What You Can Expect from a Financial Planner [Plus How Much They Cost]

The world of investing and financial planning can be confusing.

If you’ve heard about certified financial advisors, you may be wondering exactly what do they do and whether or not you need one.

Even as a CPA myself, I’ve found this world a bit confusing. But I spoke with some friends who are advisors, did my own research with an advisor session, and I’m here to share what I learned with you.

A financial planner can do anything from managing your investments to giving your finances a total overhaul. Different financial planners get paid in different ways. Some charge a percentage of the assets they manage, typically 1-2%. Others get paid by the hour, often $150 to $300 per hour.

What is a Financial Advisor?

The term “financial advisor” is a broad one that can refer to many different types of people or services that help people manage their money and reach their financial goals.

When it comes to giving financial advice, anyone can choose to do without getting any particular certification. But to actually sell investment products, financial advisors must pass a series of tests.

Financial advisors who have completed all the required testing can become broker-agents or registered investment advisors. We’ll discuss how broker-agents and Registered Investment Advisors are different under the “What is a Fiduciary Financial Advisor” section.

What is a Certified Financial Advisor?

Technically, there is no such thing as a “Certified Financial Advisor.” But Certified Financial Planners (CFPs) definitely are a thing. While all CFPs are financial advisors, not all financial advisors are CFPs.

To become a CFP, you must submit yourself to a grueling education process that includes several courses and a killer exam. Once the education requirement to become a CFP has been satisfied, three years of full-time personal financial planning experience or two years of apprenticeship experience must be completed before an advisor can receive the CFP designation.

When I interviewed Jeff Rose, a CFP himself and founder of Good Financial Cents, he talked about how intense and difficult it was to become a CFP.

The process that I went through to become a Certified Financial Planner™ professional was one of the hardest times of my life.

But he also says that the time, effort, and financial sacrifice that it took to become a CFP earned him a lot of credibility.

“Almost anyone in our industry can become a financial advisor, but taking the extra time and effort to become a CFP® has earned the respect from my peers and also my clients.”

Finally, the Certified Financial Planner board requires all CFPs to complete 30 credit hours of continuing education every two years so that they can stay well-versed in comprehensive financial planning.

What is a Fiduciary Financial Advisor?

A fiduciary financial advisor is someone who is required to act in the best interest of their clients. While you wouldn’t be crazy to expect that all financial advisors would have this requirement, unfortunately, they don’t.

Many financial advisors are only bound to a “suitability” requirement, which means that they can only make investment suggestions that meet a client’s age, risk tolerance, and financial circumstances.

Fiduciary advisors, on the other hand, are held to a much higher standard. They must always put the interest of the client’s above their own. That means if a particular investment product or strategy is best for the client, they must recommend it even if it means less money (or none at all) in their own pocket.

How can you find a fiduciary financial advisor? This is where the distinction between a regular broker-agent and a Registered Investment Advisor (RIA) comes into play. RIAs are required by law to act as fiduciaries for their clients, whereas broker-agents are not.

And in the CFP Board Code of Ethics, they require all CFPs to act as fiduciaries as well.

What is a Fee-Only Financial Advisor?

There are three main categories of financial advisors:

- Commission: These types of advisors make all their money from the commissions that they earn on investment product sales.

- Fee-Based: These types of advisors charge some sort of flat fee for their services, but may also earn on commissions on product sales.

- Fee-Only: These types of advisors cannot earn any commission from product sales. As the name aptly suggests, the fee is their only source of income.

Since fee-only financial planners don’t receive any commissions, many believe this removes nearly all potential conflict of interest. They are paid to give you good advice. Period.

And if you aren’t happy with their services, you can always go find another fee-only planner who serves you better. For this reason, the interests of the client and the fee-only financial planner are usually closely aligned.

Later on in this article, I’ll talk about my first experience sitting down with John, a CFP at Frisco Financial Planning. When I met with John, I asked him what my readers should look for in a financial advisor.

- A Certified Financial Planner Professional with several (at least 10) years of experience.

- Not employed by a large financial institution (bank, brokerage fund, or life insurance company).

- Fee-only (paid directly by the client and receives no commission).

I couldn’t agree more with John. By just following these three guidelines you will have a great chance of finding a wonderful financial advisor who only acts in your best interests.

What do Financial Advisors do?

When I interviewed Jeff Rose, I asked him what kinds of services he tends to provide for his clients. Here’s what he had to say:

“…Most people that come to me need a game plan for a successful retirement. They rely on me to analyze their situation and develop a plan of attack that does two things: 1. Satisfies the goals they are trying to accomplish 2. Does so in a fashion that they understand and are completely comfortable with.”

In this section, it’s important to explain a key difference between CFPs and Registered Investment Advisors (RIAs).

To use a baseball analogy, CFPs are like utility players. They help clients put together a plan that encompasses their entire financial landscape, including the entire financial picture, including insurance, taxes, and estate planning.

RIAs, on the other hand, are like a lefty bullpen pitcher. They’re specialists. RIAs only give advice on investments and are highly trained to do so. For this reason, some people (especially wealthier clients) choose to work with both a CFP and an RIA in tandem.

If you’re just looking for someone to give you investment recommendations, an RIA would be a fine choice. But if you like the idea of having someone in your corner who’s keeping an eye on every aspect of your financial situation, then you’re going to want to find a CFP.

How Much do Financial Advisors Cost?

When it comes to fee-only financial advisors, there are three main types of fee structures.

1. Assets Under Management (AUM)

This is one of the most common fee structures for fee-only advisors. Their fee is simply a percentage (often around 1%) of the assets that are being managed for the client.

So if the client’s portfolio is $500,000, then the fee would be $5,000.

It’s important to note, though, that these types of advisors often have account minimums, such as $250,000. Accounts with smaller balances are often just not worth their time.

It’s also important to note that their fee is taken out of your investment, which reduces the amount available to grow. This is even a bigger issue if all your investments are in retirement accounts since they have caps. If you invest $6,000 in your Roth (the annual cap as of 2019) and the advisor takes a fee of $2,000, that effectively reduces your maximum annual investment to $4,000.

2. Flat Retainer Fee

Other fee-only financial advisors charge a flat retainer that is not linked to account size. There are many companies that use the flat retainer pricing model.

3. Hourly Fee

Do all these pricing options still sound too expensive for you?

If so, there’s one final option you may want to consider. Some financial advisors allow you to pay by the hour for their advice. Expect to pay from $150 to $300 an hour for their services.

Why Meet with a Financial Advisor

When I met with John from Frisco Financial Planning, I wanted to find out which kinds of people tend to seek out his services.

“…A majority of my client base, I’m estimating 80% or greater, is of the baby boomer generation. Most of my clients have worked in some industry or trade for a number of years and now they’re inching closer to retirement.”

I also asked John to describe his typical client. He said that his services were cost-effective for people with no consumer debt, who were already saving at least 10% of their income, and who make over $150,000 a year and/or have $250,000 saved already for retirement.”

Related: Our Vanguard Personal Advisor Services Review: Have a Human Advisor Review Your Plan

Financial Advisor Alternatives

To find a good financial advisor alternative, you first need to identify your needs. If you’re looking to get a full financial plan laid out, talking to a human CFP may honestly be your best move.

But if you’re only looking for help with picking investment products or optimizing your asset allocation, you may be able to get the service you need from a robo-advisor.

Pricing for robo-advisors tend to start at around 0.25% of assets under management. Some robo-advisors even offer plans that include access to financial advisors when needed. But you’ll typically have to pay a higher percentage to get access to these plans and they may have account minimums.

Related: The Best Robo-Advisors to Automate Your Investing

My Meeting with a Certified Fee-Only Financial Advisor

On a Fox Business segment, I was asked what investments people could trust in these tough economic times. I somewhat skirted the question and said that everyone should seek the advice of a fee-only financial planner, specifically a Certified Financial Planner (CFP), to help them sort out where they are and what they need to do to get prepared for retirement.

But, afterward, I felt guilty that I’d never taken my own advice. I’d never been to see a CFP. Most of my retirement investing advice had come from books, blogs, and employer retirement plan administrators. That was about to end. I decided I needed to go visit a local CFP.

That’s when I set up an appointment with John Gay, of Frisco Financial Planning. Prior to our meeting, John sent us our full planning report, which contained:

- Asset Allocation and Investments

- Risk Tolerance

- Lifetime Income Planning

- College Education Funding

- Appendix (fund recommendations, life insurance information, and general info)

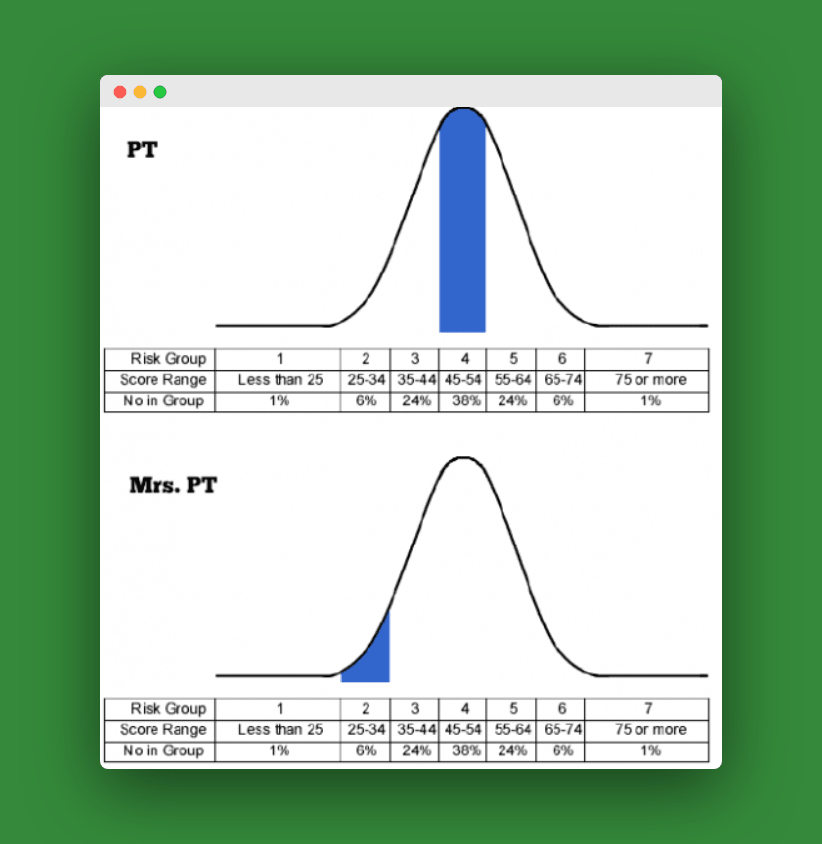

Once I arrived at John’s office, our first order of business was to review the individual risk tolerance scores for me and Mrs. PT.

Our Risk Tolerance

We had each taken a risk profile assessment to evaluate our risk tolerance. The assessment was around 25 or so questions. John revealed our scores and also went over some of the questions where Mrs. PT and I disagreed the most.

As you can see by the charts below, I scored in the average range (52), whereas Mrs. PT scored very low (30) with regard to risk tolerance. I knew she was conservative. But man, did I underestimate by how much! Looking back on the survey, Mrs. PT said that there were some financial terms and concepts that she didn’t fully understand while taking the survey and that this may have affected her results slightly.

However, she stands by her conservative stance and feels like the survey had a needed effect on our allocation.

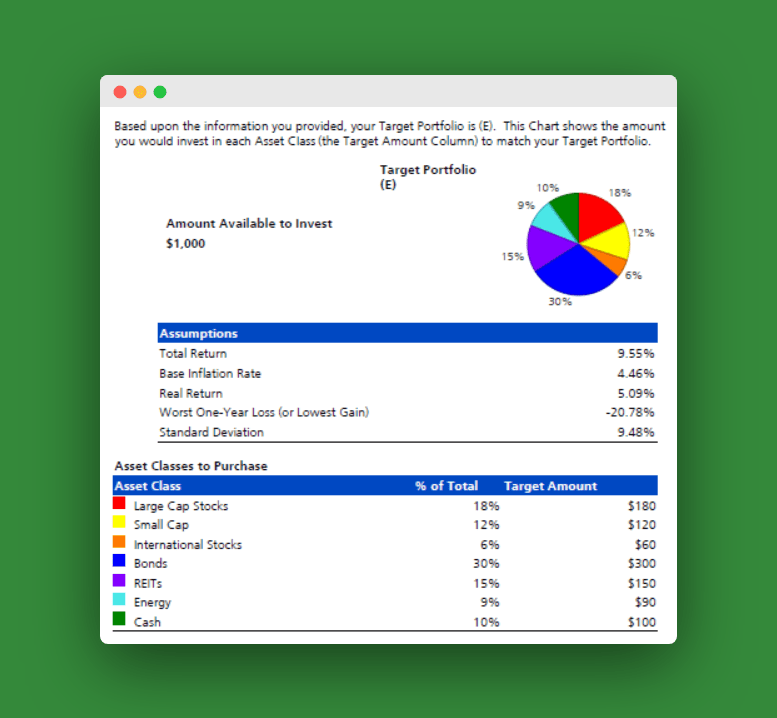

The software that John used took our combined risk tolerance scores and created an asset allocation that aligns with our feelings toward investment risk. Here are the results:

Proposed Asset Allocation

A simpler way to present this would be to say that we should be investing 60% in stocks, 30% in bonds, and 10% in cash equivalents.

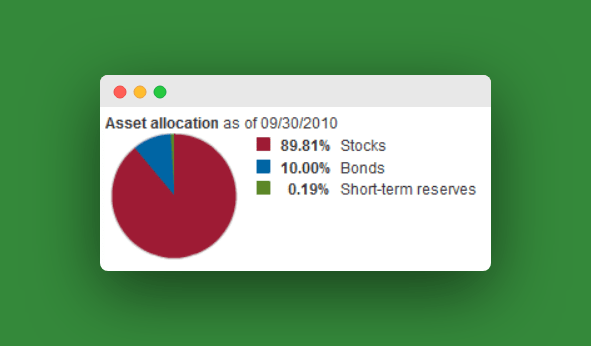

So where are we right now? Well, our current asset allocation is far more aggressive than this. We have most of our retirement assets in stocks, with under 10% in bonds. Our biggest fund is the Vanguard Target Retirement 2040 Fund (VFORX), which has the following allocation:

Most of our other funds are stock-only index funds. Our total current allocation across all funds is probably somewhere around 93% stocks, 7% bonds. That’s a far cry from the allocation proposed.

What this tells you is that I’ve been making most of the retirement investing choices without much regard for Mrs. PT. It appears as though I have some adjustments to make so that our investments reflect our risk tolerance.

Recommended Funds

John then went on to suggest some funds for us to achieve the proper allocation (John loves the ETF):

- Large Cap Stock Fund: SPDR S&P 500 ETF (SPY)

- Small Cap Stock Fund: Vanguard Small Cap ETF (VB)

- International Stock Fund: Vanguard Europe Pacific ETF

- Taxable Bond Fund: Vanguard Total Bond Market ETF (BND)

- Inflation-Indexed Bond Fund: Barclays TIPS Bond ETF (TIP)

- Municipal Bond Fund: ishares S&P Natl. Muni Bond ETF (MUB), SPDR Barclays Short-Term Muni Bond ETF (SHM)

- Real Estate (REIT) Fund: (VEA) Vanguard REIT ETF (VNQ)

- Energy/Commodities Fund: Vanguard Energy ETF (VDE)

- Cash Equivalent Funds: Taxable Treasury Money Market Fund, SPDR Barclays Capital 1-3 mo T-Bill ETF (BIL)

John said that for each of our investment accounts that are over $10,000 (in our case, a Rollover IRA) we should shoot to have these investments. For the accounts at or below 10K (our Roth IRAs, a Traditional IRA, and some misc. funds) we should just pick a Vanguard Target Retirement Fund that mirrors the 60/30/10 allocation.

Related: The Secret to Becoming Your Own Financial Expert

Other Information

John’s session included a discussion of life insurance and college education funding for our kids. I’ll save that info for another post, but I can tell you that John was spot on with his recommendations for term life insurance and 529 college savings plans.

Finally, John stressed the need to build our emergency fund to a level more suitable for a self-employed, sole breadwinner.

Basically, we need to do all we can to build up a bigger cash cushion before we progress much further in our retirement investments. I couldn’t agree more. Right now we have around six months worth of living expenses saved up. He suggested up to 18 months worth. It’s hard for me to ever argue against a bigger emergency fund.

Related: The Complete Guide to 529 College Savings Plans

Conclusion:

Overall, I’m glad that I met with John. I left more confident about our financial future and Mrs. PT and I now have a better grip on how to direct future investments.

You may find similar value in speaking with a financial advisor as well. But it’s important to never stop self-learning about ways to save and invest more wisely. No one, not even a fiduciary CFP, will ever be as passionate about your personal financial goals as you are. Consider using SmartAsset to find a financial advisor.

Have you ever met with a financial planner? If so, what were your main takeaways?