The Paycheck Protection Program (PPP) – What We Know & Where to Apply

If you’re like me and you run a small business, you could qualify for the Paycheck Protection Program (PPP).

This looks to be a promising opportunity for small business owners and the self-employed to recoup some of the damages inflicted by the economic and social effects of COVID-19 and the subsequent government response.

The PPP will allow you to continue to pay yourself, your employees, and possibly your independent contractors (those you issued a Form 1099) for an eight week period through June 30, 2020!

Look, I’m no fan of taking out loans for your business. But this particular program essentially created a grant (free money) for you to use to pay your employees, as well as your rent (see below for all qualifying expenses), through this rough patch we’re experiencing.

Quick Navigation

- Summary of the Paycheck Protection Program

- Paycheck Protection Program Details (eligibility, loan amount, timing, forgiveness, etc)

- Paycheck Protection Program Calculator

- Banks Taking Applications

- Application Form for PPP

- Documents Needed to Apply

- Other PPP Questions & Resources

April 24, 2020 Updates:

- Today the President signed into law the PPP “Enhancement” Act. This adds an additional 320 Billion to the program. The SBA will start processing applications again next Monday, the 27th at 10:30 AM ET.

- Get your application (re)submitted to an approved lender ASAP. I’d recommend your own business banker, as well as a number of FinTech options, like BlueVine via Nav, Kabbage, LoanBuilder by PayPal, and Lendio. There is no risk from submitting multiple applications.

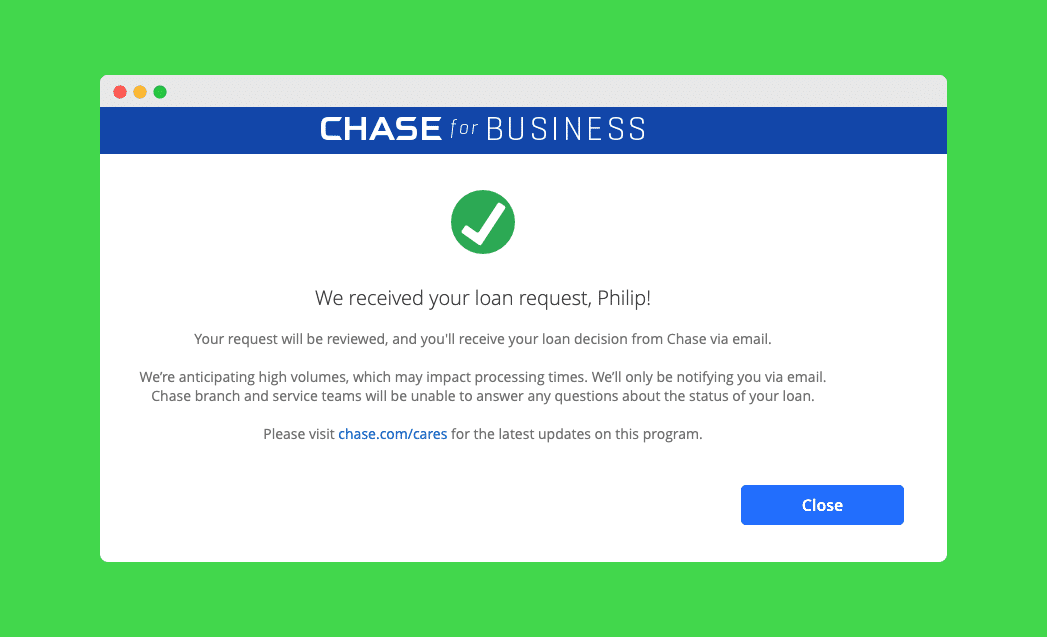

- I finally heard from Chase about my other two businesses. One is ready to be submitted to the SBA by Chase on Monday. The other loan was apparently held up by an error. I apparently didn’t include the correct payroll documentation. Chase encouraged me to re-submit my application and stated that they would “consider [my] earliest submission date when processing [my] new application.” I resubmitted my application today.

April 18, 2020 Updates:

- As I’m sure you’ve heard, the funding for the PPP has run dry. I’m hopeful Congress will appropriate more funds next week, but I would not be surprised if it takes longer or the extra funds never materialize.

- While I’m disappointed that the funds ran out so quickly, I’m mostly disappointed in my business banker, Chase. They left me in the dark throughout the entire process. While I was able to get one loan funded through them, my other two (larger) loans didn’t get funded AND they never told me otherwise.

- Had I known Chase wasn’t going to fund me – which we now know they prioritized certain businesses over others and didn’t fund loans in order of application – I would have applied elsewhere.

- So today I’m starting the process of applying with Bluevine through Nav.com and LoanBuilder by PayPal. Yes, at both places, for both businesses. Yes, this means I’m making multiple PPP applications. But this is the choice I’m left with, and I’m only sorry I didn’t do this earlier. I strongly suggest you consider doing the same.

April 16, 2020 Updates:

- Yesterday at 4:15 PM I received an email from Chase that one of my PPP loans had been approved. The email stated that “Chase will deposit your loan funds into your oldest Chase Business Banking checking account within the next three business days.”

- This morning I got funded! I just noticed a couple of new pending deposits into my business checking account. One for the amount of my approved PPP loan, and one for $2,000 ($1,000 for each of my employees), which I’m assuming is the EIDL advance. See screenshot below.

April 14, 2020 Updates:

- Still no word from Chase on my PPP loan application. I did receive the random email from the SBA officially confirming that the EIDL advance will be given out in $1,000 per employee increments. Those who have already received the EIDL Advance have reported getting this email three days before funding.

- Also, the Treasury issued a new Interim Final Rule addressing the requirements for the self-employed when applying for the PPP loan. Notable takeaway: if you are self-employed and haven’t filed your 2019 taxes, you need to fill out a 1040 Schedule C and turn it in with your PPP application. Line 31 from the Schedule C should be used in your payroll costs calculation.

April 9, 2020 Updates:

- I haven’t been approved or funded for my PPP applications. I talked to my Chase banker today and she didn’t have much of an update other than saying (1) some Chase business customers have received funding for their PPP, and (2) I should just watch my email for approval info.

- Additional funding for the PPP hasn’t passed yet, but it was promising to see it go up for a vote in the Senate so quickly.

- Capital One hasn’t opened up PPP applications for their small business customers.

- Senator Shaheen issued a letter to the Treasury and the SBA urging them to change their ruling regarding the $10k EIDL grant.

April 7, 2020 Updates:

- The US Treasury has asked Congress for an additional $250 billion for the PPP.

- The US Treasury has also released more FAQs regarding the PPP. My big takeaway: you can use 2019 payroll data (vs previous 12 months) for the application.

April 6, 2020 Updates:

- The Chase online application for PPP is up! You can visit https://recovery.chase.com/cares1/sba-loan-forgiveness to get started with your app if you are a current customer (you are required to login).

- I applied for my businesses. I submitted my W-3, a summary sheet showing how I made the Payroll Costs calculation (I just made it quickly in Apple Notes and saved it as a PDF), and I also uploaded my 2018 business tax return. That’s it! I’m in!

- In EIDL news, this press release from the Massachusetts SBA came out today and noted, among other FAQs: “EIDL Loan advances will start to be distributed this week. $1000 per employee up to $10,000 max”.

April 5, 2020 Updates:

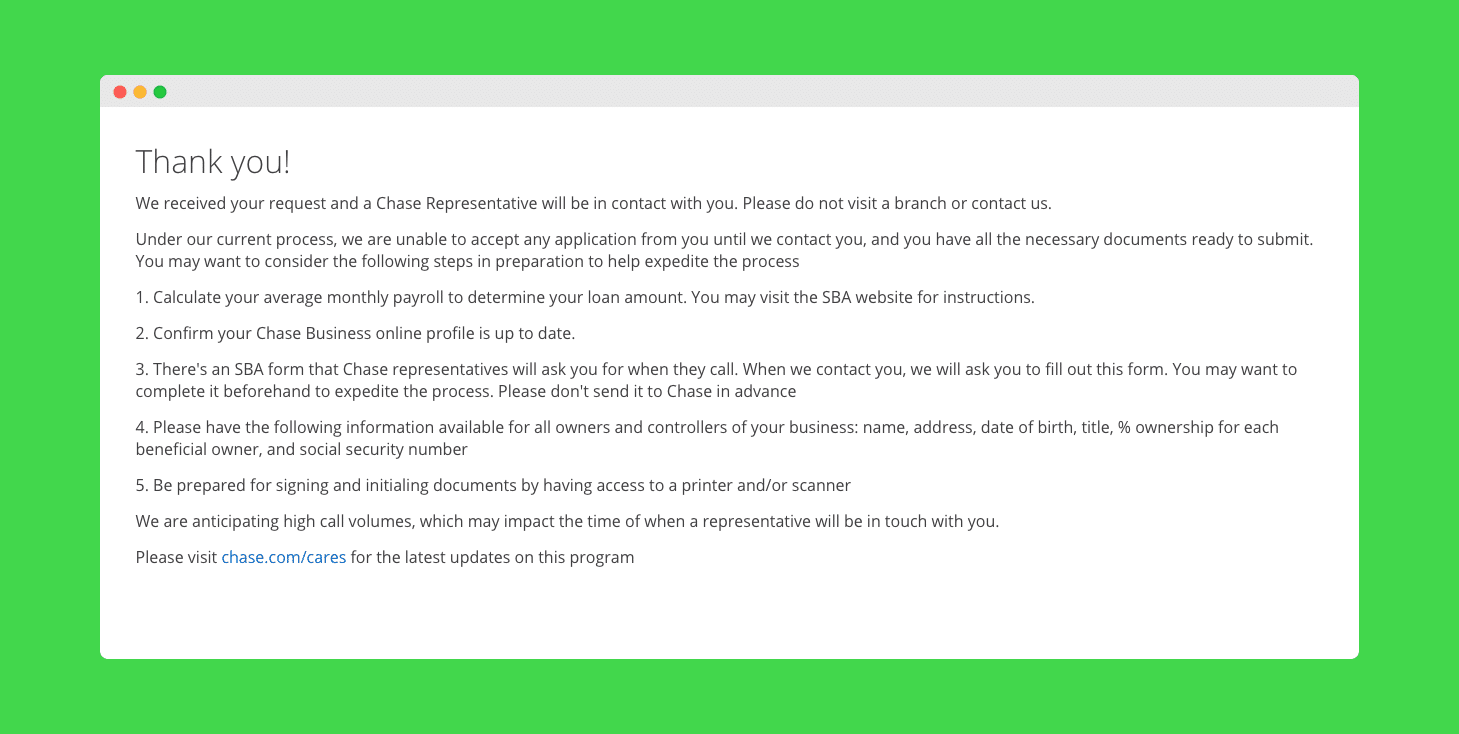

- Chase emailed me today letting me know that soon I would be notified about 1. their online application portal being open, or 2. applying for the PPP over the phone with a business representative.

- Documents I have ready for my application as soon as Chase opens the gates: completed & signed Form 2483, 2019 W-3 Form, 941s for all 2019 quarters, 940 for 2019, my Texas franchise tax certification, and a Addendum with a listing on all the businesses I own.

- I created a central place for all COVID-19 resources from my website. It includes CARES Act info, tips for making money during this time, and tips for your personal finances.

April 4, 2020 Updates:

- I just heard from a friend on Twitter who’s in touch with a Chase bank Business Relationship Manager, “We are strenuously working to get a website based application up and running. Until then, Business Relationship Managers like myself will be calling business customers to take formal applications this weekend and beyond.” That’s promising. My relationship manager hasn’t called me yet.

- Nav just went live with their full application, saying “this secure, digital application will feed directly into your official application once lenders come online early next week.” I’ve been told by a Nav rep that you will have a chance to officially submit this application once they’ve matched you. So, if you wanted to apply to this, it won’t duplicate your efforts, with say Chase, once they have something up. Hedge your bets, basically. (full disclosure, Nav will likely be getting a commission from the bank they ultimately refer you to, and I may be getting a percentage of that commission as well)

- After some further thought, I’ve decided to leave my 1099 contractors out of the equation. I’ll email them next week to suggest they apply for the PPP themselves next Friday, the 10th. Hopefully, the EIDL $10k grant comes through and I can use that to fund contractor activity for the next month or so.

- Bank of America is changing their PPP policy to allow for all business customers to apply, not just those with existing loans.

- A small business owner with less than 50 employees reported on Reddit 2 hours ago that they were officially approved for funds.

- I was quoted in Forbes on the negative fallout of the initial days of the PPP launch. Follow Ryan Guina on Forbes for more updates.

- Excellent Twitter thread from Senator Rubio on the problems currently between banks/SBA/Treasury that he’s committed to helping clear ASAP.

- President Trump tweeting about increasing funding for PPP:

I will immediately ask Congress for more money to support small businesses under the #PPPloan if the allocated money runs out. So far, way ahead of schedule. @BankofAmerica & community banks are rocking! @SBAgov @USTreasury

— Donald J. Trump (@realDonaldTrump) April 4, 2020

April 3, 2020 Updates:

I have not been able to submit my application. But, I’ve placed myself into the Chase PPP “queue”. If you’re a Chase business customer you can head to https://recovery.chase.com/cares1/sba-loan-forgiveness and fill out the two page form. At the end, you’ll find out that Chase now needs to speak to you directly to complete the application. Here’s the screenshot:

The form they reference in the note is the new SBA PPP form linked below.

Most other big banks aren’t taking applications. I’ve heard of no online portals being open with the exception of Bank of America, who has opened a portal for existing business loan customers.

Secretary Mnuchin keeps tweeting progress from his SBA reporting information. Where is this activity actually happening other than BOA?

UPDATE over $1,800,000,000 #PPPloan now processed by @SBAgov mostly all from community banks. Big banks taking in large amounts but not yet submitted in these numbers! #CARESAct #SmallBusiness

— Steven Mnuchin (@stevenmnuchin1) April 3, 2020

It’s frustrating.

Midnight April 2, 2020 Updates:

Right now believe it or not there is still confusion on the inclusion of 1099 contractors in your payroll cost calculations. The final rules from the SBA are out and although it explicitly says independent contractors are excluded from their employer’s payroll cost calculations, it does state that you are eligible if:

“You were in operation on February 15, 2020 and either had employees for whom you paid salaries and payroll taxes or paid independent contractors, as reported on a Form 1099-MISC.“

What I’m doing: It’s past midnight on the East Coast and so I’m making a last-minute judgment call to include my 1099 contractors in my payroll calculations. I’m submitting my applications (here’s the new final form) with that data included. I’ll report back with what the bank says tomorrow.

Now with regard to the banks, several closed business for the day before Secretary Mnuchin issued the final rules. And on their way out the door, they said they were NOT going to be processing PPP applications on Friday, April 3rd. This includes my bank, Chase.

Since there are a limited number of funds available and this will be a race to see who can get their applications in first, I am searching for alternative banks. My advertising partner, Nav (the small business lending broker and credit score company) sent an email tonight explaining that they “will collect the same information as a bank and match you to multiple SBA lenders as they come online.”

I’ve submitted my pre-application with Nav and I’ll wait to hear from them overnight or first thing in the morning. My second option is FNBO. They have a branch near my home and I’ve been in contact with them today and they said they would let non-customers apply with them.

That’s it for now. I’ll update you when I have more info.

April 2, 2020 Updates:

- Official statement from Chase bank: “Financial institutions like ours are still awaiting guidance from the SBA and the U.S. Treasury. As a result, Chase will most likely not be able to start accepting applications on Friday, April 3rd, as we had hoped.”

- In today’s White House Press briefing Secretary Mnuchin stated that the program WILL launch tomorrow, April 3rd. And the interest rate will now be set at 1%.

- It’s here. The interim final rule from the SBA on the PPP. I’m digging through this now and I did spot that independent contractors are, in fact, to be excluded from the payroll cost calculations. I’m assuming banks are absorbing this now and implementing this and the new final application into their systems. Applications for the PPP should be able to start tomorrow!

- Important Update re: Using Independent Contractors in your Payroll Costs Calculation – I’ve had a chance to analyze the Treasury guidance to borrowers and the sample application and I’m fairly certain that their stance to SBA lender banks will be to only use your full-time and part-time employee payroll data to establish your payroll costs, and therefore, your loan amount. This is disappointing because (1) I think the law actually speaks to allowing contractors in your payroll costs calculations, and (2) many small businesses only use independent contractors. Now, these employers won’t be able to use that data for their loans. This is an evolving situation, so this may turn out to be a non-issue.

- President Trump stated during his March 31 daily press briefing that PPP applications will be taken starting this Friday, April 3rd. The Treasury Dept issued guidance to borrowers, lenders, and a sample application. Highlights from Treasury guidance to borrowers:

- Small businesses can apply April 3 and self-employed can apply April 10.

- This loan has a maturity of 2 years and an interest rate of .5%.

- Not more than 25% of the forgiven amount may be for non-payroll costs.

- Loan payments will be deferred for 6 months.

- Chase just emailed some of their business customers stating: you need a Chase business checking account to apply with them; the application with Chase will be entirely online. Chase also shared what information should be needed for the application. See below.

- Calculate your maximum loan amount using the PPP Loan Calculator below.

- Ready to apply? Jump to the list of banks and institutions currently taking pre-applications. Banks should begin taking full applications from small businesses by Friday, April 3 and from the self-employed by April 10. This is a confusing distinction likely caused by a rush to get this out. The implication here is that if you have employees you can apply on the April 3 date, but if it’s just you and your net earnings, you’ll have to wait to April 10 to apply.

- Consider also applying for the EDIL at SBA.gov now that they have a streamlined application and you may qualify for the forgivable $10,000 grant. You might be able to have both the EDIL and the PPP depending on your expenses.

- I joined Rachel Brenke for a special episode of the Business Bites Podcast to discuss the Paycheck Protection Program. Listen in…

All three of my businesses were (and should continue to be) negatively affected by COVID-19. Sales are down, partnerships have been dissolved, booked deals were lost or postponed indefinitely, and in some cases, even changes in service provider technology has disrupted business as usual. Therefore, I’m applying for a PPP loan for all three businesses.

After I did some research and spoke with others familiar with the program, I decided to share what I found out here. I’ll keep this piece updated as I get more information and work through the application process.

Disclaimer: I’m not your CPA. I don’t know your particular situation. The information I’m sharing in this article is just information, not individual advice. Don’t act on anything without working with your CPA or other professional first.

Note that the newly enacted Coronavirus Aid, Relief, and Economic Security (CARES) Act includes a number of things (like those personal stimulus checks), but in this piece, I’m focused on the $350 billion section known as Paycheck Protection Program or PPP (also know as the Small Business Interruption Loan in the Senate version of the bill).

Quick Summary of the Paycheck Protection Program Loan

- Rate:

4% fixed0.5%1.0% - Amount of Loan: 2.5x average monthly payroll (including owner & 1099 contractors)

- Terms:

Up to 102 years - First 6

-12months of payments are deferred - No collateral or personal guarantee required

- Loan forgiveness on funds used for qualifying expenses (e.g. payroll, rent, etc.)

- Application will go through SBA approved banks – possibly your own business bank

- Rate:

Yes, you read that correctly. The loan is 100% forgiven (essentially making it a grant) for all of your qualifying expenses.

This is money the federal government is dumping on our economy through small businesses to help us ensure people get paid salaries and for contract work. If you’ve been affected and you’ve got staff you continue to support I encourage you to apply.

Related: How to Get Unemployment Pay if You’re Self-Employed (Including Gig Workers and Freelancers)

Paycheck Protection Program Details (eligibility, loan amount, timing, forgiveness, etc)

Eligibility. To be eligible for the PPP you must be a small business, sole proprietor, “side hustler”, or non-profit that has fewer than 500 employees. You must have been in business prior to February 15, 2020. And you generally need to (or expect to) experience negative effects from COVID-19 on your business (e.g. loss of sales). Specifically,

“An eligible recipient receiving loan forgiveness under this section shall make a good faith certification that the uncertainty of current economic conditions justifies the loan request to support the ongoing operations of the borrower, and acknowledges that funds will be used to retain workers and maintain payroll.”

From my understanding so far, this program has a very wide application.

https://twitter.com/ptmoney/status/1244001260149317635

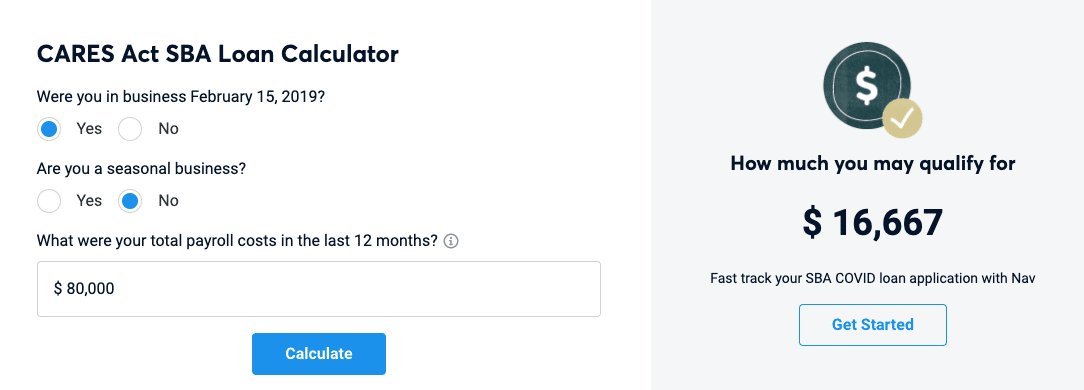

Loan Amount. You can borrow up to the lesser of 2.5 times your average monthly (U.S. based) payroll for the last 12 months, or $10 million dollars. “Payroll” generally includes salaries and benefits minus the payroll taxes paid and is capped at $100,000 per employee.

You can also include amounts paid to U.S. based part-time workers and contractors in your payroll calculations. Update: It looks like the Treasury is interpreting the law in a way that would not allow you to use independent contractors in your payroll cost calculations. I personally think they are ignoring the “compensation to” portion of the sentence below, but I’m not the Treasury and I don’t get to make the rules.

You don’t need to put up collateral and you don’t need to pay any fees to initiate this loan.

Calculate your loan amount. As an example, let’s say you paid $150,000 in salaries and $50,000 in benefits over the designated timeframe. You would have a total of $200,000 in total payroll costs. You would then divide that number by 12 to get your average monthly payroll of $16,667. You would be eligible to borrow 2.5 times that amount, or $41,667.50, through the PPP.

Loan forgiveness. Now here’s the exciting part. Any qualifying expenses you incur in an eight week period during the program window (starting from the date of your loan and ending no later than June 30, 2020), are eligible for loan forgiveness.

Qualifying expenses include salaries, of course. But they also include rent, mortgage payments, group health insurance payments, utilities, interest on debts, and some other minor expenses.

Paying back the loan. Each bank will have to develop a process. But generally speaking, at the end of the eight weeks, you simply show evidence of your qualifying expenses to your lender bank and they forgive the equivalent amount on your loan.

Any remaining loan amount will then need to be repaid. You’ll have up to 10 2 years to pay back the loan, at a fixed rate of 4% maximum 0.5% 1%. The first 6 to 12 months of payments can be deferred.

Paycheck Protection Program Calculator

Enter your business’ total payroll cost data in the fields below and calculate your maximum loan amount under the Paycheck Protection Program.

Temporarily Unavailable

Seasonal Employee PPP Calculator

Our partner Nav has a helpful calculator that takes into account any seasonal employees you have. Try it out.

Banks/Lenders Taking Paycheck Protection Program Applications

You have until June 30, 2020, to apply. But these loans will be issued on a first-come, first-served basis. I would apply quickly.

Banks should begin taking full applications from small businesses by Friday, April 3 and from the self-employed by April 10.

Since the federal government is using the SBA existing program to deliver these loans you should be able to apply for the PPP at any of the current SBA approved banks and even more banks as long as they are FDIC. There is no listing (from what I can see) of these SBA approved banks.

The SBA website normally funnels you to a bank using a matching program, but their system doesn’t appear to be working currently.

Over social media I’ve discovered several banks & institutions already taking contact information (not full-blown applications yet) for those interested in applying for the PPP:

- Nav (broker who will match you with banks taking applications – might be the fastest way to apply)

- US Bank (now taking online applications with current customers; opening to non-customers soon)

- Sunrise Banks (now taking applications by email)

- Key Bank (open to customers)

- Live Oak Bank (only working with existing customers; suggesting non-customers look elsewhere)

While these aren’t full applications yet, these banks are signaling that they will be quick to roll out these loans. A good sign if you are considering one of the above banks.

A good indicator for which banks might be able to act quickly is who has historically produced a lot of SBA loans. This information is public, and you can actually see from the March 2020 data who the top SBA lenders are.

Beyond those banks, the lender StreetShares has a PPP calculator that will help you estimate your possible loan amount. They promise to put you in touch with an approved bank very shortly.

I’ve contacted all of these banks, including my own bank, Chase. My Chase banker got back to me and shared that she’ll be calling me as soon as they get guidance from the SBA. She also shared a landing page with me where updates to the Chase process will be released.

I’ll likely apply with Chase for all three loans, but we will see.

Paycheck Protection Program Application Form

Here is the final (fillable) form from the SBA that you can use to apply for the Paycheck Protection Program.

The SBA released a sample application form earlier, but this final version had some slight tweaks.

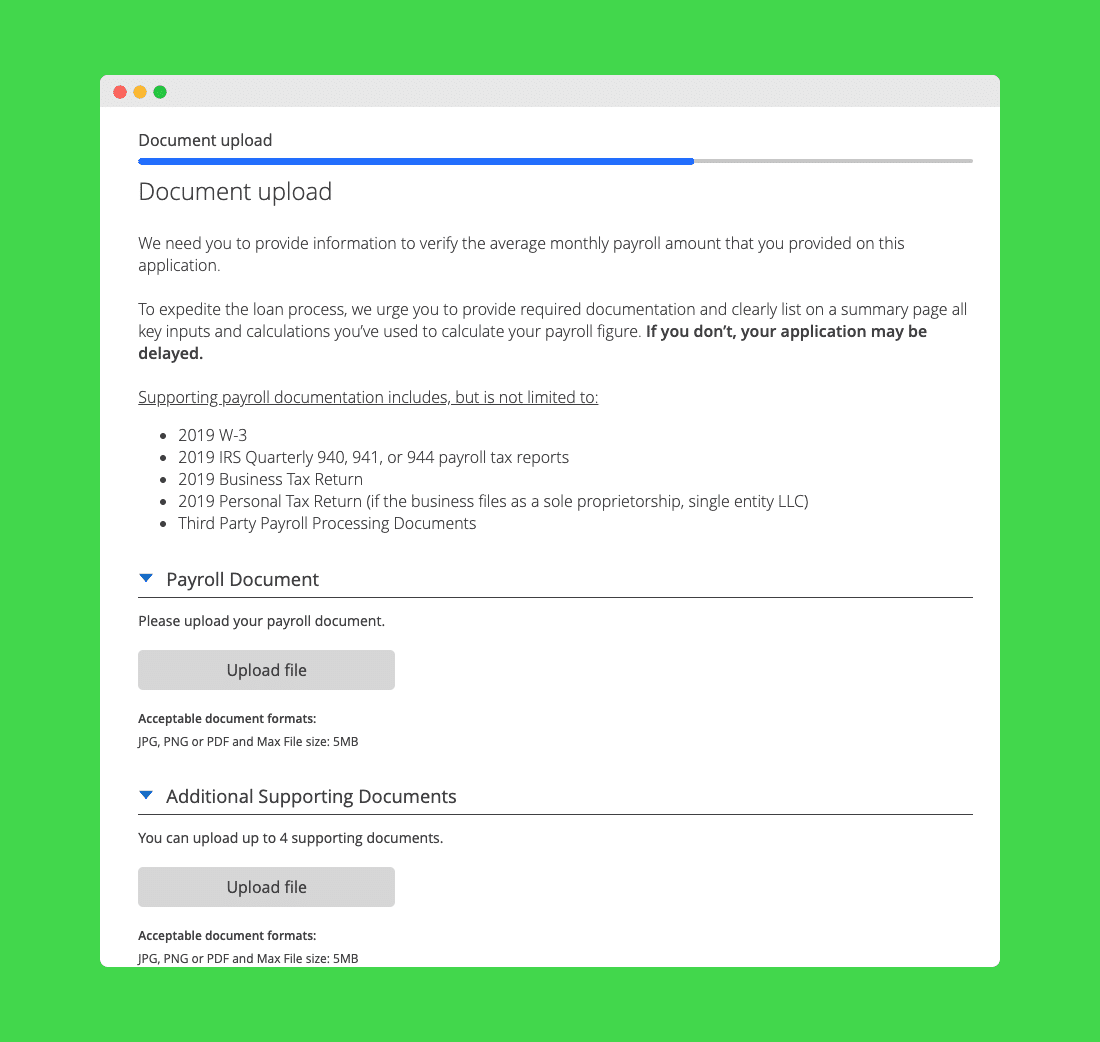

Documents Needed to Apply for the PPP

I’m starting to gather the following information:

- Evidence of my business start date. Tax ID issuance and LLC formation documents should do.

- Payroll Records from the last 12 months, including 1099s I issued.

- Annual profit/loss statement.

You should be able to grab this information from your payroll system records and bookkeeping records. Reach out to your bookkeeper and they should be able to help.

Other Questions About PPP

What if you have multiple businesses? As long as each business meets the eligibility requirements you can apply for a separate loan for each entity. Each loan will correspond with a unique federal Employer Identification Number (EIN).

What if you are the only employee? If you pay yourself a salary, you can include that in your average payroll calculations. If you don’t officially pay yourself a salary and just take your net earnings home, you will likely need to apply on April 10 as a self-employed person and use your net earnings in your calculations.

How does the PPP differ from the Small Business Administration’s Economic Injury Disaster Loan (EIDL)? Although both are SBA loans, these are different programs.

The EIDL is administered by the SBA directly. The PPP is administered by SBA approved banks. The EIDL is not eligible for forgiveness (although it does have a possible $10,000 max grant component that is). The PPP is eligible for forgiveness.

Can you have both loans? Yes, but you need to use the funds from each for different expenses.

If you have applied for (but not accepted) the EIDL loan, you can still wait to see if you get the PPP loan and then just take the one you prefer.

The final application form for PPP shows that if you have an existing EIDL, you have to add it to your PPP loan.

https://twitter.com/ptmoney/status/1244827006266679296

There’s some confusion around this and so all I can tell you is here’s what I’m doing: I applied for the EIDL at https://covid19relief.sba.gov/#/ and checked the $10,000 grant box during the application. I don’t plan on taking the actual EIDL loan, but I will take the $10,000 grant portion and put it to use immediately. The SBA says this will happen in 3 days!

As soon as the PPP application becomes available I will apply for that. Loans should close a few days or weeks later. I’ll then take the PPP funds and put them to use on my eligible expenses over the next 8 weeks.

Should you apply for PPP if your business can survive without it? There’s a definite grey area here. Do I really need this loan to get by? Maybe not. But my financial preparedness has nothing to do with true economic damage (currently and potentially) done to my businesses at the hands of the government.

Do these economic damages precisely equal the amount I’m taking out (2.5x my monthly payroll?)? Probably not yet. But the government is not asking me to take a loan out based on my actual losses. The reason?…no one knows what will happen next.

This is being dumped on us in a very uncertain time. Nothing is known. If you have employees and contractors you are supporting, take this money and ensure they get paid over the next 8 weeks.

More Guidance & Sources on PPP

Correction (March 30, 2020): The previous version of this piece linked to the Senate version of the CARES Act which did not include a reference to independent contractors being included in the payroll costs calculations. We’ve updated our link to the final version of the bill, H.R. 748, which was signed by President Trump and includes the section “(bb)” on including independent contractors in your payroll costs calculations. Second Correction (April 1, 2020): Now that the Treasury guidance is out on this bill it appears as though independent contractors will NOT be included in payroll cost calculations unless they have a 1099.

Other Lending Options

1. Personal Loan Options

If your personal expenses are mounting, consider a personal loan rather than running up high-interest credit card balances. Check out Fiona to compare offers in less than 60 seconds.

You can also obtain a loan from LendingTree.

Check your credit score now using a service like Nav.com and then use Experian Boost to try to increase your credit score before you apply.

2. Home Equity as Another Option

The traditional way of tapping into home equity is to obtain a home equity loan or HELOC through a bank or a lender. You are charged an interest rate, have to pay assorted closing costs and must commit to making monthly payments – in addition to your regular mortgage payments. If you are interested in a HELOC, consider using Figure. You can apply in minutes and, if approved, you can receive the money in as few as 5 days.1

However, in this new exploding FinTech landscape, innovative ways to tap into your home’s equity are popping up. And some of them are quite promising like Unison.

For those who already own your own home and have equity you want to tap into, the Unison HomeOwner program allows you to do that without getting a loan and without monthly payments.

Click here to learn more about Unison’s HomeOwner program and see if you qualify.

3. Consider Other SBA Loans

If you need funding for your small business, it’s hard to beat SBA loans. They come with favorable terms and may be easier to qualify for than other business loans.

But as with any government-sponsored initiative, the SBA loan program can be confusing. There are multiple SBA loans, each with different purposes and terms. But in this guide, we’ll cut through the clutter to give you the most important answers that you’re looking for.

Read: Everything You Need to Know About SBA Loans

What questions or concerns do you have about the Paycheck Protection Program? Have you applied?

1 Five business day funding timeline assumes closing the loan with our remote online notary. Funding timelines may be longer for loans secured by properties located in counties that do not permit recording of e-signatures or that otherwise require an in-person closing.

can an employer get ppp loan and exclude some employees? Can the Freedom of Information Act be used to see salaries that were used or is all salaries from 2019 used when applying for this? What does an employee do if he has been used for this program and has not received any of its benefits? my employer said she can loan me some money but i have to pay her back altho i worked last year and was working this year for her and the 2 other employees got ppp. she runs a public stable and a therapy riding facility. any information would be appreciated. would like to get what is due nothing less or more. thanks

It is not right that a PPP Loan is based on credit. I did not get approved.

Thanks for this. I was reluctant to file as I am self-employed, sole prop LLC. That said, reading through your notes, we are similar. So I filed. I used Paypal because my bank, TIAA CREF does not do PPP loans. I also applied for EILD, but as of yet, have not received any word.

We are in the same boat! I am a Single Member LLC and I applied for the EIDL application on April 12th and havent received any notification about the status yet.

I just applied for the PPP application and got approved.

I am a sole proprietor running a landscape construction business with my husband. He does physical work in the business and is paid via paycheck each week with taxes taken out. I run the admin side of the business and take owner ‘draws’ as needed. Since my pay technically comes out of the ‘profit’ of the business and there is no profit at the moment and since my pay is n0t part of what shows up on my quickbooks payroll reports- how do I include m0ney to pay myself in what I list on my PPP application?

Some employees would rather collect Unemployment Insurance than PPP wages because of the $600 additional UI funds promised on top of regular UI benefits.

Can anyone tell me how PPP wages square up with UI benefits?

I have received our PPP loan and want to keep a running spreadsheet to prove where our money is going. However, I have two questions. Are Cell phones/Ipads (used in our business) considered a utility? A few of our employees applied for unemployment (we are not essential), I heard I can pay them out of PPP to bring them up to their average pay while they were employed, is this true?

Thank You

Hi Phillip,

I am not sure if I am reading the posts correctly but its seems as if you applied for the PPP and EILD advance? Is that correct? I didn’t think we could apply for both. I am still waiting for Chase and I applied the first day it opened up online. I am wondering if I should try to get the advance thru sba.gov in the meantime. Is it faster? Thanks for all the information!

Sarah

Hi, Sarah. Yes, I applied for both. You can do that as long as you use the funds for different things.

Hi Philip,

Can we apply for the EIDL advance AFTER applying for the PPP loan? Like you, I am still waiting to hear that my PPP application has been approved through Chase and am wondering in the meantime if I can apply for the advance? I know on the Chase application there was a question about if we applied for the EIDL grant (which I marked no because at the time I had not applied).

Hi Phillip, the EIDL Advance is automatic paid to you once you apply and are approved for your SBA PPP Loan.

Updates:

I got both the $3,000 EIDL advance AND my $1,533 “Stimulus” direct deposit this morning.

WFB, my bank, finally lowered themselves to my level on Monday and asked me to fill out a loan application. Evidently, they determined that I more properly fell into the “self-employed” tranche as a single-member LLC. Again, they asked for 1099s for my contractors to prove payroll. This is about the hundredth time a lending institution has recognized that 1099 contractors are a part of payroll. I guess I will know if this is correct once they actually have me sign docs on it: roughly $44,000 vs $22,000 if they allow the 1099s.

As a matter of interest (?), the WFB application makes the 4th place I have applied for this same, stupid loan. I have submitted, more or less, the same documentation to all 4 places. We’ll see who offers first. I guess/think/hope.

What happens is a salesmen is on commission and receives a 1099 from us. are they covered under our PPP program .

Also if I have tried to rehire a few employees but dont answer their phones . i am responsible for hiring them back ?

If an employees has no more sick time coming to them and doesnt not want to come to work for whatever reason . under the PPP PROGRAM do I have to pay them if they dont show up for work or stay at work for a min time

I am self-employed (independent contractor, receiving 1099) and do not have a separate business account with my bank. Can I apply for the PPP through my personal bank account ?

Yes, Steve, you can, as long as you can find a bank that will do the loan. I’d start with your personal bank.

I have an LLC Partnership with 1 W-2 employee. There are 2 partners and we draw a certain amount each month. We have not filed our 2019 partnership return yet and are not sure if we need the PPP for our employee and the self employed program for ourselves as partners. Do you have any insight? Thank you.

I have the same set up and same question. Any insight? Thanks for any info.

Is PPP available to agriculture, farmers filing a 943? Not showing that potential on PPP form.

Have you guys compared option of PPP loan/grant vs unemployment for single owner operator LLC businesses?

If I have submitted an application for a PPP and some of my employees may not want to chance waiting that long for help and want to file for Unemployment benefits – will that affect my PPP loan application numbers?

I realize that contributions I make to my employees SEP can be included as income in the PPP. However, I am wondering, that as the employer, if my contribution to my personal SEP can also be counted as income and included in PPP calculations.

Currently, I am self-employeed, but do not have a business account. I regret delaying that decision, because all the lenders seem to only take applications for existing business accounts. Are there any lenders accepting applications for new customers or will my bank where I have my personal account accept my 1099?

No good information on what percent of my home based business utilities can be paid/forgiven via the PPP loan. I assume my cable/phone/internet is fair game and maybe half of my electric bill, but what percent of my home mortgage is allowed?

I would think we could follow the IRS rules on home office deduction here. https://www.irs.gov/businesses/small-businesses-self-employed/home-office-deduction

Is this PPP loan for payroll active if a business is still operating. In other words, we have 12 out of 25 employees working full time from home & 13 are not getting paid.

Do I submit my payroll for all 25 employees under this program & will get the grant for all 25. I will pay back the 13 now prior to loan.

It’s based on last year’s payroll or the last 12 month’s payroll. It’s the average. So theoretically, all your 25 will be included in the calculation of the loan. You should then hire those 13 back and start paying them for the 8 weeks. That’s what the program is for…to get people back to work and getting paid. The Chase app actually asked for the number of employees you will rehire or retain because of the loan.

I got this from Wells Fargo last night. I applied first thing Saturday morning, right after they opened their portal:

“We want to keep you informed on your interest in the Paycheck Protection Program application through Wells Fargo.

“Due to high demand, we are not able to begin your application at this time, but you remain in our queue based upon when you submitted your initial interest.”

I have no idea what this means.

I got that too and applied when you did. I wish some of these places would just speak a normal language because when it submitted it was fine. . . .

Thanks for all the useful information. I found 3 official locations that verify that 1099 contractors should not be included in your calculation of “payroll costs” under the PPP.

FAQ released by the Treasury on the evening of April 6, 2020

https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Frequenty-Asked-Questions.pdf

Question 15: 15. Question: Should payments that an eligible borrower made to an independent contractor or sole proprietor be included in calculations of the eligible borrower’s payroll costs?

Answer: No. Any amounts that an eligible borrower has paid to an independent contractor or sole proprietor should be excluded from the eligible business’s payroll costs. However, an independent contractor or sole proprietor will itself be eligible for a loan under the PPP, if it satisfies the applicable requirements.

Interim Final Rule by the Treasury on April 2, 2020

https://home.treasury.gov/system/files/136/PPP–IFRN%20FINAL.pdf

III. 2. h.

Do independent contractors count as employees for purposes of PPP loan calculations?

No, independent contractors have the ability to apply for a PPP loan on their own so they do not count for purposes of a borrower’s PPP loan calculation.

III. 2. p.

Do independent contractors count as employees for purposes of PPP loan forgiveness?

No, independent contractors have the ability to apply for a PPP loan on their own so they do not count for purposes of a borrower’s PPP loan forgiveness.

I’d really like to know what part of the CARES Act forces my 1099 contractors to work for me while they are being made as whole as possible because they qualify for a loan and I don’t.

Did ANYONE involved in creating this program actually think about it for a moment?

I am a single member LLC, who has a website business that started last year, Who has not sold any products. am I eligible for any govt loans

You are, yes. I would look into the PPP calculation and also investigate your options under the Emergency EIDL for the grant.

I filled out the Bank of America App. I am a single member LLC and pay myself a salary. I put the number of employees as 1 but I put the average monthly payroll as $9715.00 including costs. While the salary component is less than $100k the costs make it greater than $100k. Will I be automatically disqualified from getting the loan? Can I submit a change to cap the costs@below $100k? The Bank of America applicaiton has no options to change? Can I submit another application?

I’m fairly certain they will automatically cap you or you will get another chance at some point to make changes. If you end up with too much, you can always just pay it back early.

Small Business Owner

I have a full time employee who has contracted Covid-19 and has just used up their accrued sick time and vacation time. How will this affect my eligibility for the Paycheck Protection Program?

Regards,

I have another question that I haven’t seen answered here or anywhere:

As a single-member LLC, I have three 1099 contractors. The general thinking here is that I can’t use them in my calculations because they are not employees and, theoretically, they can apply for help on their own. What seems to me to be missing here is that, while it may be true that they can apply for their own PPP loan, if I don’t pay them, they won’t work for me. They aren’t going to say, “Well, I know you aren’t paying me but I’ve applied for a PPP loan on my own, so I’ll keep working for you.”

This has to be addressed somehow.

Hi PT,

1. Thanks! Very helpful!

2. One thing is unclear. If I exclude all my 1099 people (4), then I am a one-person firm (S-Corp). I make more than $100K. And the firm put $10K in my SEP-IRA.

So, what is my requested loan amount??

With your calculator, without including the SEP-IRA amt: $20,833.33

Or, WITH the SEP-IRA included, then: $22,916.67

Which is right?

And can you point to something that supports your answer?

Thanks!

Joe

Thanks

Thanks so much for the great information. Any luck with Chase responding to you? I too bank with Chase and all I’ve been able to do it complete their short online. They say they will have a representative call me…knowing how Chase operates, I’m not feeling to optimistic about that. I called my local branch this morning and they said not to come in, that I need to wait for a call, but they had no idea when that would be. In the meantime, the money is being loaned out by other Banks who are more prepared.

Hey, Bob. If you’re like me you got another “hang tight” email this morning from Chase. It looks like they are close to having an online portal up and some biz reps are working manually with clients…not sure if there’s a priority to that. I would be surprised if they don’t have the online portal up and running by Monday.

Thanks for all of the wonderful information on this! I have my accounts with WF but NAV just opened up their full application. Would you recommend submitting the full application even while I wait for WF to get back to me after I submitted my initial interest form with them this morning?

Yeah, it won’t count against you to apply with Nav. Until Nav actually matches you and submits to your chosen lender, you won’t have an official app in.

Wells Fargo’s portal is now open but it’s a “we’ll get back to you in a couple of days” scenario.

Also, I read through the PPP Rule and the reason no 1099’s contractors are accepted for the calculation is that they can apply on their own.

So, as a single-member LLC, I have no idea how to apply or what tranche I’m in, “self-employed” or “small business”.

Mik, my interpretation is that it comes down to if you pay yourself a regular payroll salary or not. Do you process payroll? If not, then my stance is you are in the April 10 category.

Hi! I just applied a couple of days ago for the PPP program through my Square account. I have a linked business bank account and thats how I charge all of my clients. I am self-emloyed, single-member LLC and only have independent contractors working for me.

I dont take a “salary” rather I just use part of my net earnings. Any idea how I can have my loan forgiven for the PPP?

Wells Fargo’s portal is now open… but, like Chase, it just takes your phone and email and says they’ll get back to you.

I’m still wondering about my 1099 contractors, too. It makes ZERO sense to exclude them.

so I am filling the ppp and it says payroll x 2.5 + edil = amount of loan

so i applied for the eidl but don’t have an answer

so do i calculate the eidl in so that i am asking for more?

banker doesn’t have answer

Hey, Pam. I’m not factoring in EIDL since I haven’t heard from the SBA on that.

Good Morning! One of the best reads on the net today.

Quick question: I started my career coaching and headhunting business last August – it’s a tech platform and I have 4 employees who are equity-staked. We don’t technically have a payroll, though my other three employees are 200k plus in salaries in their real jobs. Can I use this to hire more people?

I’d refer you to Nathan Latka’s info. He’s in the startup/equity space. https://blog.getlatka.com/saas-guide-coronavirus-covid-loan-program/

Phil: Thanks for the comprehensive article. It was a relief to find an article that answered 99% of my questions. Maybe you can help me with the last one. I am an independent contractor that draws on my commission throughout the year, however, the company I am working with manages that money for me and my clients pay the company. My commissions are equal to or exceed my draw. I provide services to other companies that have been closed indefinitely because of COVID. Because the business is seasonal, I haven’t quite felt the effect yet, but I will, and soon. Since my commissions cover my draw, and I am still taking a monthly draw from the company, since my business will be affected in the coming weeks due to the seasonality, am I breaking any rules by drawing AND applying for PPP? I don’t see anywhere in the “eligibility” section the statement that Independent Contractors are ineligible if they continue to be paid a draw. Thoughts?

Yep, I think what you’re interpreting is correct. All of my writers/consultants will be eligible for the PPP on their own and I’ll still pay them because I want us to continue the work we’re doing. You get to double dip now, in exchange for what could be a double whammy in the next few months.

Thank you so much for your help in making sense of the confusing details. Regarding FTE, I own a business with 16 part-time employees. All their hours combined equal only 4.2 FTE (meaning 4.2 x 40 hours/week). I have already laid off 12 of them. I read about hiring them back as part of the PPP.

–There is verbiage about “keeping your business going.” But we are closed by mandate and don’t know when or if we’ll be able to reopen for business. Is it intended that I rehire these employees and then just pay them for doing nothing? I’m fine with that, but is that the intent?

–Since it takes 16 part-time employees to make up the 4.2 FTE’s, do I HAVE to rehire ALL of them, or could I theoretically rehire, say, four or five of them and just pay the total payroll of 4.2 FTE employees? Meaning, pay out the same amount as before, but maybe to not as many people. My thinking is that maybe I could put a few people to work full-time doing repairs and maintenance, etc, rather than 15 part-timers.

Thank you!

I have a similar question. There are 10 full time and 4 part-time. The part-time employees are better off filing unemployment right now but their pay is included in the FTE calculation and I need to keep payroll expenses at 75% of the loan funds.

Phil – In guidance I am seeing it is not clear re part-time employees. We have both. I know full-time employees must be retained. Are you seeing anything for part-time?

Thanks!

First, let me say thank you in re to having the most reliable information I have found online. I too have a huge issue with the new Interim Rules released last night. I also concur that the Q&A section, though being clear, is based more on opinion and not on any reference to the legislation actually signed into law. Its hard to imagine that a hypothetical situation where a business has only 1099’s and no W-2’s can legally and ethically apply but cause a $0 loan amount. Just insane. Also, Just an FYI that a new loan form popped up last night, and guess what, the only change was on page two where they require you to initial…

The Applicant was in operation on February 15, 2020 and had employees for whom it paid salaries and payroll taxes or paid independent

contractors, as reported on Form(s) 1099-MISC.

So they want you to show and have the income of 1099’s to qualify but can’t use it? I’m sorry but such asinine rationale is why we are in this mess to begin with.

I would like to know the following:

What is being done to ask SBA/Treasury to revisit the 1099 issue? I have spoken to the Office of my Member of Congress and so far nothing yet. I even reached out to the few contacts I have in DC (yes, I do have those), but everyone is “working from home” and unfortunately political appointees move out of jobs quickly so my SBA contact no longer works there. I spoke to two different Banks, specifically with business lenders, and both knew nothing about this and obviously far less than anyone that reads this page. I do not know but is an Interim Final Rule the last step or can they revise/reverse it?

Do we have any legal rights to challenge the rule? My concern is that by the time the dust settles the funding will be gone.

Is it still ok to apply with our 1099-MISC included being calculated in the loan amount? Are other people doing this too or just giving up? If approved, I question the potential ramifications if I could be denied or have the loan recouped or even just slowed down.

For me, the difference between including and not including my 1099’s is huge. Only my W-2’s gets me only 16% of what I was originally expecting. Well into the six figures.

Sorry about writing so much but I’m assuming that many of us are or were depending on this to keep us in business and take care of our people. I gladly welcome any news or advice.

Heard from a contact today that the CRS is advising that 1099’s can be included. Hopefully the rule will be revised before Monday.

For a sole proprietor with net profit of $100,000 and no employees, their maximum loan amount will be $20,833.

My question – How do you calculate the forgiveness amount? Does the sole proprietor take a distribution for that amount during the 8-week window that equals the loan amount, or at least 75% of the loan amount (remaining 25% is rent/utilities), or do they need to have net profit during the 8 week window? Or is there some other way to calculate?

Thank you for this article! I appreciate having a clear, easy-to-understand, reliable source of information. I’m an LLC with no payroll and 1099s, so I’m guessing I’m 4/10, but I’ll be checking back here for updates.

i am an llc and told i could apply now and count myself as the employee

Thanks, Pam! Who did you apply with? My bank is requiring 940s and 941s. 🙁

I found this site to be clear and informative. I have a question; can a foreign owner of a US business qualify for a Paycheck Protection Loan?

Thank you,

Wow this was so helpful! Some of this terminology is a bit new to me. I made the mistake of applying now, though I am an Independent Contractor. If I get denied, I fear I wont be able to reapply on the 10th. So many articles mentioned applying ASAP. Thoughts?

Hi Phil,

Now they seem to asking how many full time employee you have.

No mention of part time. Do you know if all employees are covered or just full timers>

I am the owner of the dental office, and I have 8 employees, all of them only work 1 or 2.5 days per week( paid by hourly). But me and my husband, we are consider the full time employee ( paid by salary). For the PPP, should I have to pay my part time employees?

Phi- Thanks for keep tabs on this. In the final rule it looks like there are conflicting statements on whether you can include independent contractors in payroll calculation. For example, in 2E they state to “Subtract any compensation paid to an employee in excess of an annual salary of $100,000 and/or any amounts paid to an independent contractor or sole proprietor in excess of $100,000 per year.” So isn’t that basically saying that you can include independent contractor compensation if it is less than $100,000 per contractor? What do you think?

I’m just seeing this and I agree. A total conflict. Darn, this thing is so back and forth. I guess with this being the final rule it will be up to the banks.

Hi Philip-great info provided. A few observations. I dont think borrowers can get loans for different companies. This is new and can be found in the document on the Dept Of Treasury site. Here is the link and the explanation:

https://home.treasury.gov/system/files/136/PPP–IFRN%20FINAL.pdf

k. Can I apply for more than one PPP loan?

No. The Administrator, in consultation with the Secretary, determined that no

eligible borrower may receive more than one PPP loan. This means that if you

apply for a PPP loan you should consider applying for the maximum amount.

While the Act does not expressly provide that each eligible borrower may only

13

receive one PPP loan, the Administrator has determined, in consultation with the

Secretary, that because all PPP loans must be made on or before June 30, 2020, a

one loan per borrower limitation is necessary to help ensure that as many eligible

borrowers as possible may obtain a PPP loan. This limitation will also help

advance Congress’ goal of keeping workers paid and employed across the United

States.

Also I have another question. Is the average monthly payroll determined by the last 12 months (April 1, 2019 thru March 31st 2020) like the law says or The last calendar year (January 1, 2019 thru Dec 31st 2019) like the SBA application says. This is very very important. If you read the link on the treasury dept from above it gives contradicting answers-see below:

THIS ONE SEEMS TO INDICATE THE LAST 12 CALENDAR MONTHS (APRIL 1ST THRU MARCH 31ST)

e. How do I calculate the maximum amount I can borrow?

The following methodology, which is one of the methodologies contained in the

Act, will be most useful for many applicants.

i. Step 1: Aggregate payroll costs (defined in detail below in f.) from the last

twelve months for employees whose principal place of residence is the

United States.

THIS ONE BELOW SEEMS TO INDICATE JAN 1ST THRU DEC 31ST:b.

What do lenders have to do in terms of loan underwriting?

Each lender shall:

i. Confirm receipt of borrower certifications contained in Paycheck

Protection Program Application form issued by the Administration;

ii. Confirm receipt of information demonstrating that a borrower had

employees for whom the borrower paid salaries and payroll taxes on or

around February 15, 2020;

iii. Confirm the dollar amount of average monthly payroll costs for the

preceding calendar year by reviewing the payroll documentation submitted

with the borrower’s application;

A borrower is technically the entity, not you the individual.

I’m submitting just my 2019 data.

Hi Phil,

We’ve been going back and forth with our bank and did some digging ourselves regarding the compensation cap of $100K per employee annualized. Specifically in our reading, which we passed by a few others, the the statute specifically defines “compensation” to include everything, but then specifically excludes only “annual salary” in excess of $100k (not referencing the other items of compensation). The instructions in the PPP application say “payroll” over $100k. Finally the Treasury PPP fact sheet implies “salary, wages, commissions or tips” are capped at $100k using short-hand that is different from the wording in the statute.

Basically, we’re reading the correct calculation to be salaries and wages (excluding any amount per employee over $100K in annual salary) + other payroll costs (health, retirement benefits, state/local taxes). Not $100K per employee inclusive of additional payroll costs. Would you think our reading is incorrect here?

We’ve seen many sites that say the cap is inclusive of those additional costs, which likely won’t be a huge problem for many, but could mean some businesses are taking a smaller loan than they could be (if our reading is correct).

Hi David,

We have been going back and forth on the same issue. From my most recent conversations, it seems that the interpretation of the 100k cap may vary by bank.

Were you able to receive any further guidance?

Phil,

I am seeing different info of different sites. I am a single member LLC (real estate broker with 6 agents/independent contractors)

My account files one personal return and my income is my net profit of my schedule C

Some sites say apply on April 3rd as a sole proprietor (website link below), others (your advice) say April 10th as self employed.

Which one is correct?

https://bench.co/blog/operations/paycheck-protection-program-self-employed/

Hi Philp,

Thank you for taking my question.

Is the health benefit covered by the PPP?

I have been trying to reach banks all day for the SBA PPP loan assistance. My own community bank where we have our business account does not offer SBA loans at this time. All of the bank I have contacted state they only offer SBA loans to their customers. I am eligible with a small business of only 7 on payroll and I’m kind of in a panic already. How can I apply for this loan? Is there no on-line application process?

Hi Phil, thank you for the info. I have a business just starting paying myself last quarter at year end as the business finally made some money, so how do I calculate my payroll as it only cover’s 3 months actually, and if I divided it by 12 as what the calculator goes, it will make that cost 1/4 of the salary. How should I do it? Thank you in advance

My gross payroll for 2019 was $551,930, my tipped employees claimed $198,118 in tips received. For the calculation, do I use $551,930 (without claimed tips) or $750,048 (with claimed tips)? While we are closed, I would be paying my tipped employees their pay plus an average of what tips they would have made, correct?

Hi Michele & Pete…..

I’m in the same boat. I have seen where tips are to be paid to servers through this program but no actual instructions to do so.

Hi Phil, thanks for this great info.

Can I apply at only 1 bank or will I be able to apply at multiple banks and take the loan from the first one who approves me? I am concerned about how quickly my bank processes the application, and if they will run out of money before they get to mine.

Great question. I’ve thought about hedging my bets as well. I’m currently banking with Chase, but I have FNBO as a secondary (I’ve spoken with the banker there). I would not recommend actually submitting two applications (this might trigger a fraud alert), but I think it’s helpful to be in communication with two banks to see who’s most prepared and ready to roll first.

Hi Phil,

One more question for you…does a multi member LLC with no payroll and only partner distribtions and 1099 independent contractors (which I believe you feel maybe disallowed) file on April 3rd or April 10th.

Thanks again for all the information

My guess is the 10th, but like I said below, it’s clear as mud at this point. Let’s see on Friday.

Thank You for your fast responses and information

Do you have a link to the Treasury guidance that you mention a couple of times in this article stating the independent contractors will be disallowed? My read of (bb) is the same as yours.

Hey, Josh. It’s here: https://home.treasury.gov/policy-issues/top-priorities/cares-act/assistance-for-small-businesses

The Treasury is not outright saying contractors aren’t allowed, they are just silent to it. I’m assuming the worst here.

Great article and information! Any update on the question of whether a multi-member LLC that has no employees, and only hires independent contractors, and the LLC members take monthly distributions to cover their personal living expenses, would qualify for getting a PPP Loan?

Hi Phil,

This is a great article and more information then my bank (a large national one) has been able to tell me.

We have an LLC with a single employee. Should we wish to apply for the PPP loan do we apply on the 3rd and include our member distribtuions that are subject to self employment tax in the payroll amount or do we have to wait until the 10th. It would seem that waiting to the 10th would penalize LLC’s in favor of S corps where the owner can draw a salary. The bank has not been able to answe this question. Thank You

This isn’t spelled out yet, but it would make sense to simply apply with the bank as soon as possible using the Gross Receipts or Sales from the Schedule C. Frankly, the 3rd vs 10th thing is very confusing because a sole prop is the same thing as an independent contractor. The Treasury goofed that up. I’m hoping this gets cleared up by Friday. Just keep listening to the SBA, Treasury, and your bank. I’ll try to keep you updated as well. Twitter hashtag #paycheckprotectionprogram is a good place, too. Good luck, Jon.

Thanks Phil it is a Multi-Member LLC so I think I will just take the payroll and also include the distributions subject to self employment tax and include it on the 3rd unless the bank tells me otherwise.

Q1: What is specifically meant by “payroll costs are capped at $100,000 on an annualized basis for each employee”?

Q1.A: Since the lenders are requiring monthly payroll records to determine the average monthly payroll costs for 12 months preceding loan origination, is the payroll for each month capped at the gross wage amount for the month that would be annualized out to $100,000?

Would I be correct to interpret that the calculation would be an employee that is hourly (not salary) and makes more than $8,333 in gross wages for any given month, possibly due to OT, would be capped at the $8,333 amount and anything over that amount could not be counted for payroll during that month (even if the employee might only make $85-95,000 a year and be under the $100K annual cap).

Or is it the total annual amount the employee makes for the 12 preceding months over $100,000? If it was the 12 month total and someone who was hourly or salary then makes over $100,000 a year, in say the first 10 months, would you just not include anymore of their wages/salary in the final 2 months of calculations?

Also, no mention on PUCC, auto, or cell phone allowance/stipend paid to employees as being calculated as part of gross wages, any clarity on that?

Appreciate the insight… question: Laid off my employees on March 18th. They filed for unemployment. I am assuming they will get unemployment, and that amount may be 60/70% of their salary. Should I get this loan and pay them the difference to ensure I have employees when they eventually come back to work? At this time they could be out of work until the June30th forgiveness time frame… but what happens if we are closed past June 30th, will those loans convert to become a .5% loan to be paid back? Is this a draw type loan as need funds, or a set amount (an amount of which I don’t know).

In regards to the EIDL Grant, I have read that the grant amount would be subtracted from what is forgiven under the PPP loan. Is that true even if the grant is used on different expenses? Is there specific expenses the grant has to be used on like the PPP? Have you seen any more information about that?

What does it mean by: Payment of State or local tax assessed on the

compensation of employee?

And in regards to payroll costs this includes the full salary paid to an employee (which includes their federal tax withholding and their portion of payroll taxes), right? We just can’t include the employer portion?

Lastly, even though independent contractors can apply on their own if we as a company still need the contractor it seems like we will be at a loss to not be able to include them in our payroll costs. As well as a few contractors just recently became employees so our monthly average will be quite a bit lower than it truly is for employees because last year they were independent contractors.

How is fte employee calculated? How do PT employees affect the calculation? We have a 38 hr wk week for our ft workers.

Great question. It’s not clear at this point. Hopefully the SBA/Treasury/banks clarify.

I put my employees on furlough March 13. The PPP Bill states that those laid off until 30 days after the Bill was signed will not count against forgiveness. Does that mean I have to have the employees back on payroll within those 30 days? Or, can I keep them on unemployment on – say May 10 – and still get full forgiveness (after the 30 days). Our state dental association has now says we are not to open again until at least May 10.

I put my employees on furlough beginning March 13. The PPP Bill notes that employees laid off until 30 days after the signing of the Bill will not count against forgiveness. Does this mean that I need to have hired back all employees at the end of those 30 days to get 100 percent forgiveness. Or, does it mean that since I put them on furlough earlier I can put them back on payroll – say May 10 – and still get 100 percent forgiveness – our Dental Association says not to reopen until then so my goal is to keep them on unemployment until May 10 unless it reduces the forgiveness.

We are a fractional ownership HOA at an ocean community. We have 10 full-time employees. Our HOA dues cover the cost of salaries and benefits for those 10, so there is no economic hardship as the dues will continue to come in. Can we apply for the loan, it doesn’t seem ethically correct without some hardship.

Can I increase my employees and or independent contractors over the next 8 weeks and include their compensation when applying for forgiveness in 8 weeks? God willing my business grows during this time I need more people.

I’m confused by how to calculate the average monthly payroll total (for a restaurant)….does it include payroll taxes, etc? The form asks for “number of jobs.” How is this calculated and based upon what period? The average year, or this time of year? This time of year we are lean anyway….so if average, we will be forgiven less even if we are staffing the most we can use for take-out/ delivery. Many of our staff also do not want to work for fear and wish to shelter in place. How does that factor in? Thank you!

Same question 🙂

Same here, does this refer to the number of positions we have? Or is it asking about the number of employees we currently staff?

Same question

Same question

Thanks for the details. Question – will the employer match of Social Security and Medicare tax be considered part of payroll costs. These are additional cash payments beyond gross paid incurred by the employer so it seems appropriate to include these as payroll costs.

To my knowledge, no. The reason is these expenses are actually being deferred to 2022.

Hello Philip,

Can you give your thoughts on sec. 1106 (d) for limits on forgiveness and how it relates to 1106 (d) (5) for exemptions for re-hires. It seems to me that there can be a significant decrease in the amount of the loan that is forgiven if employees aren’t retained or if there are decreases in salary during the loan period with a look back period going to 2/15/20.

Thank you in advance!

Thanks for such a wonderful site, very helpful! I also bank at Chase although I didn’t receive any email like you describe.

My question is, how strict do you think they will be on the “evidence of business start date”? I started my business 20 years ago, if I ever got an EIN letter, it’s long gone. The IRS can get you a copy but that apparently takes at least a month under the best of circumstances. Since I’ve been with the same bank and the same bankers for years, do you think that getting that proof will be critical to the loan application?

I hope I can help a little. I started my business over 20 years ago & we had to get a FEIN with the State Dept of Revenue(ours is Wisconsin, so Wi Dept of Revenue). Perhaps go to your state’s website & see if you can find something there as to how to get yours).

Hi Philip,

Thanks for the summary. My reading is that an Employer uses payroll as the loan calculation mechanism, and sole proprietors use 1099’s, etc for their calculation.

Your loan calculator adds both. Can you confirm if my reading is incorrect?

Hey, Dennis. Good question. The way the law was written makes this a bit hard to decipher. Specifically, that (bb) section under the “payroll costs” definition. It says “the sum of payments of any compensation to or income of a sole proprietor or independent contractor that is a wage…” (emphasis added). So the way that someone who has both W-2 employees and independent contractor (as represented in 1099s) should read the payroll costs section is to gather both data points.

If you have one or the other, you would just input that one. Maybe what I’ll do to make the calculator more clear is add “net earnings from self-employment” to the independent contractor side.

Thank you so much, PT. This article is unbelievably helpful and more comprehensive and actionable than anything else I could find online (including SBA’s website).

I co-own two small businesses and am applying for a PPP loan for both due to uncertainty, not actual realized losses. One of my businesses is tied to the construction industry and the 2008 crisis didn’t hit us until 2010-11.

I’ve reached out to the banks I already have a relationship. I also filled out the form on StreetShares…thanks for including that link

Glad it helped. Hopefully, this puts us all in a better position in 8 weeks.

“What if you are the only employee? If you pay yourself a salary you can include that in your average payroll calculations.”

If a new and/or struggling one person business doesn’t currently make enough to pay a salary and needs the loan forgiven is there any way to do that?

I would talk to your bank about it and see if you qualify. The expenses ultimately have to be used to pay legit salaries, rents, etc.

This is great information; concise, timely, and accurate! My question is if your business employs both salaried employees and 1099 contractors, I see where section (bb) includes them in payroll expenses. But what about in calculating FTE’s? Is contract labor excluded from the FTE calculation for forgiveness?

Hi, Clyde. Good question. The Act defines “payroll costs” and states that they are used in the loan amount calculation. Then, when it starts talking about “eligible use of covered loan” it references “payroll costs” again. They are the same thing. Contract labor is in both.

Philip:

Thanks for your reply and I agree that “payroll costs” should include contract labor:

1. When determining the eligible loan amount; and

2. When identifying authorized uses of the covered loan.

But what about when calculating the percentage of loan forgiveness? Does the borrower only use employees, both salaries and hourly, when calculating FTE’s when determining the forgiveness percentage? The language in Sec. 1105 uses the term ‘employee’ and not ‘payroll’ costs’ when calculating the percentage.

My interpretation is that, when the borrower calculates FTE’s for the ‘before’ and ‘after’ periods, that they should exclude contract (1099) labor and only use employees (W-2) in this calculation.

Is that your interpretation?

Oh, you’re talking about the limits to loan forgiveness (1106(d)). I see. Thanks. Well, I agree that for that section it only speaks to full-time employees, yes. The law doesn’t want us firing folks or reducing wages and keeping 100% of the money just for rent, for instance. The way I interpret this section is that if you didn’t have any full-time employees (just had ind. contractors, for instance) then your loan forgiveness couldn’t be limited. One last promising point is that the SBA might waive this section entirely. They’ve been given discretion to: “The Administrator and the Secretary of the Treasury may prescribe regulations granting de minimis exemptions from the requirements under this subsection.”

Thanks for the info you sent our way.

I have this question

questions regarding unemployment benefits:

• Confirm there is no waiting week

• Confirm employee will receive 100% of current wage up to 4 months

• How is medical/life/etc insurance benefits treated? Is employee covered?

Emergency Economic Injury Grant and Economic Injury Disaster Loan recipients and those who receive loan payment relief through the Small Business Debt Relief Program may apply for and take out a PPP loan as long as there is no duplication in the use of funds. What you said was if you have one type of loan you can get another type. That’s not really “true”.

My assumption is that you are using the funds for the same thing. But you make a good point. I suppose you could use the PPP loan for all your payroll and rent, and then use the EIDL loan for other expenses.

Hi! thank you for this article! very helpful

quick few questions – in order for it to be “forgivable” we have to employee the same amount of people on June 30 as we do now – am I missing any other requirments?

We are out of work…what should we do between now and when we get the loan? should we tell people to file for unemployement or just pay them so they don’t go get other jobs and then the loan isn’t forgivable

To my knowledge, there is no requirement to have the same number of people employed. But the Act is clear on what the funds need to be spent on to be eligible for forgiveness.

should we tell people to file for unemployement or just pay them so they don’t go get other jobs and then the loan isn’t forgivable. I have only laid off 2 employees but we are paying all health/dental insurance if hours are reduced.

There is an FTE used when calculating the forgivable portion so the fte count becomes important.

Thanks so much!

For my business, a short term rental,

I have a manager ( 1099) and a cleaner (1099). I am a sole proprietor and have never been paid a salary.

Since I have ZERO traditional payroll employees, can I use my 1099 people solely? Or are they only allowed in the calculation in ADDITION to

“ regular” employees-

My interpretation is that You can use them solely, yes.

I am a Marketing Professional, former Agency owner, and MBA student who works in a business consulting law firm. In regards to claiming Indy 1099 contractors, I don’t think or see how this can be possible. They are independents and can apply for the PPP as well according to the CARES Act and according to the Dept of Treasury. They are subject to paying taxes just as you are as a sole proprietor.

Under section 1102 “INCLUSION OF SOLE PROPRIETORS, INDEPENDENT

CONTRACTORS, AND ELIGIBLE SELF-EMPLOYED

INDIVIDUALS.—

‘‘(I) IN GENERAL.—During the covered period,

individuals who operate under a sole proprietorship

or as an independent contractor and eligible

self-employed individuals shall be eligible to

receive a covered loan.”

In hindsight, this is apparent. But the language of the law made it confusing with the “compensation to” reference in “(bb)”.

Phil, a couple of people have asked about “number of jobs” on the form. Any idea what that is? As far as applying tomorrow, I too, received nothing from Chase as far as an email but I bookmarked their page to see if it’s updated. I am assuming since this is where I bank that’s the best place to start although finding a “person” there is quite a challenge even before this. I subscribed to the 5 banks you have listed on your site..but in the end, supposing we here nothing from our own banks and nothing from the ones we contacted, preliminarily, whats the best course of action as far as applying? Throw darts? How’s the average person supposed to know where to pick to apply? Any thoughts?