an available credit issue.

The good thing is that in the immediate your credit mix only makes up 10% of your credit score. So, even if you reduce your credit mix, a 10% knock against your credit score isn’t crushing.

Credit expert John Ulzheimer said this about credit mix in a Credit.com article,

“it’s certainly not a priority to address, anyone who has hopes of maxing out their credit scores should pay attention.”

Do You Even Need a Good Credit Score?

Another obvious question to ask yourself (that many of you have already been thinking in your head) is “why do I need a good credit score?” Well, you may not.

If borrowing is in your future, either through a refinance or new real estate purchase (or another type of credit for that matter), then you probably want to consider maintaining a quality credit score.

Additionally, a lack of credit score or poor credit score could hurt your chances of renting a house or apartment. Not every landlord uses credit scores/history, but some will. I do.

But I know that lack of score would not automatically put someone out of the running for me. It’s bad history that I’m mostly concerned with.

But if this (getting more credit, renting, etc.) is not a big deal for you, then you could definitely stop caring. Many people who have reached financial freedom are proud of their lack of credit history and the fact that they don’t care.

Here’s my friend Adam Baker when he found out he has no credit score:

Just had my credit score checked – and it was reported I have "NO SCORE"… Whoo-hoo. Finally. 🙂

— Adam Baker (@AdamCBaker) July 27, 2012

I’m not quite to that point myself. I enjoy maintaining a responsible credit history and I like that it gives me more financial options. But I do plan on being there one day.

So the bottom line is this, if you maintain a decent credit mix (mortgage and a few “open” revolving accounts) and pay all your bills on time, you should not have a problem maintaining a good credit score. If you close the revolving accounts (i.e. credit cards) you will take a slight hit to your credit.

Over time, as your credit history begins to fade away and all your report shows is a loan for a mortgage, your score could take additional hits. But by that time your goal of financial freedom may have been achieved and your need for a credit history could be a thing of the past.

Should I Freeze My Child’s (or My Own) Credit?

According to a report by the research firm, Javelin Strategy & Research, 11.1 million adults were the victim of identity theft in 2009 in the United States, and the total annual amount lost to fraud was $54 billion.

Children are often also the victim of identity theft. In fact, 1.48% of minors were victims of identity theft in 2017. Thieves will even use Social Security Numbers before they are issued. It’s possible for a newborn baby to already be a victim of this. Here’s an article from CNBC about this.

Why Children Are the Victim of Identity Theft

Many people do not realize that that credit card companies do not have an easy way to verify the age of an applicant especially if someone has not applied for credit before.

Most credit card applications simply ask for your date of birth without providing any proof. Children and teens are a prime target for identity theft because they have perfectly clean credit records.

Children make easy prey for identity thieves, since parents do not usually check their children’s credit reports. A crime can go undetected for a very long time which can compound the problem.

Warning Signs of Child Identity Theft

If your child has been the victim of identity theft, it may take you quite a while to find out about it. Many parents realize the news when they are rejected while attempting to open a savings account or 529 College Savings Plan for the child because of his or her bad credit.

Or, parents may find out the terrible news when pre-approved credit card offers, bills, or financial statements are received in the child’s name. These should be red flags for a parent that there could potentially be a problem.

How To Freeze Your Child’s (or Your) Credit Report

You should check your child’s credit report, but that may be slightly more difficult than the parent might imagine. An adult can go online to one of the three credit bureaus and order a credit report. But, if you want to request your child’s credit report, you have to send that request to the bureaus in writing. Here’s an article from Experian that goes into more detail.

Children do not actually have formal credit report if they are under the age of 18, but the credit bureaus will be able to provide you with information on your child if they are the victim of child identity theft and have a credit history.

Once you’ve determined that your child’s credit report is clear, you may want to put a freeze on their credit to prevent any future fraud.

A credit freeze or also known as a security freeze will not allow any potential lender access to the credit report at all without permission. This will prevent new credit from being issued. Placing a credit freeze on a child’s credit report as early as possible will prevent child identity theft. You can place a freeze on your child’s or your own credit (or both!)

A law passed in 2018 required all three credit bureaus to offer this service for free.

Equifax: You can freeze your Equifax credit report on their website. (Visit Equifax here.) If you are freezing the credit report for a minor, it has to be in writing.

Experian: You can also freeze your Experian credit report online. (Visit Experian here.) To freeze a credit report for your child, you’ll need to submit a form in writing. Here are the full directions, as well as the form you’ll need to complete, directly from Experian.

Transunion: You can freeze your Transunion credit report on their website. (Visit Transunion here.) If you are looking to freeze your child’s credit report you can find the full instructions here. They also require the submission to be in writing.

The Drawback Of A Credit Freeze

A credit freeze is designed to prevent a credit reporting company from releasing your credit report without your consent to a new lender.

However, you should be aware that using a credit freeze can delay you from being approved for new credit if you really are applying for a new loan. You have to notify the three different credit bureaus individually in order to allow the release of your credit information.

With a credit freeze, you’ll have to turn the freeze off and back on when applying for a new loan, credit, or mortgages.

You can also run into trouble with other financial transactions that request a credit report such as applying for new insurance, government services, rental housing, employment, investment, license, cellular telephone, or even turning on new utilities.

A credit freeze provides excellent protection against identity theft for an adult or a child. But you should not forget that it is very restrictive.

Placing a credit freeze on a child’s credit report as early as possible will help prevent your child from becoming a victim of child identity theft. More children than ever have found themselves the victim of identity theft and many are at the hands of a close family friend or relative.

But, a parent can help prevent identity theft of their child by taking preventative measures.

Where Should You Check Your Credit?

You can get your free credit reports from annualcreditreport.com. For those not familiar with it, it’s a website that the three credit reporting agencies (Experian, Equifax, and TransUnion) have set up based on a requirement from the Fair Credit Reporting Act.

Using this website, you can link to the three agencies and get a free copy of your credit report from them once a year.

Bear in mind that once you link to one of the agencies, they will try everything in their power to entice you to spend money on other products (credit score, customized reports, etc.)

You don’t have to do any of this.

Stay focused. Just keep following the small links to get your free report. I always save the report as a pdf file. If you don’t have Adobe Creator then just copy and paste the HTML page to a Word(.doc) or Text (.txt) file.

Beware of Unofficial Websites

As you’re probably aware of, there are many websites out there that will sell you your credit report. Here’s a word from the Federal Trade Commission on these unofficial sites:

“Many other websites claim to offer free credit reports, free credit scores, or free credit monitoring. But, be careful. These sites are not part of the official annual free credit report program. And in some cases, the free product comes with strings attached.”

Get Your Credit Report Three Times a Year for Free From AnnualCreditReport.Com.

The three nationwide consumer reporting agencies are all required to provide you with a free copy every year. It’s a good idea not to pull them all at once.

Instead, it might be best to get your free report from each of the agencies at varying times during the year.

For instance, you could pull one in late January (shortly after the holiday season), another in July (after returning from vacation), and the last sometime in the fall (just for kicks).

Note: If this is your first credit history check, you are about to apply for a mortgage, or you suspect fraud, you’ll want to get all three at once. The three times a year method is just for general monitoring purposes.

Think Beyond AnnualCreditReport.com.

There are three big problems with using AnnualCreditReport.com as your ONLY source for credit reports:

The Big Up-Sell: When you use the AnnualCreditReport.com website to get your three reports you’ll be pressured to sign up for a bunch of services that will cost you.

Now there’s nothing wrong with paying for something of value, but if you’re going there with the intention of just getting your free report, you’ll have to fight through the many sales pitches that are going to be thrown at you. The Fair Credit Reporting Act should have explicitly prevented this. But they didn’t go that far.

No Free Extras and No Free Credit Score: While going to AnnualCreditReport.com will definitely get you a free credit report, it won’t give you anything else for free, certainly not a free credit score. There are no credit monitoring services or credit score that can be had for free by going there. All you get is your three free credit reports.

Limited to One Per Year: The biggest limitation of AnnualCreditReport.com is the fact that you can only get one credit report from each of the agencies each year. Most people think to check their reports at the beginning of the year when the motivation for budgeting and getting things in order is strong.

But then later on in the year, you may be considering a loan or may suspect some type of fraud. At that point, most people either do nothing, or they fork over money to get their credit report. But you don’t have to pay. You can sign up for a free trial using one of the services listed below. Just make sure you cancel your account prior to the free trial running out.

See below for the other ways to get your free credit report.

Five Reasons to Check Your Credit Report

It’s important to occasionally review your credit reports. Here are a few of the reasons why I do it:

Check Your Reports for Fraud

Someone uses your personal information to open up a credit line. Then they run up a huge balance and never pay the bill. You don’t find out about it till it’s too late.

There’s a big negative on your credit reports. When you try and apply for credit on your own, the lender won’t do it because of the negative history. Checking your reports a few times a year is a good way to ensure you aren’t being taken advantage of by someone.

Review It for Errors

In addition to fraud, there’s actually a good chance that your credit reports have errors on them.

The errors could be things like accounts that aren’t yours, missing information, incorrect credit limits, missed payments that aren’t accurate. These errors could be negatively affecting your credit score.

It’s important to check your credit reports so that you can fix these credit report errors.

Prepare for a Loan

If you happen to be planning on getting a significant loan in the near future, like a mortgage, then it’s crucial you review your reports for the types of fraud and errors listed above.

The rate on the mortgage, car loan, or small business loan is going to be based on what the credit agencies are reporting about you. This could mean thousands in savings by having the score you deserve.

First Time Credit Check

If you’ve never reviewed your credit report, this is the time to do it. It’s easy and free.

Make Sure You’re Getting Credit

Another reason to review your credit reports is to make sure you are getting credit for the history you have. It’s not uncommon for one of the three reports to be missing important information, like an old account that had a positive payment history.

Take a second to review your report and make sure you’re getting credit for your positive history.

What About a Tri-Merge Credit Report?

A tri-merge credit report or 3-in-1 credit report is just what it sounds like. It’s a report that combines the information from the three major credit reporting agencies and presents it in one easy to consume report.

The three major bureaus all report different information. Some may be more accurate than others. They get their information from different methods. Therefore, what is on one report may not be on another.

For these reasons, it’s important to understand what is on each of the three reports. A tri-merge report combines all that information into one report so that you don’t have to pull all three reports and combine the information yourself.

Tri-merge credit reports are often used by landlords when evaluating potential renters, or by lenders when considering a loan. If you are evaluating someone’s credit, remember to get their permission.

Experian can also provide you a 3-bureau credit report for a one-time fee. Or you can sign up for Experian’s CreditWorks, which will send you a tri-merge credit report on a monthly basis.

Get a Free Tri-Merge Credit Report

I don’t know that there is a place where you can get a tri-merge credit report for free. However, I do know that you can create your own tri-merge report for free. Just visit AnnualCreditReport.com and request all three of your credit reports: TransUnion, Equifax, and Experian.

Then take your reports and consolidate the information. Any information missing on one of the reports you might want to report to them if it’s something that might improve your credit score.

Get a Tri-Merge Credit Report with Scores

For those not in the do-it-yourself crowd, there are credit score companies who will take your credit report information and combine it into one report for you.

They will also give you a credit score. They, of course, charge a small fee for this service.

Conclusion

No matter where your credit score is today or credit mistakes that you’ve made in the past. you can improve your score. We’ve covered a ton of ground in this piece, but maybe you still have questions. Consider Just Answer as an option to get them answered by a financial expert. But remember the basics of building a good credit score are really simple. Pay your bills on time and don’t spend too much of your available credit.

If you do those two things on a consistent basis, you’ll be able to build a sky-high credit score…maybe even faster than you think.