Is 4% Savings in a Gamified Banking App For Real? It’s Not. [Beam (beta) Review]

Update: Accoridng to a CNBC investigation, Beam appears to be having trouble returning money to customers. I got out in June 2018. Skip Beam and try one of these FDIC insured online savings accounts instead.

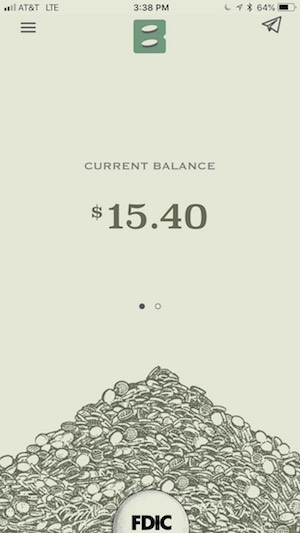

Iused Beam from April 25th, 2018 to roughly mid-June, 2018 and I can report that yes, as part of the beta test they did pay a nice baseline 2% APY on up to $15,000. That’s a top-tier rate as of June 2018, even if you compare it to other high-interest online accounts.

Iused Beam from April 25th, 2018 to roughly mid-June, 2018 and I can report that yes, as part of the beta test they did pay a nice baseline 2% APY on up to $15,000. That’s a top-tier rate as of June 2018, even if you compare it to other high-interest online accounts.

At the time, I felt comfortable with my money there, despite concerns from other online reviewers. I spoke with the Beam team and I believe they’re on an earnest mission to help people save more while pushing banking forward. I no longer feel comfortable with Beam.

Did I earn 4%? Yes, but only the first day when I had 3 “Billies” (explained below).

Over one month, the most I ever made with Beam from simply using the app’s daily Billie was 2.99% (for the day). To make 4% it seems I would have needed to be doing multiple customer referrals regularly.

Confused? Let cover some basics and then I’ll come back to the details…

What Is a Beam Bank Account?

Beam offers customers a demand deposit account with a 2% base APY and no associated fees.

Beam offers customers a demand deposit account with a 2% base APY and no associated fees.

While a standard bank account may have limits on the number of withdrawals you can make per month and offer a minimal interest rate, with Beam’s demand deposit account, you can transfer funds to and from your account at any time—and you’ll earn far more in interest than any standard bank will offer.

Currently, Beam caps account balances at $15,000. This limit may increase to $50,000 in the future.

What Are the Requirements?

Beam is still conducting its private beta testing and is taking names for their public beta program (which I am taking part in), so interested customers must apply to be put on the waitlist. However, you can improve your standing on the waitlist by referring friends and family.

To apply, you must be a U.S. citizen, be 18 years of age, have an existing bank account at a designated financial institution, agree to terms of service, and fill out the Beam application located on the app. In order to keep up with compliance, Beam may ask for a photo ID, additional information, or documentation from time to time. I did all of this and was really happy with the on-boarding experience.

Beam’s Features

With many financial institutions flooding the market with banking apps, Beam needed to set itself apart. Beam has two features that allow the app to stand out from the rest: 24-hour fund transfers and a 2% base APY.

Fund Transfers

In order to establish your Beam account, you must link it to an external bank account. I linked mine to my Capital One 360 account.

Beam then sets up access to your third-party account. You need to verify all information is accurate before proceeding since Beam does not double check account information. This then allows you to move funds in and out of your account at any time.

It takes about 24 hours for your funds to appear in your account. This is much faster than most online bank transfers.

However, you do need to keep in mind that Beam is not responsible for any additional fees that occur from transactions in the account. Beam does not charge any fees, but your financial institution may have rules and regulations for moving your money out of the account.

Earn 2% Guaranteed APY (and Increase It to 4%?)

Most big box banks offer a 0.01% interest rate on savings accounts. The bank then turns around and receives 4%-5% interest on the money they lend to borrowers, which means the bank is making money off of your hard-earned cash. As if that weren’t frustrating enough, with annual inflation at 2%, you are losing money by keeping it locked up in a savings account. “Earning” 0.01% interest means you are slowly losing your buying power.

Most big box banks offer a 0.01% interest rate on savings accounts. The bank then turns around and receives 4%-5% interest on the money they lend to borrowers, which means the bank is making money off of your hard-earned cash. As if that weren’t frustrating enough, with annual inflation at 2%, you are losing money by keeping it locked up in a savings account. “Earning” 0.01% interest means you are slowly losing your buying power.

You guys know this, though. And it’s why you use online savings accounts to up your savings rates. But those are still only in the 1.5% to 1.85% range (as of June 2018).

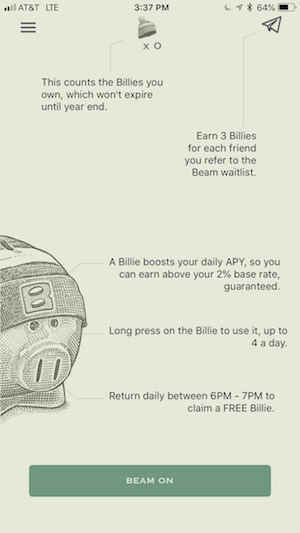

While the guaranteed base APY is 2% (awesome), Beam users can increase their APY to upwards of 4% (although I never experienced more than 2.99%) by interacting with the app. Users can accept free rewards (“Billies” in Beam lingo) on the app, which will increase the account’s APY for just one day. Billies arrive daily between 6PM and 7PM local time, and claiming them is free, easy, and free of strings. But the next day, your rate goes back to 2%. I found this disappointing. Beam, in my view, over-promised.

How can Beam afford these better rates? They say it’s partially because the bank has no brick-and-mortar location. Like online banks, this results in lower overhead and more money available for customers. But according to Beam, they also believe in sharing more banking profits with their customers, which means they are able to offer better returns than even most online banks.

Pros and Cons of Using a Beam Account

Pro: High APY

No doubt about it, the APY is the biggest benefit of a Beam account. No one else is even coming close. Although, in terms of true comparison, you’re only talking about ~2.5% vs the 1.85% you can currently get from CIT Bank (without the upper limit or gamification piece).

Pro: Accessibility

The Beam app is simple to access. You don’t have to jump through hoops to open an account and Beam makes it easy to transfer funds from your external account. The process is user-friendly and the interface is super clean and fun.

Pro/Con: Gamification & Referrals

Every day you have to go to the app to increase your APY by using Beam’s Billie rewards. You can also boost your APY by referring customers to the app. Gamification can make earning money more fun for some. But for me, this is just disappointing. Time is more valuable to me than money (as it is for most humans instinctively, IMO). And Beam is ignoring that.

I’m not one for using personal referrals to increase my interest rates. Don’t get me wrong, I monetize this blog through referral marketing partnered with inbound education. But I’m not hitting up my friends, family, and close contacts for referrals. No one wants to be that person.

Con: Potential Third-Party Fees

Beam promotes its unlimited fund transfer feature, which is certainly a helpful aspect of the account. However, you need to remember that Beam is not responsible for third party fees, which they highlight in their terms of service.

If your current bank account charges you for ACH transfers in and out of your account, you may want to be cautious. For what it’s worth, I didn’t experience any fees transferring between Beam and Captial One 360.

Before you proceed with establishing a Beam account, make sure you understand your bank’s structure for transaction fees.

Why Choose Beam?

Don’t choose Beam. Skip it and go with an FDIC Insured online savings account.

If you want a 2% interest rate on up to $15,000 of your savings with a bare-bones bank vs having ~1.5% from your potentially more-robust online savings account then by all means, get in line to start an account with Beam. And if you enjoy going to your banking app daily to press a piggy bank button then you’ll really love the increased 0.10-0.99% interest rate you’ll earn.

I opened my Beam account in July. I asked for a 500.00 withdrawal in August, 2 weeks later I requested to close my account, still in August. i have not received a dime. Todays date is 10/15/2020. PLEASE BE CAUTIOUS. MONEY IN, NO MONEY OUT.

I opened a Beam account in July. In August I decided to try one of their easy withdrawals. No money was ever transfered back to me. So I decided to close my account. On August 28, 2020 I requested to close my account. To date October 15, 2020 I have no money.Please be careful before you fall into this trap. I was told the money is insured, what shoud I do next?

Beam is fraud company , dont fall into there trap.once they got money u r screed..it taking more then 3 weeks or months.. to get money when u request withdraw money back…you hear all story from them , the other banks not giving money to them so they cant give you….stay away..dont fall into there trap.

Yeah, the author should either remove this post or clarify at the very top that Beam is fraudulent. I can’t get my money out. It’s really scary. Should we be organizing some kind of suit? How do we find out who their investors are?

Hi JC,

I too requested a withdrawal 2 weeks back and it is in pending status for some time now. I tried reaching out to them with no response. Did you get your money withdrawn?

I joined the waiting list on 4/7/18. I JUST got the go ahead to open an account on 2/5/19, with a limit of $400 total transfer to the account. At first I was getting notifications on my phone to get my free Billie between 6-9pm but that did not happen on the weekend and I forgot to get my Billie. Even on the following Monday I did not get the notification so now I set an alarm on my phone daily to remember to get my free Billie. I have to look into whether it makes more sense to use one Billie per day or to accumulate them and jump to 4% for the day. I assume it doesn’t affect your average APY over the course of a year but the earlier I use them the more interest I accumulate earlier, and assuming interest is compounding on this account so I might as well up my balance sooner than later.

Good post related to beam – review and it is more helpful. thank you so much.

Thank you very much

I’m not gonna lie, high interest rates like this certainly set off my BITCONNEEEECCCCT red flags…

I’ll watch it for a few months and see what happens. I know it says FDIC-insured but I’m still skeptical. If something is too good to be true it usually is…

lol

Hi PT. I got on the BEAM waitlist earlier this year and I am using the BETA test version. Today, my rate is over 4%. I think I pressed too hard on the pig …. or something…. I am still not exactly sure of the process with how the rate increases at the various levels. It seems sort of random. Anyhow, I have promoted BEAM on my facebook page and today, five people signed up. This moved me up the list to number 362 for the fully operational version of BEAM and it gave me 15 Billies…. Which I plan to try to spread out over the coming days to have a better rate day after day. Yes, going on at 6pm to collect a Billie is an easy thing to do, but it is also easy to forget to do.

I also have accounts with ALLY, SYNCHRONY, CIT, and GOLDMAN SACHS. I wanted to try out all of these online banks and I am happy with the APYs on all of them that are sigfinicantly higher than my brick and mortar account with CHASE.

Very cool, Thomas. Nice summary of the beta on boarding and billies. At the end of the day I think this will be a nice addition to the list of other options out there and attract more people to the idea of doing more with their money.