How I’m Using the QSEHRA [Managed by Take Command Health] to Deduct My Employees’ Healthcare Benefit

In this article, I’ll share how I set up a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) to deduct the healthcare expense reimbursement benefit I offer my three full-time employees. In short, this is how I help my team with their health care needs (and get a tax deduction for it) without having to buy an expensive group health insurance policy.

A QSEHRA is a plan that allows employers to reimburse employees for their health insurance premiums and out of pocket medical expenses tax-free. Employers can cap their monthly per-employee expenses at an amount of their choice.

If you have a small team like me (or if you work on a small team) you should look into this.

How I Learned I Needed a QSEHRA

Here’s a little backstory. As most of you know, in addition to PT Money, I’m also the CEO of FinCon. Thankfully, FinCon has been growing! But like any small business, we’ve run into growing pains. A big one was health insurance–I couldn’t recruit the right people to my team without accounting for it in some way, but it seemed like such a big headache and expense.

That’s when we learned about a new option called a QSEHRA. It’s lean, it’s flexible, it’s tax-advantaged, and it’s budget-friendly. A QSEHRA allows small businesses to set aside a fixed health allowance each month that employees can then use for their own individual health insurance or medical expenses.

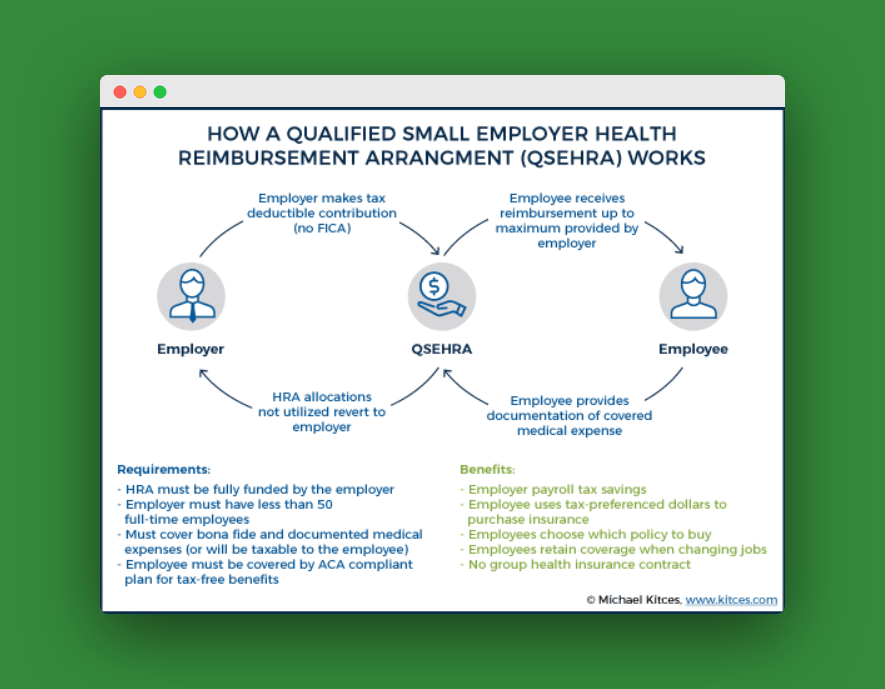

QSEHRA is pretty new, but I think it’s going to take-off and I’d recommend any small or growing business take a look at it. Michael Kitces has a great write up on them. Health Reimbursement Arrangements (HRAs) have been around forever. This is a new flavor of HRA that was created at the end of 2016 through bipartisan legislation called the 21st Century Cures Act.

A new startup company, Take Command Health, pitched the idea one year at FinCon and won 2nd place in our pitch competition for their idea. They’ve put together an excellent guide that explains how a QSEHRA works.

Bottom line: with the QSEHRA I could offer the benefits my employees needed without administering a clunky group plan. We signed up to let Take Command Health handle the arrangement and have been using a QSEHRA for a while now.

Here’s TakeCommand’s explainer video on the QSEHRA:

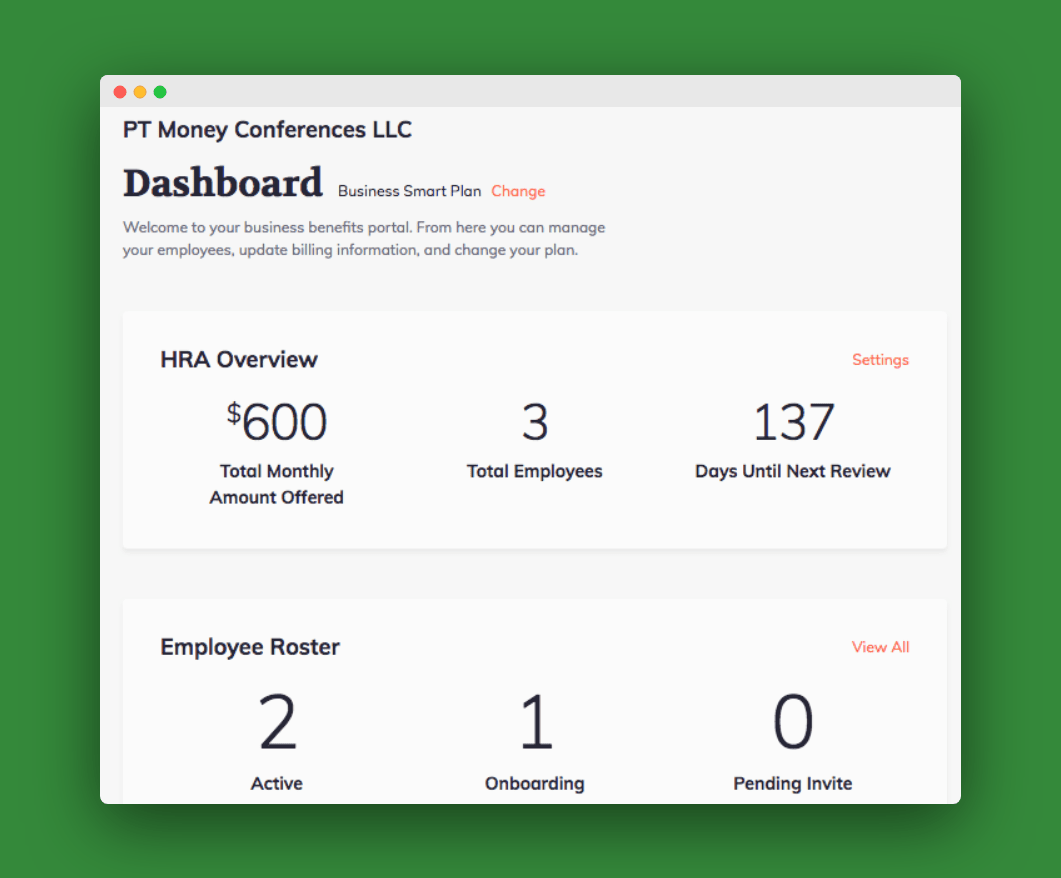

The FinCon QSEHRA

Our QSEHRA looks like this:

I’m paying $600 to three employees so they can reimburse their premiums. Two of the employees are single (eligible for $150) and one has a family (eligible for $300). One employee has yet to sign up for the benefit. And I’m using the “Business Smart Plan” from Take Command Health, which adds a few extra benefits to employees for $15/mo each.

In total, I pay $92 a month for this service. $15 per employee for the HRA and the additional $15 per employee for the Business Smart Plan. I may eventually turn that piece off since all of my employees use Medishare and receive most of these benefits already. Check out our full Medishare review here.

You’ll notice I am not on the plan myself. That’s because I claim S-Corp status when I file my taxes and I’m the owner. I can’t participate. But I can still deduct my own health care costs. So, no biggie.

The Advantages of a QSEHRA

Let’s break down the pros here to see if the QSEHRA might be right for you.

It’s tax-efficient: Before we signed up for QSEHRA, we had come up with a common workaround solution: I was just adding an extra “health stipend” onto my employees’ salary for them to buy what they needed: health insurance premiums, medical sharing payments, general medical expenses, etc. The problem is that money gets taxed like income.

A QSEHRA basically accomplishes the same thing as a health stipend but is tax-free. That can make a big difference. Consider a 10 person company offering a $300/month health stipend:

| Taxes & Fees | Taxable "Health Stipend" | QSEHRA |

|---|---|---|

| Reimbursement Amount | $3,000 | $3,000 |

| Employee Income Tax (~25%) | 750 | 0 |

| Employer Payroll Tax (~15%) | 450 | 0 |

| Total Monthly Taxes | $1,150 | 0 |

Boosts retention: Wondering what the number one factor is for millennials and job-seekers considering a new job? You guessed it–health insurance benefits. Without a competitive benefits package, the best and brightest might choose to go elsewhere. Another perk for employees is that they can choose the best plan for them instead of being looped into a group plan that might not cover their doctors, their prescriptions, or their health needs.

Saves time: Selecting and administering a group plan takes a lot of time and effort. Choosing the right QSEHRA administration platform will save you time down the road as well. Take Command Health’s QSEHRA platform on-boards employees, generates plan documents, ensures that you remain compliant, and makes tax time easier.

Saves your budget: These costs are predictable. Unlike a group plan that might creep up in costs year after year, you control the amount contributed to a QSEHRA. It’s on your terms and within your budget. Wondering what happens to the leftover funds if they aren’t used? It stays with the business and doesn’t rollover. That means you aren’t responsible for funding a bunch of accounts; you only pay out when an employee submits an expense for reimbursement. Sweet deal!

It’s flexible: You can design your QSEHRA to fit your needs. Want to just reimburse for premiums like me? Great. Want to add qualified medical expenses to the deal? Even better. Want to scale the contributions based on age, status, or family size? You can do that too (as long as it’s fair!)

Disadvantages of a QSEHRA

Of course, it’s not a perfect plan. Here are the downsides:

New and kind of confusing: I’m a CPA and I have trouble wrapping my head around some of the complexities involved with this arrangement. Thankfully, Take Command Health has both excellent education (setup guides and tax law coverage on their blog) and excellent support. When I have a question I simply email their support team and a response comes quickly–oftentimes from their CEO, Jack Hooper.

Owners can’t participate: As the owner of the company, I can’t actually participate in the arrangement myself. I can still give myself this benefit (the healthcare reimbursement), but I can’t deduct it using a QSEHRA. Thankfully, as the owner, I can deduct my own health insurance above-the-line on my personal return.

UPDATE: Individual Coverage HRA Available in 2020

Beginning January 1, 2020, there is a new tax-advantaged HRA that employers can utilize. It’s called the Individual Coverage HRA (ICHRA) and it’s basically a souped-up version of QSEHRA.

ICHRA will allow employers to have more control over their benefits budget. Perhaps the best feature is that there are no minimum or maximum contribution rates. This will help small businesses be able to offer more value to employees and hopefully be able to retain quality talent. Allowances can be increased too, based on your employee’s age or number of dependents.

Employers using an ICHRA will be able to reimburse employees tax-free for individual insurance and medical expenses. ICHRA takes away some of the red tape and hassles associated with QSEHRA. Employees decide which benefits go with each class of employees (there are 11+ customizable classes). After setting monthly allowances, your work as an employer is basically done. Employees choose whatever plan they want from the individual marketplace.

Here’s a guide that explains it further.

The good news is that ICHRA offers flexibility. It can be offered with a group plan if you want to keep certain employees under an existing plan.

Take Command Health will be adding the Individual Coverage HRA to their platform of products. This is not replacing QSEHRA, but will be offered alongside it.

My Experience Setting Up a QSEHRA with Take Command Health

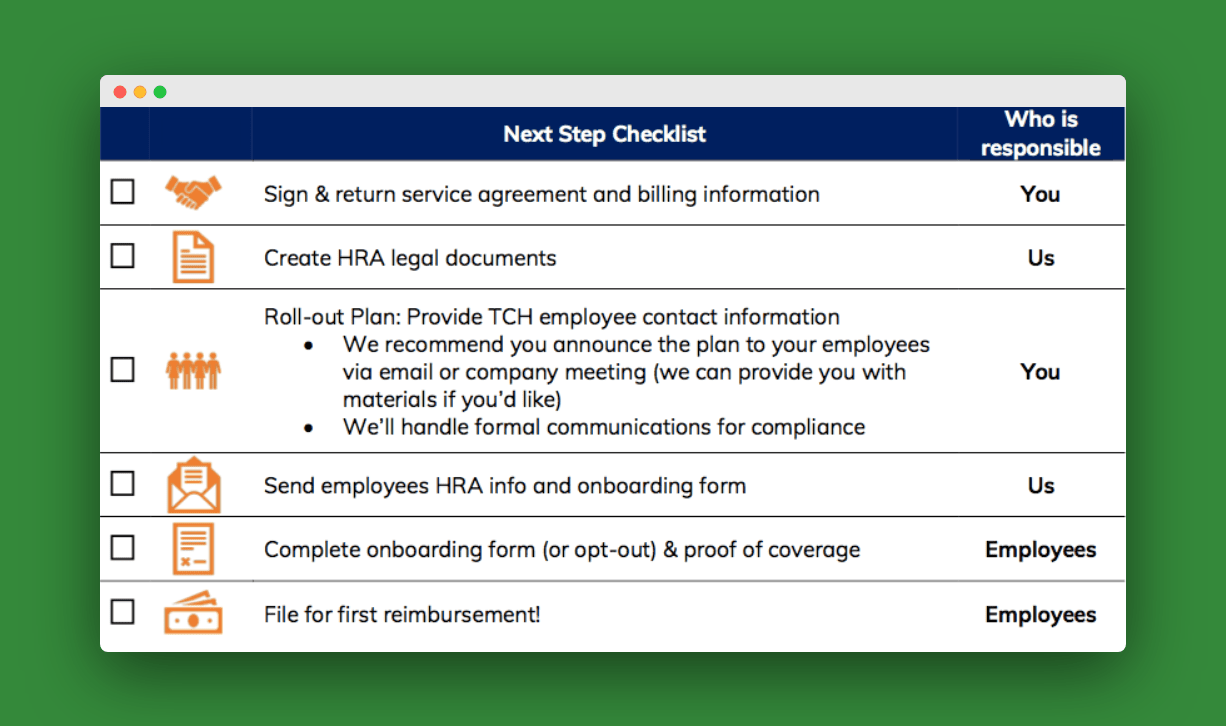

Once I wrapped my head around how the plan works, it was pretty easy to just let Take Command Health set it up! At a high level, there are a few agreements to sign, forms to prepare, and communication with the employees. Then, the Take Command Health dashboard and my payroll service take care of the rest. For more of the details of how my setup went down, click show

The exact next steps were:

- Take Command Health: Create HRA legal documents

- Me: Roll-out Plan: Provide Take Command my employees’ contact information and personally introduce it while they handle the formal intro.

- Take Command Health: Send employees HRA info and onboarding form

- Employees: Complete on-boarding form and provide proof of coverage (my employees use Medishare too)

- Employees: File for reimbursement

Overall I’m pleased with how this arrangement has worked out. Because of their knowledge and customer service Take Command Health is a great company to use if you need a QSEHRA for your own company.

Let me know in the comments if you’re considering it and/or if you have any questions for me or Jack and his team.

In this article (https://ptmoney.com/medishare-review/) you wrote that “ou may be able to deduct the cost of reimbursing them for their Medi-Share monthly share. I did this myself by setting up a QSEHRA.” implying that you benefit from setting up QSEHRA. Here you said you are not participating in the plan because you are the owner.

Contradicting information. How do you deduct Medishare premiums?

Great catch, Ivan. I need to update my reviews. It’s a bit complicated but I’ll give it a shot to explain here. When I first signed up for the qsehra the rules were still fuzzy and it looked like my employees and I could all use it and deduct our medical sharing premium. Then I found out the owner of an SCorp couldn’t participate. So I dropped out. Then I found out Medi-Share alone probably wouldn’t pass the requirement for “insurance coverage” even though it is exempt from Obamacare. So I now have dropped the qsehra entirely. And I just reimburse my employees a bit more to make up for the lack of the deduction. Make sense?

What leads you to believe that you can reimburse Medishare premiums on a tax-free basis via a QSEHRA? QSEHRA only allows tax-free reimbursements after proof of minimum essential coverage, but Medishare is not considered minimum essential coverage. Yes, Medishare members are except from the ACA requirement for MEC, but that is not the same as having proof of MEC.

Good question. One I had too. Take Command addresses it here https://www.takecommandhealth.com/blog/medi-share-sharing-ministries-small-business-hra-qsehra I’m comfortable with that line of reasoning and I eagerly await any clarification from regulators.

Thanks. I don’t quite agree with the leap in logic but it’s an interesting interpretation.