The Complete Guide to 529 College Savings Plans

Have you been thinking about saving for your child’s future college expenses? Are you curious if you should get started with a 529 college savings plan?

It took me three years from the time I started thinking about setting up a 529 college savings plan to actually open one up. It’s one of those big financial check-offs that just seems to elude us…till it’s too late.

If you’re like me, you’re probably wrestling with this big life decision too and not doing much. But here you are. Reading this guide. So let’s do it! For real this time.

I’m confident this guide will give you everything you need to understand 529 college savings plans options and get one open for your child(ren) today!

After all, I’m proof that you can do this. I now have 529 college savings plans opened for each of my three children and I’m automatically contributing a small amount each month to fund them. Our goal is to fund a year or two of college.

If I can do it, you can!

Table of Contents

What is a 529 College Saving Plan?

A 529 college savings plan is a savings plan for educational expenses (named after the Federal tax code 529) set up by individual states or institutions. They’re designed so that you are encouraged to help save for your child’s education (college or trade school).

The encouragement comes in two forms: the ability to save money free from federal taxes and the ability to receive a deduction on state taxes (if you have a state tax and you use your state’s plan).

These state-sponsored 529 college savings plans have been around since 1996, but they have been gaining real popularity in the last few years.

The 529 college savings plan is sort of the Roth IRA of the college savings world. Meaning, your savings grows tax-deferred and the withdrawals are tax-free as long as you use them for qualifying educational expenses.

Fewer taxes. More college savings. What’s not to love? 529s are a really good deal.

529 College Savings Plan Rules

The rules are simple. You can contribute after-tax dollars to the plan of your choice and withdraw the contributions and investment earnings from the plan at any time for qualifying higher education expenses used by the beneficiary of the plan (aka your child).

Contributions are therefore limited to the amount necessary to pay for the beneficiary’s qualifying expenses. However, as you’ll see below the funds can be transferred to other beneficiaries.

Note gift tax rules can affect your contributions and some states do limit the amount of annual contribution to their plan. Have more nuanced questions on the rules? Visit the IRS Q&A page on this subject.

Savings vs Prepaid Plans

There are two types of 529 college savings plans: prepaid and savings. It’s important to know the difference. Some states offer one or the other, both, or a plan that combines the features.

Prepaid 529 Plans

Prepaid 529 Plans usually give you more tax benefits and college discount for schools in that particular state. The prepaid plans are considered inflation-busting since they allow you to save for college at today’s prices.

But they also come with more restrictions. For instance, if you decide to use a prepaid plan in your state and then later send your child to a college out-of-state you’re going to forfeit some of the savings you were able to get by being in an in-state prepaid plan. This varies greatly by state plan.

If you don’t have a state tax, like me in Texas, then you should likely look into savings plans just to give you more flexibility.

529 Savings Plans

529 Savings Plans are more flexible. You can usually use these types of plans at any accredited college or university in the country. For instance, I’m a resident of Texas and have a 529 Savings Plan with Ohio.

Since it’s a savings-type plan, I can use the funds wherever I want, as long as it’s for qualifying education expenses.

It’s important to note that you can use both plan types. See the story below from someone who used both types.

529 College Savings Plan Calculator

Let’s calculate what’s possible with a 529 college savings plan. The simple yet elegant 529 college savings plan calculator from Backer perfectly visualizes what the results of using a 529 plan could be for your child’s college expenses.

I plugged in a hypothetical and was pleasantly surprised to see that by using a 529 college savings plan to regularly save for my five-year old’s college expenses I will be able to save an additional $3,000 by the time he’s ready to go to school.

Try the calculator from Backer.com out for yourself.

The following information explains the benefits and risks associated with these accounts.

Benefits of a 529 College Savings Plan

This method of saving for college expenses offers benefits beyond tax breaks and deductions:

- Parents retain control of the fund. This is important if you worry that your child may decide to use their college savings for a trip or a new car. You have control over the account and make the decisions when and how the money will be used.

- Until you decide to withdraw the money you, will not have to worry about reporting information on your tax return. The year you withdraw the money will be the only time you receive a 1099 form to report taxable or nontaxable earnings.

- These plans offer flexibility. You can move your investment to another 529 savings plan or change the beneficiary (see how below) if your child does not go to college or receives scholarships which cover the expenses.

- Most 529 college savings plans allow for substantial deposits and anyone can contribute, not just the beneficiary’s parent. Grandparents, extended family, and other individuals can contribute to your child’s education over the years. In most cases, there are no age restrictions or income limitations for these plans.

- Plans owned by a parent or other donor will not have a significant impact on your child’s ability to receive federal financial aid. That’s because the 529 account is considered a “parental” asset.

- With the recent tax code changes, 529 accounts can now be used to pay for up to $10,000 per year of K-12 educational expenses.

Disadvantages of a 529 College Savings Plan

Using a 529 college savings plan can be an excellent way to put money back toward ever-growing college expenses. But they are not without certain risks or penalties.

- Withdrawing money for anything other than qualified educational expenses triggers income taxes on the earnings as well as a 10% penalty. If you have received a state tax deduction you may have to repay that as well.

- Some colleges take into consideration family-owned 529 college savings plans when determining scholarship or grant recipients.

- Certain savings plans have high administrative fees which can reduce your earnings. It is very important to carefully review all information before committing to a specific plan. Do your research, shop around, and compare plans carefully to find the best option for your family.

When to Start a 529 Savings Plan?

Just start now!

Don’t get too caught up in the different kinds of plans/accounts. Just pick something and go for it.

The truth is, a majority of folks out there wait till it’s too late to start doing anything. And it’s not because they didn’t have the money. It’s because they thought about it a couple of times over the years and never acted–either because they were confused by the choices, or too lazy to set it up.

Had they just started an automatic savings withdrawal to a CD or simple savings account they’d be better off than where they find themselves.

I used to be one of these people. For the longest time, I hadn’t decided on a specific place to stash my college savings.

You can actually open a 529 before your child is born. You will just need to remember to change the beneficiary to your child once they are born and you get a social security number.

Should You Use Your State Plan?

If you live in Texas like me your situation is pretty good. You don’t pay state income tax.

Therefore, there are no college plans that are particularly advantageous for Texans, unless you are dead set on sending your kid to a Texas school. In which case, there are prepaid plans that might be better for you.

Bottom line, you’re freer to look at another state’s plan. Most plans will let you participate in their plan and use the funds anywhere.

That being the case, the next thing you need to worry about is fees, flexibility, and fund options. Online publications are always ranking 529s based on these factors. You could look through one of those lists and narrow down your choices, pull the trigger, and start saving.

If you don’t have a state income tax like me, then you should consider Backer as your home for your 529 College Saving Plan. You won’t miss out on any deductions by using Backer’s crowdfunded 529 college savings plan service.

Related: See our list of the states without an income tax.

What Funds Should You Invest in Within the Plan?

Once you have the 529 college savings plan set up, you’ll need to decide what to invest in.

Most plans offer target-date or age-based funds. These fund accounts get more conservative as your child ages.

That way, when your child is 16 and the market crashes, half your investments won’t be taken. By then, you’ll be in more conservative investments.

See our guide to determining the proper asset allocation for your 529 college savings plan.

Be Careful with Age-Based Plans

Here’s a quick story about how important it is to set the correct beneficiary on your plan if you are using age-based funds.

A few year’s back I was reading a r/personalfinance thread (great place for pf advice by the way) from someone considering the Ohio 529 Savings Plan.

I’m a fan of that plan, so I chimed in with how I thought it was a good plan for me, a Texan since I do not have a state tax deduction to consider.

Additionally, the CollegeAdvantage plan (as it’s commonly known) comes with an easy online interface and most importantly, low-cost funds from Vanguard.

The redditer went on to ask me about the different funds and which one I chose.

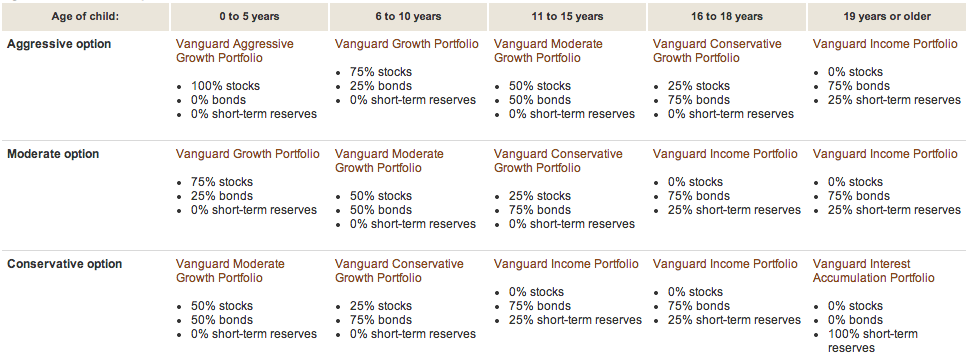

I shared with him that I chose the Vanguard Aggressive Age-Based Option for both of my daughters. When studying the plan on the Vanguard website I discovered that the fund’s mix of stocks, bonds, and cash was based on the beneficiary’s age.

Here’s a visual breakdown from Vanguard:

This is something I remember knowing with my first daughter. But I somehow forgot when opening up the second daughter’s 529 account.

You see, we didn’t have our second daughter’s SSN or even birth date when we opened the account. We actually opened it using my wife as the beneficiary, before the birth.

By the time my second daughter was born, we had funded the account and we were already invested in the age-based fund: 75% in bonds and 25% in cash. Why this allocation? Because my wife is older than 19, obviously!

So thanks to this Reddit thread I realized the error of my ways. Now I know why my second daughter’s account has performed so poorly compared to my older daughter. Because the second daughter’s account has been in bonds and cash! So embarrassing. Here’s the annual performance comparison:

Daughter #1 (under 5yrs):

Daughter #2 (actually based on Mrs PT’s age – over 19yrs):

Once I realized this, I changed the 529 college savings plan beneficiary, something I was dragging my feet on because I didn’t think it mattered.

I spoke with CollegeAdvantage briefly and they assured me that once I changed the beneficiary information the bonds/cash funds would be sold and the account would reinvest into stocks (based on the under-five bracket).

This is certainly something I should have done 2.5 years ago. The good thing is that we’ve got 16 more years to make up the difference.

The moral of the story is to always take time to understand your investments. Even with the best intentions (like starting a 529 college savings plan before your child is born), mistakes can be made.

College Savings or Retirement Savings Which is More Important?

I think it’s important to take care of your retirement needs prior to considering college savings. There are no loans or scholarships available for your retirement.

Not to say you need to have your retirement fully funded before you save for your kids. You just need to be making the maximum contribution needed to help you achieve your retirement goals and then think about college savings.

This is just my view. You may take a different stance.

The Millionaire Next Door Shouldn’t Pay for Their Kid’s College

I’ve been listening to the Millionaire Next Door lately and the authors spend a lot of time talking about how millionaires (specifically the next door variety) end up using their wealth for their kid’s education (private schools, colleges).

They say that this is a mistake because children that receive large financial gifts are not frugal with that money.

Frugality is what is credited with making ordinary, hard-working people into millionaires to begin with. So by giving your children a big financial gift, you are depriving them of one of the factors that will help them become a millionaire themselves.

I’m a believer in that approach. Mrs. PT is a staunch believer in it. The money we have saved in our 529 college savings plans for our children will be more of a supplement. Right now we are placing $75 a month for each child into 529 College Savings Plans.

With a few lump sum contributions and some birthday money, we will likely be able to help our children out with a few semesters of college.

We’re excited to see our kids taking some responsibility for the cost of their education. They can do this by working, using scholarships, or even taking small loans (which I’m not entirely opposed to)

See Also: Teaching Kids About Money [The Complete Guide]

What Other Blogger/Parents are Doing

I reached out to some of my blogging friends and readers and asked them this question:

“Do you currently use or plan on using a 529 college savings plan to save for your child’s college education? If so, why? If not, why?”

Sense to Save – We do not currently have a 529 college savings plan for our baby. Right now, we have a small savings account for us to buy unexpected things he might need. Once we get our car paid off, we’ll increase our retirement savings and start a college savings account for him. I expect that to happen sometime next year.

No Credit Needed – I do not use 529s to save for college, at least right now. I have three kids, and I’m working hard just to put $2,000 per child in their Education Savings Accounts (ESAs). If at some point, I’m available to fully-fund their ESAs and all of our retirement accounts, I might consider opening 529s.

Read our article on the different ways to save for college, which includes ESAs.

Free From Broke – We do have state 529 college savings plans for both of our children. The NYS plan is administered by Vanguard who are known for their low fees. There’s also a nice choice of funds in the plan. And of course, we get a break on our state taxes. We also like the flexibility in how the money could be used when our kids are in college.

Wide Open Wallet – I’m not currently saving for my kid’s college because I don’t think their college should come before my retirement. And I’m not saving as much for retirement as I would like. When I’m maxing out my IRAs then I will look into saving for college.

The Happy Rock – Not currently, but our children are young. We are still trying to figure out how we want to handle college for our children. When the decision is made we will use a 529 or an ESA. If we use a 529 I will most likely not us my state’s(NJ). I will scour the 50 deals for the top one for our situation.

No Debt Plan – We do not currently use a 529 college savings plan to save for our kid’s education. We actually just started saving up money for kids in the future (none currently). We do plan to use a 529 or similar savings tool in the future, but I just haven’t had time to research them enough. Plus the amount of money we have set aside right now is pretty small. Once we get to a larger amount it will make more sense to open the account.

Budgets Are Sexy – Nope – but only because I don’t have any kids yet) If I did, however, Yes I’d hook it up with a 529 college savings plan for sure! Not that I’ve researched it all that much, but I always hear great things about it.

The Shauls – We have thought about it, but because we live overseas (and plan to for the remainder of our lives), it is hard to plan where our children would go to school. But our situation isn’t the most common in the states. If we lived somewhere, and it looked like we were going to be there for a good length of time, we would do it. It’s a good way to put money away for them, even if just to get them through the first year. We wouldn’t pay for their entire education, but enough to get them started. By then, hopefully, they will have acquired some healthy financial habits to carry them forward.

ABCs of Investing – We have RESP accounts set up for our kids (Canadian equivalent) although to be honest, it’s the grandparents that fund it. I think it’s a good idea to save some money for your kids’ education but I don’t put a lot of priority on it – ie it’s a “nice to have”.

Moolanomy – I am currently using 529 to save for my son’s college education. I chose 529 because of its low cost investing options, state tax deductibility, and tax-deferred growth. I also like the fact that I could transfer the money to other people in my family if my son doesn’t use up the money.

Rocket Finance – I don’t have 529s for my kids because I can’t afford it right now, however, I have savings accounts for all of them and I put any extra cents I can squeeze out of our budget into them.

Good Financial Cents – I currently have a 529 college savings plan for my son. We are currently using an out of state plan because I felt the investment options were far superior to what my state offered. I also felt that it made enough of a difference to overcome the state tax benefit.

My Dollar Plan – We have about two dozen 529 accounts, so I think that makes me an expert…. oh no, wait, maybe a junkie. 🙂 We use the Iowa plan for Upromise contributions, the New Hampshire plan for the 2% cash back credit card, our Wisconsin plan for the tax deduction, and the Ohio plan because it’s my favorite – low expense Vanguard index funds.

See our review of the Upromise program.

Free Money Finance – Yes, we have a 529. Why? Because we’re probably not getting any financial aid and need to save for our kids’ college. The 529 we’re in is also through our state and we can write off $10k in contributions each year.

Reader J – No kids yet, so I haven’t really checked into it too much. But Jesse at The Penny Saved brought this up; I recommend doing the math of one CD/savings deposit with variable rates per week (given the plummeting rates lately, but bound to eventually return) vs a currently tax-deferred program. Things can change with new policymakers.

More Common 529 College Savings Plan Questions

I’ve had some more nuanced questions from readers regarding saving for education expenses using a 529 college savings plan. Below I’ll answer a few. Hopefully, this will get you more comfortable with the account so you can start funding one for your kid’s college education.

1. What if my child doesn’t end up going to college?

The savings and earnings from the savings are always your money. You, the donor, always maintain control over the funds. The beneficiary (your child) has no control. You can switch beneficiaries at any time (typically once a year).

So, if your first kid doesn’t go to a qualifying institution, then you can switch the plan beneficiary to another child, yourself, or whoever.

As an example, when we welcomed our second baby girl into the world we had already opened up a 529 college savings plan for her. At the time she wasn’t born, so we needed an alternate beneficiary.

We chose my wife as the temporary beneficiary. But when she was born, it was time to transfer the account to its rightful owner, our new girl. Here’s how that process works with Ohio’s plan:

You can’t just simply change the name on the account. First, you have to open up an entirely new account (using the same account holder) with CollegeAdvantage and transfer the assets from the first account to the second.

You can’t complete this transfer using your online account access. You have to download a pdf form from this CollegeAdvantage forms page, complete it, and mail it to CollegeAdvantage at PO Box 692196 Cincinnati, OH 45269. Instructions on how to use this form can be found at this CollegeAdvantage account changes informational page.

To complete the form, you will need the account holder and current beneficiary information. You will also need the new beneficiary’s info (including SSN). Next, you will have the option to transfer only a partial amount, change the investments, and change the EFT information.

Finally, you will need to sign the form in front of someone who can provide a signature guarantee. This is different from a notary. But it looks like you can get one of these guarantees at a bank.

2. What if you don’t have anyone to transfer the funds to?

The only thing that you may forfeit for not using the funds for education spending is the tax savings on the funds and a 10% penalty on the earnings from the savings.

As an example, let’s say:

- You deposit $50,000 now into a 529 college savings plan.

- Fast forward 18 years and your funds are now worth $60,000. You’ve earned $10,000!

- Let’s assume your child decides to skip college.

- If you withdraw those funds and use them for yourself on Twinkies, the $10,000 would be subject to the tax and the penalty.

- You’d roughly owe the Federal Government $3,000 to $4,000. You’d walk away with around $56,0000 of your $60,000.

But, the 10% penalty can be waived if your child becomes disabled, dies, or gets a scholarship.

3. What if my child gets a scholarship to college, then what happens to the 529 college savings plan funds?

Like I said above, you generally have a few options: transfer to another beneficiary and give it to them, sit on the funds until another option becomes available, or withdraw the funds penalty-free (you just have to pay the taxes).

The penalty is waived if your child gets a scholarship though.

4. Should I open a separate 529 account for each child or should I have just one account?

Yes, open an account for each child. To my knowledge, you can only have one beneficiary of the funds from an account.

5. Can you withdraw 529 college savings plan funds for an emergency with or without penalty?

Generally, you have complete control over the funds in the plan. You can withdraw your funds at any time, for any reason. As I mentioned above though, you’d be subject to a tax and penalty on the earning from the savings. There is no hardship rule that I know of that would exempt you from the penalty.

6. What age or when do you HAVE to withdraw the 529 college savings plan funds?

There generally is no age or time limit for withdrawals.

7. Could the 529 college savings plan act as a nest egg fund for my children?

Using the 529 college savings plan for anything other than educational expenses would be an inefficient use of the plan. If you’re looking for a place to stash some emergency savings, consider an FDIC insured high-interest savings account or a brokerage account.

8. Should I consult a CPA, CFP, and understand the plan I’m getting into?

This is advised, but it’s not absolutely necessary. If you’re unsure about opening up a 529 college savings plan, please visit a fee-only financial professional to understand your full range of college savings options. There are other options like Coverdell ESAs that might be better for your situation.

Another reason to consider working with a pro is that each state plan and tax implications have an impact on your decision. Take time to research the plan you’re getting into. Read the guidelines of the plan. Call up your state’s plan administrator and have them explain it to you.

Do 529 College Savings Plans Actually Work?

You might have that nagging question in the back of your mind,

“when my child heads off to college in x number of years, will this really have a positive impact on the affordability? (i.e. will this really work out to benefit my child?)”

Let’s take a look at the impact the 529 college savings plan is having and how you can calm that nagging questions above.

On a macro level, we know that 529 college savings plans are gaining popularity. However, their impact on the U.S. college student is still very small. They currently aren’t being used by many folks.

Only around 5% (or 1.4 million) of U.S. college students actually used a 529 college savings plan in 2011 to pay for some of their college education.

So even though you and I know and use 529 college savings plans, parents of kids heading off to college today didn’t know much about them or didn’t bother to learn about them and use them.

It does get better when you look at the average balance. In 2018 that number is around $24,153. While that won’t pay for an entire four years at most colleges, it’s evidence that people who have 529 college savings plans are doing some serious saving.

Improve Your Chances of 529 College Savings Plan Success

Let’s go back to our question: will the 529 college savings plan really work out to benefit my child? The three factors involved in answering the question for yourself are:

- What will the cost of college be like when my child graduates high school?

- Is my savings enough, or will the return on my savings be enough?

- Will my 529 college savings plan assets reduce the financial aid my child receives?

We can somewhat control the first two factors. And the third likely isn’t much to worry about.

Controlling Costs of College

While we can’t control the actual cost of an individual college, by being open to choosing a more affordable college, we can remain flexible in our choice and choose the college that makes the most financial sense when our children graduate.

By 2030 it will likely cost a quarter of a million dollars to attend a private university (crazy), but a public university will probably cost $100,000. Still insane, but it shows the huge difference choice can make.

And if your child is willing to do two years at a community college, then that price could be reduced even further. Check out Vanguard’s College Cost Calculator to do your own projections.

Related: Read our picks for the best college degrees to get.

Controlling Savings and Return on 529 College Savings Plans

We can certainly control how much we save each month towards our 529 college savings plan. Even if it’s just a small amount each month, it can have a pretty big impact. $50 a month over 18 years at 7% expected return will net $21,700. Invest a couple of tax refunds or bonuses over the years and that number could be much higher.

We can’t control the stock market return, but we can diversify our investments within our 529 college savings plans such that they aren’t exposed to a great deal of risk the closer your child gets to graduation.

So the bottom line seems to be to save more, diversify, be flexible in college choice, and temper your expectations about covering 100% (which may not be desirable anyway…see my thoughts on millionaires above).

Controlling Financial Aid Impact of 529 College Savings Plans

But what about that third factor? How will your federal education assistance be affected by what you have saved in your 529 college savings plan?

If you look at the FAFSA right now, the 529 college savings plan is supposed to be considered as an investment asset owned by the parents. This will have an impact on how much federal student aid the student will qualify for. But only by a small amount.

According to Vanguard, the worry about 529 college savings plan impact in financial aid is unfounded.

Parents get to exclude some non-retirement assets (including the 529 college savings plan) and those 529 plan assets that do get included are only able to affect financial aid by a maximum of 5.64%.

So if you have $25,000 saved up in a 529 college savings plan and you can’t use the non-retirement funds exclusion (because you have a boatload of cash, for instance), your child will receive $1,410 less in financial aid. While that’s not chump change, it isn’t a reason to stop using your 529 plan.

Additionally, some private colleges take into account the 529 college savings plan assets when doling out aid packages.

From all of the poking around that I’ve done, it appears that this is a college by college impact and so your best bet is to be in contact with the college to learn of their policies. All the more reason to stay flexible with college choice.

How One Family Used Their 529 College Savings Plans

When it comes to diversifying contribution sources, some people use a hybrid approach involving a 529 prepaid plan and a savings plan to guarantee that most or all college expenses will be affordable. Here’s an example:

Here’s Jan Keenan, a mom of three recent college graduates and an attorney at Keenan & Austin, P.C.. She chose to use a hybrid approach to create a little more security with her education savings.

We bought MET (Michigan Education Trust) contracts for our three children when they were 12, 11, and 8. We also put money into 529 savings plans for them when they were a few years older. The MET contracts paid for their tuition, and the 529 savings plans paid for their room, board, and books.

We paid $20,000.00 for each MET contract and they paid out an average of about $40,000.00 in tuition costs for each child. We put $22,000.00 into the 529 for our oldest, $21,000.00 for our middle child, and $18,000.00 for our youngest. By the time each kid got to college, they each had about $28,000.00 in their 529 accounts.

Remember that prepaid plans have their pros and cons, so make sure you understand the difference between a 529 savings plan and a 529 prepaid plan at the individual state level. But I do like this hybrid approach and honestly, I’d never thought of it. Prepaid plans are only available in some states.

Open Your 529 College Savings Plan in 5 Mins with Backer

If you live in a state that doesn’t have income tax, or you don’t want to use your home state plan for any reason, you have a lot of plans to choose from. With each state offering their own plan, just the research alone can be enough to keep you from getting started. That’s where Backer comes in.

Backer makes choosing and opening a 529 account easy. You can go from start to finish in about five minutes. Just answer a few questions about yourself and your child and Backer will make a recommendation of which plan is best for you. If you agree with their plan selection and investment choices, they will open the account for you, in your name.

That’s an important point–the 529 is in your name. It isn’t like if you were to invest with a brokerage house, say Betterment for example, Backer simply helps you open and share the account with others, they do not take the funds under management.

Also note, the rules that apply to the account remain the same whether you have Backer help you manage things or not. Maximum contributions, withdrawal rules, and approved use of funds all still apply.

Building Your Backer Team

If getting help choosing a 529 isn’t cool enough, their specialty lies in the ease of getting others to jump in and help the parents save. When you set up your account Backer allows you to “build your team.” This means you can invite others to contribute to your child’s college fund.

Backer provides an easily shareable link you can send to anyone who might want to help contribute to your child’s college account. The link will take the family member right to your child’s contribution page, and it also shows them how that gift will grow over time. So instead of receiving gifts that will be quickly outgrown, your child can receive college funds. This is perfect for grandparents, aunts, uncles, and close friends who want to do more than just give your child another piece of molded plastic.

Cost of Backer

Backer is free. Yup, free. They run on a “pay what you can” model that allows you to choose how much you want to pay per month, between $0 and $10 per month.

If you’ve been putting off opening a 529 college savings plan, now is the time! Backer is here to help you and I can’t think of any reason not to get started today.

Hello, very useful and interesting publication. Sorry I just found your blog. Now I will appear here more often. And I was looking for information about the 529 plan, because my friend moved from Iowa to California and as it turned out – the conditions in these states are different. Pay attention, first of all, to the 529 plan of your State. This plan can (but not the fact) give you maximum benefits in the form of reducing the taxable base, low maintenance fees and good interest rates. Consult an investment advisor in a bank where you have a main account. They are usually happy to give you advice, subject to opening 529 accounts with them in the bank, but do not rush to do it. Take a pause. Googling for 529 plans for your state. Print the latest review and spend a couple of hours studying it.