SBA Loans: Everything You Need to Know

Notice: For COVID-19 related SBA loan information, see our coverage of the Paycheck Protection Program (PPP). Or for more coronavirus (COVID-19) SBA resources, skip to the bottom where we discuss the EIDL and SBA Debt Relief Programs.

If you need funding for your small business, it’s hard to beat SBA loans. They come with favorable terms and may be easier to qualify for than other business loans.

But as with any government-sponsored initiative, the SBA loan program can be confusing. There are multiple SBA loans, each with different purposes and terms. But in this guide, we’ll cut through the clutter to give you the most important answers that you’re looking for.

SBA loans are backed by the Small Business Administration (SBA) and provided by private lenders. Loan amounts range from $500 to $5 million. Because SBA loans are guaranteed by the SBA, they’re considered less risky for the lender, which could improve your approval odds. To qualify for an SBA loan, you’ll need to meet the business type and size requirements and you’ll need a good credit score and business plan. In many cases, you’ll also need to purchase a life insurance policy equal to the amount of the loan.

Let’s take a closer look at how SBA loans work and who qualifies for them.

SBA Loans for Business

One of the common misconceptions about SBA loans is that the Small Business Administration provides the funding themselves. But that’s not the case.

Instead, the SBA simply guarantees a portion of the loan to reduce the lender’s risk. There are numerous banks and lenders that offer SBA loans. To find one, you can use the SBA’s lender match tool.

The SBA also sets the guidelines and terms for how lenders can administer these loans. They can be as small as $500 and as large as $5 million.

SBA Loan Requirements

If you’re thinking about applying for an SBA loan, there are a few conditions that will need to be met. Below are the most important SBA loan requirements that you need to know.

Who Qualifies for an SBA Loan?

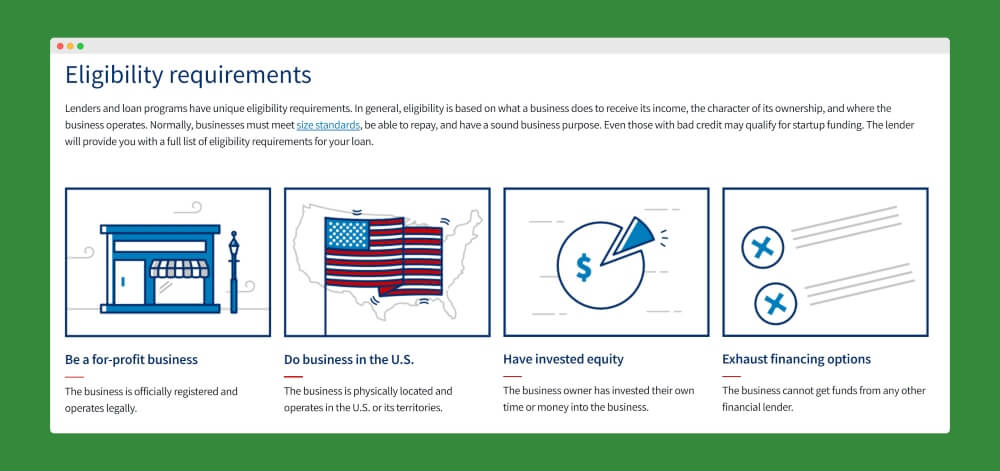

To qualify for an SBA loan, you’ll need to meet four basic requirements:

- Be a for-profit business

- Do business in the U.S.

- Have invested equity (i.e. you’ve invested your own time or money into the business)

- Exhaust financing options (i.e. you can’t get a normal business loan)

Additionally, you’ll need to meet size standards and you’ll need to prove that you’re likely to be able to repay your loan. See the table of size standards.

And although the SBA minimizes some of the lender’s risk, they’re still going to want you to have a decent credit score. A score of over 670 would be a good start. But a score in the 700s would be even better. If you need help in this department, check out our ultimate guide to improving your credit.

Finally, you won’t qualify if your business is primarily involved in lending money, life insurance, or pyramid schemes. See the full eligibility requirements here.

Are SBA Loans Hard to Get?

There are two main reasons why SBA loans can be harder to get than other loans. The biggest reason is the requirement that you “exhaust other financing options” first. It’s only after you’ve pursued all other available financing options, that you can apply for an SBA loan.

The second reason that they can be hard to get is the fact that they come with SBA-regulated terms and guidelines. In other words, the interest rates, down payment requirements, and fees may be lower than a traditional loan. Lenders don’t want to take loans with such favorable terms and hand them out like candy.

How to Get an SBA Loan

To get an SBA loan, begin by finding an approved lender. Then, you’ll need to fill out an application. And we’ll go ahead and warn you now–filling that application out is going to take you a while.

Here is a quick list of the documents that you’ll be required to submit with your application:

- Borrower Information Form

- Personal Background and Financial Statement

- Business Financial Statements

- Year-End Profit and Loss (P&L) Statement for the last three years

- Year-End Balance Sheet for the last three years, including a detailed debt schedule

- Reconciliation of Net Worth

- Interim Balance Sheet

- Interim Profit & Loss Statements

- Projected Financial Statements that include month to month cash flow projections, for at least a one-year period.

- Business Certificate/License

- Loan Application History

- Income Tax Returns

- Resumes (for each business partner)

- Business Overview and History

- Business Lease

Several of the items above come with accompanying forms that you’ll need to fill out.

So if you decide to apply for an SBA loan, you better buckle your seat belt and prepare for the marathon of documentation you’ll need to collect and provide. See the full SBA loan application checklist.

SBA Loan Interest Rates

The SBA sets the maximum interest rate that lenders can charge, based on the prime interest rate plus some padding. At the time of this writing, the prime rate is 4.75%, but you can always double-check it here. The interest rate varies by the type of loan that you take out.

| 7(a) Loans | Terms less than 7 years | Terms over 7 years |

|---|---|---|

| $0 - $25,000 | Prime + 4.25% | Prime + 4.75% |

| $25,001 - $50,000 | Prime + 3.25% | Prime + 3.75% |

| $50,001 or more | Prime + 2.25% | Prime + 2.75% |

| Express Loans | |

|---|---|

| Up to $50,000 | Prime + 6.5% |

| Above $50,000 | Prime + 4.5% |

Here is the full table of all the types of loans the SBA issues and their interest rates.

SBA Loan Life Insurance Requirements

As mentioned earlier, the advantage of SBA loans for lenders is that the guaranteed portion limits their risk. But it doesn’t eliminate their risk entirely of an SBA loan default.

To help protect lenders, the SBA requires that some borrowers take out an SBA loan life insurance policy. When the success of a business relies heavily on one owner’s participation, a life insurance policy will be required.

If you’re just starting to build your business, there’s a good chance that you’ll fit this criterion. In this case, you’ll need to take out a life insurance policy to match your loan amount.

Related: How to Buy the Best Life Insurance in 7 Easy Steps

Bestow Review

If you need to get term life insurance to meet the SBA loan requirements, you may want to consider Bestow.

When you apply for life insurance with Bestow, they use algorithms instead of medical exams to determine insurability. This means that you could get approved in as little as five minutes!

Bestow’s life insurance plans offer coverage from $50,000 to $1 million and premiums start at $8 a month. Plus, they’re backed by A+ rated insurers.

One of the great things about using life insurance policies offered by Bestow to fulfill your SBA loan requirements is that you don’t have to name your lender as the only beneficiary. Instead, you can elect for lenders to receive their payout through a collateral assignment. And you can assign another beneficiary to receive the rest of the payout.

For example, let’s say someone takes out a $250,000 loan and a corresponding $250,000 life insurance policy. Over the next 10 years, the borrower pays off $100,000 on their loan before dying unexpectedly. In this case, the lender would receive $150,000 of the life insurance payout (the remaining balance) and your beneficiary would receive the rest.

Bestow knows how to fulfill your SBA loan life insurance requirements. So if you are currently looking for a policy, get a free quote from Bestow to see how affordable it could be.

Types of SBA loans

There are several SBA loan programs. However, the most common loan is the SBA 7(a) loan. With 7(a) loans, you can borrow up to $5 million.

- For 7(a) loans under $150,000, the SBA will guarantee up to 85%.

- For 7(a) loans over $150,000, the SBA will guarantee up to 75%.

The interest rates can be variable or fixed, depending on the lender. Currently, the maximum interest rates for 7(a) loans range from prime + 2.25% to prime + 4.75%, depending on your loan size and length.

Finally, 7(a) loans charge a one-time guarantee fee of 2.0% to 3.5% and an ongoing guarantee fee of 0.55%

SBA Express

In most regards, SBA Express loans follow the same rules and requirements as 7(a) loans. But the biggest advantage of SBA Express loans is that they come with an expedited approval process.

According to the SBA, you can receive an SBA Express approval response in as little as 36 hours. So if you need emergency funds, SBA Express could be an appealing option.

But there are downsides and limitations. First, SBA Express is only offered on loans up to $350,000. Second, the SBA will only guarantee 50% of the loan, so it could be harder to get approved. Third, for loans under $50,000, you’ll pay a higher interest rate of prime+ 6.5%.

SBA Loans for Veterans

The SBA offers special financing to military veterans through their SBA Veterans Advantage program.

In most regards, the Veterans Advantage program matches the 7(a) loan guidelines. But there is one important difference. With the Veterans Advantage program, the SBA removes the up-front 2.0% to 3.0% fee.

That could save you a good chunk of change. So if you’re a former member of the armed forces, this is definitely a program that you should look into. Learn more about the SBA Veterans Advantage Program.

SBA Loans for Women

There aren’t technically any specific SBA loans for women. But their Office of Women’s Business Ownership (OWBO) is dedicated solely to helping women level the playing field in business.

Through the OWBO, women can get business counseling and training. And the SBA says that their goal is to give at least 5% of all federal contracting dollars to women.

The SBA also advises that some female business owners may qualify for funding through the 8(a) Business Development program. Learn more about SBA programs for women.

SBA Loans for Real Estate

If you’re looking to buy commercial property with your SBA loan, you may want to consider a 504 loan. These SBA loans can only be used to purchase long-term fixed assets. But the great part about 504 loans is that they come with lower down payment requirements (10%) and fixed interest rates.

See a quick view chart of all SBA loan types and terms.

SBA Loans for Coronavirus (COVID-19) Relief

If you’re a small business owner who’s dealing with financial burdens brought on by the COVID-19 crisis, there are a few SBA loan programs that could help. The most generous program is the Paycheck Protection Program (PPP), which was launched with the signing of the CARES Act.

With PPP, you can borrow up to 2.5 times what you normally spend each month on payroll, utility, rent, and health insurance premiums. And as long as the funds are used for those purposes, 8 weeks of expenses can be fully forgiven. Check out our full guide to the Paycheck Protection Program. Or continue reading to learn about two other SBA loan programs that can also provide coronavirus relief.

Economic Injury Disaster Loan (EIDL)

Economic Injury Disaster Loans are low-interest loans designed for small businesses that suffered serious economic hardship. And with President Trump’s signing of the CARES Act, any businesses that have been negatively affected by COVID-19 are eligible to apply for an EIDL.

How Can Business Owners Use the EIDL Loan?

Like the Paycheck Protection Program, EIDL funds can be used towards payroll, rent, and mortgage payments. But, with the EIDL program, you can also use your funds to cover financial obligations that you can’t pay due to lost revenue. For example, you could use EIDL funds to pay invoices from your suppliers or lease payments on your equipment.

What are the EIDL Loan Interest Rates and Terms?

Economic Injury Disaster Loans are capped at $2 million and come with an interest rate of 3.75% for businesses and 2.75% for nonprofits. Payments are deferred for a full year, while PPP loans are deferred for 6 months. But, like PPP loans, interest will accrue during your EIDL deferment period. Finally, Economic Injury Disaster Loans come with terms as long as 30 years — 15 times longer than the 2-year maturity dates of PPP loans.

Is the EIDL Loan Forgivable?

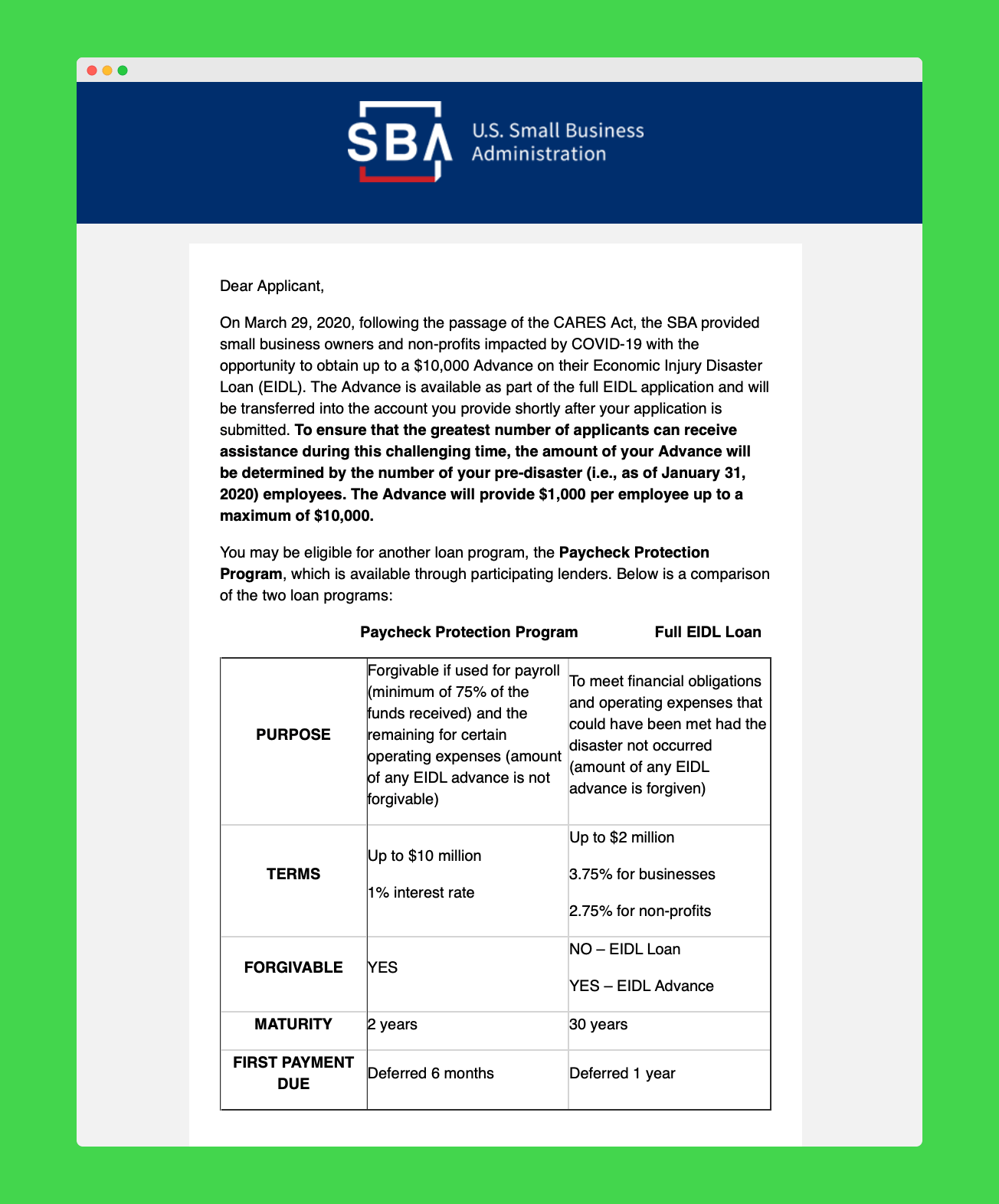

That’s a bit of a complicated question. Unlike the PPP program, the lion’s share of an EIDL loan is not forgivable. However, if you need emergency funds, you can get up to a $10,000 cash advance within three days of submitting your EIDL application.

This cash advance is a grant (dubbed the Emergency Economic Injury Grant) that doesn’t need to be repaid under any circumstances. So even if it turns out that you’re denied for the EIDL, applying could still be worth a cool $10,000 that you won’t need to pay back.

The SBA has provided further guidance on the advance and it appears that applicants will be receiving $1,000 for each employee. See this email from the SBA:

When Can Business Owners Apply for an EIDL Loan?

This is another area where the EIDL program wins out. Since PPP is a brand new program, it’s not available to everyone yet. Officially, lenders will start accepting applications from small business owners and sole proprietors on April 3rd. But independent contractors and self-employed individuals will need to wait until April 10th to apply.

However, the EIDL is an existing program that many lenders already offer. For this reason, you can apply for an EIDL loan right now. Apply at https://covid19relief.sba.gov/.

Who Can Apply for an EIDL Loan?

Any small businesses or private non-profits with less than 500 employees can apply for an EIDL. This includes:

- Sole proprietorships (with or without employees)

- Independent contractors

- Cooperatives and employee-owned businesses

- Tribal groups

For loans under $200,000, the EIDL does not require a personal guarantee. But you will still need to meet the lender’s credit score requirements.

Can You Apply for Both the EIDL and PPP Loans?

Yes, you can! However, you can’t use both loans for the same purpose. For example, if you use the PPP loan to cover payroll, you couldn’t use the EIDL towards payroll expenses as well. However, in this situation, you could use the EIDL to cover debt obligations or paid sick leave for your employees.

EIDL vs PPP: Which Program is Better for Small Business Owners?

Personally, I don’t have immediate plans to apply for either loan. The main reason why is that I don’t currently have any one on my payroll besides myself and my income hasn’t taken a significant hit yet. However, I know my case is rare and many other small business owners are hurting badly right now. I want to keep the funds available for those who really need it.

But if you have been negatively affected by the COVID-19 crisis, PPP is better if you’re looking to maximize forgiveness on qualified expenses. But the EIDL is better if you’re looking for more flexibility on how you spend the funds or you want longer repayment terms. Even if you plan to focus mainly on the PPP program, the $10,000 EIDL grant could quickly inject some much-needed cash flow into your business.

SBA Debt Relief Program

Do you already have an existing SBA loan? If so, the financial fallout of COVD-19 could make it difficult for you to make your payments. Thankfully, the SBA has instituted a debt relief program to give small businesses a reprieve.

With the SBA Debt Relief Program, the SBA will cover all loan payments (both principal and interest) on existing SBA 7(a) loans for the next 6 months. And SBA 7(a) loans that are taken out within 6 months of the signing of the CARES Act (September 27, 2020) will also qualify for this benefit.

This debt relief should be automatic. In other words, your bank should just stop auto-debiting your account without requiring any intervention on your part. However, if you notice that your lender is continuing to auto-draft your account, you’ll want to give them a call.

The Bottom Line

SBA loans come with attractive rates and terms that make them one of the most desirable sources of small business funding. But if you’re planning to apply for an SBA loan, be prepared. You’ll probably need to jump through your fair share of hoops along the way.

If you’re ready to get started, begin by searching for an approved lender. Have you been successful in taking out an SBA loan? If so, we’d love to hear your tips or advice in the comments!