Which Retirement Plan Should You Choose for Your Business? [Solo 401k vs SEP IRA vs SIMPLE IRA]

One of the most common questions I see from new entrepreneurs is about their retirement plan options. Specifically, I see a lot of people talking about the Solo 401k vs SEP IRA vs SIMPLE IRA.

In short, I find that the SEP IRA is the perfect tool for the part-time entrepreneur who still has a 401k through work. The Solo 401(k), on the other hand, is great for anyone who is fully self-employed in a one-person business. Finally, the SIMPLE IRA is best if you’ve started adding employees are no longer eligible for a Solo 401(k) account.

In this guide, we’ll look at the tax and administrative differences of each self-employed retirement account, in both the short and long terms.

Let’s dig into each of these accounts so you can fully understand the differences.

Why It’s So Difficult (Yet So Important!) to Keep Saving For Retirement in Self-Employment

One of the reasons it can be more difficult to save for retirement when you’re self-employed is that you don’t have a set income from month to month. And that can lead to a scarcity mentality and a fear of letting any money go.

Another reason is that you have to do everything yourself, from picking brokers/IRA providers, to setting up your accounts, to actually transferring the funds each month.

When you work as a W2 employee, a lot of these administrative tasks are handled by the HR team. All you have to do is sign a few documents and you’re on your way.

But this is also one of the very reasons why saving for retirement in self-employment is so important. As a self-employed business owner, no one is going to do it for you. If you don’t take the initiative yourself, you’ll be in trouble when you reach retirement.

As a bonus, you get access to special retirement accounts that regular W2 employees don’t. Not only do these small business retirement accounts have higher contribution limits than individual IRAs, but they can actually be combined with them.

Even if you’re a side hustler who also has a W2 day job, opening a self-employed retirement account could be a really smart idea. Why? Because you may be able to tax-shelter a large majority, if not 100%, of your side hustle income.

The Solo 401(k) (Great for Anyone With No Employees Except Spouse)

The Solo 401(k) is just what it sounds like: a 401(k) plan (i.e. tax-deferred retirement plan) for an individual. The individual’s business cannot have employees other than an employed spouse. The owner’s spouse can participate in the Solo 401(k) if an employee of the business.

In many ways, the Solo 401(k) acts just like a regular 401(k) you would get through an employer. Contributions to a Solo 401(k) are not taxed (i.e. they help reduce taxable income) when they are contributed. Money can be withdrawn from the Solo 401(k) without penalty in retirement (at age 59.5), when regular income taxes will be paid on the money withdrawn.

Depending on the provider of the plan, you might be able to borrow money from your Solo 401(k), up to $50,000 or 50% of the value, whichever is less. And many providers will allow you to choose from a wide variety of investments options (cash, CDs, stocks, bonds, funds, etc.) within your 401(k).

But the Solo 401(k) has it’s fair share of unique qualities as well. Because you are both the employer and the employee in your business, you can contribute both the employer’s and the employee’s (salary deferral) portions to the Solo 401(k).

The employee’s contribution limits fall in line with regular 401(k) limits, which are $19,500 for 2020. Note that these contributions are shared with any other 401(k) contributions you are making.

The employer’s contribution limits are set at 25% of compensation. Combined, Solo 401(k) accounts have a total annual contribution limit of $61,000 for 2022.

Read my full review of the Solo 401k.

The SEP IRA (Great for Side Hustlers)

The Simplified Employee Pension Individual Retirement Arrangement (SEP IRA) is very similar to a traditional IRA. A business owner, with or without employees, can establish a SEP IRA.

Contributions to a SEP IRA are deductible and grow tax-deferred until retirement (at age 59 1/2), when regular income taxes will be paid on the money withdrawn. You cannot borrow from a SEP IRA. Most SEP IRA providers will allow you to pick from a big menu of investment options to have within your SEP IRA.

There is no employee deferral contribution to a SEP IRA. All of the contributions must come from the employer. Still, the maximum contribution is the same as the Solo 401k: 25% of compensation, up to $61,000 for 2022.

The fact that the SEP IRA limits contributions to 25% of compensation and doesn’t allow employee contributions could be a problem if you’re fully self-employed.

Read my full review of the SEP IRA.

The SIMPLE IRA (Best Choice When You Can No Longer Use the Solo 401(k)

One of the downsides to Solo 401(k) accounts is that they’re completely off-limits to business owners that have any employees. If you do decide to hire an employee, you’ll Solo 401(k) will convert to a Traditional 401(k).

And, unfortunately, that usually means a lot more red tape and administrative cost. If you have 10 or more employees, a Traditional 401(k) could still be a good option. But if you’re just wanting to hire two or three people, it’s probably overkill.

Could you open a SEP IRA? Yes. But you’ll be required to contribute the same percentage of your employee’s compensation to their SEP accounts as you make to your own. A better option for business owners with only a few employees may be to open a SIMPLE IRA. With these accounts, you can contribute up to $14,000 for 2022.

And the employer contribution requirements are less intimidating. Small business owners can choose one of two options. First, you can choose to match your employees’ contributions up to 3% of their compensation. Or, second, you can choose to make a flat 2% contribution for each employee.

Be sure to sit down with a CPA or other professional to determine which particular plan is right for you.

How to Track Your Self-Employed Retirement Account Savings

Are you saving enough in your self-employed retirement accounts? To answer that question, you’ll first need to know how much money you need to retire.

Some financial experts refer to this as your “financial independence” number. In other words, how much money will you need to save before working becomes optional?

One popular way to find that number is to take your annual expenses and multiply by 25 (assuming a 4% withdrawal rate in retirement). So if you currently spend $40,000 per year, you’d need to save $1 million to be financially independent.

Next, consider how soon you’d like to be financially independent. It could be 5 years or 30 years from now, it’s completely up to you. Once you’ve set your projected retirement date, you’ll want to periodically check to see if your accounts are staying on track.

One great tool for tracking your retirement savings is the OnTrajectory financial planning software.

With OnTrajectory, you can run advanced simulations to see how your plan would perform during various historical time periods. And it can help you answer important questions like how much longer you’ll need to work or whether or not your spouse can move to part-time.

Start your 14-day free trial of the OnTrajectory planner.

Where Can You Open a Self-Employed Retirement Plan?

Ready to open a self-employed retirement plan? Thankfully, you have a lot of great options. Whether you’re looking to start a Solo 401(k), SEP IRA, or SIMPLE IRA, here are few places to consider opening your account.

Vanguard

Vanguard is one of the largest brokers in the world, boasting over $5.6 trillion in assets under management. One of the great things about Vanguard is that the company is literally owned by its investors. Vanguard exists to please its customers not outside shareholders. In fact, as they’ve grown, they’ve consistently slashed their expense ratio as opposed to increasing them.

Vanguard is well-known for their low-cost index funds and ETFs. But they’re far from a one-trick pony. They also have more custom options like target retirement funds and socially responsible investments. Plus, they now offer access to human advisors through their Vanguard Personal Advisor Services platform.

You can literally open any type of self-employed retirement account with Vanguard, including a Solo 410(k), SEP IRA, or SIMPLE IRA. Annual fees are very minimal ranging from $20 to $25 per year. And Vanguard says that retirement account service fees can be waived in some circumstances.

Read our review of Vanguard Personal Advisor Services.

Rocket Dollar

With most brokers, it’s easy to invest in stocks and bonds inside your IRA or 401(k). But it’s typically a lot more difficult and complicated if you want to invest in other asset classes like real estate, precious metals, or startups.

However, Rocket Dollar makes it easy to do that by creating “self-directed” investing accounts for their clients. With Rocket Dollar, you can use your IRA or 401(k) to invest in just about anything (as long as it’s allowed by the IRS).

Rocket Dollar charges a one-time setup fee of $360 when you open a new account. From that point forward, you pay a flat fee of $15 per month. To put that in perspective, if you invested $25,000, that would work out to an annual fee of 0.72%.

Do keep in mind that Rocket Dollar says it can take two to four weeks from the day that you pay your setup fee for your account to be fully funded. If you’re looking for expedited service, you can choose their Rocket Dollar Gold plan, which promises a turnaround time of 15 days.

However, with Rocket Dollar Gold, the setup fee increases to $600 and the monthly fee is also higher at $30 per month.

Alto

Alto is another broker that allows you to use your retirement account to invest in alternative asset classes. With an Alto IRA account, you can use your retirement funds to invest in private equity, venture capital, real estate, cryptocurrency, and more.

To make their alternative investment platform possible, Alto works with an impressive number of partners including Forge, AngelList, YieldStreet, WeFunder, AcreTraders, and many more. Some of their partners only work with accredited investors while other investments are available to everyone.

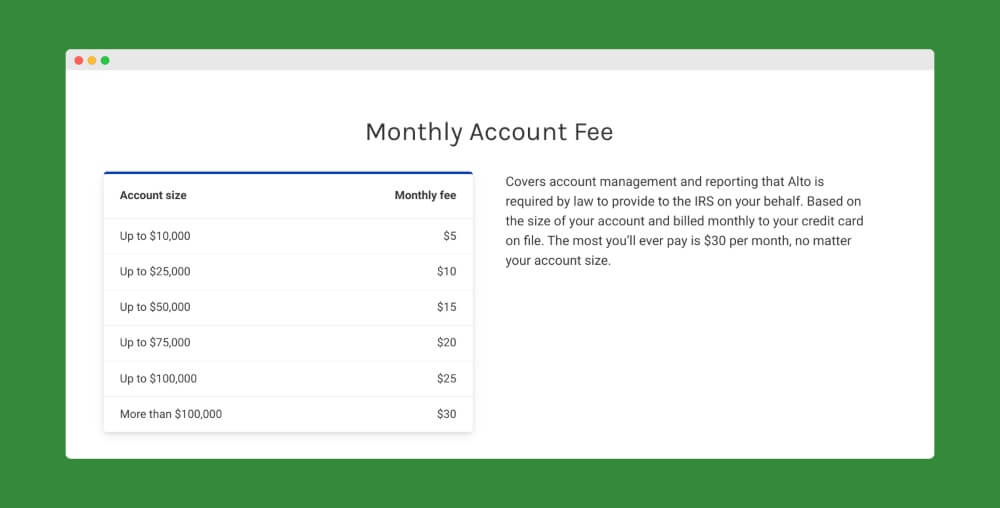

For what they offer, fees on Alto IRA accounts are very reasonable. There are no setup fees whatsoever. And monthly management fees start at only $5 per month (the max is $30).

AltoIRA also charges no transaction fees for transactions under $5,000. Transactions from $5,000 to $10,000 come with $25 fees. And the max transaction fee you’ll ever pay is $150.

Betterment

If you prefer a more hands-off investing approach, Betterment could be a great option. Like other robo-advisors, Betterment will build you a diversified portfolio that matches your risk profile. And they automatically rebalance your account to keep your ratio of stocks to bonds in line with where you want it.

https://www.youtube.com/watch?v=A-9II-zBq1k

For now, Betterment only offers individual IRAs (both Traditional and Roth) and SEP IRAs. They, unfortunately, don’t yet support Solo 410(k) or SIMPLE IRA accounts.

Betterment’s fees start at only 0.25%. But for a higher fee you can also gain access to Certified Financial Planners. Depending on the size of your account, CFP access could cost you from 0.40% to 1.50% of your assets under management. Or you can pay a flat fee for CFP advice — with prices ranging from $199 to $299.

Read my full review of Betterment.

M1 Finance

Based in Dallas, Texas, M1 Finance is a sort of hybrid between a robo-advisor and self-directed investing. Once you choose where to invest your money, M1 Finance will manage your portfolio. This includes periodic rebalancing of your account and dividend reinvesting. Your only responsibilities are to choose your investments and fund your account.

The service is built around what it refers to as “Pies.” These are individual portfolios are a mix of exchange-traded funds (ETFs) and individual stocks. ETFs are a staple of the robo-advisor universe. But, individual stocks are offered by only a few providers, and when they are, they’re usually selected by the robo-advisor.

One of the most compelling features of M1 Finance is that there are no fees for robo-advising. That means no annual advisory fee, no monthly fees and no trading fees. M1 Finance explains it makes money like traditional brokerages, however, but it earns most of its money from making transactions and holding assets instead of through fees. Therefore, believing these revenue streams are more than enough to support a strong, vibrant company, M1 Finance offers investment services to customers at no charge.

Read our review of M1 Finance.

Ally Invest

Ally is probably best known for their bank account products. But their Ally Invest platform is competitive as well. Like Betterment,

First,

Check out our full review of Ally Invest.

Finally,

Worthy Bonds

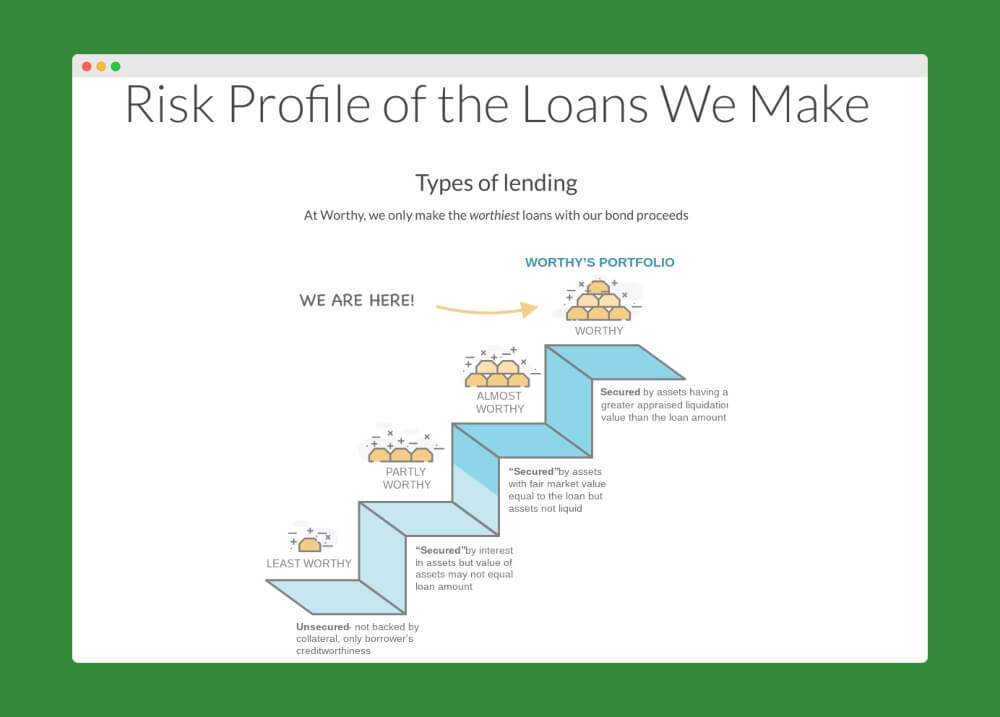

With Worthy, you’ll earn a fixed 5% annual rate of return on bonds that you purchase. Worthy is able to offer this incredible rate of return by using its bond proceeds to invest in asset-backed small business loans. In other words, they only invest in businesses that can secure the loan with actual assets (like real estate.)

The great part about asset-backed loans is that they’re fairly low-risk for lenders. And Worthy spends extra time researching businesses to make sure that they truly are a “worthy” investment. Because of the nature of their loans and their due diligence in choosing businesses to lend to, Worthy is able to confidently promise a 5% return on their bonds.

If you already have a self-directed IRA (like Rocket Dollar or Alto), you can start investing in Worthy Bonds today. Just make sure that you have your account information handy (including your Custodian’s name) when you create your account. If you don’t currently have a self-directed IRA, Worthy can help you open one with their partner, New Direction Trust Company.

Why I Chose a Solo 401(k) from Vanguard

Ultimately I chose a Solo 401k because I was no longer employed by someone else and I didn’t have access to a regular 401(k). I missed being able to defer tens of thousands of dollars in income each year.

Had I still been employed by someone else and working on my business part-time I would likely have used a SEP IRA. I also liked that I could add my wife to the plan at some point, which I’ve done since. Mostly I liked that I could contribute as an employer and an employee for a really large contribution.

Lastly, I would say that I liked that Vanguard offered an easy-to-setup Solo 401k plan that was fee-free for me since I’m at their Voyager service level.

![Which Retirement Plan Should You Choose for Your Business_ [Solo 401k vs SEP IRA vs SIMPLE IRA]](https://ptmoney.com/wp-content/uploads/2013/06/Which-Retirement-Plan-Should-You-Choose-for-Your-Business_-Solo-401k-vs-SEP-IRA-vs-SIMPLE-IRA.png)

I’ll be looking into this next year. The main goal this year is to knock out student loans as much as possible, so there won’t be any business income available to contribute.

I like your focus, Lance. I bet you knock them out sooner than you think. The good thing about the Solo 401k is that you can open it up on Dec 31 and you have until you file taxes to contribute the employer portion. Very flexible on the start.

I opened a solo 401k with Vanguard because of the high limits and the low fees. I could have contributed to a 401k with my employer but I with the solo 401k I can make after-tax contributions with my Roth 401k and the fees for John Hancock funds (through my employer) are quite ridiculous.

I never thought about having a Solo 401k as a substitute for a bad employer sponsored 401k. Good move.

This is a great overview. I’m not currently self-employed so I have an individual Roth and then an employer sponsored 401k. These are working well so far, but I hope to eventually be self employed, so this knowledge will come in handy. Thanks.

Thanks, Jake. You know, I know several part-time entrepreneurs who use the Roth, 401k, and a SEP IRA (i.e. the trifecta) to max out their contributions.