Protect Your Small Business with Insurance from CoverWallet

I have been working for myself for nearly a decade, but I have only recently started to think of myself as a small business owner. As a freelance writer, I thought I could opt out of many of the expensive aspects of traditional entrepreneurship.

I thought I had no need for things like small business insurance. After all, I have no employees and an office that is not open to the public. I always assumed there was no need for me to carry insurance for my one-woman business.

Unfortunately, that attitude could have gotten me into some pretty hot water. And I’m very lucky that the belated realization that I need to treat my business like a business never caused a financial disaster.

The fact is that every business owner–no matter how small–should protect themselves with insurance. But it can be tough to know exactly what kinds of insurance you need and when you need it most. Every small business has different insurance needs based on its industry, location, and size. And getting the right coverage package can feel confusing.

CoverWallet is an online small business insurance platform that can help you figure out your coverage needs and find the policies that will make the most sense for your business. CoverWallet makes researching and buying business insurance as simple as any other internet shopping.

Here’s what you need to know about getting the small business insurance coverage you need:

Why You Need Small Business Insurance

The law requires some businesses to carry certain types of small business insurance. For a cash-strapped entrepreneur, skipping the optional insurance may seem like an easy way to reduce overhead. This was my belief for the first few years of my freelancing career. But skimping on your insurance needs means you might be flirting with disaster.

What kinds of disasters might you face? First up are legal types of disasters. Even though you may be handling everything legally, there is still potential for someone to file a lawsuit against you. Dealing with a lawsuit costs time and money your business can’t afford. Getting appropriate coverage will help you and your business weather any potential lawsuits without them affecting your continued success.

Then there are natural disasters. The hurricane that leaves your showroom hip-deep in water. The fire that destroys your warehouse. The earthquake that cuts off your internet service for weeks. Having the right insurance will mean you are prepared to rebuild after a fire, flood, or act of God.

Finally, there are man-made disasters, such as theft or vandalism. Your small business insurance will cover you in case of stolen inventory or broken windows.

The good news is that your business insurance premiums are tax-deductible. The insurance you need may not be as expensive as you fear since it will reduce your overall tax burden.

See Also: Small Business Mistakes to Avoid

CoverWallet Has You Covered

If just looking at the list above has you hyperventilating–after all, needing insurance usually means you need to talk to an insurance agent–there’s no need to worry. The online small business insurance platform CoverWallet has taken the sting out of shopping for small business insurance.

CoverWallet describes itself as a concierge service to help business owners manage their commercial business needs all in one place.

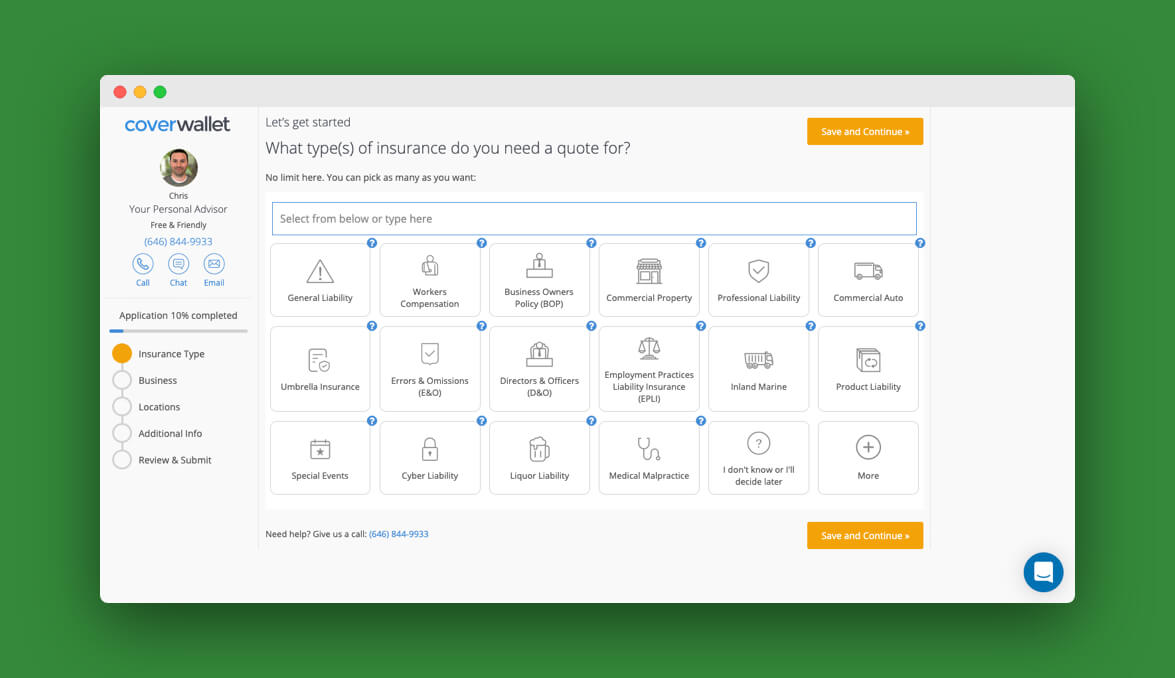

The company partners with insurance carriers to cover 30 different types of business insurance. CoverWallet does not provide the insurance themselves but instead matches business owners with insurers who can offer them the coverage they need. Their partners include many heavy hitters in the insurance industry, including Liberty Mutual, Berkshire Hathaway, Progressive, and AmTrust, among others.

In addition to their coverage options, CoverWallet also has excellent resources for small business owners. You can read through their insurance guide and tips for business owners to better understand your coverage needs.

From there, the site will ask you for some basic information about your business. These questions include:

- What industry you are in

- Your history of business earnings and losses

- How long you have been in business

- The number and type of employees you have

- Your business assets

- Tax filing information

With this information, CoverWallet will then send you quotes from compatible carriers who can cover your insurance needs. In general, CoverWallet will get you quotes within one to two business days.

Since CoverWallet does the legwork for you of finding multiple quotes, you can easily comparison shop for the right policy without having to spend days on the phone or in insurance agents’ offices.

It’s important to note that your business credit score may have an impact on the insurance rates you’re able to acquire. A business credit score may not be required to apply for insurance, but a higher business credit score will lower the price of an insurance policy.

So it’s definitely worth paying attention to your business credit score. If you’re unsure of how to build business credit, give Nav a try. They’ll help you monitor your business and personal credit for free.

Related: Get Free Personal and Business Credit Scores at Nav.com

CoverWallet can be especially helpful if you need multiple policies for your business. All of your information will be conveniently located on the company’s platform. That means you can access any information you need, view your policies, file any necessary claims, and make your premium payments all from the My CoverWallet dashboard.

CoverWallet also stores all of your insurance certification information on your account. That makes it very easy to get those certificates if you need to submit proof of compliance.

While the CoverWallet online interface is easy-to-navigate and intuitive, you also have the option to speak to a representative via email, chat, or over the phone. Chats and phone calls are answered during business hours (until 6 pm ET on business days), and you can schedule a time for a representative to call you back.

Get a free quote from CoverWallet today!

Everything you need to keep your company protected, at a competitive price. All online, in minutes. Receive customized advice and get free online quotes, in no time.

Make Sure You Are Adequately Covered

For a long time, I thought my business wasn’t big enough for business insurance. But if I want to ensure the continued success of my business, adequate coverage is a must. Every small business owner needs to recognize that not only are they legally required to carry some forms of insurance, but that their future may depend on getting the right coverage.

Previous generations of entrepreneurs could have been excused for procrastinating on finding the small business insurance they needed. Back then, shopping around would take days, if not weeks, and it could be difficult to know exactly what you need.

But now that CoverWallet offers a one-stop-online-shop for all of your small business insurance needs, there’s no reason not to get the coverage that will protect your business. You can learn what you need, get a quote, ask questions, purchase policies, pay your premiums, file claims, and store your insurance certification all in one place.

That kind of peace of mind, all in one place, will help small business owners sleep well at night.

Do you own a small business? What kind of insurance policies do you carry? Tell us about it in the comments!