Raisin (SaveBetter) Review: Is it Legit?

Do all these savings account interest rate increases have your head spinning about where to stash your cash? It’s great that we’re finally earning interest on our money again. But rates are changing quickly. It’s hard to know where to save.

That’s where the revolutionary savings platform Raisin (formerly SaveBetter), comes in. They offer access to some of the best rates in the nation for insured savings products from the numerous financial institutions they partner with – from the convenience of a single account that you open with Raisin.

Don’t worry. I’ll explain more. I’ve been trying Raisin, and I’ll share all I know in this comprehensive review.

Table of Contents

What is Raisin?

Raisin is a savings platform. Not a bank. They partner with different banks and credit unions and their respective savings products (savings accounts, money market deposit accounts, and CDs) and allow you to save into these products through their platform.

They are a first-of-its-kind savings platform that allows you to tap into multiple savings products from multiple institutions, all under one account.

That’s the point of the service. Get the best savings rates without having to jump around to different banks all the time.

I know Raisin’s President and marketing team, and I’ve done business with them via FinCon.

Is Raisin Legit?

It’s a unique platform. But yes, it’s legit. I have an account with Raisin, and my money is earning interest now.

Several financial experts have reviewed the tool, most notably Rob Berger (trusted Youtuber, attorney, and friend). Rob loves Raisin and vouches for it.

Like I said above, I know a few Raisin team members and can vouch for them.

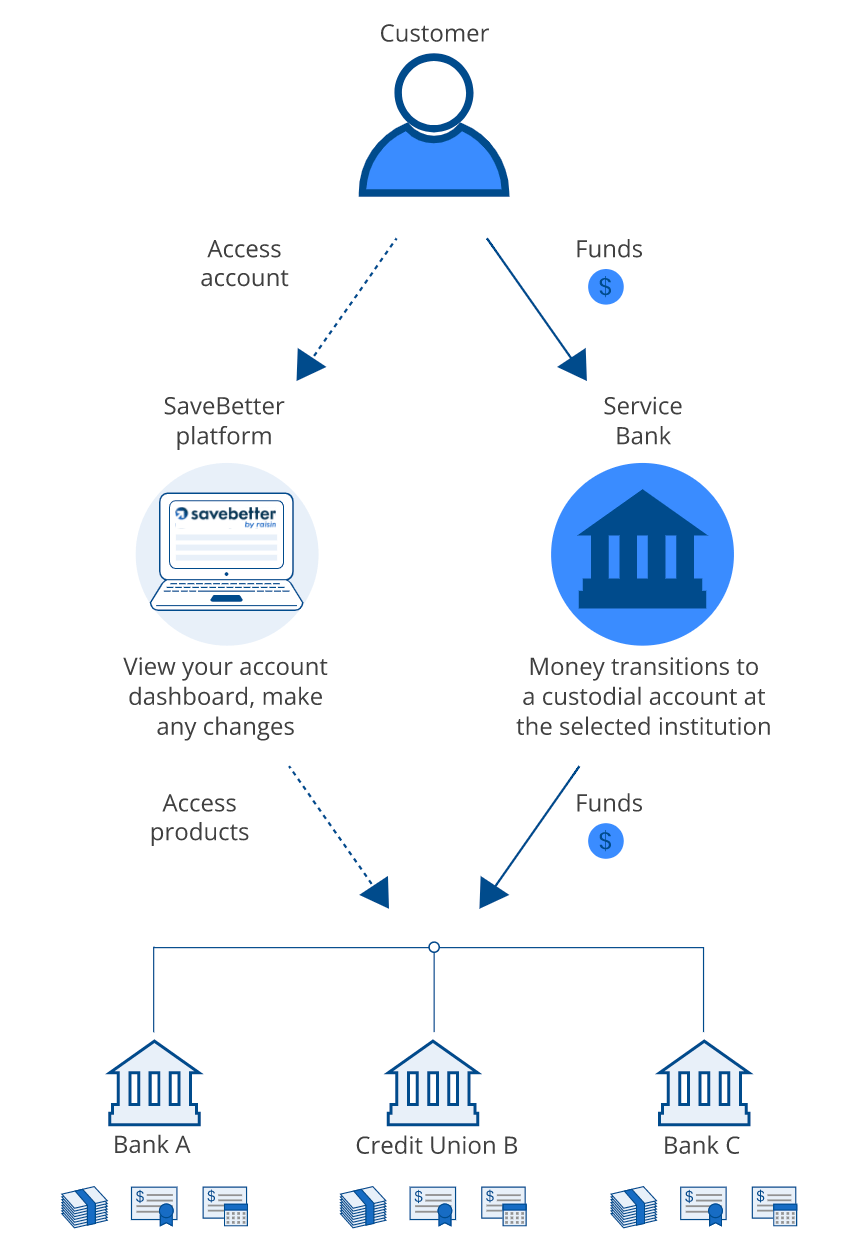

Is Raisin safe? If you’re concerned about the FDIC-Insurance thing, that’s understandable. But the best part is Raisin never touches your money.

When you make a deposit, the money is transferred from your primary (or reference) bank account to the institution and product you selected by their insured service bank (Central Bank of Kansas City).

Once your deposit is transferred, it is held in a custodial account (a pooled bank account) with the selected institution. In other words, your funds are always held with an insured institution.

Most importantly, the FDIC or NCUA insurance is transferable to you with the selected institution up to the applicable limits.

Here are their exact words on the topic:

“Although Raisin customers’ deposits are pooled in omnibus accounts, there is no impact on the eligible deposit insurance coverage you receive from the financial institution holding your savings. This is because the government entities providing federal deposit insurance — the FDIC for banks and NCUA for credit unions — permit pass-through coverage. So your money that’s pooled in a custodial account still has the coverage it would have were it held in an individual account in your name.”

How Raisin Works

Raisin shows you several savings options (savings accounts, CDs, and money market deposit account) and allows you to sign up for the products via the Raisin portal. You never have to go to the partner banks / credit unions.

Once your account (or accounts) are established, you can see them all on the Raisin dashboard. Move money around, transfer it out, whatever you want.

Banks and credit unions that Raisin works with at the time of this article:

- Western Alliance Bank

- The State Exchange Bank

- American First Credit Union

- mph.bank

- Blue Federal Credit Union

- Third Coast Bank

- The Atlantic Federal Credit Union

- Great Lakes Credit Union

- Liberty Savings Bank

- Ponce Bank

- Bellco Credit Union

- Continental Bank

- Patriot Bank

- Idabel National Bank

- SkyOne Federal Credit Union

- Sallie Mae Bank

- Lemmata Savings Bank

- Axiom Bank

What Raisin Offers

Raisin offers high-interest savings accounts, money market deposit accounts, and CDs. They have traditional CDs and “no penalty” CDs.

Here are the best offers from Raisin right now:

|  | |

5.50% | 5.25% | 5.26% |

Partner banks and credit unions create these products. Raisin allows you to tap into them all from one dashboard.

Does Raisin Offer Business Accounts?

Raisin does not offer business accounts as an option, only individual and joint accounts, but the platform continues adding new features and functionality.

What Does Raisin Charge in Fees?

They don’t charge fees to you. They charge a fee to the banks and credit unions on their platform. The partner banks and credit unions also do not charge a fee. It’s a free service to you.

How Much Can I Earn from Raisin?

Raisin has the highest savings rates available today. At the time of this piece, those savings account interest rates are above 5% (and above 5% on CDs). Use the calculator below to determine how much interest you would earn in a year with a Raisin account:

This calculator allows you to see the amount of interest that you will earn over the course of a year.

Steps:

- Enter the principal (the amount of money in the savings account) and

- enter the APY (the annual percentage yield) in the appropriate input fields, and

- click the “Calculate” button

The result is displayed in the “Interest” field below the button. Try it!

Pros and Cons of Raisin

Pros

- Highest savings rate available today

- Everything under one platform/login

- Simple interface and fast signup

- FDIC-Insured or NCUA-Insured

- Unique offering

Cons

- Limited banking solutions

- New fintech

- No 3rd party app links (e.g., Empower)

- No trust or IRA accounts

Raisin Referral Bonus: Up to $125

Raisin ended their public account opening bonus. However, they still have an active existing customer referral bonus.

If you plan to open up an account through Raisin with at least $5,000 then you could qualify for a bonus of up to $125 by using a referral code. Here are the details:

You can earn $25 for $5,000 USD in initial deposits maintained over 90 days and $5 additional for every $5,000 thereafter, up to $125 in bonus for $105,000 USD or more.

Referral bonus cash will be deposited by Raisin US LLC into customer’s and into referee’s external bank accounts, respectively, that were linked to Raisin.com within 30 days of satisfying all terms to qualify for referral bonus cash.

US customers only. Not open to Raisin Solutions employees. Raisin reserves the right to terminate this offer at any time and to deny Customer referral bonus cash for any reason.

Want to do a little bonus stacking? Open up a Raisin account using a referral code, then refer your spouse, family members, and friends. You will earn $50 for everyone you refer through their program. You can make up to $1,000 in referral bonuses.

Should You Use Raisin?

Raisin is an excellent fit for you if you always like to have your savings earning the best interest rates but you’re tired of jumping around signing up with new accounts.

Raisin is also great for aspirational savers. Maybe you’re just getting started saving, and you want a secure “offsite” place to store your separate savings. Raisin would make a great partner in your efforts.

Raisin is not for you if you’re looking for a one-stop banking solution with checking, cards, etc.

Saving made simpler: Access multiple high-yield savings products from one account. FDIC-Insured. $1 Minimum Balance.

FAQs

How do I know that my money is safe with Raisin?

All accounts at Raisin have insurance from either FDIC or NCUA (for credit unions), which protects your money up to $250,000.

Are there any minimum balance requirements to open an account with Raisin?

Most, if not all, accounts opened through Raisin can be done so with a $1 minimum balance.

Is there a limit to how much I can deposit into my Raisin account?

No, but you may want to spread your deposits across multiple products if you put more than $250,000 into Raisin.

Can I access my account and make transactions with my account on holidays or weekends?

Yes

What is the process for depositing and withdrawing money from my Raisin account?

You connect an external bank account and transfer the money. It takes 2-3 business days.

Are there any penalties for withdrawing money early from a CD account through Raisin?

Yes, on certain CDs, there is an early withdrawal penalty. Each bank will determine the penalty. However, Raisin does offer several no-penalty CDs.

Is there any paperwork required to open a Raisin account?

No physical paperwork, no. The entire signup process is done online and in minutes. It involves providing basic information, agreeing to terms, and connecting with an external bank.

Can I open multiple accounts under one Raisin account?

Yes, you can have multiple bank or credit union savings accounts or CDs under one Raisin account. You can also open a joint Raisin account.

Can I use Raisin account to pay bills or for other transactions?

There is no bill pay with Raisin. You can transfer money in and out of your Raisin account at any time into an external bank account and pay your bills from there.

Are there other benefits to using Raisin rather than opening an account directly with a bank or credit union?

The significant benefit is simplicity—one account to manage your savings.

How do I contact Raisin customer service?

Raisin can be reached by email at service@raisin.com, via live chat on Raisin.com, or by calling (844) 994-EARN (3276).

Does Raisin have an app?

No. At this time they don’t have an app. However, their website is accessible by mobile browser.

Does Raisin offer a signup bonus?

Last Summer they offered a $125 signup bonus depending on how much you deposited. But that promotion has ended.

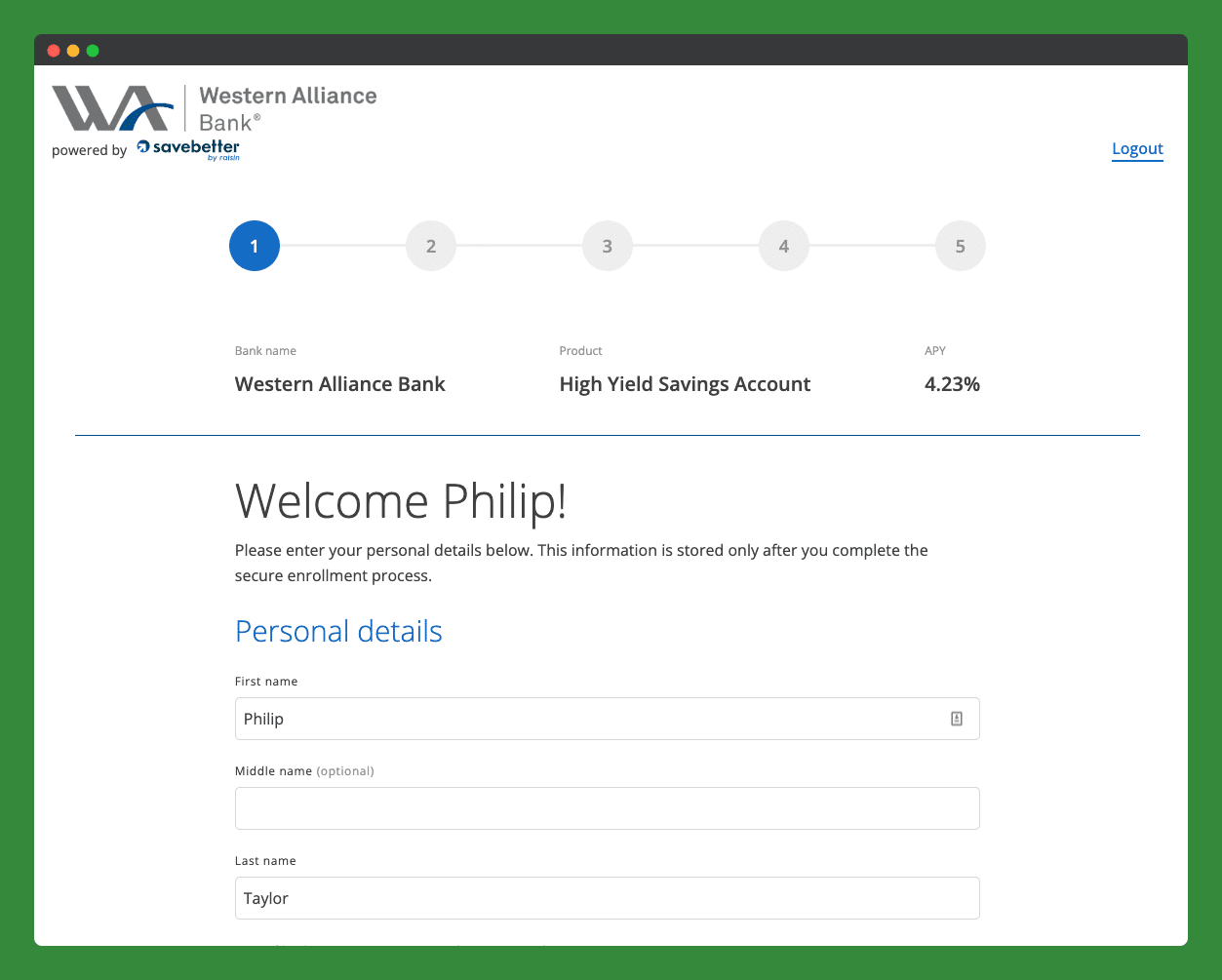

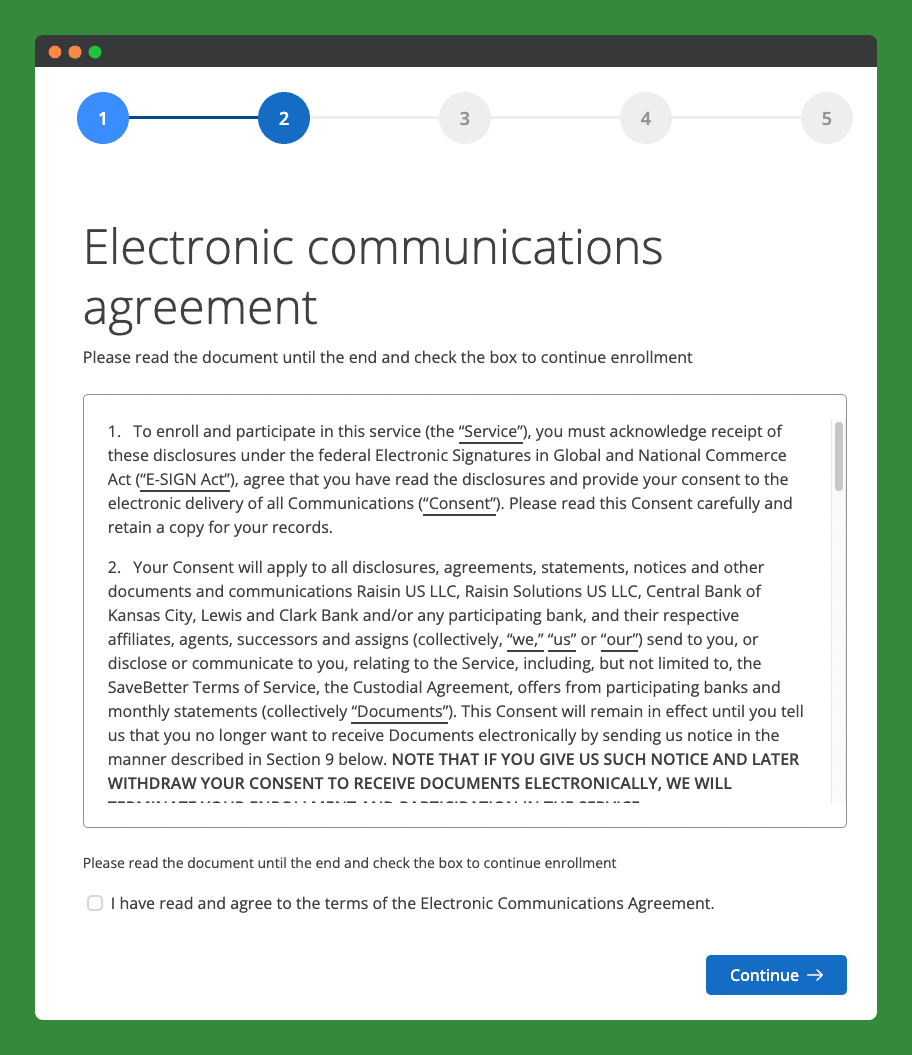

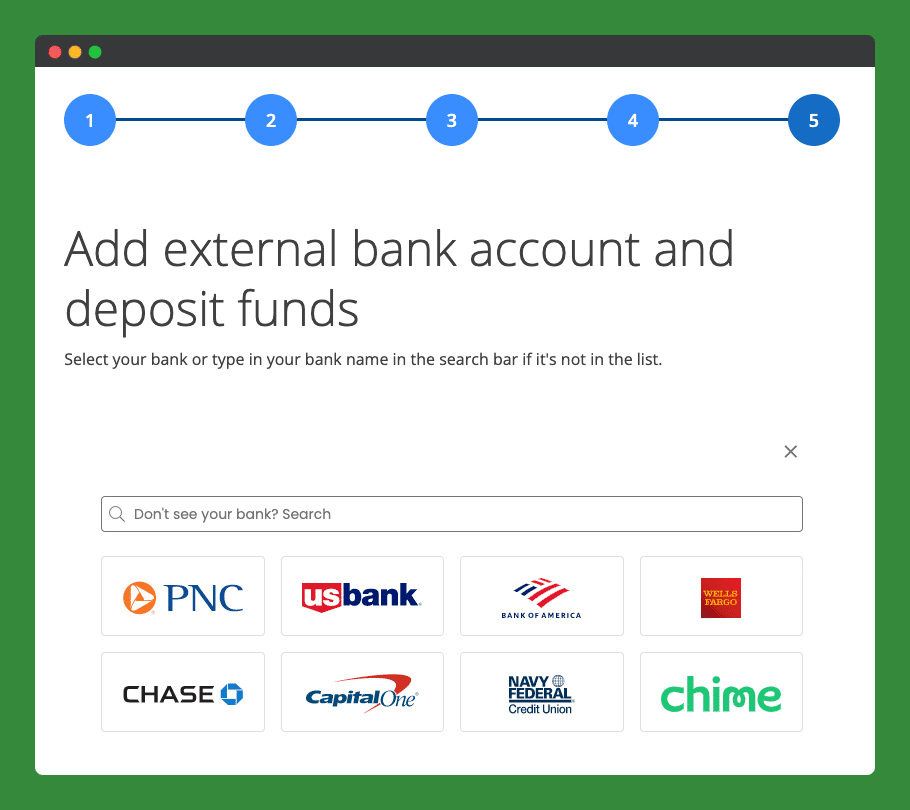

Steps to Sign Up with Raisin [in 5 minutes]

I signed up with Raisin and captured all the screenshots to show you what it’s like.

Step 1: Head to Raisin.com and pick a product (savings, CD, etc.)

Step 2: Complete the basic bio, including your Social Security number.

Step 3: Sign an electronic agreement, several terms of service, and tax certification.

Step 4: Connect an external bank account and deposit at least $1.

Step 5: Repeat the process for any more products you would like.

Ready to give Raisin a try? Head to Raisin.com and learn more.

Saving made simpler: Access multiple high-yield savings products from one account. FDIC-Insured. $1 Minimum Balance.

Customer service rep(s) who don’t care about their jobs costing the company new clients such as myslef and big deposits ($300K). Had issues with opening a joint account where despite providing 100% correct information the site would not verify my identity. The rep’s response: “There is nothing I can do”. When inquired via email I got the same response and attitude telling me that I was probably dealing with the same rep, and very likely, the only rep SaveBetter has. Opened an account under my wife’s name but then when inquired about how we could add a co-owner to the account we got no response. SaveBetter went completely silent. Now I’m sure the SaceBetter execs would want to know that they are potentially losing business due to lack of assistance from customer service rep, but the odds are that they too don’t care. The silver lining to my experience was that I saw a glimpse of what could have happened after we opened and fund the account with a large deposit and then ran into problems trying to access it. We would have basically been on our own. Went ahead and opened a High Yield account with our reputable HELOC financial institution. Getting a few dollars less in interest but definately worth the piece of mind.

Thanks for sharing your experience, Ray.

Since mid-week last week, the Savebetter site has been undergoing “maintenance” and should have been back online yesterday, January 30th. Nope – down for 5 days and counting. There is no communication other than “we’re having problems, try again later”. This is very disconcerting as I have been unsuccessfully trying to withdraw funds (bank transfer data is now missing from my account). I sent an email to their CEO, Marcel Bock. No response.

I can see how you’d be frustrated. I’m confident they will resume normal operations today and improve communication. I’m sure it will be difficult to get a hold of the CEO. But you can reach them by email at service@savebetter.com, via live chat on SaveBetter.com, or by calling (844) 994-EARN (3276).

Update: the site is back up and running.

I recently opened an account with them. How do I know my money is actually in a particular bank? Can I go to that bank and make sure my money is there? I have only had my account for a week and put money in a No-Penalty CD.

Once your deposit is transferred, it is held in a custodial account (a pooled bank account) with the selected institution. In other words, your funds are always held with an insured institution. Most importantly, the FDIC or NCUA insurance is transferable to you with the selected institution up to the applicable limits.