Mint Review – How I Use Mint.com to Keep Track of My Money

Keeping tabs on your finances is both easier and harder than it used to be back in the old days. (And by “old days,” I mean the 1990s).

On the one hand, you no longer have to choose between tracking every penny by hand or firing up the kerosene-powered spreadsheet program to record your income and expenses. (If you were lucky enough to have a computer at all!)

On the other hand, since so much of our finances are handled digitally, it can be harder to keep tabs on it. We no longer keep our finances centralized in a single bank.

This is one of the reasons I use Mint.com. They make it easy to keep track of all of my financial accounts.

Editors note: PT now uses Empower to track his net worth. If you’d like to give that a try, you can read our Empower review here.

Mint launched back in 2006. The program was created by Intuit, who also created Quicken, Quickbooks, and Turbo Tax.

With Intuit’s proven track record of simplifying personal finance, Mint has made itself one of the most trusted names in modern budgeting. And it’s free!

Even though Mint has been around for quite some time, Intuit works consistently to improve program and be more responsive to budgeters’ needs. Here’s what you need to know about how Mint can help you take better care of your money:

Table of Contents

How I Use Mint

I use the free online-based software, and the free smartphone app (available for both Apple and Android).

With this, I can keep track of all of my family’s financial accounts. This includes our checking and savings accounts, credit cards and other loans, the mortgage, 529 accounts, and all of our investment accounts.

I check the app about once a week to see how my accounts are doing. I also receive alerts when I have a low balance or when I’ve spent an unexpected amount in a spending category. It helps prevent me from mindlessly overspending and allows me to adjust before I get us in the red.

I also love that Mint tracks my net worth. This lets me keep an eye on our overall finances without forcing me to do my own calculations.

While I use Mint mostly to see the big picture of our money situation, you can do a lot more with the program.

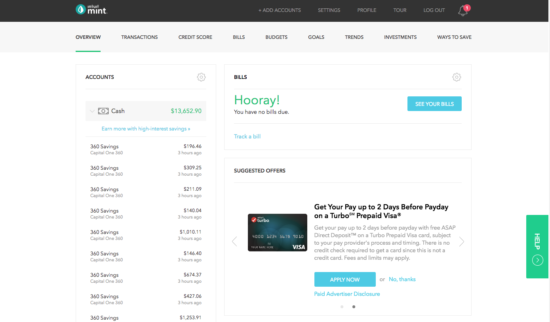

Overview: Getting the Big Money Picture

The magic of Mint lies in the fact that you can get all of your financial information in a single dashboard. When you sign up with Mint, you provide the program with your financial accounts.

You can include everything from your bank accounts to your investment and retirement accounts, bills, credit cards, 529 accounts, and real estate purchases.

Over the years, Mint has expanded the number and types of accounts it can connect. Now you can link up to smaller banks, utility companies, and other similar accounts that may not have been linkable in the past.

The more accounts you can link to Mint, the more complete your financial picture will be. The user interface for signing up is smooth and easy to use. It can just take some time to plug in all the necessary information.

Once you have linked up all of these accounts, Mint allows you to see all of your financial information in one place, including your net worth. I love being able to track my net worth over time.

Security

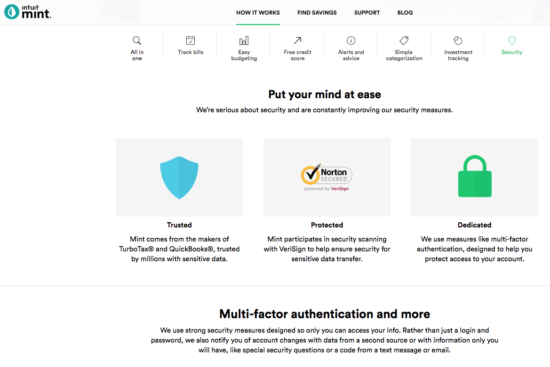

It’s important to note that you must provide Mint with your login information to access your accounts. People are often leery about providing this kind of information online.

Let me assure you that Mint offers the same kind of security you see at an online bank. This makes them just as safe as Capital One or Bank of America.

The program uses VeriSign to help ensure security for sensitive data transfer. It also uses measures like multi-factor authentication to help you protect access to your account.

In short: It’s as secure as checking your accounts on your bank’s website.

The Features

You can certainly use the dashboard overview to keep an eye on your finances as I do. But, Mint can do a lot more than give you a bird’s eye view of your accounts.

Let’s go through all of these features and how you can use them:

Transactions

To get into the details of your finances, Mint tracks your transactions and automatically assigns a category for each one.

Mint is pretty good (but not perfect) at figuring out the correct category for expenses and income based on the vendor. But this can lead to some miscategorization that might make your budget tracking a little more complicated.

For instance, all our purchases from Walgreens are categorized as Pharmacy. Even when I purchased candy for Halloween or printed out family photographs, it still shows up as “Pharmacy”. It’s up to you to manually re-categorize purchases like this.

You can also manually add any transactions done in cash or through an unconnected account. This is easy to do and can help you have a complete view of your transaction history.

Mint allows you to sort your transactions by specific account, account type, spending category, or date with all this information.

Credit Score

Mint allows you to access a free credit score based on your Equifax credit report. Your score is updated monthly, and you can see what factors are influencing your score to get a sense of how to improve it (or keep it nice and high).

Related: Improve Your Credit Score with Our Ultimate Guide to Credit

Bills

You can link all of your bills, from utilities to medical bills and everything in between, to your Mint.com account. This gives you a truly all-in-one picture of your finances.

You’ll have all of your financial information in one place so you won’t forget to pay a bill.

The Bills tab lets you know what bills you have due during the month. It will alert you to your available cash and credit and give you a timeline of when each bill is due. From here, you can quickly figure out how, when, and with what money you will be paying your bills.

Budgets

The budgeting feature can be an excellent resource for anyone who wants to get their spending or budget under control. Mint allows you to set monthly budgets for your spending categories. Even if you don’t set a budget, the program will provide a dollar amount as your monthly budget for a default set of budget categories.

However, you don’t have to stick with the default budget categories or dollar amounts. You can get as specific or general as you’d like in creating your spending categories.

For example, you could create a large food budget that covers all grocery spending and dining out. Or, you could get hyper-specific and break down your food categories to grocery stores, farmer’s markets, restaurants, fast food, coffee shops, and food trucks, and assign a specific dollar amount as your monthly budget for each of these particular categories. It’s all up to you.

Remember that the smaller the categories, the more manual tracking you will likely have to do. If you are starting out, it’s probably easier to use broad categories. Then break them down later if you find you need that.

Once your budgets are set up, the program will automatically track your spending in each category. Which again, is not perfect but does a pretty good job of assigning the correct categories to your expenditures.

The fun part is that you can quickly look at how you are doing in each category based on color-coding. When you have plenty of money left in a budget category, that category’s bar graph will be green.

As you get close to your limit, it turns yellow. And if you hit the limit or go over it, it turns red.

This colorful screen is an excellent tool for people who don’t want to dig deep into their transactions.

Instead, you can call up the budget screen and check the categories before you make a purchase. If you’re still in the green, you’re good to go. If not, you may want to take a closer look at your budget.

Goals

Why manage your money if you’re not going to do something with it, right? Which is why this feature is such an important part of what Mint offers to users. It helps you create savings or debt reduction goals in a fun and intuitive way.

You start by selecting your goal, follow their prompts in estimating your needs and how long it will take. For savings goals, you’ll choose which account you’ll be using to save for the goal.

The program will automatically track your progress. For debt reduction goal, the program will track the debt account and let you know how you are performing each month.

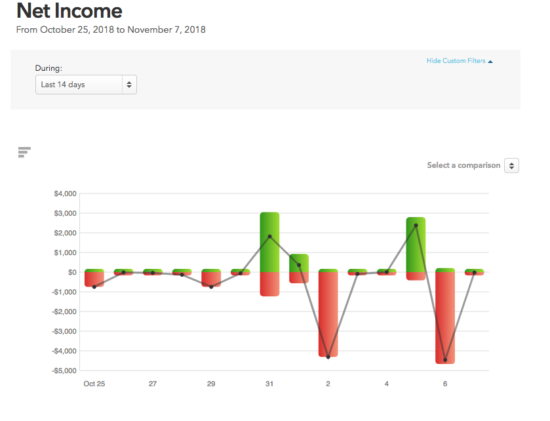

Trends

This is a section you won’t really be able to use until you’ve got a few months’ worth of transactions recorded. However, this tab can be both really cool to see and incredibly helpful, once you do.

The Trends section is where you’ll find most of your graphs and charts, which can be a lot of fun to look at.

The Trends tab will show you how your spending in each category has changed (or maintained) over time. This gives you a better understanding of your spending habits and where your money is going.

You can also use this function to check your progress over time. It will help you identify weak spots in your budget or places where you might need to make some changes.

Investments

The investments area is a drill down into your investment accounts. With online access to your accounts, Mint can determine which funds you are invested in.

It displays all sorts of information, including your

- performance

- value

- allocation

- comparisons to the market

All of which is very cool.

Related: Empower vs Mint: Which is Better?

Ways to Save

One of the unique features of Mint is its suggestion tool under the Ways to Save tab. This is how Mint is able to be free to users.

They refer you to products that will give you a better savings rate, lower fees, or lower interest rates on debt. The sales of these products help pay for the program.

The Mint App

The smartphone apps for Mint.com are a great way to keep track of your money on the go. You can’t add accounts from the app, but you can see the overview of your accounts and drill down into the details of your transactions.

I use my iPhone app 99% of the time vs. going to the site, and I love how intuitive and user-friendly the app is.

Mint Alternatives

While Mint is the oldest online budget tracker out there, it’s no longer the only game in town. It’s worth looking at how Mint stacks up compared to its two closest competitors: YNAB (You Need a Budget) and Empower.

YNAB

YNAB is geared toward folks who have never budgeted before and could use some scaffolding to learn how.

It’s an online budgeting program based on the envelope method. Budgeters set money aside for specific categories of spending. The program guides you through the budgeting , setting goals, sticking to them, and reconciling accounts.

YNAB believes that you need to be hands-on with your money to budget successfully. This means that while the program automatically imports transactions, it is also set up to make manual entry of transactions very easy and simple.

Compared to Mint, YNAB offers a little more hand-holding and provides you access to a large online community. All this comes at a higher cost; however, YNAB is free for the first 34 days and costs $6.99 per month.

Empower

Empower (formerly Personal Capital) is geared toward those with more complex financial tracking needs. One way to describe Empower’s budgeting software is an “account aggregator.”

This program allows you to track and understand every single penny in all of your financial accounts, much like Mint.

The difference is that once you link up all of your various accounts, Empower summarizes your finances and offers you basic investment guidance.

Empower also recently released a Retirement Planner tool. This tool can help you build, manage, and forecast your retirement savings in the same place you handle your regular budgeting.

The Investment Checkup feature asks you to create a basic risk profile, pick a target retirement date, and projected income sources. With this information, the program will recommend a portfolio for you.

Finally, a fee analyzer can help you to understand the fees you are paying on your current investments.

Like Mint, Empower is completely free to users. It’s an excellent option for anyone who wants a little more investing and retirement planning advice than Mint can offer.

We made a more complete comparison of Empower vs. Mint so anyone can decide which one works best for their needs.

The Bottom Line

Mint can make budgeting easy and simple, especially for anyone too busy to track their own spending. It takes a little time initially to get everything set up.

But, once it is humming along, you’ll find that Mint gives you the information you need to make the best choices about your money.

Note: An alternative to Mint would be to create this with a manual spreadsheet and update it yourself by logging into your accounts periodically. Lucky for you, I’ve created such a spreadsheet.

Time to get started tracking your accounts with Mint. Sign up for free and add your accounts to see your net worth.

Hey PT- I realize this was written a couple years ago… Do you have any updated info on mint v mvelopes v ynab? -Katie

I appreciate the comments on this site. Our financial advisor suggested we sign up on mint.com, and I was taken aback by the fact that it sees all of our accounts (I thought it would just be checking). So it’s good to see others’ experiences of the site.

I like Mint! They also have a pretty good help page that tells you of known and resolvable issues and other issues that have not been fixed. The help page fixed all my problems with the exception of one, my car loan shows up as a credit card because it is through a small bank. However, they were working on a solution. I haven’t checked to see whether I can now change the designation because it really doesn’t matter.

For the first 3 months on Mint I could not get my main bank to load several accts into Mint after numberous tries. All other accounts were tracked just fine. Then, one day my main accts showed up and have been working and loading each time I log in. This has helped me with my finances more than just about any tool I have found. (Second to Dave Ramsey)

I’ve noticed that I have to actually press the update button on the Overview page now. Before it used to auto-update when I logged in.

If that’s not the issue then I have to think it’s something with the secure connection with BOA and Fifth Third.

I have to assume that If everyone was having issues with BOA updates, then we’d be hearing about it. I’d encourage you to report this as an issue under the “get help” section. Hope you can get it worked out.

@PT-I was able to add my accounts to Mint a few weeks ago, but they never update with current information. And it’s not just my login information because my daughter has an account and I incorporated her information as well and it never updates either. I do not use “Safe Pass”, which is what the help section says could be the problem. While BOA had balances from when I first was able to sign in, my Fifth Third accounts show up, but with 0 balances. I’m so disappointed that I can’t continue using these tools to track my finances! I REALLY like using these snapshots and the fact that there are Apps out there, but so frustrating right now! I had to resort to creating a spreadsheet to track my transactions until I can get this thing going! I’m so bummed that Quicken is cutting this off in 2 weeks!

@Becky – Yes, I was a fan of Quicken Online too. I still have my old account there. Are you able to see any detailed information? Or are you saying you can’t see data from BOA because you can’t do an update? When I’ve had update trouble in the past, it’s always because I have my login security credentials wrong.

As for Mint paying bloggers, I don’t think they do that. To clarify, I do not do paid posts (e.g. “here’s $100, please write about x product”). They did just open their affiliate program up at Commission Junction though. That could have something to do with the increase in reviews you are seeing. Definitely made me more motivated. But I love Mint and would (and have) written about them long before they had an affiliate program.

I was using Quicken Online, which I loved. Then just this month, they are closing it down and incorporating into Mint.com. I was fine with this, except now on Mint, I cannot see my activity from either Bank of America or Fifth Third Bank, which is where I do almost 90% of my banking. I just logged in this morning and NONE of my accounts would update. Wondering if you’re having the same issues? Also wondering if Mint is paying bloggers to write about their site since I’ve seen several posts about them?

This is what i have been looking, one stop management for all personal finance matters.. excellent…

Great comment, AG. I used to use My Portfolio, which incorporated reward and airline miles. Very cool.

I don’t use mint.com but I do use Bank of America My Portfolio. It provides all of the same features you discussed (including net worth calculations). I agree with your overall point that anybody who really wants to get ahead financially should have some dashboard metrics and information they are reviewing about all of their financial accounts.

Let’s face it. Seat-of-the-pants accounting is a Betty Crocker recipe for financial disaster!

All of these tools are ultimately designed to get us in touch with our money. Being out of touch with our money and where it’s going is like aiming for financial security without a roadmap. Good luck with that!

I agree, my portfolio is great – but lacks one very useful feature – there is no iphone app! Mint is great because you review your budgets before you buy in a store/restaurant. Now if Mint would only figure out how to connect to BofA everything would be great…