Greenlight Review | The App I Used to Teach My Kids About Money

Update: I used Greenlight for over four years with my kids. I loved it. However, this past year they started promoting things on their platform that, in my opinion, aren’t for kids. We’ve moved on to FamZoo.

Did you ever wonder why personal finance was not taught in your K-12 years of school? I certainly did! Not once in my early education was I offered the opportunity to learn about personal finances. It was up to my parents to teach me.

Parents are the ones ultimately responsible for providing every aspect of a financial education–from giving children an allowance to helping them start their own business.

Unfortunately, not all parents are equipped to help their kids learn about creating strong financial habits.

If you didn’t have parents who explicitly taught you how to manage money, you might feel overwhelmed at the idea of teaching your kids.

This is where Greenlight can help.

The Greenlight debit card and app – which I used for 4 years – can be a great conduit for you to teach your children financial literacy. It will also help keep the peace for just $4.99/mo.

Let me explain in my review of Greenlight.

Table of Contents

What Is Greenlight?

Greenlight was built by parents for parents.

Tim Sheehan, CEO, and co-founder of Greenlight was constantly frustrated because he wanted to give his kids a consistent allowance to help them learn how to handle the responsibility of money, but he never had the cash to give his kids.

Tim suspected many other parents may have the same problem. He wanted to find a way to teach his children about financial responsibility while making it simple to give them money.

The solution? Greenlight.

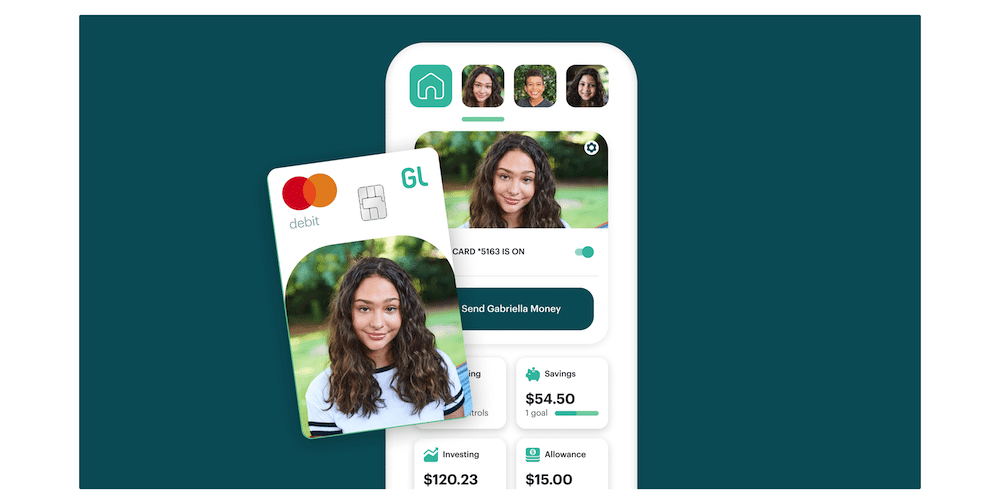

Greenlight is a parent-controlled, real-life, version of a bank account for your children. When you sign up for the program, your child receives a PIN-enabled debit card, which can be used to make purchases but cannot be used at ATMs or for cashback.

The big benefit of this card is that the parent can decide which stores or type of stores, and the amount of money in the account, get the “greenlight”–that is, you as the parent decide how much and where your child may spend their money.

Banking services for Greenlight are provided by Community Fedral Savings Bank. Funds are FDIC insured. It’s legit.

How Greenlight Works

From your Greenlight Parent’s Dashboard, you will add money to your account.

Once you have completed this, you will be able to send your children money, which they may automatically apply to their Greenlight debit card spending, saving, investing, and giving buckets.

Once you have sent funds to your child’s account (in the initial setup), Greenlight will prompt you to designate an interest rate for the savings bucket. I set mine at 2.5%.

This interest rate will be automatically deducted from your Greenlight Wallet every month. This will help your child learn the awesome power of compound interest.

Since you will be paying all of the interest, you want to make sure it is an amount you and your family feel comfortable with.

You can move money from your Dashboard into your child’s account anytime you would like. Your children can also move funds.

However, such a child-initiated transfer must be approved by you in order for the transaction to be completed. They will not be allowed to do anything without your approval.

Related: Teaching Kids About Money [The Complete Guide]

Greenlight Benefits for Your Kids (and You)!

This debit card and app come with a lot of features and benefits. Let’s dig into the specifics.

No More “Mom/Dad, can I get this?!?!”

Hands down the best thing about Greenlight is that it virtually eliminates the in-store fits/arguments about money.

When you give your kids their own card and weekly funds, they get to decide what to buy. If there’s no money on the card because they already spent it, “oh well.”

Letting your kid make the “should-I-buy-it-now-and-blow-all-my-money?” decision now is the best thing you can do for them.

My kids no longer ask for things in stores. If they did, I’d just say, “you’ve got your own money.”

Visual Learning Tool

Traditional bank accounts have such a small amount of interest that kids have trouble seeing how the money grows over time.

With Greenlight they can see the growth in a more timely manner. This could encourage them to want to put more money in savings and be more responsible with the funds given to them.

Some children are visual learners and this is a great way to capitalize on that.

Instant Notifications

You will receive instant notifications letting you know what your children are trying to spend their money on. Greenlight will also let you know if any purchase was declined and if you need to add additional funds to the account.

Transactions are flexible and happen quickly. Let’s say your child is at a store and they are requesting to buy an item. You then receive a notification and can instantly send them money to cover the cost–or you can deny the request if the purchase is something you do not approve.

Easy Transfers

You can contribute to your account via direct deposit of your wages, a debit card, ACH, or even Apple Pay. However, there are a few limitations on the amount you can deposit.

- For ACH, you must deposit at least $20.00 for the initial transaction and $1.00 after that.

- For a direct deposit, the minimum contribution is $1.00. And for your debit card, every time you transfer funds there is a minimum requirement of $20.00 per transfer of funds.

Usage Limitations for Your Children

You can limit and determine stores and merchants you do not want your children using. Maybe you don’t want them shopping on Amazon, you can decline all purchases from Amazon.

You can also add money to the “Spend Anywhere” section in the app. This allows your kids to spend that dollar amount at any location they choose.

Customizable Alerts

Greenlight will send you a notification when your child spends money or would like to spend money.

You can also get notifications when balances are low or charges are declined. You can choose how you want to set up your account.

Ability to Add Multiple Children

You can add up to five children per account. I have all three of mine on the account.

This app could also be used by grandparents if they wanted to ocassionally give them money.

Greenlight Customer Service

Greenlight is a paid service and so for users they have excellent customer service. You can reach their support center through the app.

If you can’t find an answer there you can email them at support@greenlight.com, text them at 404-974-3024, or call them at 888-483-2645.

Greenlight Invest and Greenlight Max

In an attempt to offer more service and create some differentiation, Greenlight has introduced an Invest plan and a Max plan. Let’s quickly look at each.

Greenlight Invest is simply the base plan, plus access to their investing platform. With their investing platform, your kids can invest in stocks (including fractional shares with as little as $1) and exchange traded funds (EFTs).

The platform goes to great lenghts to educate your kids on investing as well, which includes tutorials and stock info. As a bonus, you can participate in Greenlight Invest from your parent wallet. See pricing info below.

Greenlight Max includes everything in the Invest plan, plus 1% cashback on spending, a cooler-looking card, and some added protections (ID theft, cell phone, and purchase protection). See pricing info below.

Security and Costs for Greenlight

Many of Greenlight’s features are similar to a credit card. Which means that sometimes merchants will hold extra funds to make sure you can cover the transaction.

For example, if you are staying at a hotel they will charge your card a deposit in case of incidentals. This extra hold on the account could cause the card to be declined.

Unlike a credit card, however, Greenlight offers a Personal Identification Number (PIN) for its card. This feature allows you protection for you and your kids against identify theft.

In case your card is lost or stolen you can put a freeze on the account until the situation is resolved. You can do this straight from the app on your phone.

In addition, upon verification of your identity, your card account is FDIC-insured. The FDIC insures deposits up to $250,000.

Greenlight costs $4.99 per month for the basic membership plan, but there is a free trial for the first month. There are no fees for transferring money to the app or within the app.

Greenlight has additional memberships plans:

Greenlight + Invest is $7.98/mo

Greenlight Max is $9.98/mo

Greenlight vs FamZoo vs Current vs GoHenry

There are a ton of competing apps available to help you and your kids manage money together. We have a full review of FamZoo (which we now use), which you can read. In the future we hope to have full review of these others. But in the meantime here are the basics for you to check out:

What You Need to Know Before Signing Up for Greenlight

You are completely responsible for your child’s card use. If you do not closely monitor the account, the card may not serve its purpose.

Remember this is a tool to help your children with financial literacy and build strong financial habits. Don’t let it get out of hand or allow them to purchase anything they want. Use this tool for guidance.

Card Replacement Cost

Since this is not a traditional credit card, there are fees for lost or stolen cards. You will receive your first replacement free. Every replacement after that will be an additional $3.50.

Age Restrictions

This service is aimed at children ages 8-18. There is no age restriction on card usage, but a child must be 13 in order to download the app on their phone.

Credit Card Restrictions

Transferring money to your Greenlight account from a credit card will be seen as a cash advance by your credit card company This will likely incur high fees and interest on your credit card account.

If you are used to using your credit card for everything this may not be the tool for you.

How I Used Greenlight

My main goal with Greenlight was to get my children using money as much as possible, within limits. When you use money, you make mistakes, you feel emotions, you have experiences.

This is what I want for my kids.

I’m not trying to shield them from money, or overly-protect them. I want them to experience the pain of being broke, the sadness in regretting a purchase when they get home, the joy in savings and giving, and the sense of accomplishment when they’ve reached a goal.

I want them to experience these things NOW, not when they are 18, 20, or worse, 24-25 like I did.

Here’s exactly how my wife and I used Greenlight with our three children (ages 8, 11, and 13).

Funding Their Accounts

I gave my kids $1 per year for their age. So, my 12-year-old got $12 a week, my 10-year-old got $10/week, and my 7-year-old got $7 per week.

This amount is like a salary/allowance. It is NOT tied to any chores, behavior, grades, etc. They get the weekly pay, rain or shine.

(Side note: We do have our kids to do chores and help out around the house. However, there is no payment associated with it)

They each told me how much of the weekly pay they wanted to put towards savings and giving and I use the app to set this up. I check in with them a couple of times a year to make sure they are still happy with their decision.

Using the App and Card

My kids don’t have phones yet so they use the app on my phone when they need to check their balance or make a transfer between bucket accounts.

My wife holds their debit cards in her purse. 99% of the time she’s the one with them when they are out and about, so it works best.

Spending Rules

They were expected to use their cards to buy the following:

Toys, games, treats, souvenirs, gifts for family/friends, book fair (after the first 2 books), extras, etc. Eventually, the card will be used to buy gas for their vehicles, cell phone service, and many other optional expenses that they’ll enjoy if they want.

Don’t worry, we still get them things for their birthday/Christmas, snacks when the whole family is partaking, and more than enough of the necessities. But they are responsible for everything extra.

What Else?

At the end of the year, when my wife and I looked at our annual giving, we had our kids review their Greenlight giving account and do their giving – moving the money from Greenlight into an actual charity.

That’s about it.

Is Greenlight Worth the Cost?

Financial literacy is important. You are responsible for teaching your children strong financial habits and guiding them toward a successful financial future. It may take a little time and effort – and in this case, $4.99/mo – but it will truly pay off.

Read about how we’re using FamZoo instead of Greenlight.