Fundrise Review: Commercial Real Estate Investing for Everyone

Traditionally, there were only two ways to invest in commercial real estate. You could get started for a (relatively) low financial investment if you personally maintained the property. Or you could invest a major chunk of change into real estate development as a form of passive income. But neither of these options allowed the average Joe with a day job to invest a modest amount. Without time or serious money, real estate investing was closed to most of us. We love Fundrise because this real estate crowdfunding platform allows anyone to add commercial real estate to their portfolio for just $500. This allows average investors to get into real estate for a small investment without having to become a landlord. Read our review and decide if the Fundrise investment platform is right for you. Note: This is an endorsement in partnership with Fundrise. However, all opinions are my own.

How Fundrise Works

Like other crowdfunding investment platforms, Fundrise allows smaller investors to pool their assets together to take advantage of investments that could otherwise be out of reach. With Fundrise, average investors can enjoy the benefits of passive real estate investing with an investment as low as $500. Unlike other real estate crowdfunding platforms, Fundrise does not require you to be an accredited investor to take part. Accredited investors either earn more than $200,000 per year ($300,000 for married couples filing jointly) or have a net worth greater than $1 million individually, not counting the equity in a primary residence. Not requiring accredited investors opens up Fundrise to a much larger chunk of potential investors. Get started with Fundrise here. When you invest with Fundrise, the platform uses that money to build, acquire, and/or manage a variety of properties, including office buildings, apartment complexes, shopping malls, and industrial real estate. The platform earns its returns in two main ways: by collecting rental income and through the appreciation of the real estate assets. What this means for you is that your investment is illiquid. Your money will be tied up in your Fundrise investments for a period of time (typically five years). Do not invest any money that you cannot afford to lose access to for that period of time. Related: The Secrets to Investing Success and Building Wealth with Author Dr. Daniel Crosby

Fundrise’s Portfolios

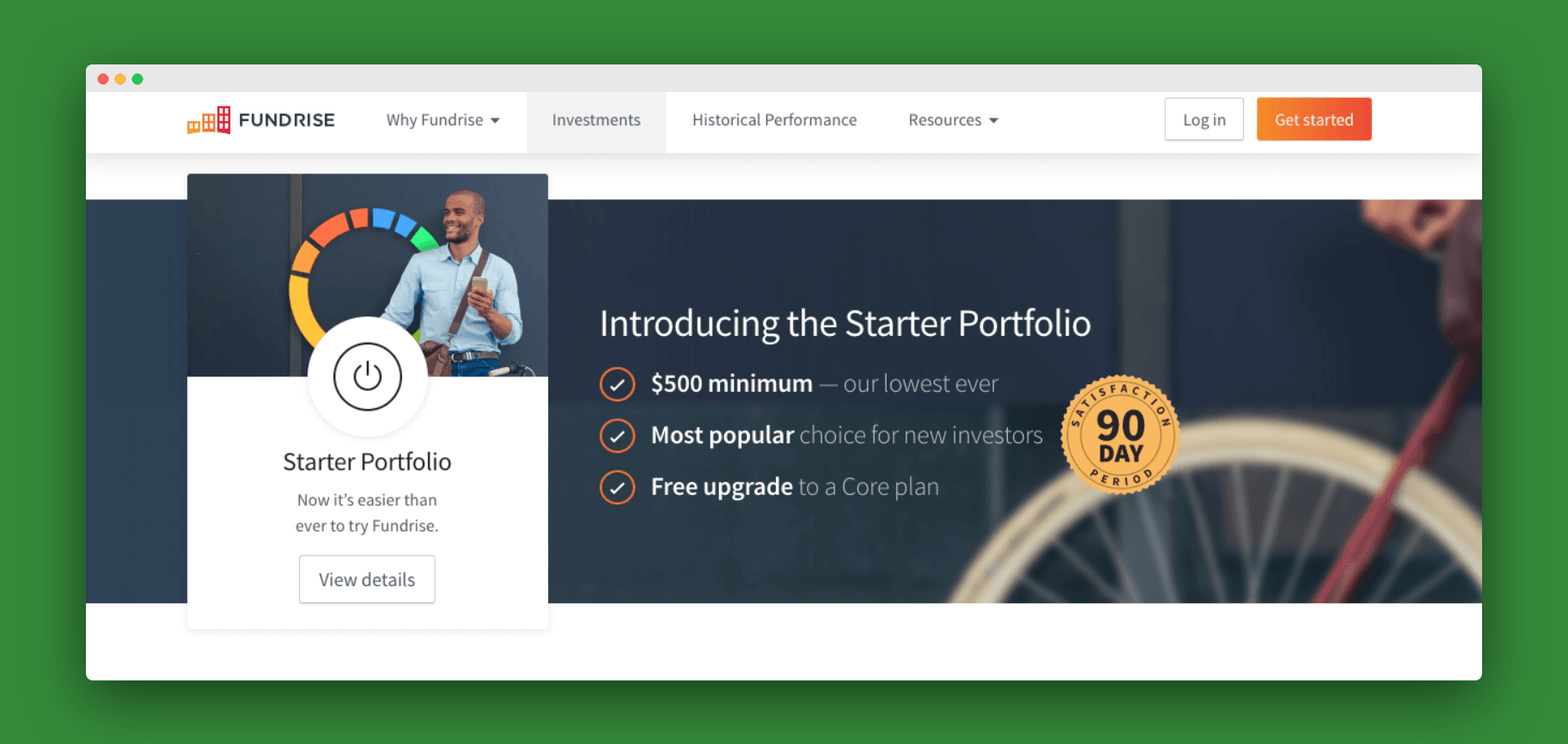

There are three different portfolio plans available to Fundrise investors. Each plan diversifies your investment differently, depending on your goals. Starter Portfolios ($500 minimum investment): These portfolios are for the investor just looking to get her feet wet. Your portfolio will have a diversified plan of five to ten real estate projects located throughout the United States. The big selling point for the Starter Portfolio is the 90-day satisfaction guarantee. If you’re unsatisfied with your investment at any time during your first 90 days, Fundrise will buy back your investment for the original amount you paid. Get started with just $500 here.

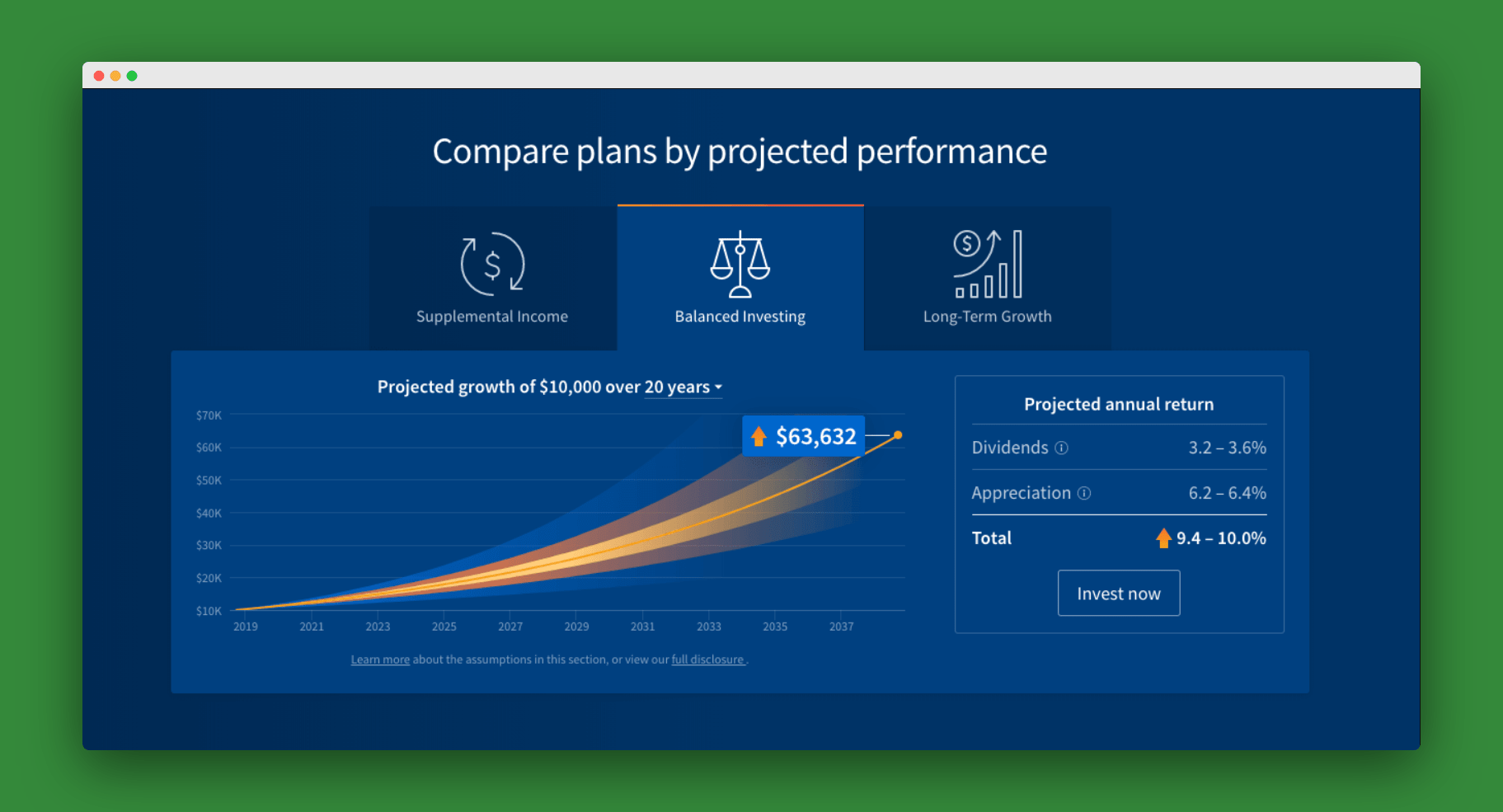

Core Plans ($1,000 minimum investment): These core plan portfolios offer more diversification, as your money will be invested in 40 or more real estate projects within the portfolio. Core plans come in three varieties: supplemental income, balanced investing, and long-term growth.

- The supplemental income plan focuses on investment properties that generate income through rent or interest. This is a great option for anyone looking for a source of consistent passive income. You can expect to receive quarterly dividends from your supplemental income core plan portfolio.

- The balanced investing plan offers you a mix of supplemental income and long-term growth. You can expect to receive quarterly dividends that are lower than what you will receive with the supplement income plan, but you can also expect to see the long-term appreciation of your initial investment.

- The long-term growth plan focuses on properties that are expected to appreciate in value, rather than on income-producing properties. While you may still receive some dividends with this plan, you are more likely to see higher returns over time through the long-term appreciation of the real estate portfolio.

Advanced Plans ($10,000 minimum investment): These plan portfolios offer the greatest diversification with 80+ projects represented in your portfolio. Advanced plan portfolios also employ more sophisticated investment strategies which can potentially increase your long-term returns.

Dividend Reinvestment Program (DRIP)

Another important aspect of Fundrise’s investment offerings is the ability to reinvest your dividends through DRIP (Dividend Reinvestment Program). When you earn quarterly dividends, you have the option of automatically reinvesting that money back into offerings on the Fundrise platform. Investors can choose which offerings they would like their DRIP reinvestments to go into. DRIP gives investors the opportunity to compound their earnings from the investment platform and increase their returns over time. Add real estate to your portfolio with Fundrise here.

How Crowdfunded Real Estate Investment Works

Whichever portfolio plan you choose, your money will be invested in eREITs and eFUNDs, both of which are proprietary offerings with Fundrise. To understand Fundrise’s eREIT offering, let’s start with the basic real estate investment trust (REIT). A REIT is an entity that allows shareholders to purchase shares in income-producing commercial real estate investments. Traditional REITs either public exchange traded, public non-traded, or private. Public exchange traded REITs are liquid but tend to have high fees and suffer from volatility. Public non-traded REITs are non-liquid but offer more stability and growth. However, they can also have high fees. Private REITs do not need to meet SEC requirements. This means you may see greater returns from private REITs because of the freedom from SEC requirements. However, you’ll need to do your own research and be sure you understand the investment totally because there is no oversight from the SEC. In many cases, REITs require a high minimum investment and offer either liquidity and volatility or illiquidity and stability. They can also sometimes come with some pretty hefty fees, and they don’t necessarily offer much capital appreciation since their structure requires 90% of income be paid back to investors. REITs can also be a somewhat complex investment for an individual investor. See also: 6 Ways to Invest in Real Estate

Fundrise’s eREITs and eFUNDs

Fundrise looked at these REIT options and decided there had to be a better way. They created the Fundrise eREIT and the Fundrise eFUND. Any portfolio you choose will include a mix of these two investment types. The eREIT is similar to a traditional public non-traded REIT, except that Fundrise has created a vehicle with a lower minimum investment, the potential for quarterly liquidity, and low fees. In addition to the eREIT, Fundrise offers eFUNDs, which are also exclusive to the platform. Fundrise uses electronic funds to buy land. The land is developed for residential real estate and sold to home buyers. The three eFunds that Fundrise offers focus on the demand for urban housing in Washington, DC, Los Angeles, and other major cities nationwise. Like the eREIT, eFUNDs also promise a low minimum investment, quarterly liquidity, and low fees. We’ve already covered the low minimum investment, and we’ll talk more about fees below, but let’s look at the quarterly liquidity right now.

Quarterly Liquidity

Being able to get your investment back in a hurry can be a major stumbling block for investors. You never know when the $25,000 you put in an illiquid investment might be the money you need to fight off the encroaching zombie apocalypse. This is one of the reasons why the SEC’s Regulation A+ rules which allow for individual investment in crowdfunded REITs will not allow individual investors to invest more than 10% of their net assets or gross annual income. Most average investors need to be able to access the majority of their money when the undead start to rise from their graves.

Fundrise wanted to solve the liquidity problem that you find with traditional REITs with their eREIT offerings. They built into their offerings the potential for quarterly liquidity, although potential is not the same as a guarantee.

What this means for investors is that you can request redemption of your shares on a quarterly basis, but depending on how long you have held the investment, you might owe a fee. Fundrise calculates your fee as a percentage discount of the share price value. Here’s the fee breakdown by time:

- Redeem within 90 days: 0% discount

- After 90 days and up to three years: 3% discount

- Between three years and four years: 2% discount

- Between four years and five years: 1% discount

- After five years: 0% discount

In short, don’t invest your Zombie Apocalypse money–or any other money you can’t live without for at least five years–into Fundrise. Their eREITs may be more liquid than public non-traded REITs, but they are still an illiquid investment.

Fees

It can be a little tough to determine exactly what you will be paying in fees with Fundrise, although they do promise lower fees than traditional REITs. With no broker-dealer handling your account, you do not need to worry about the middleman fees that often take a bite out of investments. They make it very clear that you will pay an 0.85% annual asset management fee, as well as a 0.15% annual investment advisory fee, for a total 1.00% annual fee. You can also easily find the fees you will pay for early redemption of your shares should you need to liquidate before you have held your investment for five years. However, there can also be miscellaneous additional fees that can be a little harder to track down. Fundrise is not alone in being a little less than transparent about these fees. FINRA, the regulatory body for the financial industry, has issued a warning to investors about the importance of checking the fees on public non-traded REITs. The offering circular for each eREIT and eFUND you invest in will enumerate these additional fees, although you may have uncover the information buried deep in the circulars. It’s up to you to carefully check through the circulars to make sure you understand exactly what you might be paying when you invest. As with any investment online, take the promises on the flashy front page of the website with a grain of salt and make sure you do your due diligence in reading the fine print and the offering circulars. See Also: Protect Your Investment Earnings from Being Undermined

Can You Make Money with Fundrise?

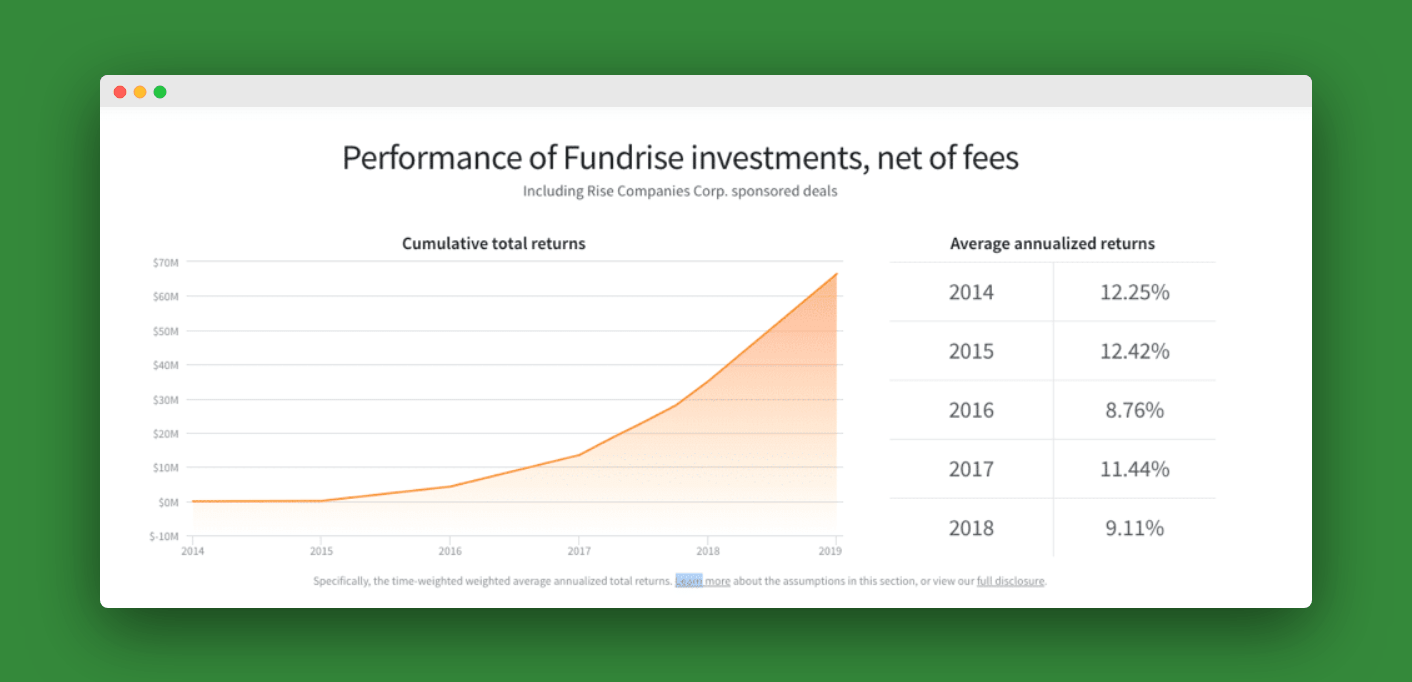

As with any investment, the big hairy question is whether you can expect decent returns. The short answer, according to Fundrise’s historical return data is yes:

Now before you start seeing dollar signs in your eyes, remember that past performance is no guarantee of future returns. That’s true of every investment, not just Fundrise, but it’s important enough to repeat (or even embroider on a pillow.) In addition to that universal truth of historical returns, you need to contextualize Fundrise’s information. With that context, you’ll have a better sense of what you can reasonably expect by investing with them. Fundrise calculates the average annualized return of 9.11% in 2018 net of fees. That means this is the return investors experienced after their fees were paid. This calculation also assumes that investors reinvested their dividends rather than cashing them out. Taking your quarterly dividends as cash will reduce your return. Finally, these calculated returns are based on returns incurred rather than returns paid. Since not all returns are paid, Fundrise calculates average annualized returns using weighted averages. This means some of their products are weighted higher than others in making these calculations. In other words, your mileage may vary. That said, Fundrise’s historical returns have been solid, and investors seem satisfied with their performance.

Should You Invest with Fundrise?

Fundrise has certainly opened the doors to real estate investing for many, but it’s not a one-size-fits-all solution. Before you jump in, it’s smart to consider if this platform truly aligns with your financial goals and personal situation. Here’s a look at who Fundrise typically suits best:

- Meets basic eligibility requirements. You’ll need to be over 18, have permanent US residency, a valid US tax ID, and file taxes in the US to invest on the platform. (Source)

- Doesn’t need to be an accredited investor. Fundrise is a fantastic option for non-accredited investors looking to get into private real estate, private equity, and private credit without the high barriers to entry. (Source)

- Has a long-term investment horizon. You should feel comfortable letting your money grow for at least five years. While early redemptions are possible, they often come with fees, so patience is a virtue here.

- Prefers a hands-off approach to real estate. If you’re keen on real estate exposure but don’t want the hassle of property management, tenant issues, or finding deals yourself, Fundrise takes care of all the heavy lifting.

- Seeks to diversify their investment portfolio. Fundrise offers a way to add private real estate assets that often behave differently than traditional stocks and bonds, potentially smoothing out your overall portfolio’s ride.

- Is comfortable with some illiquidity. Unlike publicly traded stocks, your money in Fundrise isn’t instantly accessible. Real estate investments take time to mature and liquidate, so be prepared for that.

- Is willing to dig into the details on fees and account levels. While Fundrise aims for transparency, understanding the specific fees for each eREIT or eFund, and how different account tiers (like Basic, Core, Advanced) affect your options, requires a bit of reading. (Source)

If these characteristics don’t quite match your investment style or financial situation, it’s perfectly fine. Fundrise might not be the perfect fit, and exploring other investment avenues could be a better path for you. It’s all about finding what works for your unique circumstances.

On the flip side, if you’re someone who needs immediate access to your funds, prefers direct control over individual properties, or is looking for quick, speculative gains, Fundrise probably isn’t your best bet. Its long-term, diversified strategy is built for patient investors, not day traders.

Fundrise Pros and Cons at a Glance

Every investment platform comes with its own set of advantages and drawbacks. Fundrise is no different. To help you weigh your options, here’s a quick rundown of what makes Fundrise shine and where it might fall short.

The Good Stuff: Fundrise Pros

- Accessibility for non-accredited investors: This is a huge plus, opening private real estate to a broader audience who might otherwise be locked out. (Source)

- Low minimum investment: You can start with a relatively small amount, making it approachable for many budgets.

- Diversification potential: Offers exposure to various private real estate, private equity, and private credit assets, which can help balance a portfolio and potentially reduce overall risk. (Source)

- Passive income potential: Investments can generate quarterly dividends, offering a steady income stream without active management.

- Hands-off management: Fundrise handles all property acquisition, management, and disposition, freeing up your time and effort.

- Potential for long-term appreciation: Aims for growth over time, similar to traditional real estate investments.

- Opportunity Zone investments: Offers specialized funds like the Fundrise Opportunity Fund for potential tax benefits in designated areas. (Source)

Things to Consider: Fundrise Cons

- Illiquidity: Your money is tied up for the long haul. Real estate isn’t a liquid asset, and early withdrawals can be costly or restricted.

- Fees require careful review: While Fundrise aims for transparency, you’ll need to dig into offering circulars to understand all the costs associated with specific eREITs and eFunds.

- Performance isn’t guaranteed: Like any investment, there’s no promise of returns, and real estate values can fluctuate with market conditions.

- Less control: You don’t get to pick individual properties or have a direct say in management decisions.

- Withdrawal limitations: Even with early redemption options, there might be waiting periods or penalties, so don’t count on instant access to your cash.

- Not ideal for short-term goals: If you need your money in a year or two, Fundrise is likely too slow-moving for your needs.

| Pros | Cons |

|---|---|

| Low minimum investment | Not a fully liquid investment |

| Offers real estate diversification | Real estate based investments could react to volatility in the real estate market |

| Low asset management and advisory fees | Fees within the individual eREITs and eFUNDs are not entirely clear |

| 90-day guarantee to get your money back | |

| Quarterly liquidity | |

| Dividend Reinvestment Program (DRIP | |

| Historical returns are good |

The Bottom Line

With a minimum investment of just $500 and the ability to reinvest your dividends, Fundrise gives average investors the platform they need to get started in real estate. Add in the 90-day satisfaction guarantee, and there is a lot to like about testing the real estate investment waters with Fundrise. Just be ready to leave your fund untouched for five years, or pay a fee to access them. With Fundrise, you don’t need to be an accredited investor or a committed DIY landlord to reap the benefits of real estate investing. You just need to be a savvy investor who is willing to do your research and make smart choices. Start investing in real estate with Fundrise here. Have you invested with Fundrise? Tell us about your experience in the comments?