Self Employed? Here’s Everything You Need to Know About Disability Insurance

According to the Council for Disability Awareness (CDA), “over one in four of today’s 20-year-olds will become disabled before they retire” and the average length of disability is a frighteningly long 31.2 months.

These statistics reflect the fact that illness, rather than injury, is the leading cause of long-term absence from work, accounting for 90% of all disability claims. And even the most safety-conscious among us aren’t immune from disease.

Disability insurance protects your income if you become disabled. With short-term disability insurance, you can expect to receive payment for up to six months, while long-term disability insurance policies can pay out until retirement. Your disability insurance cost will depend on the payout amount that you choose and other factors like your age and health.

As important as disability insurance is for all workers, the self-employed have a particular need to protect their income. But policies for the self-employed can be difficult to find. Here is what you need to know about finding disability insurance when you are your own boss.

What is Disability Insurance?

Disability insurance protects your income in the event that you become disabled. While life insurance and health insurance are important, you don’t want to overlook disability insurance.

There may nothing more valuable to your financial health as your ability to earn income. If for any reason you’re no longer able to work, disability insurance can kick in and replace part of your lost income.

In addition to Social Security disability insurance, there are two types of disability insurance that you can buy–short-term and long-term insurance. Let’s take a look at the difference between the two products.

What is Short-Term Disability Insurance?

As the name suggests, short-term disability insurance is only meant to temporarily replace your income. Here are some of the common characteristics of short-term disability insurance.

- Waiting period: Typically less than 14 days

- Benefit period: Typically 3 to 6 months

- Percentage of income replaced: Usually 60% to 70% of gross income

If you suffer an injury or an acute illness that keeps you from working for a few weeks or months, short-term disability insurance can fill the income gap. But if you’ll be away from work for longer than that, short-term insurance won’t be enough. That’s where long-term insurance comes in.

What is Long-Term Disability Insurance?

Here are some of the key characteristics of long-term disability insurance.

- Waiting period: 30 days to a year

- Benefit period: As little as two years but could last until retirement

- Percentage of income replaced: Usually 60% to 80% of gross income

As you can see, you have to wait longer to start receiving long-term disability insurance. But, depending on the policy that you choose, long-term disability insurance could literally payout for decades until you reach retirement age.

How Does Disability Insurance Work?

With disability insurance, you’ll pay a monthly premium as with other types of insurance. If you suffer a disablement, the waiting period (also called the elimination period) will need to elapse before you can begin receiving benefits.

Typically, the longer the waiting period, the more affordable the monthly premium. With long-term disability insurance, you could significantly lower your monthly premium by choosing a six-month waiting period vs a shorter period like 30 days.

But what if you can’t go six months without an income? That’s where short-term and long-term disability insurance can complement one another. By purchasing both, you’ll pay less for long-term income protection while still protecting your short-term income.

But the cost of short-term and long-term insurance can be very similar. So if you already have a six-month emergency fund in place, you may be better off only purchasing long-term disability insurance.

How Much Disability Insurance Do You Need?

The answer to that question depends completely on your financial situation. As mentioned above, disability insurance can generally replace up to 80% of your income. But if you choose the highest payout you’ll also pay the highest premiums.

If you’d like to save money on premium, you could choose a smaller payout. But if you have several large debt obligations (think student loans, mortgages, car loans), that probably wouldn’t be a smart move.

If your house is paid off and you’re debt-free, you may be able to get by with a lower payout. Otherwise, you should probably shoot for the highest payout that you can afford. If you’re still not sure, you may want to get some legal advice. Consider trying Just Answer to ask a lawyer your specific questions.

How Much Does Disability Insurance Cost?

According to Breeze, disability insurance cost ranges from 1 to 4 percent of your current income.

So, for example, let’s say you make $50,000 per year. In that case, you could expect to pay $500 (1%) to $2,000 (4%) per year for disability insurance. That works out to a monthly payment of $42 to $167.

If you choose a plan with a max payout, expect to pay closer to 4% of your current income. As you choose progressively smaller payouts, your disability insurance cost will move closer to the 1% range.

Other factors that affect disability insurance cost include your age and health. The younger and healthier you are, the less expensive you can expect disability insurance to be. And, once again, choosing a longer elimination period will lower your premiums as well.

Disability Insurance for the Self-Employed

Now that we’ve covered the basics of disability insurance and how it works, let’s take a closer look at self-employed disability insurance. Disability insurance for the self-employed can be more complicated. There are a few extra things you’ll want to consider. Here’s what you need to know.

1. You May Need to Work Without a Disability Net for a Few Years

I know that’s probably not news that you wanted to hear, but it’s true. The insurance industry is all about mitigating risk. And as every freelancer knows, making a go of self-employment is (in some ways) riskier than collecting a steady paycheck.

Related: Self-Employment–A Year Later

For that reason, insurers need to see that your income is relatively stable before they will even begin to look at underwriting your policy. According to Barry Lundquist, President of the Council for Disability Awareness, insurers need to know that your self-employment status is a career, and not just something you are doing while you’re between jobs.

In addition to your employment and income history, your insurer will consider if you are a good health risk and if you pose a risk of policy lapse–which tends to be high among the self-employed.

Considering the fact that insurers lose money on disability insurance policies in the first year, even without any claims, it’s understandable why your insurer would want to make certain you will keep up the premium payments.

All of that adds up to needing good credit and several years of income records–generally about three–before you can find a disability insurer willing to take on a self-employed client.

2. The Passive Income Conundrum

An additional issue that the traditionally-employed don’t have to deal with is the question of how passive income fits into underwriting for the self-employed.

For instance, I published a book on retirement earlier this year, which is earning me royalties. My hope is that it will continue to earn royalties for me throughout the coming years.

While that money will add to my income, I also don’t have to work to bring it in. So how will an insurer view my passive income when underwriting my policy?

According to George Davidson, president of Secura Consultants, it’s important to remember that there is no such thing as purely passive income.

Royalties from books are at least somewhat dependent upon promotion and marketing, so suffering a disability just when a book is launching could have a negative effect on your royalties.

How to Get Around the Passive Income Problem

For that reason, Davidson recommends working with an insurance agent who is willing to negotiate with underwriters.

In general, underwriters will simply disregard passive income that is less than about 10% of your income as a whole. So if you earned $50,000 total last year, of which $5,000 was from royalties, your insurer will simply look at your total income without worrying about your royalties.

If your passive income is a larger share of your total income, a good agent who has experience in negotiating with disability insurance underwriters can get your passive income alleviated in underwriting, particularly if he can prove that a disability would have a negative effect on the promotional work that you do.

Basically, it’s important to be able to pinpoint the continuing work you do in order to bring in your “passive” income. And make sure you communicate that aspect of your business with your insurance agent.

Related: Understanding Your Small Business Insurance Needs

3. How to Find the Right Self-Employed Disability Insurance Product

There are a couple of ways to make sure you have the disability coverage you need as a freelancer.

The first is to plan ahead–before you even leave your traditional job. According to Barry Lundquist, a small percentage of disability policies are portable, so you can take them with you when you quit your cubicle-dwelling job.

Another option is to look for professional groups or associations that might offer insurance options. For instance, a lawyer deciding to work freelance from home might be able to purchase a less expensive plan through her local Bar Association.

Finally, it is certainly possible to find a reasonably-priced individual policy. Davidson recommends the International Disability Insurance Society as a place to start your search. Or you could get a disability insurance quote online from Breeze.

Breeze – Disability Insurance for the Modern Workforce

Over the past few years, several online companies have tried to modernize the process of shopping for things like life insurance and health insurance. But Breeze is one of the first insurtech companies to focus on disability insurance.

The application process with Breeze is 100% online. And they say that their approval process rarely requires a medical exam or even a phone call.

In fact, they say you can go from quote to coverage in 15 minutes!

What Makes Breeze Unique?

In addition to their streamlined application process, Breeze has several other features that set them apart:

- Their employees don’t earn commissions. They only have your best interests in mind.

- Renewability: Their policies are guaranteed renewable until ages 65 or 67

- Monthly benefit: $500 to $20,000

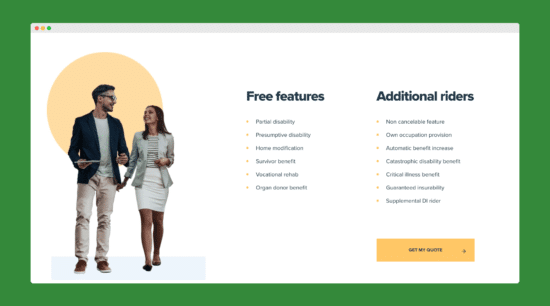

- Free features: Their policies come with built-in features like partial disability coverage, presumptive disability coverage, home modification coverage, survivor benefit, vocational rehab, and organ donor benefit

Additional Disability Insurance Riders

Breeze offers all of the most popular disability insurance riders, including:

- Non-cancelable feature

- Own occupation provision

- Automatic benefit increase

- Catastrophic disability benefit

- Critical illness benefit

- Guaranteed insurability

- Supplemental DI rider

The first two riders on the above list are definitely worth considering. With a non-cancelable rider, you’ll guarantee that your policy can’t be canceled, reduced, or modified for any reason.

An own occupation provision is also important. With this disability insurance rider, your policy will pay out as long as you are unable to work in your own occupation. This could matter the most for people who have high-income jobs like medical professionals.

For instance, imagine that a surgeon had “own occupation” coverage. In that case, he or she would receive disability insurance benefits as long as his disability kept him from working as a surgeon–even if he could do other work, such as becoming a primary doctor.

Get a quote from Breeze and start protecting your income today.

Make Sure You Are Adequately Protected

Your income potential is your greatest asset. It pays to protect yourself against the possibility of losing that asset. After all, you insure your cell phone. Why not your income?

At one time, shopping for disability insurance could take days or weeks. But Breeze now offers a streamlined application process that can all be handled online. In some cases, you may be able to get coverage within 15 minutes.

There really are no more excuses. Don’t let your self-employment keep you from getting the income protection that you need. Start shopping today for short-term or long-term disability insurance with Breeze.

Have you shopped for disability insurance? What was your experience?