The Last Day to File Taxes (and What to Do If You Can’t Pay)

Update: It’s confirmed. Taxpayers will have (according to the IRS website) until April 15, 2026, to pay and file their personal 2025 taxes. That’s the last day to file your taxes in 2026.

Head’s up…many post offices stay open later on tax day to ensure you get your return filed.

Table of Contents

New for 2026: One Big Beautiful Bill Act Tax Changes

The 2026 tax season brings significant changes from the One Big Beautiful Bill Act (OBBBA), passed in July 2025. Key provisions that may affect your 2025 tax return (filed in 2026) include:

- No tax on tips: Qualifying tip income may be deductible (income limits apply)

- No tax on overtime: Qualifying overtime income may be deductible (income limits apply)

- Car loan interest deduction: Interest paid on qualified passenger vehicle loans may be deductible

- $6,000 seniors deduction: If you’re 65 or older, you may qualify for an additional deduction up to $6,000 (single) or $12,000 (married filing jointly), subject to income phase-outs

- Increased Child Tax Credit: Expanded credit amounts for families with children

- Higher SALT deduction cap: State and local tax deduction cap increased from $10,000 to $40,000 for 2025-2029 (with phase-outs for high earners)

Use the new Schedule 1-A to claim these deductions. Many taxpayers can expect larger refunds this year due to these changes.

More Deadlines: Last Day to File Taxes in 2026

- January 26, 2026 – IRS officially opened e-filing for the 2026 tax season.

- January 31, 2026 – This is the date by which you should have received a W-2 from the employers you worked for during the tax year. If not, contact their HR/Payroll department to resend tax documents.

- March 16, 2026 – Last day for partnerships and S corporations to file their taxes using Forms 1065 and 1120S (March 15 falls on a Sunday). They can also file an extension using Form 7004.

- April 15, 2026 – Last day to file taxes as an individual. Extension Form 4868 should be filed if you can’t complete your return on this date. Payment needs to be made, though. This date falls on a Wednesday in 2026.

- May 15, 2026 – Last day for non-profits with a calendar year to file their Form 990.

- September 15, 2026 – Last day for corporations to file extended returns.

- October 15, 2026 – Last day for individuals to file extended returns.

Quick Filing Tips

Here are some things you can do to ensure you file on time by the deadline.

- Add the tax deadline to your calendar right now! Paper calendar, digital calendar, etc. Set up the deadline or a reminder so you don’t forget.

- Grab a checklist to ensure you know what forms to start looking for in the mail and in your inbox. Check the items off as they come in. That leads to my next point…

- Start a file folder (digital and/or physical) for keeping all of your forms in one place. Once you’re ready to file, you’ll know exactly where to find everything.

- Review the new Schedule 1-A to see if you qualify for any of the new deductions from the One Big Beautiful Bill Act.

Tax Penalty if You Don’t File by the Deadline

You will be penalized 5% (of the additional taxes you owe beyond what you paid in) each month you haven’t filed. This penalty maxes out at 25% of the additional tax you owe.

So if you owe $100 in additional taxes after April 15th, you’d owe $105 ($100 plus the 5% penalty).

Wait to file more than 60 days after the tax deadline, and you’ll face a minimum penalty of $435 or 100% of your tax, whichever is the smallest.

Important note. Always file even if you cannot pay. The penalties for not filing listed above are much steeper than those for not paying. The failure to pay the penalty is only 0.5% for each month you don’t pay, capped out at 25%.

If you can’t file a complete return, file an extension.

Related: Where to Get Your Taxes Done (The 3 Best Places and Prices)

What If You Can’t Pay Your Taxes This Year?

Does your heart sink when you receive a piece of mail from the IRS?

That’s reason enough to dread tax season. I have a friend whose family always filed extensions on their taxes. This, of course, added to the stress of tax season. After April 15th no one in her family would go to the mailbox.

My friend decided at age 18 she was fed up and wanted to start filing her taxes. With some help, she prepared as soon as she received her tax documents. She never stressed again because she had plenty of time to adjust.

If you’re asking, “What if I can’t pay the taxes I owe by this year’s filing deadline?” I can help! Here are a few guidelines for avoiding and reducing IRS interest, filing penalties, and underpayment penalties.

- If you can’t pay your taxes, file your tax return and pay as much as possible by the tax filing deadline.

- Then, set up a payment plan with the IRS. You’ll still have to pay interest and penalties, but this will significantly reduce the total amount you’ll owe.

- Then make adjustments to your W-4 or quarterly tax payments so you can avoid owing taxes in the future.

File Your Tax Return (Most Important!)

Unless you made less than the minimum IRS requirement, you’d need to file a tax return. Check out this article to find out the minimum income needed to file taxes.

If you can’t pay all or part of the taxes you owe, you’ll still want to file your tax return by the deadline.

Otherwise, you’ll be charged a penalty of 5% of the taxes you owe for each month (or partial month) after the tax filing deadline until you do. This includes a 4.5% failure to file penalty and a 0.5% late payment penalty.

If you go five months without filing, the failure to file a penalty will max out. However, if you haven’t paid by then, the 0.5% late payment penalty will continue accumulating until it reaches 25%.

At that point, your total penalty will be maxed out at 47.5% (25% late payment penalty and 22.5% failure to file penalty.)

If you file more than 60 days past the tax filing deadline, you’ll owe a minimum penalty of the lesser of $435 or 100% of the amount you owe.

You don’t want to end up in that situation, so plan! Check out our Tax Preparation Checklist for help getting started.

Note that you can always file for an extension, but an extension of time to file doesn’t give you an extension of time to pay. You’ll start accruing interest and penalties immediately after the April 15th tax filing deadline if you owe taxes.

You can avoid the interest as long as you pay 90% of the taxes you owe by April 15th. Here’s what the IRS has to say about this.

Pay What You Can Without Compromising Basic Necessities

If you cannot pay the total amount of the taxes you owe by the tax filing deadline, the IRS will charge you interest on the outstanding balance. The interest rate is subject to change each quarter and is calculated by adding three percentage points to the federal short-term interest rate.

Paying as much as you can by the deadline is your best strategy. The more you pay toward your balance before it’s late, the less you’ll have to pay in accrued interest and penalties.

Here’s some more info from the IRS about penalties and interest.

Set Up a Payment Plan

As soon as you realize that you’re not going to be able to pay your taxes in full, you’ll want to reach out to the IRS to set up a repayment plan. Note that you cannot qualify for any repayment plan until you have filed all the required tax returns.

Once you’ve completed this step, you can choose a short-term repayment plan or establish an installment agreement.

Here’s how to apply online for a payment plan with the IRS.

Short-Term Repayment Plan

If you believe you’ll be able to pay your balance in full within 120 days and you owe less than $100,000 in total (including taxes, interest, and penalties), then your best bet is to file for a short-term payment plan. This won’t cost you anything other than the fees and interest previously mentioned.

With this arrangement, you can pay the amount you owe by check, pay online using the IRS Direct Pay system, or pay by debit or credit card.

IRS Direct Pay

Direct Pay pulls the funds directly from your checking or savings account.

You’ll receive an immediate confirmation when your payment is processed, and you can schedule your payments up to 30 days in advance. You can also cancel or change your payment up to two business days before the scheduled processing date.

Credit or Debit Card Payments

If you prefer, you can also make payments using your credit or debit card. The IRS allows you to process these payments online, over the phone, or even using your mobile device. While the IRS doesn’t charge a fee for this option, credit card processors do.

Take a look at this page on the IRS website to learn more.

IRS Installment Agreement (Long-Term Payment Plan)

If you need more than 120 days to pay your balance and you owe less than $50,000 in combined taxes, interest, and penalties, you may qualify for a long-term payment plan, also known as an installment agreement.

This will allow you to make monthly payments on the amount you owe. It will also decrease your failure to pay the penalty from 0.5% per month to 0.25%.

If you owe more than $25,000 combined, you’ll have to pay by Direct Debit and have the funds automatically withdrawn from your checking or savings account each month. This is known as a Direct Debit Installment Agreement (DDIA). There’s a $31 set-up fee and you’ll still owe penalties and interest.

There’s also an option to pay using non-automated payments via Direct Pay, credit cards, check, or money order. This is only available to those who owe less than $25,000 and will cost you $149 to set up, plus your interest and penalties.

Fill out IRS form 9465 or use the Online Payment Agreement Application if you owe less than $50,000. (You’ll find links to both here.)

If you have $50,000 or more in tax debt, you will need to include Form 433-A (Collection Information Statement or CIS) along with your Form 9465. If you owe more than $50,000, it’s recommended that you work with a tax professional, as the CIS can be challenging.

Another option is to file an 843 Claim for Refund and Request for Abatement form. There are no direct standards for whether the IRS will accept or deny this request, but it’s worth trying.

You never know where negotiating will take you, and it may eliminate some of the financial burdens. You can find this form and the instructions on this IRS webpage.

Related: (Don’t Risk it!) Get a Quality CPA to Prepare Your Taxes

How to Avoid Owing the IRS

While owing taxes to the IRS isn’t necessarily the end of the world, we can all agree that it’s a situation you’re better off avoiding. Luckily, there are some steps you can take to make sure you don’t find yourself in this undesirable position in the future.

Two of the best options are adjusting your W-4 and paying quarterly estimated taxes.

How to Adjust Your W-4

One of the most common reasons why people owe the IRS money is that they didn’t have enough withheld from their paycheck.

Even if your withholding was once correct, major life changes like a marriage or divorce may throw this off. If you’ve started a side business, this will also impact the amount of taxes you owe. Whatever the reason, you can fix your withholding by completing a new Form W-4.

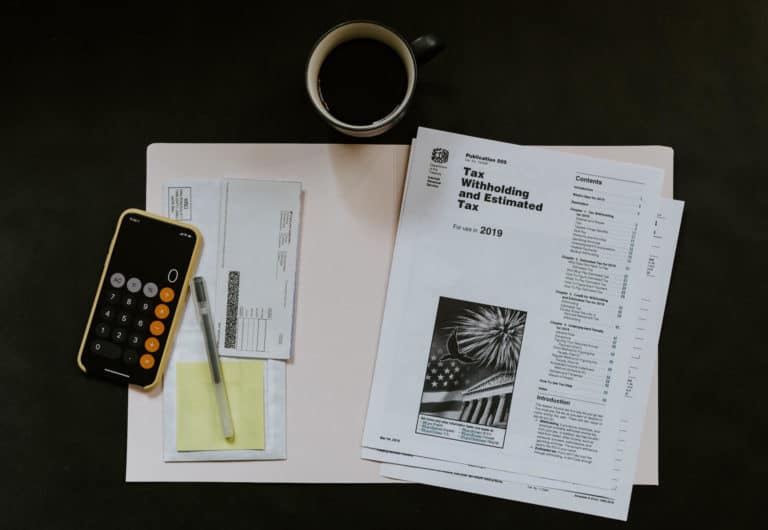

Before you do this, I suggest using the IRS Tax Withholding Estimator. Then, once you’ve determined the appropriate withholding amount, complete the Form W-4 Employee’s Withholding Certificate and provide it to your employer. (You can get a W-4 from your employer or download it from the IRS here.)

How and When to Pay Quarterly Taxes

If you have a significant amount of income coming in from your side business, then there’s a good chance you’ll owe extra taxes. While it would be easier to calculate it at the end of the year and make one lump-sum payment, income taxes are a pay-as-you-go system.

For this reason, you’ll need to estimate the taxes you owe each quarter and send a payment off to the IRS.

Related: Am I Required to Make Estimated Tax Payments on Extra Income

The schedule for making estimated tax payments is as follows:

- Taxes owed on income earned between January 1 to March 31 is due on April 15th

- Taxes owed on income earned between April 1 to May 31 is due on June 15

- Taxes owed on income earned between June 1 to August 31 is due on September 15

- Taxes owed on income earned between September 1 to December 31 is due on January 15 of the following year

Note that if any payment days fall on a legal holiday or a weekend, the payments are due on the next business day.

You should submit Form 1040-ES along with your payment, or, even better, pay online at EFTPS.gov or pay with your mobile device using the IRS2GO app, which you can download here.

Don’t Miss the Last Day to File Taxes in 2026 and Other Deadlines

So that’s the who, when, and where of tax deadlines this year. Now you know the last day to file taxes. Are you planning on filing as soon as possible or waiting until the 15th of April?

If you’ve found yourself in a situation where you owe the IRS and don’t have the money to pay it all at once, don’t panic. Make sure to file your return on time to avoid the 5% per month failure to file penalty.

Pay as much as you can afford by the tax deadline to reduce the amount you’ll pay in penalties and fees, and set up a short-term or long-term payment plan to further reduce your failure to pay penalties.

Finally, consider adjusting your W-4 withholding amounts and/or making estimated tax payments to ensure you aren’t in the same situation again.

And don’t forget to check if you qualify for any of the new deductions from the One Big Beautiful Bill Act – they could significantly reduce your tax bill or increase your refund!

A couple of years ago, I decided to use TurboTax over my certificated accountant. One of the reasons is I am always on a business trip and can’t really meet her up. But the biggest reason is that those tax software are very helpful nowadays. If you don’t know much about the entire process, TurboTax gives you step by step instruction to show you how to get it done. I am very familiar with it already so I always choose the items to work on directly. More than like, it gives you a comparison chart so you can compare it with last year’s figures side by side. The feelings you can get it done on your own is simply awesome. Just in case you get audited in the future and need some advice, make sure you purchase additional service “MAX Assist & Defend” from TurboTax. Hope I won’t need it but at least it gives me a peace of mind.

I use TurboTax, plan to file my taxes before the end of this month. Had to wait for Schedule K to show up – it is pain to own a master limited partnership (MLP). I made decent money, however, it was a pain to enter all the information in. For this one reason, I have decided to never buy an MLP again.

Luckily my father is a tax attorney so I just hand over the receipts and spreadsheets where I track my expenses each year and he deals with the rest.

Happy May Day 2012 http://fsquarefashion.com/happy-may-day-2012-quotes-text-wishes-sms-messages-sayings/

Just fyi — the april deadline in this article still has “2011” instead of “2012” (the actual year in which is the present). 😉

@SamanthaIsSooSavory Good catch. Missed that one when I was updating. Thank you very much.

What do I do if I didn’t receive a 1099-R untli March 1 – it was postmarked February 27. Can I report them? (By the way, I just filed my taxes yesterday, February 29).

Did you include the income (on your 1099-R) on your return? You can report them. Would be at least a $60 fine for them.

If i owe taxes from 09′ and 10′ can they be duducted when i file taxes this year?

@NELLE To my knowledge, you cannot deduct federal income taxes. You can deduct State taxes and self employment taxes though.

You can deduct State and local income taxes in the year that you pay them, rather than when you file.

No. The IRS doesn’t email.

I got an email saying that I have to pay penalties for not filing before January 31st. Is this legit?

I got an email saying that I have to pay penalties for not filing before January 31st. Is this legit?

Who do you contact if my w-2 was not mail out by my bank by Jan 31

@Heath1bare You should contact the HR department of the company.

@Heath1bare Banks issue forms 1099 for interest earned or form1098

for mortgage interest paid rather than W-2 forms issued by employers. If your interest earned is less than $10 per year, there would be no 1099 issued.

w/taxes due on the 18th maybe emancipation day shouldn’t be celebrated until the 19th this year…

Thanks for this unfortunate reminder.